The Pitch-Mas Shorts Went 6-for-6: My H1 2026 Scorecard (Pt.1)

Accrued Interest is the #1 short-selling newsletter for value investors. The S&P 500 rallied +9.51% in the first half of 2026; my six December shorts declined an average of -29.43%.

Accrued Interest TLDR: Ahead of the July 22 paid launch, I am taking a victory lap and planting a flag: Accrued Interest is the best value investing, short-selling newsletter on Substack. Of the twelve stocks I pitched in December’s 12 Days of Pitch-Mas, seven calls have gone my way so far — but the record I am most proud of is going 6-for-6 on the short side. While the S&P 500 rallied +9.51% in the first half, my six shorts averaged a -29.43% absolute decline, and every single one lagged the benchmark by at least 21 percentage points. Today I revisit each December thesis and preview what the second half holds. Pledge before July 22 to lock in the $199/year founding rate for life.

0. Accrued Interest Is the Best Short-Selling Value Investing Newsletter on Substack

Scan the modern financial newsletter ecosystem and the reality is stark: the vast majority of publications exist to operate as perma-bulls, riding market beta and telling readers which stocks are guaranteed to go up. It is an echo chamber of consensus thinking.

I started Accrued Interest because I saw an opening in the market for true contrarians. When I began writing publicly a little over a year ago, I did not expect to make so many short calls — but I pride myself on being a contrarian and a rigorous thinker, and I let the process find me the opportunities. Today, this is the number one value investing newsletter on Substack when it comes to identifying, researching, and breaking down actionable short ideas.

Too many writers mistake beta for alpha. And most sell-side analysts at the big banks are afraid to publish an “Underperform” out of fear that management teams will stop taking their calls. My research process is 100% independent — I answer to no institution and worry about no corporate politics. The core differentiator of Accrued Interest is an unyielding commitment to a deeply researched, contrarian point of view, backed by deep-dive video analysis.

My North Star is simple: to beat the market, you have to avoid business models that are weak or prone to underperformance. The first half of 2026 proved the process works.

Identifying six idiosyncratic losers across different sub-sectors was not a lucky macro bet. The S&P 500 rallied +9.51% during the first six months of the year. Meanwhile, the six short/Underperform picks from my 12 Days of Pitch-Mas series averaged a -29.43% absolute decline. Every single pick underperformed the benchmark by a minimum of 21 percentage points. That is true alpha.

And crucially — no shade to other writers (cough, cough) — several of these underperformers were consensus favorites pitched as high-conviction longs by some of the biggest and most popular writers on this very platform. The broader market loves an easy growth narrative. But a narrative will not protect capital from structural decay.

The market desperately needs more analysts willing to step outside the safety of consensus. If you want intellectual diversity in your newsletter diet — and my honest take, always — please pledge your subscription today and support true diversity of thought.

In the spirit of intellectual honesty: this scorecard is only half the story. A Part 2 deep dive is coming where I grade my six long picks — five of the six trailed the market, mostly casualties of the macro sell-off in big tech after a blistering rally to end 2025. Subscribe and you will get those breakdowns too.

Now for the detailed scorecard.

Now let’s go through them one by one — grouped by theme, starting with the biggest decliner in each group and working down. For each name, I will start with what I actually wrote in December, receipts first, then break down how the thesis played out.

The Illusion of Growth: Tech & Platforms

1. Fubo ($FUBO): The Death Spiral Arrived Ahead of Schedule

From the December pitch (Day 8 of Pitch-Mas):

“All 2025, I argued FuboTV was a subpar business destined to trail the market. Now, looking ahead to the media landscape of 2026, I do not think it is out of the question to ask a more fundamental question: Does FuboTV have a reason to exist much longer?”

The Scoreboard:

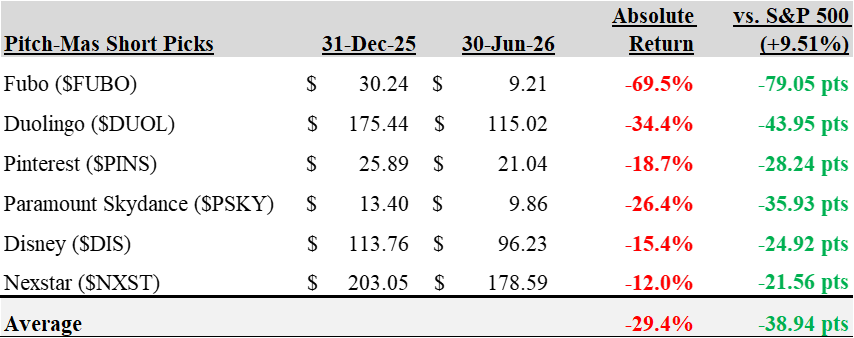

Price on Dec 31, 2025: $30.24

Price on Jun 30, 2026: $9.21

Absolute return: -69.54%

Underperformance vs. S&P 500: -79.05 points

This was the biggest winner on the short side; it is rare when a thesis plays out almost exactly as you expect. I flagged early on that virtual MVPDs suffer from structurally broken economics: operating as a middleman for aggressively priced sports and broadcast rights leaves virtually ZERO margin for error, and certainly no room for free cash flow generation. Every new subscriber is essentially a loss leader — one more weight on an albatross of a business with no real path to profitability.

Layer on the high-cost churn cycle — users acquired at high cost who cancel the moment promotional pricing ends or the NFL season concludes — and you have a treadmill of unprofitable customer acquisition. Without the capital backstops or bundling power of the legacy media giants, sub-scale players simply lack the leverage to negotiate sustainable carriage deals. I called it the sub-scale death spiral in December. The market caught up quite early in Q1.

Management tipped their hand to the underlying distress in March, executing a desperate 1-for-12 reverse stock split done strictly to artificially inflate the share price and avoid getting kicked off the New York Stock Exchange. As I said at the time: financial engineering is not a business strategy.

One aside: I received the most negative feedback on Twitter whenever I posted about Fubo. For reasons I will never understand, Fubo has a loyal army of Twitter trolls who appear to be addicted to pain. Part of why I opened my subscriber-only chat here on Substack was to have honest debates without feeding the trolls.

With the thesis fully realized, I officially discontinued coverage of Fubo this spring. That freed up research bandwidth for initiating coverage on a far more compelling situation — the combined Fox and Roku entity, which actually controls a dominant connected-TV distribution chokepoint rather than renting one.

The Accrued Interest Take: Thesis complete. Coverage discontinued. The best thing I can say about Fubo is that it made room on my coverage list for Fox + Roku.

2. Duolingo ($DUOL): The Market Finally Priced the Owl Like a Mobile Game

From the December pitch (Day 9 of Pitch-Mas):

“While it still trades at an expensive growth multiple, Duolingo’s business model resembles an addictive mobile game, not a scalable educational service. This structural flaw limits monetization and future profit margin expansion. Compounding this are existential AI disruption risks and a growing reliance on lower-value international users.”

The Scoreboard:

Price on Dec 31, 2025: $175.44

Price on Jun 30, 2026: $115.02

Absolute return: -34.44%

Underperformance vs. S&P 500: -43.95 points

Let me start with a confession. I held off coming out publicly against Duolingo, partly because there were MANY Substack writers — some of whom I respect — publishing long reports on the name. Rather than argue in the comments, I decided to let my research do the talking.

And boy, am I glad I changed my mind.

Because what I learned in time is that many investors fundamentally misunderstood this business. The market was assigning a premium EdTech multiple to what is essentially an addictive, unscalable mobile game. Investors thought they were buying a scalable learning platform; in reality, they were buying fleeting screen time that faces competition on multiple fronts.

The December thesis mapped out the structural monetization hurdles the company would inevitably hit, and the prediction that they would slam into a wall on paid conversions proved accurate. I went deeper on the post-mortem in my February deep dive, Deflating the Duolingo ($DUOL) Owl, after Q4 results confirmed the cracks. Management’s subsequent pivot away from aggressive monetization toward chasing low-value free user growth was a glaring red flag — it signaled a fundamental breakdown in the long-term profitability story and confirmed the loss of pricing power.

I think the long-term bear case remains anchored in technology. The looming, existential threat of seamless AI-driven translation is actively neutralizing the core utility of app-based language learning, permanently stripping away whatever pricing power the company might still claim.

One note of intellectual honesty, because I flagged it in real time back in March: after the stock’s first-quarter collapse, I wrote that much of the bearish case had already been priced in and that I was not necessarily expecting another sharp leg down. The stock has chopped around since. But until I see acceleration in the KPIs that matter — paid conversion, ARPU, bookings — I expect continued underperformance against the S&P 500, despite the forever-optimism of the bulls.

The Accrued Interest Take: Maintaining Underperform. The gamification wall is real, and the AI translation threat is not going away. I would not be surprised to see Duolingo rally for a quarter or two coming out of earnings. However, I cannot assign an above-market P/E multiple to a business with a paid user base that cannot scale.

3. Pinterest ($PINS): The Value Trap Sprung — Now Elliott Is Building the Exit Ramp

From the December pitch (Day 10 of Pitch-Mas):

“I am predicting Pinterest will underperform the market for 2026 because the stock is a value trap. Despite having optically healthy financials, the business has reached a growth plateau because its user mix is increasingly shifting towards international markets that monetize at a fraction of what they earn from an American or European user. In addition, Pinterest faces the risk of being a long-term ‘AI loser.’”

The Scoreboard:

Price on Dec 31, 2025: $25.89

Price on Jun 30, 2026: $21.04

Absolute return: -18.73%

Underperformance vs. S&P 500: -28.24 points

My Q4 follow-up peeled back the layers on the user metrics and revealed weak top-line growth. Pinterest’s aggressive international expansion keeps adding users who monetize at pennies on the dollar compared to the domestic base. That flood of “empty calories” is diluting overall ARPU and masking domestic stagnation. Meanwhile, shifting digital discovery habits and the accelerating threat of AI search disruption keep eroding the legacy social curation model. Today, I believe the structural thesis is intact.

But here is where the story changed. In Q1, Elliott Management injected a $1 billion strategic investment via convertible notes, triggering a large share repurchase program. And Elliott is not holding this position indefinitely. Their heavy presence all but guarantees they are forcing value creation and dressing the company up for an eventual take-private transaction or an outright acquisition to cleanly exit their position.

A structurally challenged stock can still violently pop when an activist gets involved. That asymmetry means Pinterest can no longer safely be held as a short.

The Accrued Interest Take: I am officially removing the Underperform rating and upgrading Pinterest to Market Perform. The business remains structurally challenged, but with Elliott engineering an exit ramp, the risk/reward on the short side is gone. Take the win.

The Legacy Media & Linear Traps

4. Paramount Skydance ($PSKY): The Anatomy of a Doomed Merger

From the December pitch (Day 2 of Pitch-Mas):

“Investors were overly optimistic that a Paramount Skydance bid for Warner Bros. Discovery was a foregone conclusion, neglecting to account for the regulatory risks... Paramount’s vertically integrated structure, unlike NFLX, would invite horizontal antitrust scrutiny concerning theatrical market concentration and the consolidation of news outlets CNN and CBS.”

The Scoreboard:

Price on Dec 31, 2025: $13.40

Price on Jun 30, 2026: $9.86

Absolute return: -26.42%

Underperformance vs. S&P 500: -35.93 points

This was a deeply contrarian call — an Underperform put on directly in the midst of a $111 billion mega-merger, when the M&A hype machine was running at full throttle. The core lesson is one I will keep repeating: bolting two heavily indebted, legacy-burdened companies together does not magically fix a structurally impaired business. Mergers cannot save a flawed foundation.

The market was starved for a dissenting opinion that cut through the noise. My March deep dive detailing the eight specific reasons this merger was dead on arrival remains the single most-read piece in the history of Accrued Interest.

The weaknesses exposed in the original thesis — horizontal antitrust risk, monumental regulatory hurdles, and a crushing debt load that will strangle the combined entity’s ability to invest in streaming — remain the driving forces of the stock’s decline. And the broader market clearly shares these reservations. Despite Paramount Skydance raising its takeover offer for Warner Bros. Discovery to $31 per share, WBD currently languishes around $26. That wide spread tells you definitively that institutional capital expects severe value destruction, regulatory blockades, or both.

The Accrued Interest Take: Maintaining Underperform. The deal spread is the market’s verdict, and for now, it still agrees with mine.

5. Disney ($DIS): The Albatross of Linear TV Is Still Around Its Neck

From the December pitch (Day 6 of Pitch-Mas):

“My core thesis is that Disney’s television networks division is too great a burden for the company to outperform the S&P 500. I consider a spin-off of Disney’s linear broadcast and cable channels to be inevitable.”

The Scoreboard:

Price on Dec 31, 2025: $113.76

Price on Jun 30, 2026: $96.23

Absolute return: -15.41%

Underperformance vs. S&P 500: -24.92 points

Unlike Fubo, this was not an overnight blow-up. Disney is a textbook case of agonizing, long-term structural underperformance. The company continually looks “cheap” on a historical basis, luring in retail investors, but because the fundamental business mix is structurally impaired, it serves as the ultimate value trap.

Bob Iger’s departure as CEO on March 18, 2026 — handing the reins to Josh D’Amaro — serves as a telling measuring stick. Despite the relentless media reverence for Iger’s leadership, the undeniable reality of the stock chart shows systematic underperformance against the broader market over the course of his combined tenure.

Even more important for the thesis: as I noted in recent Accrued Interest Daily updates, the new CEO has explicitly stated he is NOT looking to separate the television businesses. That stubborn commitment to a dying medium means the exact structural issues I identified during Pitch-Mas are locked in for the foreseeable future. Streaming margins simply cannot replace the rapidly eroding profits of the traditional broadcast and cable bundle. Management is delaying the inevitable.

The Accrued Interest Take: Maintaining Underperform. Until leadership capitulates and separates the linear businesses, expect the stock to keep drifting below the benchmark.

6. Nexstar ($NXST): Broadcast Decline, Now Trapped in Legal Limbo

From the December pitch (Day 4 of Pitch-Mas):

“I am still bearish on Nexstar because the problems facing broadcast TV — people ditching cable for services like YouTube TV — are only going to get worse. After they buy Tegna, Nexstar will be the biggest player, which means they will be the most exposed to all these industry headaches... The stock is likely to be dead money until late 2026.”

The Scoreboard:

Price on Dec 31, 2025: $203.05

Price on Jun 30, 2026: $178.59

Absolute return: -12.05%

Underperformance vs. S&P 500: -21.56 points

I pitched this short right in the middle of a blockbuster $6.2 billion acquisition of TEGNA. Wall Street bought the promise of cost synergies and increased scale. The contrarian view correctly diagnosed that consolidating scale in a shrinking linear ecosystem is just rearranging deck chairs on the Titanic.

What the market badly mispriced was the regulatory reality. As I have highlighted in recent Accrued Interest Daily updates, a coalition of state attorneys general launched lawsuits directly targeting the acquisition, successfully freezing the integration process. Nexstar is now legally prohibited from executing on the very cost synergies they pitched to Wall Street. Their entire growth strategy is trapped in indefinite legal limbo, suffocating any potential value creation.

And there is a newer, bigger headwind emerging: political uncertainty. FCC Chair Brendan Carr has launched an aggressive campaign challenging the broadcast licenses of Disney-owned ABC stations over editorial decisions and programming. This unprecedented level of government interference creates a chilling effect that hurts the valuation of all broadcasters. If owners become terrified that the government will interfere with what airs on the public spectrum, they will hoard their highest-quality, most profitable content and move it exclusively to unregulated cable and streaming platforms. Should premium content flee over-the-air broadcast, legacy broadcasters like Nexstar will be left holding an empty vessel of low-margin filler — impairing the sprawling portfolio of local stations they are currently trapped trying to acquire.

The Accrued Interest Take: Maintaining Underperform. The melting ice cube now comes with a legal freeze on the only lever management had left.

CONCLUSION

Six calls, six wins. The shorts gave back an average of 29% in a tape that climbed nearly 10%. That is not beta. That is not luck. That is the product of doing the work — reading the filings, building the models, and having the conviction to publish a dissenting view while the consensus was pitching these same names as can’t-miss longs.

And as promised, transparency cuts both ways. Part 2 of this scorecard will cover the long side of the Pitch-Mas ledger, where the first half was far less kind. I still consider those names good buys, and I will explain why in the next edition.

One housekeeping note: Accrued Interest officially launches paid subscriptions on July 22. The Founding 100 pledge window — which locks in the Portfolio Manager tier at $199/year for life — is open now, and the subscriber chat is running as a free open house until launch day. If independent contrarian thinking is the kind of research you want in your corner for the second half, now is the time.

More to come — stay tuned 👀

-Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.