Fox + Roku: A Brilliant Pivot from the Cable Bundle to the Living Room

An Accrued Interest First-Reaction Deep Dive on the $22B Fox / Roku Merger

Accrued Interest TLDR:I am initiating coverage on the pro forma Fox + Roku entity with an Outperform rating, and the market is wrong to have sold Fox down ~23% on the announcement. Roku ($ROKU) agreed to be acquired by Fox Corporation ($FOXA) at $160 per share — a $25B equity value, $22B enterprise value, 60% cash and 40% stock. The strategic logic is the cleanest piece of capital allocation I have seen from a legacy media incumbent in years. In 2019, the Murdochs sold their entertainment cable channels to Disney at very close to the top of the peak-TV bubble. In 2026, they are using that cash and balance sheet capacity to buy the #1 connected-TV operating system in the United States — at a moment when CTV ad share is racing past 40% of the total TV ad pie. What Fox is buying here is the front door to the living room — distribution, not another melting linear bundle. With Roku’s 44% share of U.S. CTV viewing hours, 100M+ global streaming households, and 100% authenticated first-party data, the combined entity becomes the third-largest player in U.S. television by share of viewing. Fox just stopped being a content company haggling with cable operators and became a distributor — full stop. The sell-off on Fox stock is a gift.

Please subscribe for free to read the rest of this Accrued Interest deep dive on FOX/ROKU.

Introduction: The Best Strategic Move in Legacy Media in Years

Yesterday morning, Roku announced it had entered into a definitive agreement to be acquired by Fox Corporation. I said in my May 28th update (Monetizing the Habit: Meta’s Enterprise Land Grab and Roku’s Living-Room Billboard) that I wanted to expand my coverage of Roku going forward. Waking up Monday to this M&A news was a pleasant surprise, to say the least.

There is a lot to be said about the new Fox + Roku. I wanted to give all of my subscribers one of my deep dives where I walk through the entire investor relations merger deck and translate what the executives are really trying to say. In my prior corporate life, I have a lot of experience building these investor decks from start to finish — drafting them, editing them, and working hand in hand with senior executives at multi-billion-dollar media companies to get the story right. So in today’s piece, we are going to do a page-by-page teardown and give you the full picture: what management said, what they actually meant, and what this means for both companies.

I am going to do the opposite of burying the lede. I think this combination is a brilliant strategic move for Fox.

In my prior coverage, I have repeatedly highlighted that investors have underestimated just how savvy the executives at Fox Corporation have been at navigating the switch from linear to streaming over the last 10 years. Throughout my extensive coverage of the Paramount-Skydance and Warner Bros. Discovery storylines — including “Dead on Arrival: 8 Reasons the Paramount-WBD Merger Will Fail“ — I have explained many times why I considered Fox to be the smartest of the legacy media providers. The decision in 2019 to sell the majority of their entertainment cable channels and the bulk of 21st Century Fox to Disney — cashing out at very close to the top of the peak-TV bubble — is, with the benefit of hindsight, one of the great pieces of strategic timing of the past two decades. Disney has been carrying that hangover ever since. (For more on that, see my December piece, “Why Disney Stock Will Underperform in 2026.”)

Fast forward to 2026, and Fox is now flipping the script. By acquiring Roku, the company is moving from being a content supplier negotiating with local cable companies like Comcast and Charter, to being one of the largest and most powerful distributors of digital video services in the United States. Instead of fighting over carriage and channel placement on someone else’s plumbing, Fox will now have a direct seat at the table — and a say — in how every other major streaming service is consumed by the tens of millions of Americans who use Roku as the home screen for their entertainment.

In short: this deal allows Fox to finally break free of the cable bundle once and for all. They will be able to go over-the-top — a phrase you don’t hear as often anymore — more than they ever have before.

For new subscribers, in the past I have had strong demand from readers for these detailed breakdowns of investor merger decks. For reference, you can find my prior teardowns of the Starz, Versant Media, Nexstar, and Warner Bros. Discovery decks in the Accrued Interest archives. Without further ado, let’s get into the Fox + Roku deck that management walked through during yesterday morning’s conference call.

One small editor’s note before we begin: I am going to start with the strategy and operations slides, and save the transaction overview from Slide 3 and the sources & uses from Slide 14 for the end — it makes more sense to discuss the financial mechanics together, after we have established why this deal makes sense strategically.

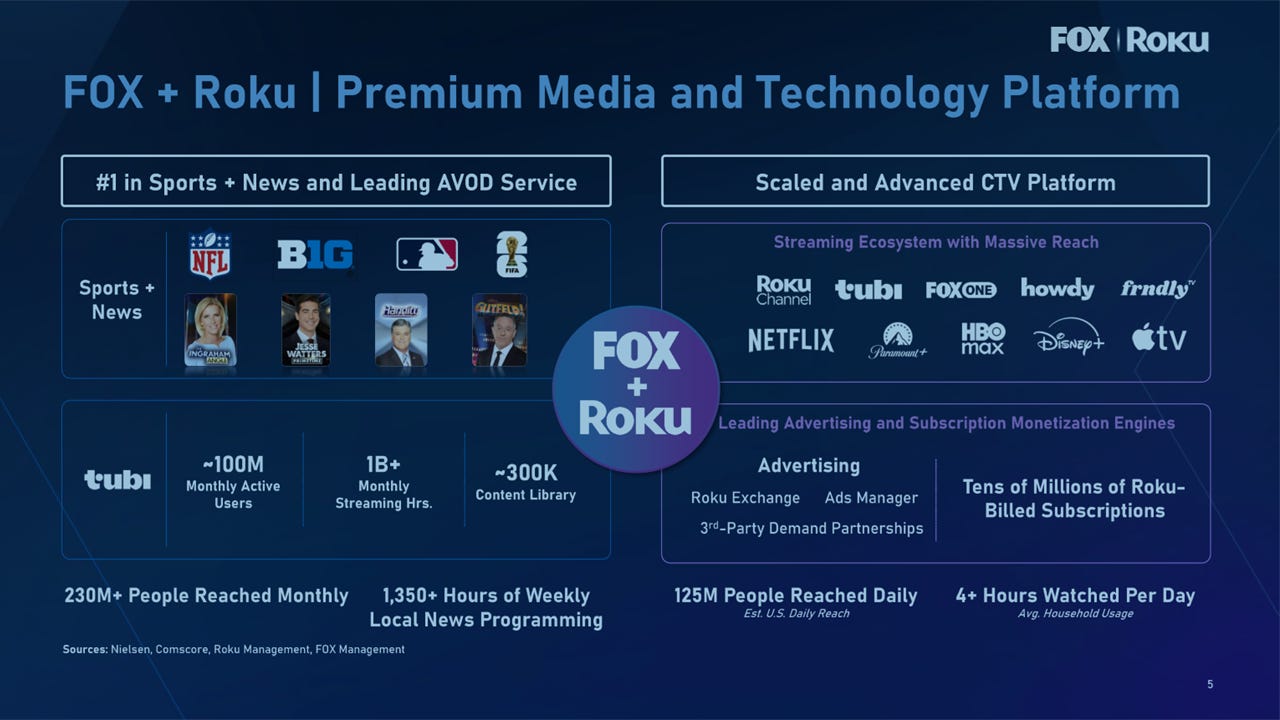

Slide 5: Fox + Roku Combines #1 Sports and News With the #1 CTV Platform — and Quietly Frees Fox From the Cable Bundle

Slide 5 is, in my opinion, the single best page in the deck for understanding what is actually being assembled here. The left side lays out what Fox brings to the table — sports, news, and the Tubi free streaming service. The right side lays out what Roku brings — a scaled, advanced CTV platform with massive reach and the monetization engines underneath it.

Fox is leaning, understandably, on its expertise in live sports and news. The news side of that story is the strongest piece. As I have argued before, Fox News is the undisputed leader in cable news, dominating the category with somewhere around a 60% share by some estimates. I laid this out in detail in my deep dive on Fox last summer: “I consider Fox News to be the most valuable network in the U.S., as it has the audience size and profitability comparable to a Big 4 broadcast network (ABC, CBS, NBC). It is a must-buy for advertisers.” That has not changed.

But there is one critical fact about Fox that the slide does not spell out — and which I want my readers to keep in mind, because it is fundamental to why this deal works. Fox owns its O&O (owned-and-operated) stations in the biggest U.S. television markets. By my estimate, through Fox’s O&O footprint, the company can connect nearly 40% of U.S. households directly, without going through a third-party affiliate group like Nexstar or Sinclair. As cord-cutting continues to accelerate, that O&O footprint becomes more valuable, not less. Why? Because Fox will eventually be able to push local-market broadcast signals from its O&O stations directly onto Roku — to homes that no longer have cable. That is a quiet, structural advantage that I do not think the sell-side is giving Fox enough credit for. It is one more way this deal lets Fox break out of the cable bundle for good.

The right side of the slide gets at the heart of why Fox is paying $22 billion. Roku gives Fox a seat at the table — and a meaningful amount of control over, as the slide puts it perfectly, “a streaming ecosystem with massive reach.” And I take that line at face value, because Roku genuinely is the front door to streaming entertainment for a huge chunk of American TV viewers. Whether you watch Netflix, Disney+, Max, Paramount+, or Apple TV+ — there is a very high probability that you start that journey by turning on a Roku-powered television.

Roku is also not exaggerating when the slide says it has “leading advertising and subscription monetization engines.” Roku serves as both gatekeeper and toll collector. Along with Amazon Prime Video channels, it is one of the top ways Americans have been re-bundling their digital subscription services — a theme I have been hammering for over a year now. Roku has stickiness because it offers a simple convenience that the cable companies used to offer: putting all of your streaming services onto a single bill, with a single password and a single interface. That is, frankly, an underrated business.

Ten years ago, if you were a basic cable network, reaching ~100 million households was the gold standard. Today in 2026, with somewhere around 60 million households still subscribing to traditional pay TV, Roku can reasonably claim to help you get to functional full distribution in the United States. That is the asset Fox just bought.

Before we get to numbers and financials, I want to underline what should already be obvious from this slide alone. Strategically, this is an incredibly smart and forward-thinking deal for Fox. This is exactly the type of move you need to make if you want to leapfrog yourself from a legacy programmer into a major streaming player.

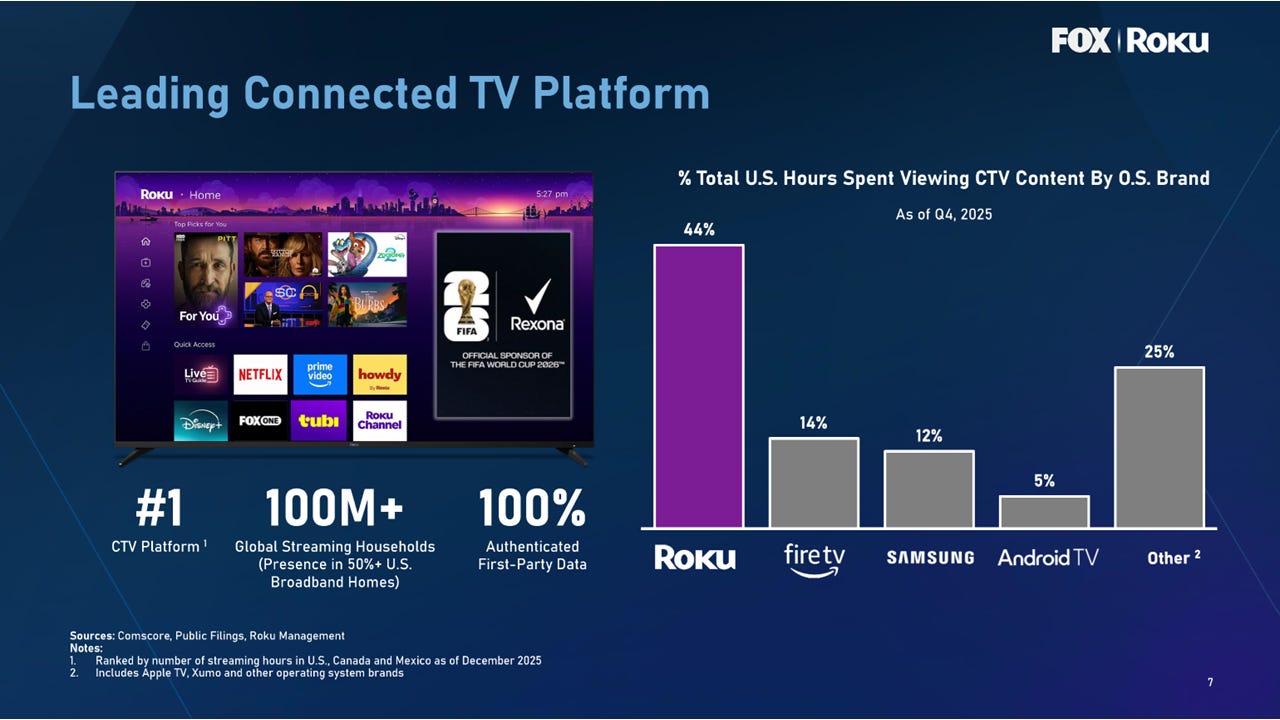

Slide 7: Roku Isn’t Just the #1 CTV Operating System — At 44% Share, It Is Roughly 3x Its Nearest Competitor

Slide 7 drives home just how dominant Roku is as the gateway to television viewing in America. The headline numbers — #1 CTV platform, 100M+ global streaming households, 100% authenticated first-party data — are not marketing fluff. They are real.

A few details I want to flag for readers, because they matter for how Fox will be able to integrate this asset:

First, the 100 million streaming households number is heavily skewed toward North America. That geographic concentration is a feature for Fox, not a flaw. Roku does not have a meaningful presence in Europe, Asia, or Latin America. Roku sticks and Roku TVs are predominantly sold in the United States, Canada, and Mexico while its newer expansions into Europe (UK) and Latin America (such as Brazil) remain in the early stages of building scale.

Fox-branded networks are also primarily U.S.-focused entities. Fox is not paying up here for international subscribers that would dilute the bottom line. The fit is clean: a U.S.-focused content portfolio acquiring a U.S.-focused distribution platform, in the most profitable media market in the world. That alignment alone is worth real money in synergy terms.

Second, the bar chart on the right side of the slide is the single most important visual in the entire deck. It shows the percentage of total U.S. hours spent viewing CTV content by operating system brand, as of Q4 2025. The numbers are: Roku at 44%, Amazon Fire TV at 14%, Samsung at 12%, Google’s Android TV at 5%, and all others (Apple TV, Xumo, Vizio, etc.) combined at 25%.

Read that again. Roku’s share of U.S. CTV viewing hours is roughly three times its closest competitor. And critically, Roku has built that dominance against trillion-dollar competitors (Amazon, Google) who have effectively unlimited capital and have been trying to take the living room for over a decade.

This stat is the entire reason this deal exists. The moment the merger closes, Fox vaults itself into first place in the most important real-estate category in American television. As more media companies push more content into streaming, Fox will now have a meaningful say in how the market evolves. That is a structural advantage that money, frankly, cannot easily replicate.

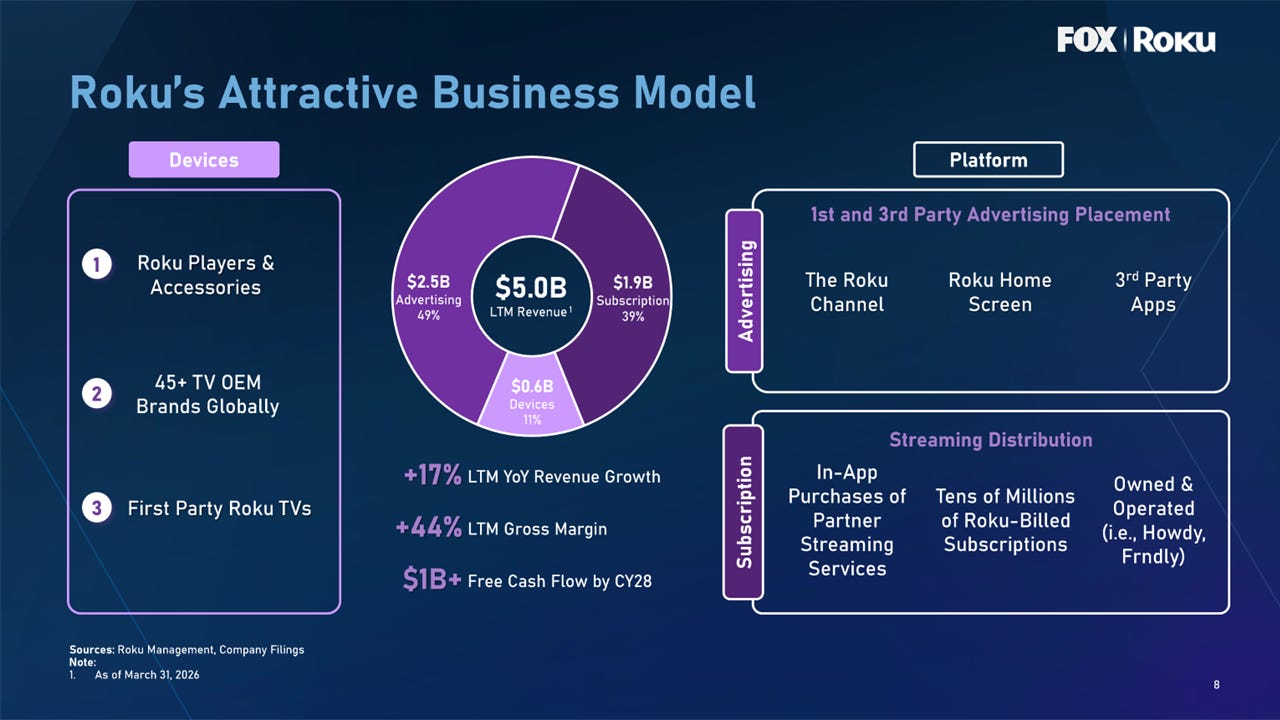

Slide 8: Ignore the Streaming Sticks — The Real Roku Business Is a $4.4B High-Margin Platform Engine

Slide 8 is a great overview for readers who are not deeply familiar with how Roku actually makes money. In my May 28th update, “Monetizing the Habit: Meta’s Enterprise Land Grab and Roku’s Living-Room Billboard,” I explained why I was dropping coverage of FuboTV (the sub-scale aggregator trap) and reallocating that bandwidth toward Roku — the structurally superior, pure-play “front door” to the living room. I never got the chance to publish a full initiating coverage piece on Roku. Slide 8 will do the job nicely.

Let me say this up front because it is counterintuitive: Roku does not make money on streaming sticks. The vast majority of the profitability comes from its Platform segment — advertising and subscriptions. Here is how to think about it. All numbers below are on an LTM basis as of Q1 2026.

Total LTM revenue: $4.965 billion, up +18.7% year-over-year. Substantially all of that revenue is generated in North America. This is not an international play. It is squarely about the United States — which, as I keep reminding readers, is by far the most profitable media market in the world.

For the purposes of this article, I am going to set the Devices segment aside. That is where Roku books the revenue from those ubiquitous streaming sticks. Devices are only about 11% of total revenue, and it is even less than that as a share of profit — because it is a consistent loss leader. In Q1 2026, Devices brought in $117.6M but sustained a gross loss of $19.1M, a negative 16.3% gross margin. For full-year 2025, the Devices segment ran at roughly a negative 14% gross margin.

And that loss is entirely by design. Roku is intentionally subsidizing hardware to drive maximum user acquisition into the Platform ecosystem. And here is the part CEO Anthony Wood made clear on yesterday’s call that I want to highlight, because it is not in most analyst notes: Roku has a compounding engineering advantage that makes that loss-leader strategy sustainable. Roku is the only major CTV platform with an operating system built from the ground up specifically for streaming — not a ported version of HTML, not a repurposed mobile OS. As a result, Roku’s OS uses significantly less memory than competitors. In a market where memory prices are spiking — which they are — that translates directly into a manufacturing cost advantage that compounds. Every TV OEM in the world that wants to ship a cheap, profitable connected TV has a structural reason to choose Roku’s OS over Android TV or Fire TV.

Now to the part that actually matters. The Platform segment is roughly $4.4B of LTM revenue, splitting out as:

Advertising: ~$2.5B (49% of total revenue), +19.2% YoY

Subscription: ~$1.9B (39% of total revenue), +26.8% YoY

Roku’s LTM Platform gross margin is approximately 44%. LTM Adjusted EBITDA was $512.9M, up +201% YoY — and Q1 2026 alone delivered $148.4M of Adjusted EBITDA, up +165% YoY. That is operating leverage finally kicking into gear.

This is the part of the business that matters. What Fox is buying with this deal is an advertising-and-subscription monetization engine, with a 100M+ household funnel feeding into it, that just hit the inflection point on EBITDA.

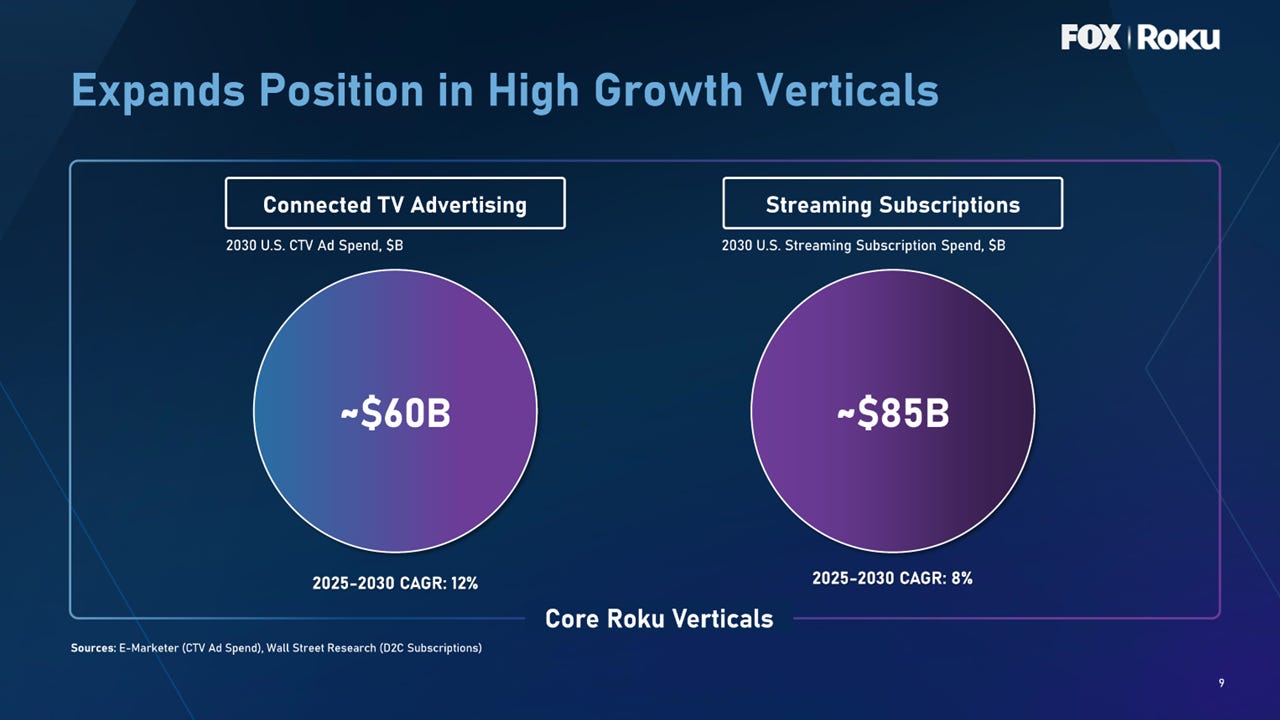

Slide 9: The Combined TAM Is Roughly $145 Billion — Fox Isn’t Buying a Company, It Is Buying a Lane

Slide 9 lays out the total addressable market for Roku’s two core verticals: Connected TV Advertising and Subscriptions. Management did a good job here, and I want to put real pen to paper on the numbers because, when investors think about media TAMs, they tend to gloss over them.

CTV advertising is currently a ~$60 billion market, projected to grow at roughly a 12% CAGR through 2030. You can quibble with the precise forecast, but the directional trend is undeniable: marketers are aggressively shifting linear TV dollars off of old-school broadcast and cable, and into the digital/CTV bucket. CTV is the very first place those budgets go.

Subscriptions is an even bigger bucket, at roughly $85 billion, projected to grow at a slower but still healthy ~8% CAGR. You can quibble with that estimate too, but the thing I know with high confidence about subscriptions is that they are higher-margin than advertising, stickier than advertising, and importantly, recurring — most customers are billed monthly, and inertia is real.

As much as American consumers complained about the cable bundle, what was undeniable was that aggregating a lot of little subscriptions into one bill worked — it reduced churn, simplified the consumer experience, and protected pricing power. Re-bundling of streaming services is the single most important consumer trend in media in 2026, and Roku is one of the two or three companies most directly positioned to benefit from it (Amazon Prime Video Channels is the other obvious one).

One concern I want to address head-on. Some readers will ask: now that Roku is owned by Fox, won’t competitors like Disney, Netflix, and Warner Bros. Discovery pull back from the Roku platform? My answer is no. Despite the intense content competition, I do not expect any of the major streaming providers to pull back on their relationship with Roku just because Fox is now its corporate parent. Why? Because consumers vote with their wallets every day, and they have already voted for Roku as their home screen. Netflix, Disney+, and Max cannot afford to walk away from Roku’s funnel any more than Roku can afford to alienate them. That mutual dependence — what management correctly called the “Switzerland” model on the call — is durable. Lachlan Murdoch was unequivocal yesterday that Roku will remain an “open, partner-friendly platform.” I believe him, and not because I am taking him on faith — I believe him because the economic incentive on both sides points in the same direction. Roku is too valuable to its partners as a neutral distributor for Fox to compromise it. Fox will make far more money keeping it open than trying to play favorites.

There is one more reason here that I want to flag, because it goes back to the 2019 Disney deal I mentioned earlier. When Fox sold the majority of 21st Century Fox to Disney, they also sold the majority of their TV and film production studios with it. That means Fox today is not a meaningful original-content creator. They are primarily a sports, news, and broadcast distribution business — plus Tubi as a FAST aggregator. The Fox + Roku combined entity will always need third-party content from Netflix, Disney, Warner Bros. Discovery, Paramount, Amazon, and the rest to fill out its app catalog and keep viewers engaged. This structural reality reinforces neutrality. Fox has every incentive to be an honest broker.

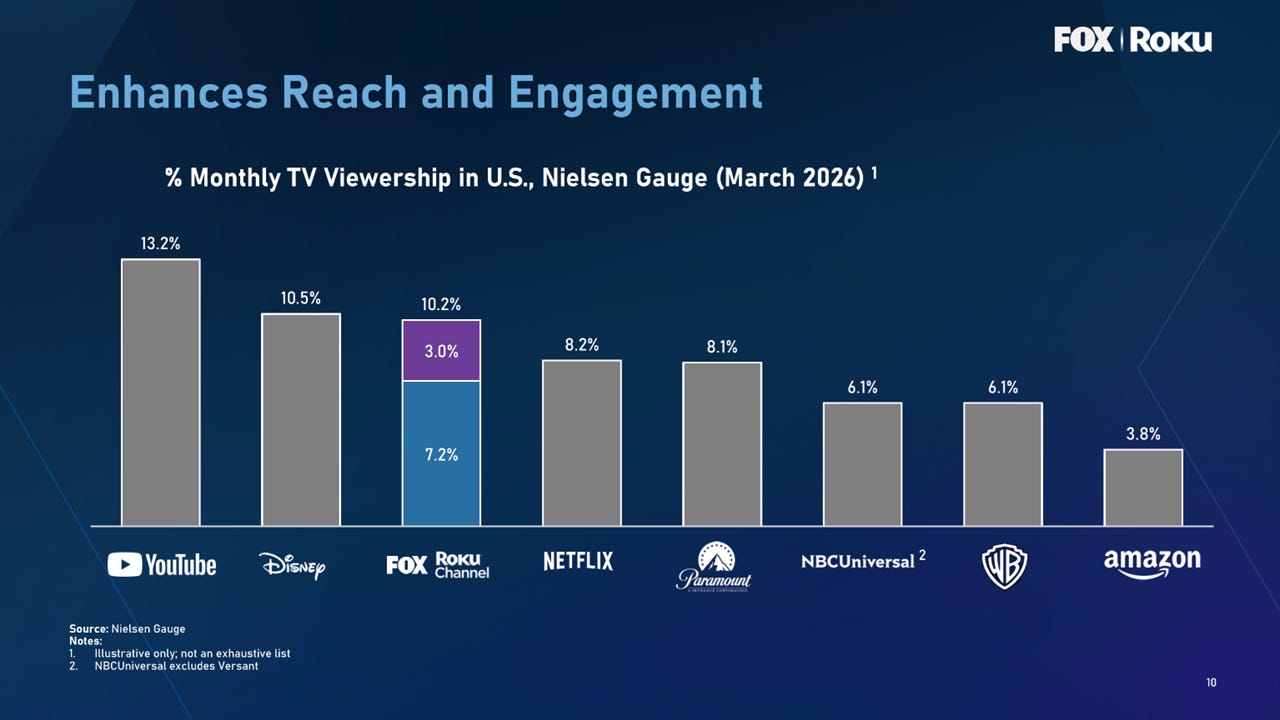

Slide 10: Combine Fox With the Roku Channel and Fox Just Leapfrogged Disney in Total TV Viewership

For long-time readers of Accrued Interest, you already know that for over a year now I have been consistently reporting on the monthly market-share changes in TV viewership using Nielsen’s Gauge report. (See my monthly snapshots, including the most recent one, “Media Stock Insights from Nielsen’s Jan-26 TV Snapshot.”) The thesis has been consistent: every single month, YouTube, Netflix, and the FAST/CTV platforms take share from linear broadcast and cable, and that trend is structural, not cyclical.

Slide 10 visualizes that point as of March 2026. Some of the headline numbers from that chart:

YouTube: ~13.2% of total TV viewing

Disney (including linear ABC, ESPN, etc., plus Disney+): ~10.5%

Fox (broadcast + cable + Tubi): ~7.2%

The Roku Channel: ~3.0%

You can argue with the precise percentages — every Nielsen methodology change moves them around — but the trend is the only thing that matters.

Here is the bit I want every reader to pause on: combine Fox (7.2%) with the Roku Channel (3.0%) and the pro forma share is ~10.2%, almost exactly equal to all of Disney.

I want to dwell on that for a moment, because the symbolism matters. Back in 2019, Fox sold the majority of its entertainment cable channels and the bulk of 21st Century Fox to Disney — a deal that, at the time, Wall Street treated as a coup for Iger and a defeat for the Murdochs. Five years later, the consensus on that deal has flipped completely. As I wrote in “Why Disney Stock Will Underperform in 2026”: “The acquisition of Fox is widely regarded as a disappointment, if not a complete failure. It is noteworthy that what was once Disney’s largest acquisition is no longer considered the strongest aspect of its investment strategy, merely five years later.” Disney has spent six years digesting that deal and trying to grow into the multiple they paid for it. They have not.

Fox, meanwhile, took the cash, kept the most defensive parts of their portfolio (Fox News, Fox Sports, the O&O broadcast stations, Tubi), waited patiently, and is now using the balance sheet to leapfrog Disney in total share of TV viewing. Embedded in that 7.2% Fox number is Tubi — a FAST service whose impact I have been highlighting in my monthly TV viewing updates for over a year — which has been quietly building share while no one was watching.

The most important point on this slide is not the precise number. It is that Fox is coming away from this deal with massive scale in TV viewership — and massive scale is exactly what advertisers want to see when they allocate budgets at the upfronts.

Cord-cutting is not going away. It is still accelerating. But I can say with confidence that Fox has not only secured itself a life raft — they have bought themselves a battleship, and they are now a commanding presence in the streaming-distribution waters.

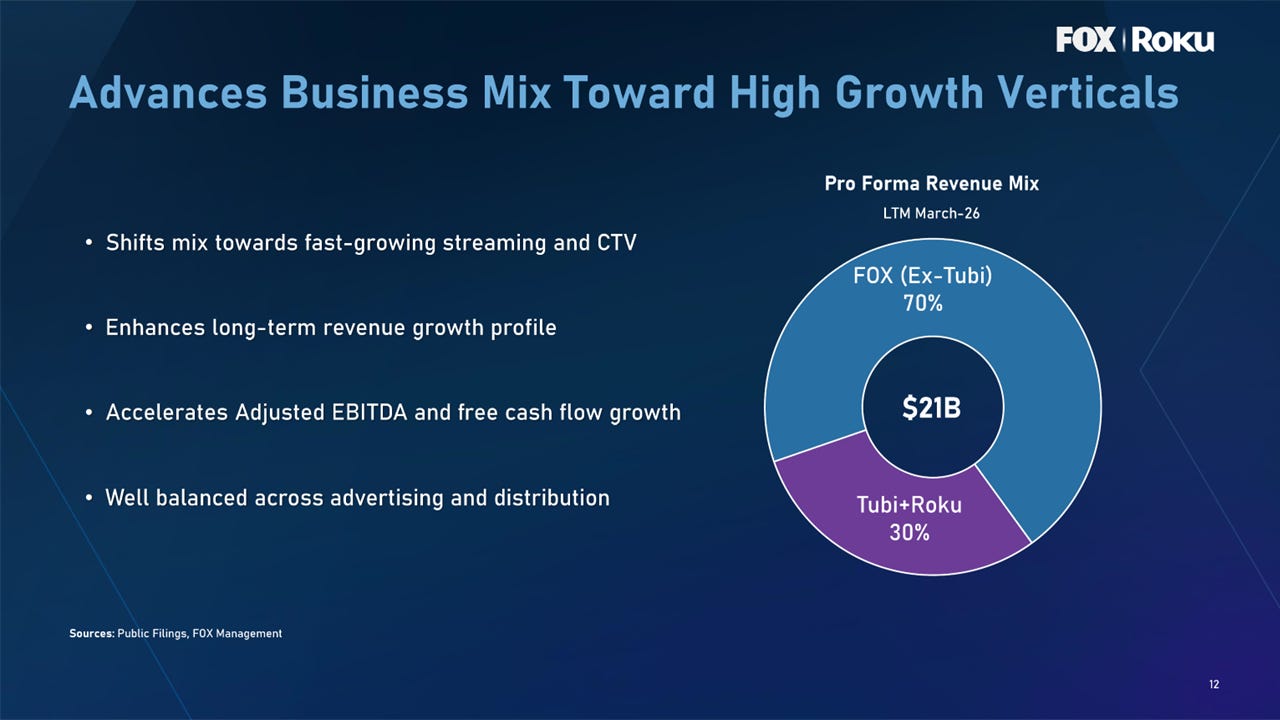

Slide 12: The 70/30 Pro Forma Revenue Mix Is the Cleanest Picture of Fox’s Strategic Pivot

Slide 12 makes the strategic pivot explicit. The pro forma revenue mix on an LTM basis is going to be approximately 70% Fox (ex-Tubi) and 30% Roku + Tubi. The total combined revenue base is approximately $21B.

I want to flag something that I think management got exactly right on this chart: they combined Tubi and Roku into a single 30% wedge. That is the correct way to think about it. Over the last several years, Tubi has been growing market share and revenue at a rapid clip, and Fox leadership has been telling the Street that Tubi is on a credible path to sustained EBITDA profitability as it scales. Combining Tubi with Roku — particularly the Roku Channel, which is its closest analog — creates a multi-brand FAST ecosystem that triples combined reach while maintaining two distinct audience pools. (As Lachlan noted on the call, Tubi and the Roku Channel have only about a one-third audience overlap, despite both being free, ad-supported services. They are genuinely complementary.)

I am incredibly excited about the possibilities for Tubi combined with the distribution power of the Roku platform and the Roku Channel. The deck claims this deal will “accelerate adjusted EBITDA and free cash flow growth.” That is the math, plain and simple.

Before we get to valuation — and I want to be clear that I am going to come back to valuation in a follow-up piece — I will say without hesitation: the combined Fox + Roku is a meaningfully stronger, healthier enterprise than either company was independently.

In my piece “The Pokémon Theory of Media Investing,” I argued that in order to beat the market in TMT stocks, you need to focus less on spreadsheet math and think harder about what really moves the needle strategically. This deal is a Pokémon-theory deal in the purest sense. Fox is evolving. Roku is evolving. The combined entity is in a different competitive category than either parent.

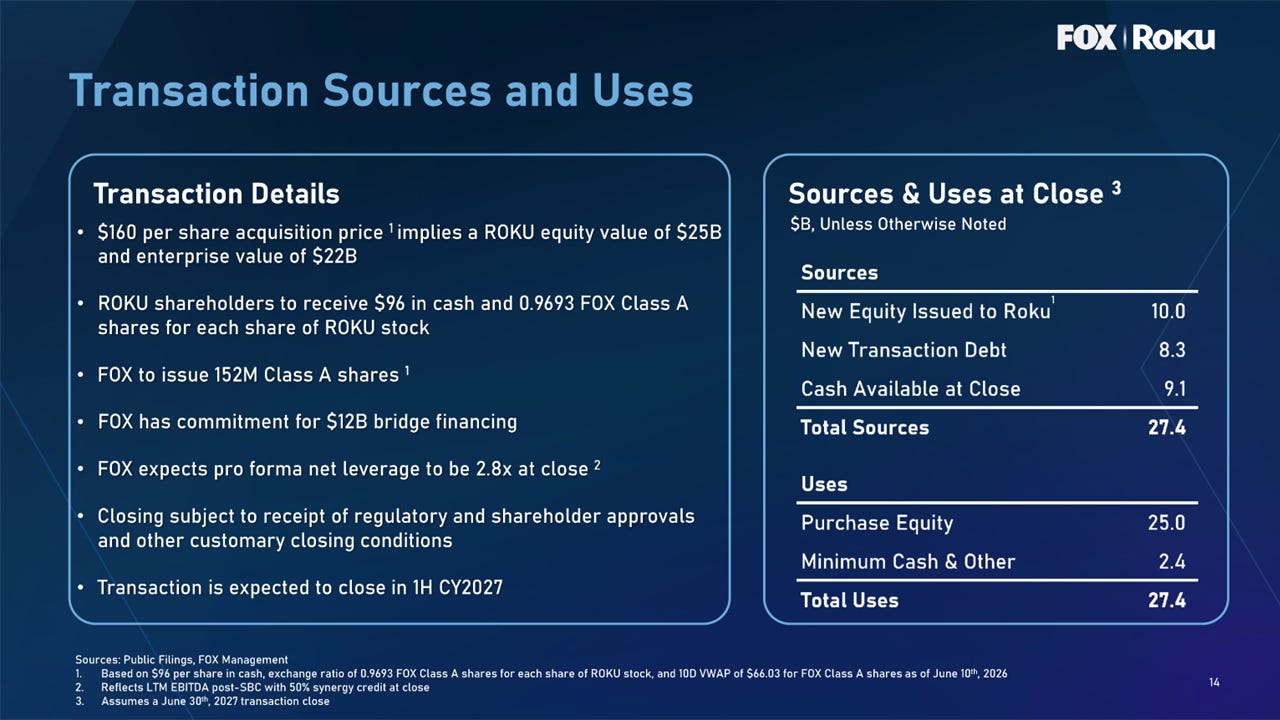

Slide 14: The Market Sold Fox Down 23%, and I Fundamentally Disagree

Let me now turn to the financial mechanics of the deal, which the deck lays out on Slide 14 (Transaction Sources and Uses). And let me start by acknowledging something that I would be remiss to ignore: the market has, as it often does, punished the acquirer. As of the time I am writing this, Fox stock is at about $52 per share — down roughly 23% over the last five days from approximately $68 on June 11th. That is a brutal initial reaction.

Here are the deal terms, in plain English:

Purchase price: $160 per Roku share, implying an equity value of ~$25B and an enterprise value of ~$22B.

Consideration mix: 60% cash ($96/share) and 40% stock (0.9693 FOXA shares per Roku share). The stock portion is anchored to a $66.03 10-day VWAP for FOXA Class A shares as of June 10th.

Pro forma ownership: Fox shareholders own ~73% of the combined company; Roku shareholders own ~27%.

Financing: Approximately $8B in new debt, supported by a $12B bridge commitment, plus approximately $7B of pro forma combined balance-sheet cash.

Leverage: Net leverage at close is projected at 2.8x pro forma LTM EBITDA (incorporating a 50% credit for synergies).

Synergies: $400M of expected run-rate cost synergies.

Accretion: Expected to be free cash flow per share accretive within two years of closing, which is targeted for the first half of calendar 2027.

I want to come back in a future piece with a full valuation of the combined entity, because the work to do there is substantial and deserves its own deep dive. But I will say this much in the meantime: I fundamentally disagree with the market selling Fox down -23% in 5 days.

Why? A few reasons. First, the 40% equity component of the deal does mean meaningful share issuance — approximately 152 million FOXA Class A shares — and that always weighs on the acquirer’s stock initially. That is a mechanical, technical sell-off, not a strategic one. Second, some of the concerns I have seen from the sell-side relate to Roku’s low-margin hardware business introducing operational complexity to Fox. I addressed that on Slide 8 — the hardware business is a deliberate loss leader supported by a genuine engineering edge, and the Platform business is what’s actually accretive. Third, the deal preserves investment-grade balance-sheet status, with leverage at a manageable 2.8x, and Fox has explicitly committed to continuing its capital return program (buybacks and dividends).

When I run my mental sanity check, what I see is a balance sheet that can absorb this, a synergy target that is reasonable rather than aspirational, and a strategic re-positioning that fundamentally changes Fox’s long-term growth profile. The market is pricing the dilution. The market is not yet pricing the optionality. That is the spread, and that is where I think there is real opportunity in Fox stock at $52. More to come in a dedicated valuation piece.

Q&A: Three Themes From the Conference Call That Investors Should Pay Attention To

The Q&A portion of yesterday’s M&A call clarified several investor concerns. I want to highlight three themes I thought were particularly important:

1. The Real Driver of the Deal Is the CTV Ad Migration. Management noted on the call that CTV’s share of total TV ad spend has grown from 25% to 41% in recent years, tracking closely with streaming capturing approximately 50% of total U.S. domestic TV viewing. That migration is permanent, not cyclical. Fox is acquiring the infrastructure — Roku’s home screen, Roku Ads Manager, the Roku Exchange, the authenticated first-party data — to capture those ad dollars as they continue to migrate. This is the single most important durable trend in television, and Fox has just bought the dominant pick-and-shovel exposure to it.

2. The “Switzerland” Model is Sacred — Fox Will Not Throttle Third-Party Apps. Multiple analysts probed whether Fox’s ownership would compromise Roku’s neutrality. Both Lachlan Murdoch and Anthony Wood emphasized — unequivocally — that Roku will remain an “open, partner-friendly platform.” Lachlan was specific: Roku already partners with YouTube TV, with Comcast, and with every major streamer. “That doesn’t change.” The strategy here is to use Roku’s rich first-party data and targeting capabilities to increase the monetization of all premium content across the board — including, but explicitly not at the expense of, third-party apps like Netflix or Disney+. As I noted earlier, the economic incentive on both sides points in the same direction. I take management at their word here.

3. Scale Is About Footprint, Not Sports-Rights Bidding Wars. Several analysts asked whether Fox would use Roku’s scale to wage a more aggressive bidding war for live sports rights against Big Tech. The answer was a clear no. Fox is not planning to outbid Amazon, YouTube, or Netflix for the next NFL package or NBA package. Scale here is defined by footprint, not by content acquisition. The deal makes Fox the third-largest player in U.S. TV viewing — and that funnel will be used primarily to cross-promote Fox’s high-margin digital assets like Fox One, Fox Nation, and Tubi, not to chase ever-more-expensive sports rights. I think this is exactly the right discipline. The mistake the rest of legacy media has been making for five years is paying up for sports as an existential moat. Fox is doing the opposite — using its existing sports franchises as a moat, and putting the new capital into distribution.

Conclusion: Fox Has Bought Its Battleship — Outperform

Yesterday’s announcement is, in my view, a transformational moment for Fox. By acquiring the #1 CTV operating system in the United States, Fox is making a clean, decisive pivot away from the eroding linear cable bundle toward the future of streaming distribution. The deal solves the distribution dilemma for Tubi, gives Fox a commanding position in CTV advertising, and brings 100% authenticated first-party data on more than 100 million streaming households inside the tent.

Could Roku have continued to thrive as a standalone company? Absolutely — Q1 2026 results showed Platform revenue accelerating to a 28% YoY growth rate and Adjusted EBITDA up 165% YoY. But scale matters in advertising, and partnering with Fox lets Roku move faster and smarter than it could on its own.

For Fox shareholders, this is what good capital allocation looks like in legacy media. The Murdochs cashed out of linear cable at the top of the bubble in 2019. They are deploying that capital into a digital distribution platform at the moment CTV is taking 41% of TV ad spend and rising. They have sold high and they are buying right. That is execution.

I am initiating coverage on the pro forma Fox + Roku entity with an Outperform rating. I disagree with the market’s 23% sell-off in Fox stock on the announcement, and I think the current price of approximately $52 per share represents a meaningful long-term opportunity for patient investors. A dedicated valuation deep dive will follow in the coming weeks.

For now, my bottom line is simple. Cord-cutting is here to stay. The cable bundle is not coming back. The future of television is the home screen — and Fox just bought it.

Relevant tickers: FOX 0.00%↑, FOXA 0.00%↑, ROKU 0.00%↑, DIS 0.00%↑, NFLX 0.00%↑, GOOGL 0.00%↑, AMZN 0.00%↑

— Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.

Part 2 is live of my Roku deep dive series! 🚢

Part 1 (above) made the strategic case for why Fox bought Roku. Part 2 goes under the hood 👉 Roku is the chokepoint of US streaming — ~44% of connected-TV viewing flows through it — and for a decade it barely charged a toll. 🚦

I break down the 3 monetization levers Roku is finally pulling, the data asset I think helps justify the $22B price tag, and the Q1 numbers showing the payoff is just getting started (Platform +28%, EBITDA +165% 📈).

Give it a read 👇 https://www.accruedint.com/p/the-strait-of-roku-how-fox-seized

Interesting read and completely the opposite of my first gut reaction.

My thinking was that "Old legacy player buying the newer digital upstart" never works, because they either 1) massively overpay or 2) completely mismanage the new digital business.

Considering the growth, the Roku price seems reasonable. Do you think Murdoch's will manage Roku well?