Why Disney Stock Will Underperform in 2026

12 Days of Pitch-Mas Day 6

For the 6th Day of Pitch-Mas, I am pitching The Walt Disney Company (DIS) as an Underperform for 2026. My core thesis is that Disney’s television networks division is too great a burden for the company to outperform the S&P 500. I consider a spin-off of Disney’s linear broadcast and cable channels to be inevitable. I predict the second, upcoming retirement of CEO Bob Iger, scheduled for the close of 2026, will be the moment the company seizes the opportunity for a major corporate restructuring. I acknowledge Iger has withdrawn his resignation plans numerous times. I am not suggesting shorting Disney stock, but using this pitch to elaborate on media industry trends I anticipate Disney will struggle to navigate in 2026 and outline the changes I would need to see to alter my perspective.

Theme 1: The Inevitability of the ESPN Spinoff

Let us be honest: the writing is on the wall for Disney to one day spinoff its television assets. I would turn more bullish tomorrow if I woke up to a formal announcement. But I do not think we will see it until Bob Iger is formally out the door.

Why Iger will not pull the trigger (Before 2027):

The Legacy Trap: Iger will likely never publicly admit to supporting a separation because it would be the equivalent of admitting the 2019 merger with Fox’s television assets was a mistake. As I said in my September article, Same Script, Different Cast, I explained how it is clear that Disney did not make the deal of the century when it acquired the majority of 20th Century Fox and most of its affiliated cable networks back in 2019.

“The acquisition of Fox is widely regarded as a disappointment, if not a complete failure. It is noteworthy that what was once Disney’s largest acquisition is no longer considered the strongest aspect of its investment strategy, merely five years later.”

The "Headache" Factor: Managing a corporate restructuring is messy. I do not think Iger wants to deal with those headaches on his way out. It is more likely that his successor gets tasked with the complex divestiture of ABC, ESPN, and the other cable networks while still maintaining performance at the other business units.

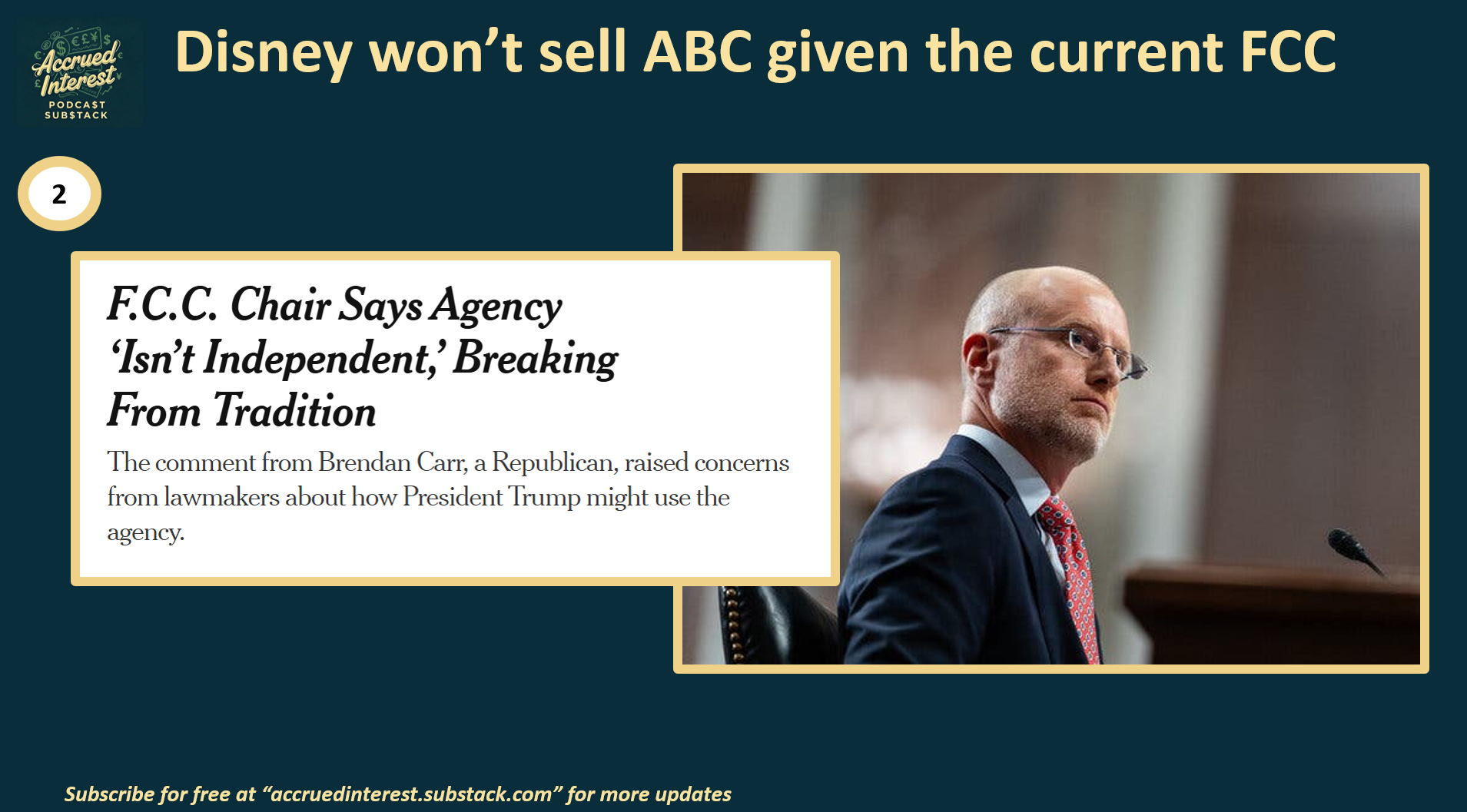

The Hard Part (ABC & Cable Networks): Divesting the other networks is trickier. ABC is a "Big Four" broadcast network, meaning any sale requires FCC oversight. With the current political climate, an ABC sale is likely a non-starter during the Trump administration.

Theme 2: Peer Pressure & The "Smart Money" Move

The reason I am confident a spinoff is coming is simple: Disney’s biggest rivals have already shown their cards and done it first. I can understand that nobody wanted to be the first company to shrink their empire. But now that Fox, Comcast, and most recently Warner Bros. Discovery have all spun off television assets in some form, this would no longer be an unprecedented transaction, and I can see Disney shareholders more vocally demanding it. Disney stock has been a perennial underperformer for most of Bob Iger’s tenure.

Precedent Transactions:

Comcast’s “Versant” Spin: Comcast recently approved the spinoff of “Versant,” shedding cable weights like USA Network, CNBC, and Syfy. They kept the premium assets: NBC, Bravo, and Peacock. In many ways, Comcast is the legacy media company most like Disney , and yet they still decided these assets had to go.

The Fox Standard: I have said it before: Fox Corporation set the gold standard by selling their networks at the peak of the cycle when they sold to Disney back in 2019. Disney, as the “winner” of those assets, ended up becoming the largest owner of cable networks just as the bundle began to collapse.

Warner Bros. Discovery: As I covered in my stock pitches on Netflix and Google recently, WBD is selling its production studio and spinning off cable networks to unlock value for shareholders.

Theme 3: The YouTube Problem (Why 2026 Will Hurt)

The core of my bearish stance on Disney is that Google, through both YouTube and YouTube TV, is already disrupting legacy media. As discussed in my “12 Days of Pitch-Mas” series, this disruption will become a significantly greater obstacle to Disney achieving its future targets in 2026 and subsequent years.

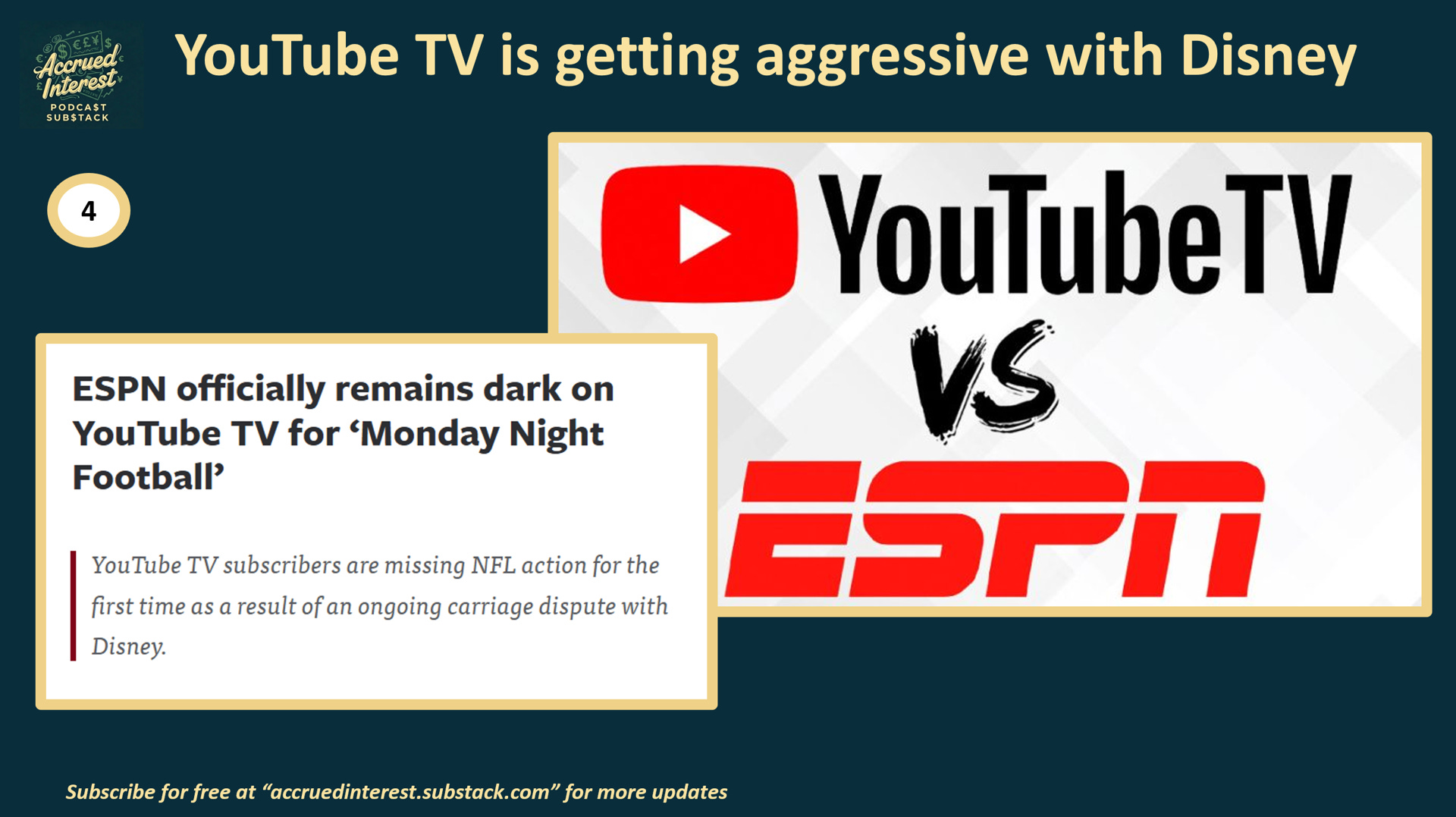

Google has “Walk Away” Power:

The Leverage Imbalance: This fall, YouTube TV let Disney networks go dark—even during NFL games. In the old days, cable companies would blink first out of fear. The fact that Google played hardball was notable because this was more aggressive than they had ever been before with television networks.

The Revenue Reality: While YouTube would love to have Disney content, their parent company Google, as an entity, does not need Disney. YouTube generates north of $50 billion in revenue. My back-of-the-envelope math suggests Disney only brings in about $2.1 billion each year in subscription revenue from YouTube TV subscribers to their channels. (10 million subs x $18 per sub, per month) When you do not need the money, you have all the leverage!

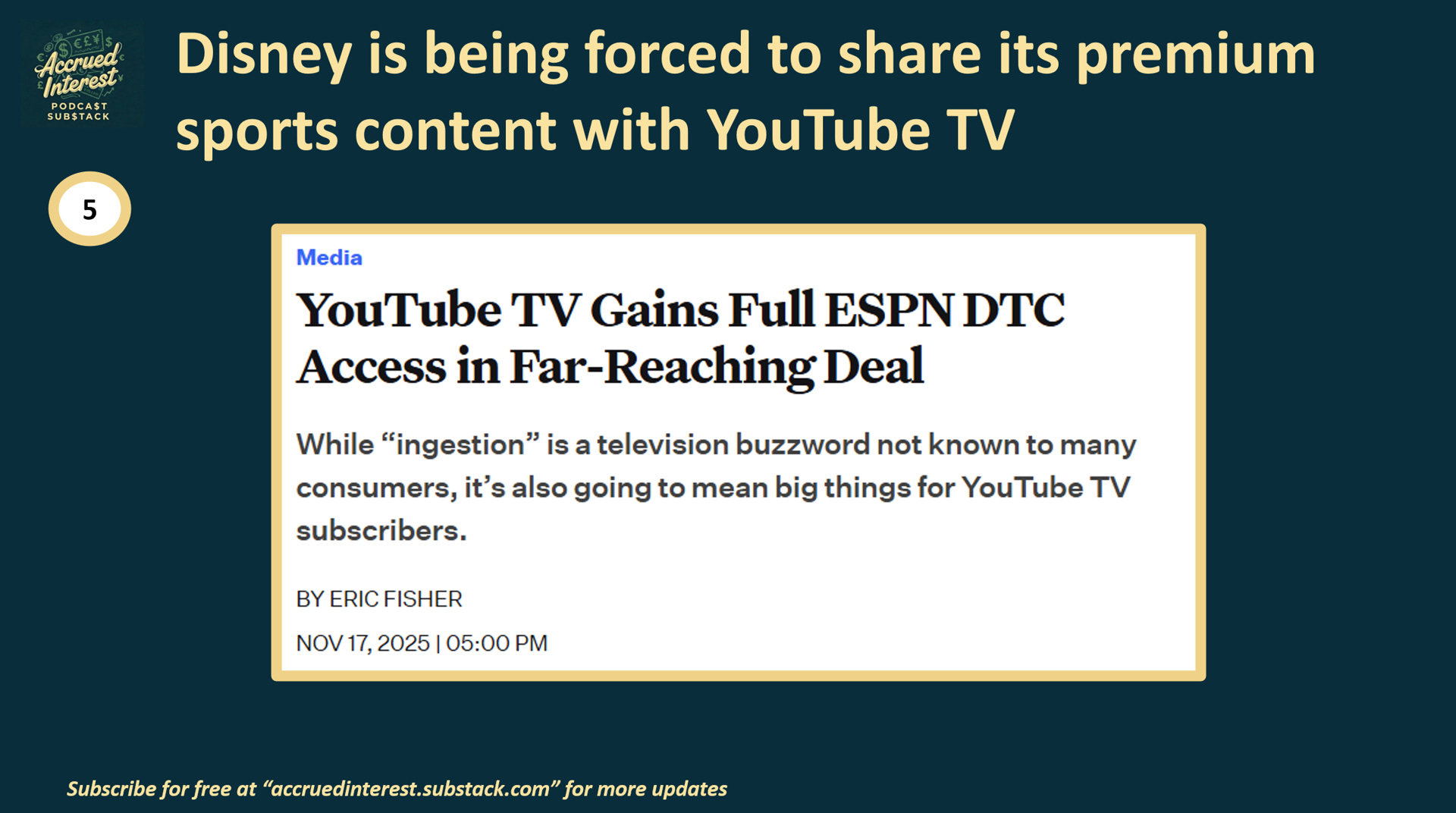

The “Trojan Horse” of Ingestion & Bundling:

The Ingestion Threat: A key tenant of the recent Disney-YT deal allows YouTube TV to ingest Disney’s premium sports content directly into the YouTube interface. This trains customers to watch sports outside of the Disney/Hulu ecosystem.

The “Skinny” Bundle: YouTube TV announced they are launching genre-specific bundles next year, starting with Sports.

Cord Shaving: Currently, every YouTube TV sub gets every Disney channel - meaning DIS has effectively 100% penetration within the Google footprint. With genre bundles, subscribers will be opting out of general entertainment channels. This will lead to “cord shaving”—downgrading to cheaper packages—which will lower the average penetration rates of Disney’s many channels.

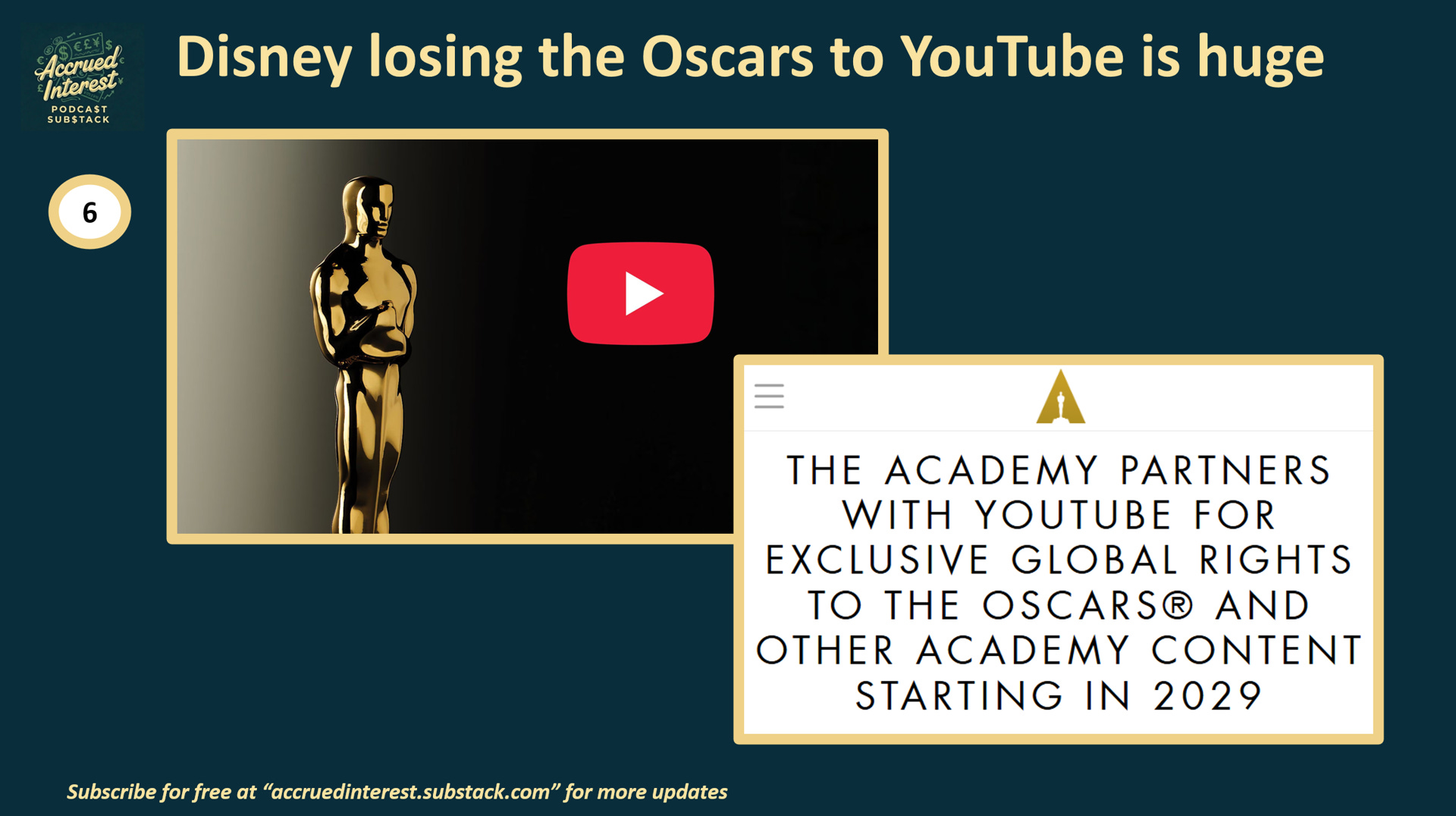

The Prestige Hit of Losing the Academy Awards:

Losing the Oscars: In a symbolic blow, YouTube won the exclusive rights to air the Oscars starting in 2029. I find it a bit ironic that while DIS 0.00%↑ successfully consolidated Hulu, it is still losing a crown jewel live event to a tech giant signals the continued exodus of premium content away from traditional TV.

Theme 4: Silver Linings for Disney

My outlook for Disney’s 2026 is not all unwelcome news. There are parts of the House of Mouse that still work, even if they are not enough to change my overall underperform rating on its shares.

Where Disney is Still Winning:

The Theme Park Money Machine: Disney is wise to shift its capital expenditures from TV toward its Disney Experiences division, which includes its theme parks, resorts, and cruise lines. They are currently running interesting dynamic pricing experiments at Disneyland Paris, which I anticipate will be implemented worldwide, extracting greater value from each visitor.

The Box Office Comeback: Despite concerns about “Marvel fatigue” and the post-COVID climate, which led many to doubt Disney’s box office dominance, the company has successfully rebounded. Disney proved critics wrong with major successes like Inside Out 2, Moana 2, and Zootopia 2. This resurgence is a result of a strategic pivot toward a successful model of high-quality sequels and live-action remakes.

CONCLUSION

My bearish outlook on Disney is based on the belief that a significant corporate restructuring of their media and entertainment division won’t happen until after Bob Iger leaves, meaning Disney’s new phase will likely be delayed until 2027 or later.

I would view the stock more favorably if they announced a divestiture, such as an ESPN spin-off. However, I expect the current operational strategy to remain for at least another year, causing Disney to lag industry performance in its broadcast and cable properties. The superior performance from the movie studios and live experiences will not be enough to offset the ongoing issues in their TV portfolio.

If you found this interesting, do not forget to subscribe. And please come back for Day 7 of Accrued Interest’s 12 Days of Pitch-Mas! You can find prior days here: Day 5 META 0.00%↑ , Day 4 NXST -0.36%↓ , Day 3 GOOGL -3.52%↓ , Day 2 PSKY -1.96%↓ , and Day 1 NFLX -0.80%↓ .

-Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.