The Strait of Roku: How Fox Seized Streaming’s Chokepoint Without Firing a Shot

Part Two of an Accrued Interest Deep Dive on Roku’s Monetization Levers

Accrued Interest TLDR: Roughly 44% of America’s connected-TV viewing flows through Roku — the chokepoint of US streaming. For a decade, its founder refused to collect a real toll. That’s over. Roku has thrown open the home screen to every advertiser, rebuilt it into a toll booth, and quietly built a live map of what tens of millions of households watch — a big, unpriced reason Fox wrote a $22 billion check. Screen $ROKU on hardware margins and you’ll see a sleepy device company. You’ll miss Q1 Platform revenue up 28% and EBITDA up 165%, with the payoff still in its early innings. It took Iran a war to weaponize its strait. Fox took this one without firing a shot.

Please subscribe for free to read the rest of this Accrued Interest deep dive on FOX/ROKU.

0. Introduction: The Chokepoint Hiding in Plain Sight

Over the weekend, Washington and Tehran sat down to begin talking through an end to the war, and for a few days the world stopped holding its breath over the Strait of Hormuz — the most-watched chokepoint on earth for months, for one simple reason: roughly 20% of the world’s oil passes through it. Iran sat on that leverage for years without fully using it. It took a war to finally weaponize the chokepoint.

I’ve had Hormuz on my mind all week, because it is the cleanest analogy I know for what Fox just did in the media industry — and for the story I want to tell in this piece.

The way I see it, Roku is basically the Strait of Hormuz of American streaming. Before you cancel me, hear me out. Roughly 44% of all connected-TV viewing hours in the United States pass through it — nearly three times its closest competitor. And much like its Middle Eastern counterpart, Roku spent years letting that traffic flow through while collecting a far smaller toll than it could have.

Earlier this week I published Part One of this deep dive “Fox + Roku: A Brilliant Pivot from the Cable Bundle to the Living Room”, where I walked through the merger deck and initiated coverage on NewCo with an Outperform rating. Last week I explained why Fox bought Roku. Today, in Part Two, I want to walk through the many levers Roku has only begun to pull — levers that can drive its revenue and profitability higher from here.

For the better part of a decade, Roku operated with one hand tied behind its back. It owned some of the most valuable real estate in connected TV and deliberately refused to monetize it. Not because it couldn’t. Because its founder didn’t want to. Understanding what changed is key to getting the stock right.

Much of the reporting that crystallized this for me comes from a sharp piece by Catherine Perloff in The Information last summer, “The Education of Roku’s Anthony Wood.”

Now let’s walk through the levers.

1. Lever One: Roku Spent Years Refusing to Sell Ads to Entire Industries — and Left a Fortune on the Table

For years, Roku capped its own highest-margin revenue by refusing to let whole categories of advertisers — autos, insurance, retail, restaurants — buy its best inventory at all. That self-imposed ban is what I call the “aesthetic tax,” and it left substantial money on the table.

Up until 2023, CEO Anthony Wood prohibited non-TV and non-media products from advertising on the Roku home screen, all to keep the experience “clean.” In his words, the company had focused on “keeping it simple” to ensure “a great viewer experience,” but “we didn’t really focus on ‘how can we use it to drive our business?’ And so that’s what we’re doing now.”

According to former employees and ad executives quoted in The Information, Roku staffers pushed to open the home screen to a broader set of advertisers, and the advertisers were begging for it — and Wood overruled them, year after year. One agency executive, David Nyurenberg of InterMedia Advertising, said he was “always pushing them on the home screen unit,” because — as he put it — “everyone sees the home screen unit when they turn on the TV.”

Now, that advertiser demand didn’t vanish when Wood blocked it from the home screen; it just got shoved downstream onto the free, ad-supported Roku Channel — a structurally worse place to monetize. The home screen is owned outright, but the Roku Channel is a revenue share.

And it gets worse: more than half of the Roku Channel’s available ad slots went unsold in 2023. Wood only recently changed his mind, opening the Roku home screen to all sorts of advertisers — auto, retail, QSR, and more.

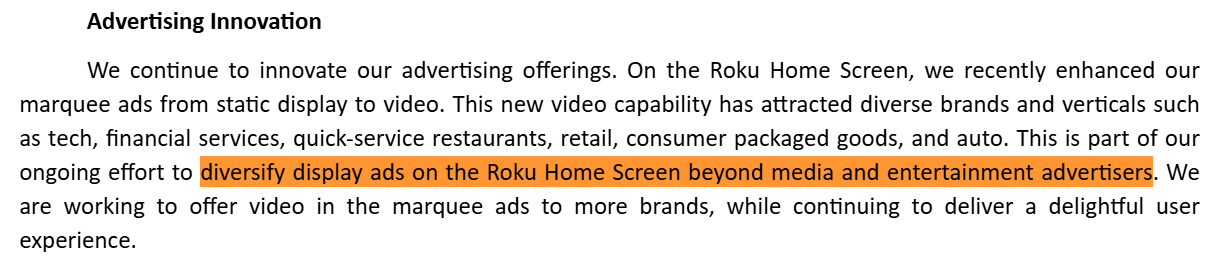

The 2024 10-K called it out plainly: Roku upgraded its marquee ads from static display to video to “diversify display ads on the Roku Home Screen beyond media and entertainment advertisers.”

By Q1 2026, ad spend from non-Media & Entertainment brands reached nearly 30% of total Roku Experience advertising revenue — an all-time high.

It’s only when you think like a business operator, not just a spreadsheet jockey, that you can appreciate how many levers Roku still has left to pull.

2. Lever Two: The Old Home Screen Waved Traffic Through the Chokepoint for Free — the Redesign Installs the Toll Booth

This is where the Strait of Roku analogy does its most useful work.

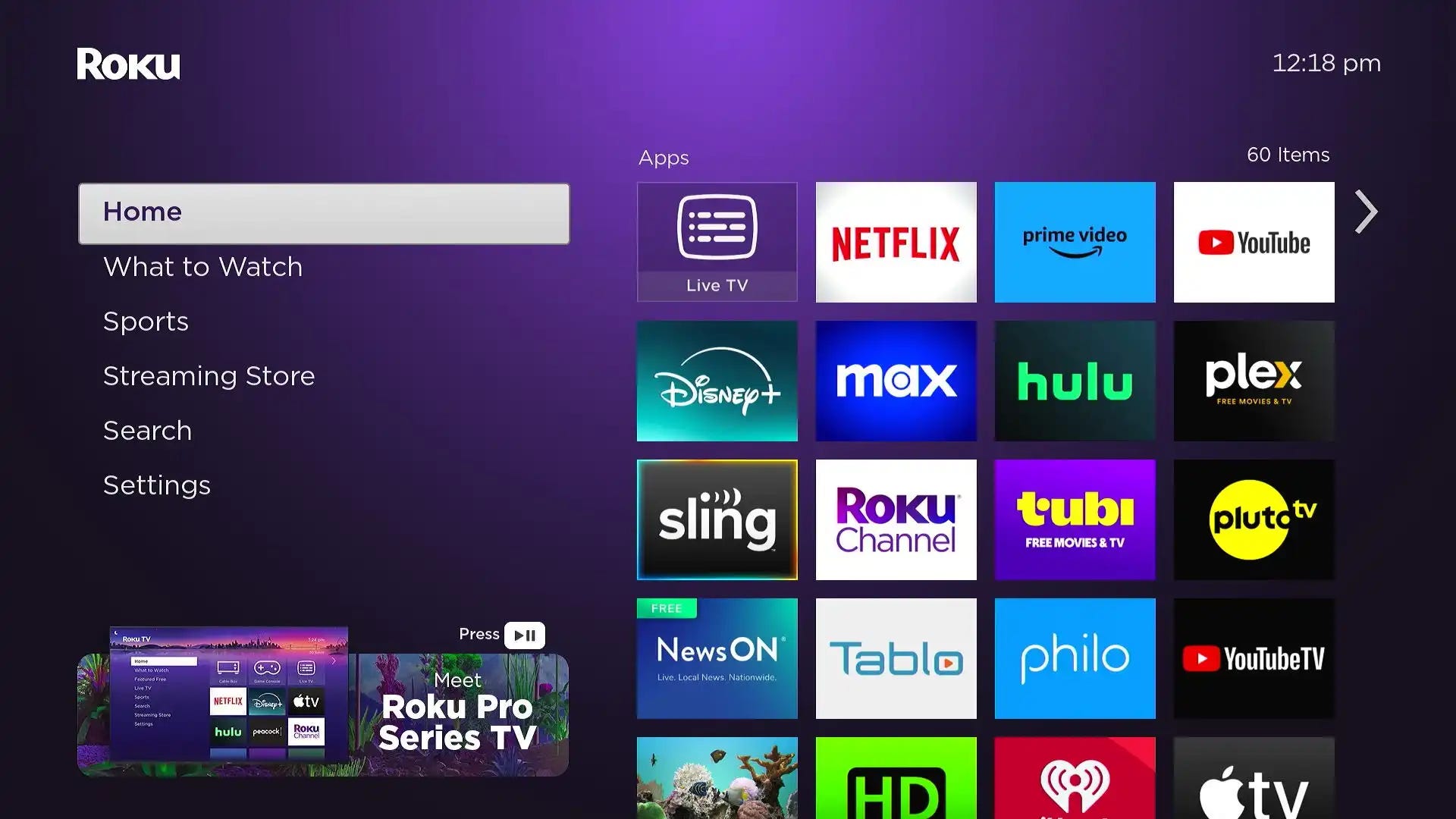

For over a decade, Roku’s home screen was a static grid of app boxes. You turned on the TV, saw a dozen icons — Netflix, Prime Video, Disney+, Hulu, and so on. Some 100 million households streamed through the chokepoint every night, and Roku waved nearly all of them through for free. From a monetization standpoint it was the worst possible design: a static grid acts as an inventory cap, dedicating the most valuable top-of-funnel real estate in the living room to a fixed set of unchanging icons. The viewer sees the grid, picks an app, and disappears into someone else’s walled garden, with Roku capturing none of the economics.

Image of the old Roku homescreen, mostly static squares

Wood resisted changing this for years, too. Former employees describe pushing him to evolve the interface toward one that surfaced individual shows and movies — the way Amazon’s Fire TV did — and being rebuffed. The data was clear: program-forward interfaces demonstrably led viewers to spend more time watching the content they promoted. Once again, Roku was choosing its aesthetics over its monetization.

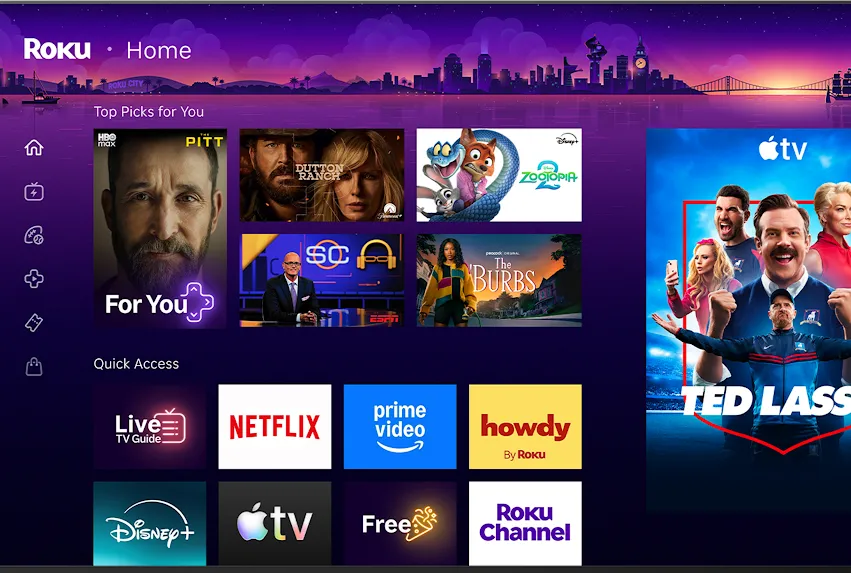

That changed on May 27, 2026, when Roku announced its first significant redesign of the home screen in over a decade. The new interface inverts the priority of the screen: instead of leading with a grid of apps, it leads with algorithmically generated, content-forward recommendations.

Image of the redesigned Roku homescreen, now with more personalized recommendations.

The company highlighted the changes in this YouTube video here.

Roku says its models now generate billions of possible home-screen combinations tailored to individual households. The redesign ships with AI-powered “Top Picks for You” rows, genre-based “Destinations,” a “Daily Scoop” trending row, a Roku City tile, and — critically — the Marquee Ad Video unit positioned so it’s visible the instant the screen loads, rather than buried a scroll to the right.

That last detail shows the toll booth going up. As Wood said on the Q1 call, “that change alone is driving more click-throughs.” Multiply that across 100 million households, and you can see why I’m so excited about this company’s potential.

The redesigned home screen turns the chokepoint into a tollgate, capturing brand ad dollars at the point of entry, before the viewer has opened a single app.

3. Lever Three: Roku Quietly Built a Live Map of What Tens of Millions of Households Watch

Wall Street has spent years treating Roku as a software interface with an ad business attached. But I’d argue a big reason Fox wrote that $22 billion check is a remarkably valuable data asset — one of the largest privately held maps of American TV behavior in existence — built on Roku’s ability to effectively “see” everything a viewer watches.

Roku claims more than 100 million active streaming households, but that footprint isn’t uniform. Some reach Roku through a streaming stick plugged into an older TV. The rest come through a smart TV that runs Roku’s OS natively — a Roku-branded set, or one of the tens of millions of TCL, Hisense, and other models that have shipped with Roku’s OS built in since the licensing program launched in 2014.

Roku doesn’t break out how many users come in through a native TV OS versus a stick, so let me show how I ballparked it.

Roughly 40 million smart TVs sell in the U.S. each year.

Roku has held north of 30% of TV-OS share for years.

Households replace their main set every 5 to 7 years.

Almost all TVs sold in 2026 are smart TVs.

If you extrapolate those assumptions across a replacement cycle, I guesstimate there are about ~60 million native Roku TVs (OS-enabled) and 40 million “stick” households. (I know these figures aren’t exact, but they’re directionally right. Argue with me in the comments if you disagree.)

So why does the split matter? Because a smart-TV OS can see things a stick simply can’t. A streaming stick is a walled garden; it only knows what you do inside the Roku interface. A native OS controls the whole set — and it runs Automated Content Recognition, or ACR. ACR takes constant pixel- and audio-level fingerprints of whatever is on screen and matches them against a huge reference database, identifying what you’re watching the way Shazam identifies a song in a bar. And it works across every input on the TV — every plug in the back — so it can “see” the streaming apps, the cable box, the game console, and so on.

ACR isn’t perfect, but it solves a big linear blind spot — finding out what the viewer did after seeing a commercial that just aired. Roku sells it not as surveillance but as “measurement and attribution,” exactly what advertisers have been starving for as dollars leave linear.

Owning this layer across tens of millions of homes gives Roku data that pure-streaming apps can’t replicate, because they only see viewer behavior inside their own walls.

If this capability sounds familiar, then it should — it’s the asset Walmart chased when it bought Vizio, the cleanest proof of this thesis. In late 2024, Walmart paid roughly $2.3 billion to take Vizio private. Walmart wasn’t doing the deal just to buy the hardware. It was buying Vizio’s SmartCast OS and its Inscape ACR data — the record of what Vizio homes watch — to pair with its own shopper data across roughly 150 million U.S. customers a week. That pairing produces advertising’s holy grail: closed-loop attribution, the ability to show a household an ad and then confirm it bought the product. It powers Walmart Connect, Walmart’s high-margin retail-media arm — and the whole move just ran the playbook Amazon wrote years earlier with Fire TV. If the data is the prize, then the TV hardware is simply the cost of admission.

Now compare the Walmart/Vizio deal to Fox/Roku. Walmart paid its $2.3 billion for Vizio’s roughly 18 million accounts; Fox is buying Roku’s 100 million-household footprint (which I’d guess has 60 million ACR-capable sets) and pairing it with live sports and news Walmart could only dream of putting next to the data.

What Fox really bought is a closed-loop attribution system on tens of millions of connected TVs, with a live feed of what those homes watch. For example, Fox can see, in aggregate, how much time Roku homes spend on ESPN or CNN through their cable boxes, then counter-program its own sports and news and nudge those viewers toward Tubi and Fox One.

For a company whose edge is live sports and news — genres that still air heavily on linear — owning the one tool that bridges linear viewing and streaming retargeting is an amazing strategic fit.

4. Roku’s Own CEO Just Confirmed the Home Screen Is Nowhere Near Fully Monetized

This last point isn’t a new lever so much as confirmation of the first three. In the Q&A of the June 2026 M&A call, Roku revealed just how much toll-collecting capacity it still hasn’t switched on.

An analyst raised a reasonable-sounding question: if Fox starts using the Roku home screen to promote its own properties, won’t that cannibalize the home screen’s ad revenue? Every pixel given to a Fox promo is, in theory, a pixel you could have sold to a third party.

Anthony Wood jumped in to correct the premise:

“I just wanted to talk a little bit about — you said a comment, which I think I just want to correct, which is that you implied that promoting FOX owned and operated properties on the Roku home screen would somehow reduce profitability for the home screen. I don’t think that’s true. Actually, it’s going to increase profitability… So one of the — so we sell ads on our home screen throughout our UI, obviously. But we also have many, many ways to promote content throughout the UIs that are not necessarily sold… and we can do it in a way that’s going to increase the amount of revenue that’s generated by the Home Screen.”

What Anthony is really saying is that the commercial ad slots Roku sells are only one layer of the home screen’s promotional surface. Underneath sits a vast amount of organic, algorithmic real estate that Roku doesn’t sell to anyone — the “Top Picks for You” rows, the genre Destinations, the menu placements, the Daily Scoop. Because it owns the operating system, Roku can route enormous viewership through all of it without touching a paid ad slot, driving demand wherever it wants — a Fox property, a partner’s show, a Roku Channel original — on inventory that has no opportunity cost, because it was never for sale.

The Roku UI is so far from fully monetized that promoting Fox’s content doesn’t compete with the paid inventory — it runs in parallel, on surface area Roku hasn’t even tried to price.

Wood was just as direct on why he’s selling now. He framed it as negotiating from a position of strength — Roku sitting “at the center of the streaming ecosystem” with the levers finally working — at what he flatly called “a great price,” into a buyer who understands what the asset is worth. This is a business that has just proven its model and wants a bigger balance sheet behind it to press the advantage.

Which brings us to the numbers from the most recent quarter.

5. The Payoff Is Only Just Starting to Show Up in the Numbers — Which Is Exactly Why Roku Sold Now

Now, here’s what changed. For years Roku reported revenue in a single opaque “Platform” line. In Q1 2026, it finally split Platform into two reported segments — Advertising and Subscriptions. That added disclosure was deliberate. You don’t pry open the hood and show investors more KPIs when the business is sputtering; you do it when things are improving and you want investors extrapolating that improvement into the future.

And the margins explain why: Advertising ran a 60.5% gross margin, Subscriptions 41.1%, the blend 51.6%. As the higher-margin advertising line grows faster than subscriptions, the mix alone pulls the blended margin up over time.

The recent revenue acceleration is the cleanest evidence that the levers are working. Full-year 2025 Platform revenue grew a steady 18% YoY. In Q1 2026, the first quarter in which the new advertisers, the video marquee units, and the run-up to the UI redesign were all scaling at once, it jumped to 28%.

Advertising grew 27% YoY to $613 million; Subscriptions grew 30% to $519 million on Roku’s best-ever quarter for Premium Subscription sign-ups. The supporting metrics all moved in tandem — programmatic ad spend up more than 40%, Ads Manager advertisers more than doubled, Marquee Ad Video advertisers doubled while spend on it tripled. And it dropped through to the bottom line, with Adjusted EBITDA hitting $148 million, up 165% YoY off a $56 million base.

The Q1 Inflection Point (YoY)

None of these are mature numbers. The non-M&E mix shift, the new UI, the ACR-driven targeting — all of it is early, the first innings of the monetization payoff. Roku didn’t sell a finished story but an inflecting one. You command a far better price demonstrating an upward earnings trajectory than delivering a plateau.

Conclusion: Iran Needed a War; Fox Just Needed Patience

Step back to Part One. The Murdochs sold the bulk of their entertainment empire to Disney in 2019, very near the top of the peak-TV bubble. They sold high. Seven years later, they’ve put that capital down on the front door of the living room — just as connected-TV races past 40% of the TV pie. The call from Part One stands: Outperform. Mr. Market mispriced Roku because its financials describe the company Roku used to be, not the one it’s becoming.

It took Iran a war to weaponize its strait. Fox needed no war — no bidding war, no bet-the-company rights auction. Just a patient, perfectly-timed deal it had been setting up since the day it walked away from cable.

Could Roku have kept building the toll booth alone? Sure — Q1 proved the model works. But advertising and data are scale games, and a Fox balance sheet lets Roku press that advantage harder and faster than it ever could solo. The cable bundle is not coming back. The future of television runs through a chokepoint — and Fox just bought the one that finally learned to charge for passage.

Next time, I’ll lay out some ideas on how else Fox can use Roku to wring more value out of its O&O properties. As always, let me know your thoughts in the comments.

Relevant tickers: FOXA 0.00%↑ FOX 0.00%↑ , ROKU 0.00%↑ , AMZN 0.00%↑, GOOGL 0.00%↑, WMT 0.00%↑, NFLX 0.00%↑, DIS 0.00%↑

— Accrued Interest

Relevant Accrued Interest Articles:

2026.06.16: Fox + Roku: A Brilliant Pivot from the Cable Bundle to the Living Room

2026.05.28: Monetizing the Habit: Meta’s Enterprise Land Grab and Roku’s Living-Room Billboard

2026.04.16: Roku’s 100 Million Milestone

2026.03.20: Dead on Arrival: 8 Reasons the Paramount-WBD Merger Will Fail

2026.03.12: The Pokémon Theory of Media Investing

2025.12.18: Why Disney Stock Will Underperform in 2026

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.

Really enjoyed reading this piece of work as well as the one from the previous week.

I would love to add one thread that I think reinforces the advertising-mix argument from the hardware side: Roku OS is structurally pre-installed on value-to-mid tier TVs (TCL, Hisense, Westinghouse, RCA, Haier, licensed Philips, plus Roku's own Select/Plus). Samsung and LG own the $800+ premium shelf; Sony runs Google TV. That means Roku's installed base skews lower-to-middle income by design.

This specific audience consistently picks ad-supported tiers over ad free, which caps Roku's subscription rev share per household but creates exactly the ad inventory Roku monetizes through ACR, FAST, and home screen real estate. Ad-supported ARPU now matches ad-free at Netflix/Disney given $40–60 CPMs, so the demographic weakness on subs is the demographic strength on ads.

Which is also why Fox is the right partner. Tubi, O&O local broadcast, and live sports/news all match the audience. A Disney pairing would have been fighting the demographic; Fox is leaning into it. The 60.5% ad gross margin vs 41.1% subs margin you flagged is the cleanest evidence that the structural design works.

Also want to add a pushback on something from the previous Fox + Roku deep dive you did last week where you mentioned that "consumers voted for Roku with their wallets". I came across an article on FT that cited Wolfe Research saying the majority of consumers actually have no OS preference or prefer something else. If that's right, the Switzerland model is more fragile than mutual economics suggest and market might be right to be careful about it. Netflix and Disney wouldn't need to pull their apps if something goes wrong. they'd just slowly lean into Fire TV, Google TV, and Vizio/Walmart and let share shift at the hardware refresh cycle.

Would love to hear your thoughts on it and thank you again for this article!