The Student Grades the Teacher: Why David Einhorn Is Wrong on Versant (VSNT)

Einhorn’s Sohn thesis treats a melting ice cube like a depreciation schedule. Q1 just showed us the leak — and Kim Kardashian is plugging it.

Accrued Interest TLDR: At this year’s Ira Sohn Conference, David Einhorn pitched Versant Media ($VSNT) as a deep-value cash machine — cheap multiples and a ~19% free-cash-flow yield. As a former Ira Sohn Idea Contest winner, I respectfully disagree: I have rated Versant an Underperform since January. The bull case only works if you accept a smooth, -7% annual decline that the Pay TV business has already breached. Q1’s “beat” was manufactured by a one-time sale of the Kardashians library to Hulu, masking a roughly -4.9% YoY organic decline. Most glaringly, Einhorn’s model ignores the 2028 cliff, when the NBC ad-sales halo, ~55% of carriage deals, and key sports rights all reset at once. VSNT is dead money until management stops empire-building and starts dismantling.

Please subscribe for free to read the rest of this Accrued Interest Versant deep dive.

0. Introduction

If you have read Accrued Interest for any length of time, you know I am always hunting for cracks in the legacy media bundle. The TMT landscape in 2026 is no longer a debate about whether linear television is in secular decline. The only live questions now are how fast the cash cow melts, who captures the high-intent viewer it sheds (spoiler: YouTube and Netflix), and what a management team is supposed to do with the river of free cash flow on the way down. That last question is where the value-investing crowd keeps stepping on the same rake — and it is exactly where I part ways with one of the most respected investors in the business.

If this stock deep dive seems longer than my usual write-ups, that’s because this one is personal. Back in 2013, while I was getting my MBA at Columbia Business School, I won the Ira Sohn Investment Idea Contest with a blind submission pitching Tribune Broadcasting. (For the details on my first 15 seconds of fame, check out my recap, How My Stock Pitch Won the Ira Sohn Investment Idea Contest.)

One of the judges who put me on that Lincoln Center stage was David Einhorn. More than a decade later, here I am taking apart Einhorn’s own Sohn pitch. It feels a little like the student grading the teacher’s homework — and I don’t say that lightly, because Einhorn is a genuinely great investor. But on Versant, I think he is wrong.

At the Ira Sohn Investment Conference on May 12, 2026, Einhorn pitched Versant Media Group ($VSNT) as a “sexy,” deeply mispriced cash machine at $41 a share. I flagged Greenlight’s new position back in my April 14 update, when the 13F first surfaced but before I had the full thesis in hand. Now that he has laid the entire spreadsheet out on a stage, I can give it the deep dive it deserves. (Go to minute 11:00 to jump to the Versant section of the presentation.)

With respect to a great investor: I think this is a value trap, and the bull math only works because it quietly assumes the one thing that cannot happen — a smooth, orderly decline of the cable bundle. Versant remains an Underperform in my book, and I want to walk you through precisely why.

Per Greenlight’s Q1 2026 13F, Einhorn established a brand-new stake of roughly 3.0 million VSNT 0.00%↑ shares — about 2.1% of the shares outstanding, or close to 2.6% of the active public float once you strip out the index whales (Vanguard owns about 10%, BlackRock about 8%) and Brian Roberts’ super-voting Class B block. For Greenlight, that is a meaningful, “medium-sized” position. But it sits well below the 5% threshold that would let him file a 13D and start swinging a board-level cudgel. In other words, this is a non-activist stake. Einhorn cannot force management to run the private-equity dismantle playbook that — as I’ll argue — is the only thing that would actually unlock value in this company. On this trade, he is a passenger on the same structural cliff as every other minority holder.

1. Einhorn’s Bull Case Is a Beautiful Model Built on Flat Lines

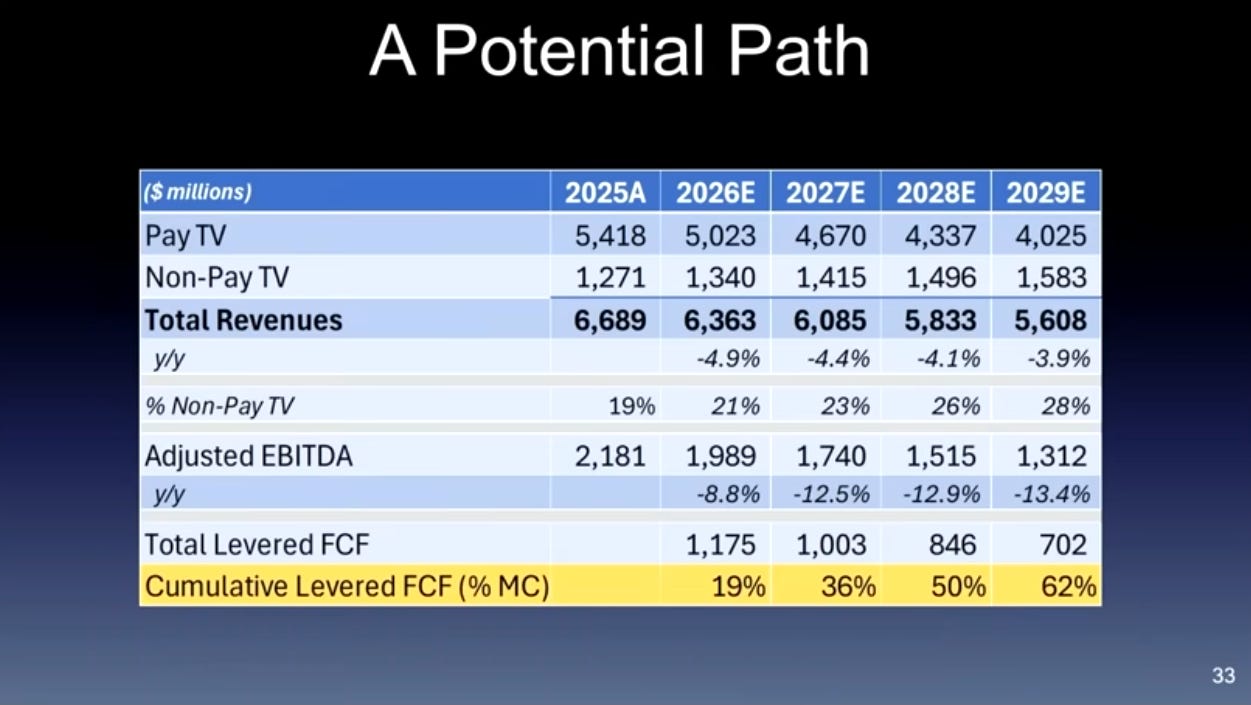

Let me give the bull case its full, fair hearing, because the way Einhorn framed it on stage, it is genuinely seductive. Every figure that follows is from his May 12 presentation, per his own estimates, assuming a stock price of about $41 per share.

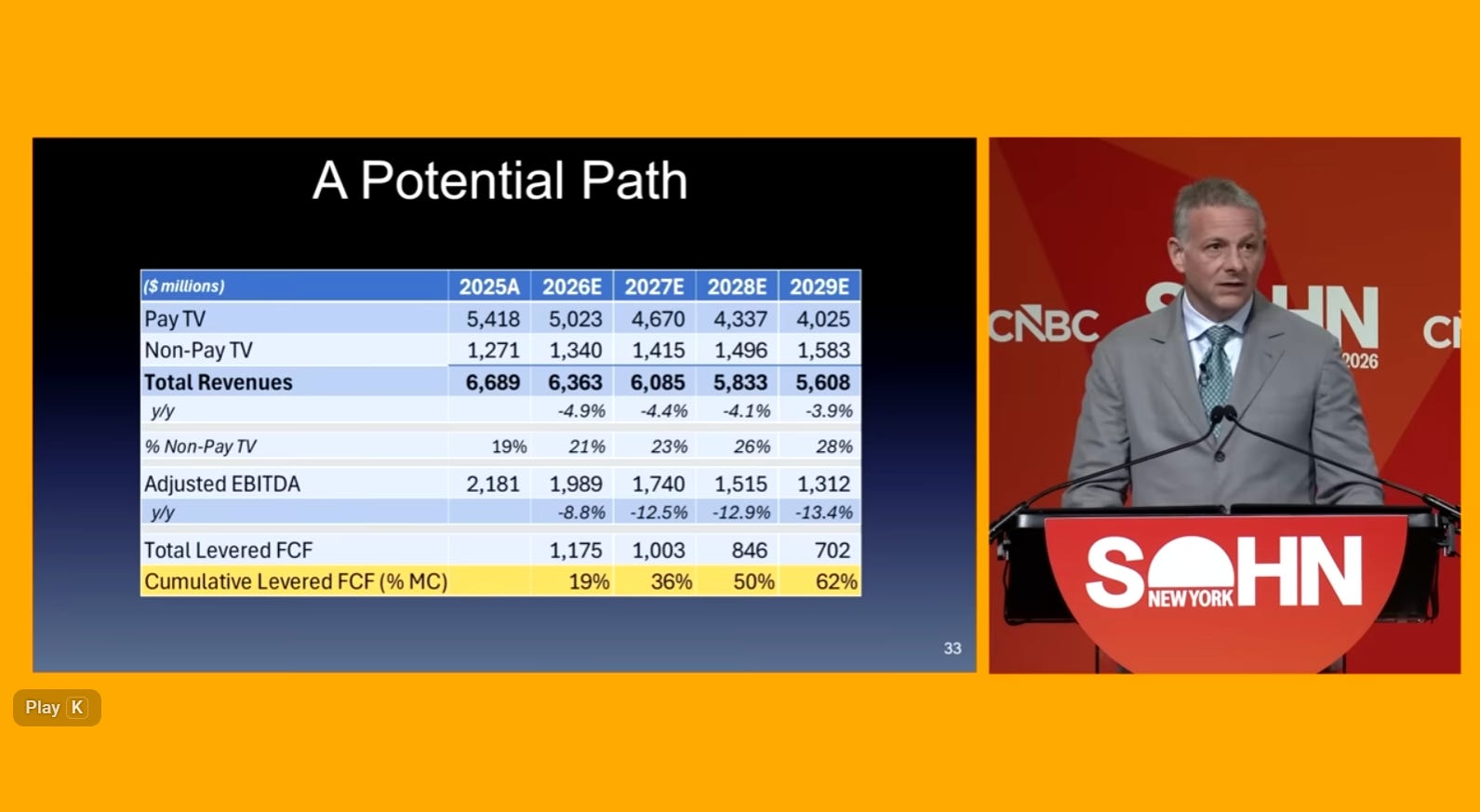

His pitch rests on the classic deep-value pillars. As of that presentation, the stock fetched roughly 4.6x earnings and 4.2x EBITDA, threw off a ~19% free-cash-flow yield, and management was buying back about $100 million of stock a quarter. He put his projections on the screen all the way out to 2029, with total revenue declining at an average of only about -4% a year in aggregate, and Adjusted EBITDA fading from roughly $2.18 billion in 2025 to about $1.31 billion by 2029.

Here is the part that mattered to me. I took Einhorn’s numbers and reverse-engineered the model to see what was actually driving that gentle -4% blended glide. Two assumptions do all the work.

First, he models the legacy Pay TV business declining at a consistent -7% every single year through 2029 (roughly $5.4 billion in 2025 grinding down to about $4.0 billion in 2029). Second, he models the non-Pay TV bucket — a hodgepodge of underweight, mismatched businesses — growing at a tidy +6% a year, every year, through 2029. Blend a -7% melting core with a +6% growing tail and you arrive at his -4% aggregate. The headline he draws from it is striking — he argues that Versant can generate about 62% of its entire current market cap in cumulative levered free cash flow by the end of 2029, leaving a business with only about one turn (1x) of net leverage.

He even tipped his cap to the melting-ice-cube bears with a clever one-liner. Einhorn conceded that Versant is “somewhat of a melting ice cube. The market these days thinks melting ice cubes are nearly worthless. Actually, they turn into a fair amount of fresh water.”

His point was that with more than 60% of programming tied to live news and events, the portfolio is supposedly far more resilient to cord-cutting than your average bag of entertainment cable channels — so you should be happy to stand under the spigot and collect the meltwater.

2. Value Traps Rarely Decline in a Straight Line

Here is my problem. The bull thesis rides on two straight-line assumptions from now until 2029, both of which seem highly unlikely. Einhorn assumes a constant -7% YoY decline in the Pay TV business and a constant +6% growth rate on everything else. That is what I call the Smooth Pace Fallacy: treating structural decay (and structural growth) like tidy depreciation schedules on a piece of factory equipment. Neither segment is going to behave the way you think it will.

Let’s take the -7% Pay TV assumption first. Cable does not melt in a straight line; it melts on a curve. As the most valuable, most affluent subscribers cut the cord first, the networks lose pricing leverage over everyone who stays, which accelerates the next leg down. And Einhorn’s “gentle” baseline already looks too generous. Versant management’s own full-year guidance math implies a -7.2% legacy decline at the midpoint.

And the most recent print on the carriage line is already past that mark. Linear Distribution — the affiliate fees operators pay to carry Versant’s channels, and the cleanest read on the core Pay TV business — fell -7.3% in Q1, even though carriage contracts typically carry annual rate increases. (I’d leave Advertising out of this comparison; that line is lumpy, swinging with the election and sports calendar, so I anchor on carriage revenue instead.) Einhorn is starting his soft glide from a pace the business has already breached — then extrapolating it, unchanged, for four more years.

Now for the non-Pay TV growth assumption of +6%. I want to remind readers that this segment is not some normal, digital-based business. This bucket contains a number of mismatched, uncorrelated assets. A constant +6% every year assumes that a grab-bag of underweight businesses, several of them levered to theatrical attendance, all march higher in lockstep. I don’t buy the smoothness on either end.

3. Why I Modeled Versant More Conservatively in January

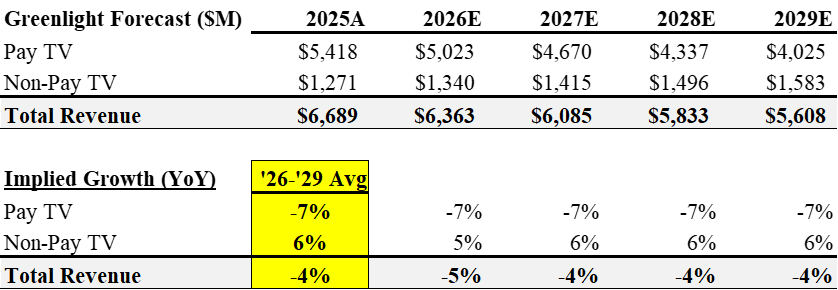

Now let’s contrast that with how I modeled Versant back in January, in Is Versant (VSNT) Cheap or Just Cheaply Valued? The Case for $27. Pictured below were my estimates at the time.

To stay deliberately conservative, I ran total revenue declining at -7% — the high end of management’s own guided decline — in every year out to 2028. I wasn’t trying to nail the decimal; as the old line goes, I would rather be approximately right than precisely wrong. My reasoning was simple, and it still holds: management teams in this industry skew optimistic, so I think it is more likely than not that Pay TV bleeds faster than the guide, and that the non-Pay TV pieces grow slower than advertised — or, at the very least, that hitting those growth numbers will require M&A, which is itself an admission that the organic growth story isn’t really there.

Put plainly: Einhorn is being too kind to both halves of the business at once, while I chose to haircut the whole thing.

4. The Versant ‘Sports Moat’ Is Rented, Not Owned

Then there is what I like to call the Rented Moat. Einhorn leans on live sports as the firewall against cord-cutting. But as a media specialist, let me tell you: USA Network is not a sports network — it is a basic cable channel that happens to show sports. USA Sports is not a standalone cable channel or streaming network. You cannot tune into a channel called “USA Sports” on your program guide. It is a production banner and marketing tool rather than a real destination.

It airs roughly 1,400 hours of live sports a year, about four hours a day, and fills the other twenty with reruns of Law & Order: SVU and Chicago Fire. Crucially, Versant does not own the rights to air any of these properties, such as WWE, NASCAR, or the Premier League. It rents them. Programming is about 55% of total expenses, and roughly half of that budget goes straight to live sports. In a world where Amazon, Netflix, and YouTube are bidding up every live right that comes loose, Versant is paying premium, escalating lease rates to rent eyeballs for a network in terminal decline. That is not a moat, but a margin trap with a countdown timer.

5. Buybacks Won’t Save a Melting Ice Cube

As I have said many times on Accrued Interest, financial engineering is not a strategy. I learned this lesson the hard way watching the local-TV roll-ups: buying back stock in a structurally shrinking business just rearranges the deck chairs faster. We have seen this movie. It is the Philippe Dauman playbook at Viacom in the 2010s — “look how cheap, look at the yield” — which ended in brutal multiple compression that vaporized the value investors who showed up early for the cash flow. I vividly remember another famous value investor pitching Viacom during the 2010s at Ira Sohn, and I can’t help but wonder if Einhorn is making a similar mistake today.

6. Kim Kardashian Saved Versant’s Quarter

Einhorn’s presentation had whimsical New Yorker cartoons but was overall light on actual math. So allow me a moment to go deep on VSNT’s Q1 2026 earnings to demonstrate the holes in the bull thesis. I want to show you exactly why I think the “fresh water” analogy is looking a lot more like a leak.

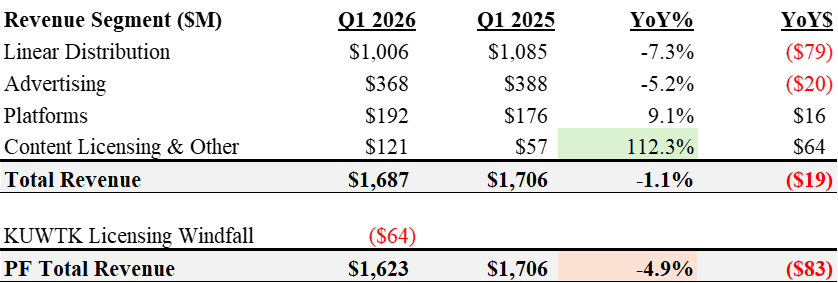

Versant’s earnings headline was solid. Total revenue of $1.687 billion was down only -1.1% year-over-year, with $704 million of Adjusted EBITDA and $286 million of net income. The market cheered. However, when reviewing earnings, I always break down which segments did the heavy lifting — and here, the answer is almost too perfect.

The Beat Was Manufactured by One Kardashian Sale

In the table below, I’ve laid out Versant’s historical revenue performance for Q1 2026 vs. 2025.

Look at that “Content Licensing & Other” line. It was up +112%, for a $64 million swing — the single largest absolute-dollar gain of any segment in the last five quarters. Do not be fooled — this was not organic digital momentum. Most of the gain was a one-off library syndication deal, widely reported to be the E! network’s Keeping Up with the Kardashians catalog licensed to Hulu. On the earnings call, when analysts asked to quantify the exact size of the deal, management was evasive. Let me explain why.

The one-time Kardashian distortion makes investors think there is more organic growth at Versant than meets the eye, but that is sadly not the case.

Strip that $64 million one-off out and Versant’s core revenue was roughly $1.623 billion — an organic decline of about -4.9%, sitting comfortably inside management’s own full-year revenue guide of -3% to -7% YoY declines.

In plain English: Kim Kardashian’s back catalog is the only reason this quarter didn’t look like the disaster the bears predicted. And notice the irony for Einhorn’s thesis. That -4.9% revenue decline is already pacing worse than the -4% blended decline his model forecast for the entire company, and VSNT needed a one-time windfall just to get there.

Selling the Kardashians catalog is a temporary patch, not a structural fix. You cannot sell your library to your competitor every quarter — you eventually run out of shows to sell. Worse, every one of these deals arms the enemy. Versant just handed the back catalog of one of its premium reality franchises over to Hulu (Disney) just to prop up one quarter’s financials, while strengthening a direct streaming rival in the process.

Versant’s Core Business Fell ~$100M While Platforms Only Added $16M

For Q1 2026, Versant’s core legacy television business segments — Linear plus Advertising — shed nearly $100 million of revenue in a single quarter (-$79M and -$20M). Counteracting that — VSNT’s celebrated digital “Platforms” segment only contributed a grand total of +$16 million, which is like using a handful of band-aids to fix a dam leak. This is why I don’t believe Einhorn’s flat +6% YoY growth forecast for the non-Pay TV segments can ever be large enough to matter against the sheer size of the melt.

The Real Tell: A $64M Beat and No Guidance Raise

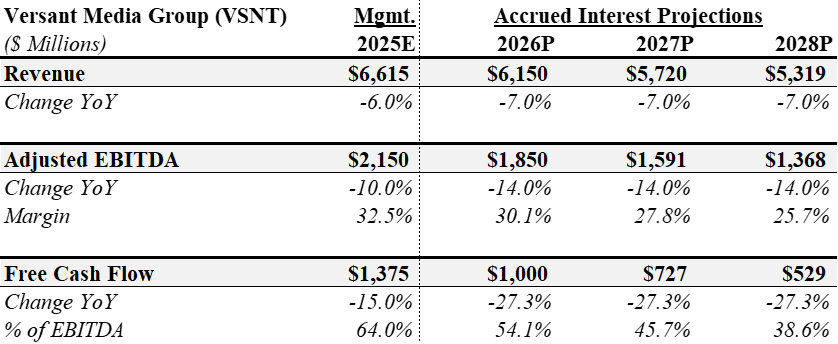

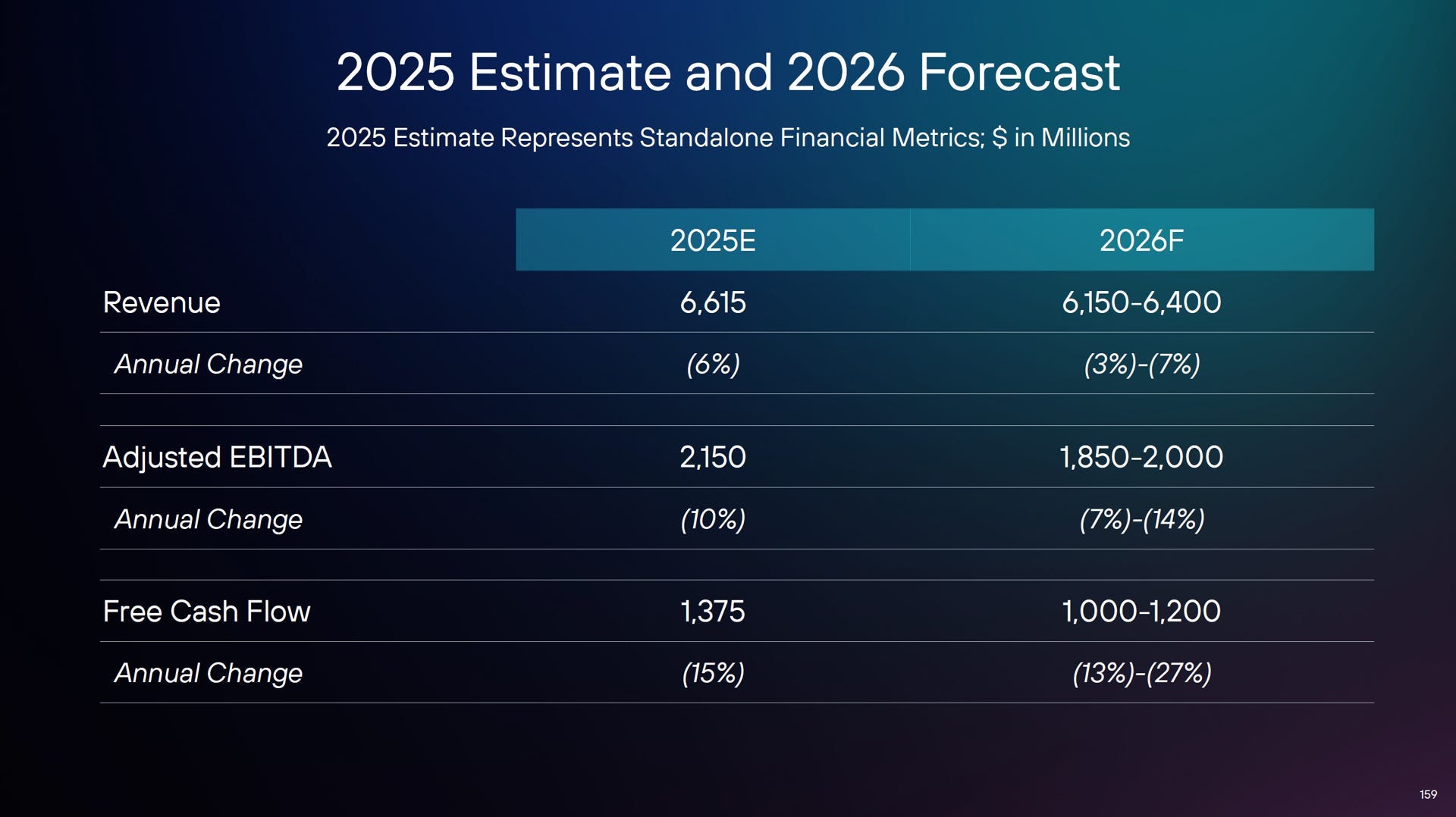

The most damning thing I noticed in VSNT’s Q1 earnings was that management maintained — but pointedly did not raise — their full-year guidance despite getting a $64 million windfall in Q1. For reference: here was the 2026 guidance presented at the December 2025 Investor day.

Revenue guidance stayed at $6.15 to $6.4B (-3% to -7% YoY), EBITDA at $1.85 to $2.0B (-7% to -14% YoY), and Free Cash Flow at $1.0 to $1.2B (-13% to -27% YoY). (Those percentages are calculated off management’s standalone 2025 revenue estimate of ~$6.6 billion, which is why they look slightly milder than they would be against Einhorn’s $6.69 billion 2025 actual.)

When a company absorbs a one-time beat and keeps the numbers unchanged, it is telling you the underlying decay is accelerating faster than the model assumed. Basically, the windfall is quietly plugging a hole you can’t see yet. Also on the call, CFO Anand Kini flagged higher programming costs from sports-rights timing in the second half, specifically Q4. I feel like Versant is using Kardashian cash to fill a back-half sinkhole.

7. Einhorn’s Model Pretends the 2028 Cliff Doesn’t Exist

Now we get to the part of Einhorn’s presentation that genuinely stopped me cold — not because of what was in it, but because of what wasn’t. He did not mention Versant’s 2028 cliff. At all. For a thesis whose entire foundation is the durability of Versant’s news and sports portfolio, leaving out 2028 is not a rounding error — it is more akin to ignoring a load-bearing wall. I genuinely don’t know whether Einhorn built this analysis himself, handed it to a junior analyst, or let ChatGPT draft the model. But that omission is precisely the kind of thing that separates a media generalist from a media specialist. You do not find this risk on a screen or in a headline multiple. You only find it by climbing into the weeds of the spin-off documents and then overlaying very specific, hard-won knowledge of how bargaining leverage actually works in practice — not theory — when it comes to television distribution negotiations.

Versant Faces Pressure on Three Fronts at Once in 2028

This is the heart of my bear case — the same one I detailed on the Yet Another Value Podcast and across my January work. Versant is over-earning today under the protective halo of the NBC ad-sales machine. When Comcast spun the company out in January 2026, it handed Versant a two-year Transition Services Agreement to keep riding NBCUniversal’s enormous ad-sales infrastructure. That umbilical cord gets cut in 2028 — and that is when a smooth glide path turns into a step-function cliff. For new readers, let me remind you of the risks involved.

First, Versant loses the “NBC Halo.” It will have to walk into the Upfronts and sell its inventory without big brother’s help — no Peacock, no Sunday Night Football, no NBCU bundle to hide behind — against Amazon, YouTube, Disney, and the rest of the industry. Versant will eventually lose the bundling leverage that, I argue, inflates VSNT’s ad pricing (CPMs) today.

For example - If you go to the web page for Versant’s channel SYFY, when you click the link “Advertise With Us”, it takes you to a landing page where they show you the entire NBCUniversal family. Right now, ad sales clients are being pitched on the value of Versant Media properties mostly due to their connection to the strongest NBC-related channels. NBC, Bravo, and NBC Sports are the high-value anchors for both advertisers and streaming growth, as evidenced by the fact that Comcast kept them to fuel Peacock while spinning off Versant’s networks.

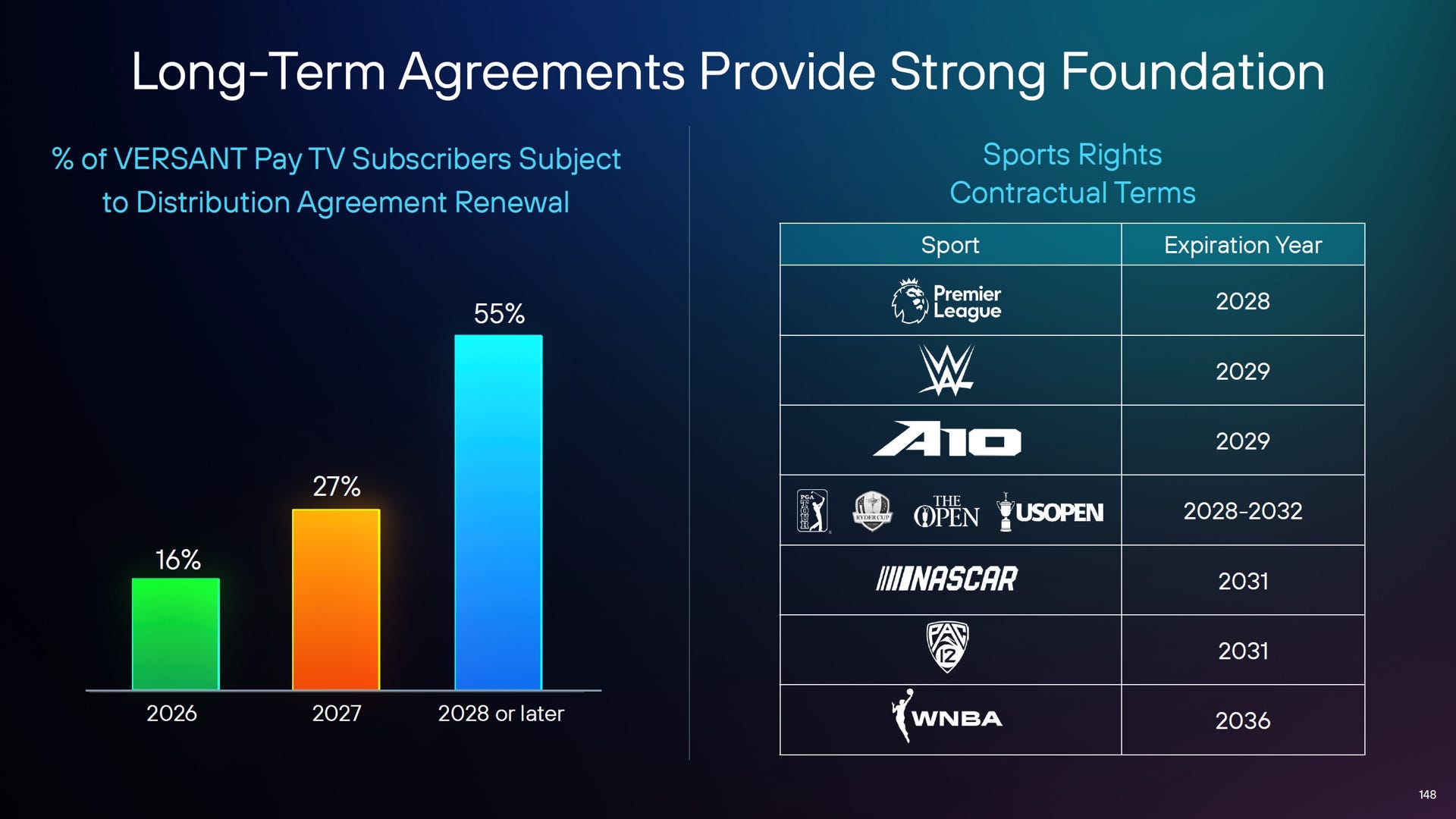

Second, roughly 55% of Versant’s Pay TV carriage agreements come up for renewal at essentially the same time, around 2028. These are the contracts with the cable operators and the vMVPDs (yes, including YouTube TV, the only distributor in the ecosystem actually growing). A company with a shrinking, lower-rated subscriber base is in for a world of pain when it comes to these post-2028 negotiations.

Third, the sports rights renew straight into that weakness — and this is the part that should terrify the bulls, not comfort them. If you happen to believe live sports is the moat, then 2028 is when the moat gets re-priced. Versant’s sports portfolio is essentially the leftover rights NBC could not fit on its main broadcast network.

VSNT is up against the digital war chests of YouTube, Netflix, and Amazon Prime — bidders who no longer answer to legacy-network economics. Post-2028, Versant either loses the rights (and the ratings collapse) or massively overpays to keep them (and the margins collapse). Either way, the company’s enterprise value will inevitably get re-priced downwards. The future of TV belongs to the streamers, with Netflix running the smartest playbook by buying surgical, high-impact events rather than inheriting a full season’s fixed cost.

You cannot model 2028 as “just another” -7% year and then show 2029 as more of the same. That Einhorn’s stock pitch doesn’t even pretend to acknowledge what is clearly Versant’s single biggest risk is why I’m comfortable standing on the other side of this trade.

8. Versant Management Needs to Stop Empire Building

For newer readers, none of this is a fresh opinion — I have been beating this drum for months. I made the bear case in Is Versant (VSNT) Cheap or Just Cheaply Valued? The Case for $27 and in Is Versant (VSNT) Worth More Dead Than Alive? back in January, broke down the spin in Decoding the Versant Investor Deck, and have hammered the 2028 cliff on the podcast circuit ever since. The thesis hasn’t changed. I think Q1 just handed me the receipts.

The Fix Is Unglamorous: Harvest, Don’t Reinvest

The prescription I have laid out for every melting ice cube — what I call “Project Turn the TV Off” — is simple and unglamorous: stop reinvesting in the decline, preserve and harvest the cash, run the legacy networks as an explicit wind-down or yield-co, and sell the genuinely good assets to private buyers who can actually use them. The strategy has to be to exit, not to tread water or expand.

Versant’s management is doing the precise opposite. Instead of dismantling, they are empire-building — feeding capital into a “growth” narrative to camouflage the core decline. The 2025 / 2026 deal log is a parade of tiny bolt-ons dressed up as a transformation: StockStory, Free TV Networks, a SAG Awards live-programming partnership, and INDY Cinema (quietly rebranded into Fandango). That last one is the tell — they buried the acquired INDY Cinema revenue inside the Platforms bucket, which is exactly how you manufacture a “+9.1% organic” headline that is partly just an acquisition.

They even scrubbed the golf KPIs from their reporting. Remember when Versant disclosed 40 million annual rounds and $4 billion in payments at the December 2025 Investor Day? We have not gotten any updates since. I think management is not sharing the golf business KPIs because those numbers stopped flattering the story, and they don’t want investors to notice.

Versant Is A Bad Bundle Wrapped Around Two Hidden Gems

Here is the framing that matters for the sum-of-the-parts. Versant is a Bad Bundle wrapped around a couple of Hidden Gems. The Bad Bundle — USA Network, E!, SYFY, Oxygen and MS NOW — throws off real cash today, but these are terminal-value-zero assets: renting sports, shedding audiences, and walking straight toward the 2028 cliff. The Hidden Gems — CNBC and GolfNow — are genuinely valuable franchises that would command a real multiple from a focused private buyer. But trapped inside this conglomerate they are suffocated: lumped into opaque buckets, starved of disclosure, and used as narrative props for a melting core.

Conclusion: Versant Is Dead Money Until the Strategy Flips

Einhorn is a brilliant investor and Versant stock is optically cheap — I’ll grant him both. But “cheap” is not a thesis, and a high FCF yield is only a gift if the cash flow shows up the way the model promises.

I still believe the evidence strongly favors the bears. I am reaffirming my Underperform rating on Versant ($VSNT) vs. the S&P 500. The day I wake up to a real reorganization plan, instead of another bolt-on, I will happily change my mind. Until then, I am perfectly comfortable being early — and being on the opposite side of a pitch from one of the game’s best value investors. I will continue to focus on exactly where this company’s true earnings power is headed, regardless of who is buying or selling the stock today.

VSNT 0.00%↑, DIS 0.00%↑, AMZN 0.00%↑, NFLX 0.00%↑

— Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.

Great catch on the Kardashian library masking the revenue decline.If we accept a faster decay curve, how does that defeat the near-term equity math? With a 19% FCF yield, zero debt maturities until 2031, and a newly launched $100M ASR, doesn't aggressively retiring the float at a 3.1x EBITDA multiple create massive per-share value over the next 3 years regardless of the terminal asset value?

Very interesting.

Do you think the management of Versant is incompetent optimists, or do they know that what they are saying is BS and just want to stay as long as possible to collect fat paychecks?