Deflating the Duolingo ($DUOL) Owl

A Pitch-Mas prophecy fulfilled: Why this overhyped mobile game is finally running out of lives.

Accrued Interest TL/DR: I break down why Duolingo ($DUOL) plummeted 25% after its disastrous Q4 2025 earnings. As I predicted in December, Duolingo is ultimately an unscalable mobile game, not a premium educational service. With paid conversion stalled at just 9%, management is now actively pivoting away from monetization to chase free users, accepting a massive, deliberate hit to near-term profitability and margins. I am maintaining my ‘Underperform’ rating. The illusion of sustainable margin expansion is broken, and I see another 20% to 29% downside as the stock’s massive growth multiple continues to compress.

Back in December, during Day 9 of our “12 Days of Pitch-Mas” series, I laid out a bearish thesis on Duolingo ($DUOL), rating the stock an Underperform. My argument was straightforward but highly contrarian at the time: Duolingo was priced for absolute perfection. Beneath the massive earnings multiple, I argued that the company’s business model resembled an addictive mobile game much more than a truly scalable educational service.

Because of that structural reality, I warned that the company would never be able to improve its monetization or expand its profit margins enough to satisfy growth investors. I predicted the stock’s multiple would contract as the market realized the low-hanging fruit had already been picked.

Now, I’ll be perfectly honest—I did not expect to take a victory lap this quickly.

But fast forward to this week’s Q4 2025 earnings release, and the stock plummeted 25% on the heels of the report. Overall, it is down -43% YTD, underperforming the S&P 500 (which is basically flat YTD at +0.26%) by over 43 percentage points.

So, what exactly spooked the Street so badly? Let’s pull apart the DUOL 0.00%↑ Q4 numbers and management’s startling 2026 guidance to see exactly why this was a classic value trap—and why the bleeding might not be over yet. Let us dive into the wreckage.

1. The Pivot: Shattering the Bull Case

The Q4 report was not just standard earnings miss; it was a fundamental shift in the company’s narrative that completely shattered the prevailing bull case. For years, bullish investors justified the stock’s premium valuation by pointing to high free cash flow conversion and the assumption of an ever-improving rate of converting free users to paid subscribers.

But the latest figures, combined with management’s startling 2026 guidance, prove that the monetization engine is stalling. During the release, management dropped a series of strategic bombs:

The Monetization Chokehold: Management openly admitted that the deceleration in user growth throughout 2025 was partly a function of their “increased focus on monetization” in recent years.

The Growth Pivot: In response, they are initiating a deliberate strategic pivot to prioritize user growth and the free learner experience over aggressive monetization.

The Profitability Penalty: Management explicitly warned investors that this strategy will “lower our financial results in the short term,” directly sacrificing bookings growth and crushing near-term profitability.

The honeymoon phase of effortless growth and margin expansion is officially over. Let us dig into the exact Key Performance Indicators (KPIs) from the Q4 report that validates every structural flaw we highlighted back in December, and why this strategic pivot is a massive red flag for the company’s long-term unit economics.

2. The Illusion of Conversion: A Paid User Plateau

As we often discuss here on Accrued Interest, when evaluating a freemium model, user growth is only half the equation. The true test of a business’s durability is its ability to effectively convert free users into paying subscribers. In my December preview, I noted that Duolingo’s paid penetration rate was barely inching up—sitting around 9.0% in Q3 2025.

The Q4 2025 results proved that this metric has effectively hit a wall. Here is exactly what the top-of-funnel decay looks like in the data:

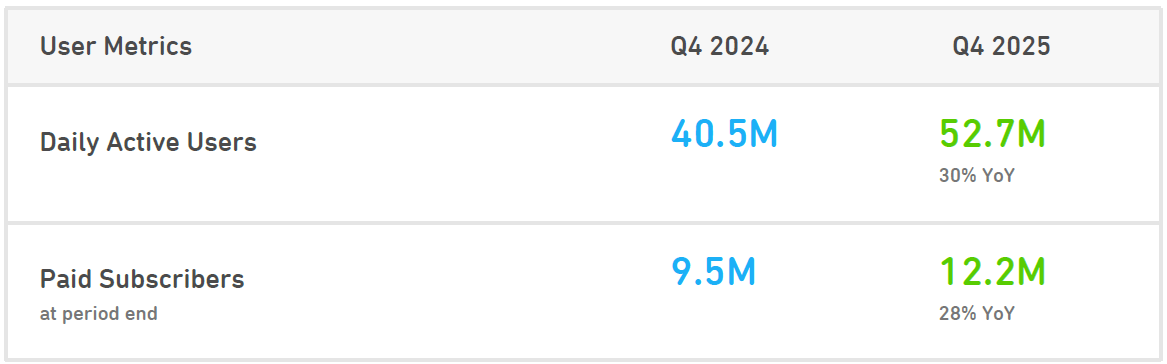

DAU vs. Paid Growth Disconnect: While Daily Active Users (DAUs) grew an impressive 30% year-over-year to 52.7 million, Paid Subscribers lagged, growing only 28% year-over-year to 12.2 million.

The 9% Ceiling: The paid penetration rate remains stubbornly stuck at approximately 9.1% (12.2 million paid subscribers on 133.1 million Monthly Active Users).

The Valuation Reality Check: The company simply cannot convert its massive user base fast enough to justify the astronomical growth multiple the market had assigned it.

Even more damning, management effectively threw in the towel on pushing for higher conversion. By admitting that pushing users to pay was actively choking off top-of-funnel growth, they acknowledged a structural ceiling. In other words, you cannot aggressively squeeze a mobile game disguised as an education app without eventually driving the casual free players away.

3. The Strategic Pivot (Or, The Growth Penalty)

Faced with a stalling conversion engine and decelerating user growth, management announced a massive strategic pivot for 2026: they are deprioritizing monetization to focus on the free learner experience. The goal is to reach 100 million DAUs by 2028. However, the financial penalty for this pivot is brutal.

Several KPIs and financials in the Q4 results and 2026 guidance provided the hard data that triggered the -25% stock drop. The reality perfectly captures the whiplash between Duolingo’s peak monetization performance in 2025 and the massive financial penalty they are taking to chase their new 2026 user growth strategy:

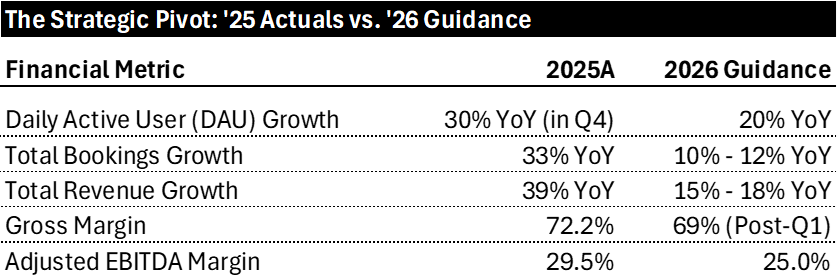

Decelerating User Growth: Despite abandoning monetization to focus entirely on user growth, top-of-funnel growth is still expected to decelerate by a third. DAU growth fell from 51% in Q4 2024 to 30% in Q4 2025. Management expects 2026 DAU growth to slow further to approximately 20%. CEO Luis von Ahn admitted that the 2025 deceleration was partly due to an “increased focus on monetization in recent years”.

The Bookings and Revenue “Reset”: Growth is collapsing. Management explicitly admitted they are sacrificing potential growth to fund this pivot. Revenue growth is being more than cut in half as the conversion engine is deliberately cooled down. Total bookings growth was 24% in Q4 2025. Management guided for only 10%–12% bookings growth for FY 2026. They noted that bookings could have grown by 20% if they had continued to operate as they had in previous years by focusing on monetization.

Profitability and Margin Compression: Margin expansion has hit a hard ceiling and reversed. The lack of operating leverage means subsidizing free users compresses overall profitability. Gross margins are expected to drop to roughly 69% for the remainder of 2026 due to the costs of offering AI features to a wider, free user base. Expanding expensive, AI-powered features to a larger base of non-paying users is structurally destroying gross margins.

The “Double Whammy” is that Duolingo is paying a massive price in profitability and bookings, yet they still expect DAU growth to slow down to 20%. They are sacrificing their margins but not actually accelerating their user base. Adjusted EBITDA margin is expected to decrease to 25% in 2026, down from 29.5% in Q4 2025.

4. Key Commentary on Monetization & Strategy

Management’s comments during the earnings cycle emphasized that they are essentially “buying” future users at the expense of current margins.

“The short-term implication is that this year will see slower bookings growth and lower profitability... I believe this is the right course to take.”

“We’ll focus on improving the free learner experience to grow word of mouth and feed our next user growth engines like chess, math and music, even though that moderates near-term financial growth.” — Luis von Ahn, CEO

That follow-up answer directly validated my “Profit Margin Plateau” and “Lack of Operating Leverage” bear arguments from December. The company is choosing to subsidize free users with expensive AI compute (Video Call, etc.) and marketing spend, leading to the exact multiple contraction I predicted.

In December, a core part of my thesis was that I could tell DUOL was a mobile game because the high R&D spend was just sales and marketing by another name. A game is an inherently shaky business model because eventually players run out of gas and stop playing. Therefore, as a mobile game, it should trade at a discounted multiple compared to the S&P 500. Still today, Duolingo trades at a slight premium to the market, which is not deserved.

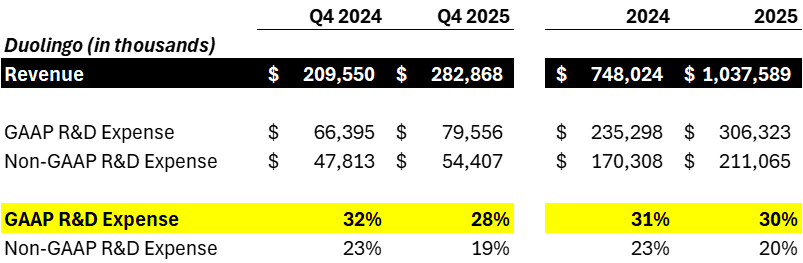

I see the same issues with the updated Q4 and FY 2025 numbers: R&D spend is unsustainably high for a company hoping to expand its margins. In Q4 2025, R&D expense as a percentage of revenue dipped slightly vs. last year, from 32% to 28%. However, for the full year, the FY 2025 ratio of 30% of sales was almost the same as last year’s 31%.

5. Valuation — DUOL is Still Not Cheap

The reason DUOL stock has underperformed the market YTD is because of severe multiple compression. In my December Article, DUOL traded at 43x 2026 GAAP EPS and 24x 2026 adjusted EPS. The math checks out: the multiple dropping from 43x to 24x is a 45% decrease, which roughly matches the stock’s return.

Analysts are still updating their estimates post-earnings (these may go lower), but based on median estimates as of 2/27 in the AM:

● GAAP EPS: $4.19 in 2026, and $5.23 in 2027.

● Non-GAAP EPS: $7.20 in 2026, and $9.52 in 2027.

With the stock rounded to $100 per share the day after earnings, it is trading at:

● GAAP EPS Multiple: 24x for 2026, and 19x for 2027.

● Non-GAAP EPS Multiple: 14x for 2026, and 11x for 2027.

While there are legitimate times to use Non-GAAP EPS or make other adjustments, this situation with DUOL is not one of them. The reason for the massive delta is Stock-Based Compensation (SBC). When the stock price is going up, this is easily ignored. But when the KPIs and other metrics go sideways or down, you absolutely must focus on GAAP EPS.

6. Reflections from a Value Trap Hunter

Shorting is notoriously brutal—stocks naturally drift upward, and publicly calling out a beloved consumer darling like Duolingo as a value trap is a quick way to invite ridicule. Seeing respected writers fiercely defend the stock made me double-check my math, but the numbers didn’t lie.

Here is the truth about hunting value traps: you rarely need a smoking gun. The best shorts aren’t born from explosive catalysts; they come from the slow, agonizing bleed of multiple compression. Bulls get caught in the trap because they fixate on consensus estimates holding steady, completely ignoring the structural rot underneath.

My thesis was never about predicting a single bad quarter. It was about an investment model hitting a brick wall. When I look for shorts, I hunt for companies operating near their absolute ceiling, yet carrying a valuation that demands an impossible level of future profitability. The bet was simple: as the broader market slowly woke up to the reality that Duolingo is an unscalable mobile game, the multiple would collapse under its own weight.

And that is exactly what we are watching play out.

CONCLUSION

Even at $100 a share, the bleeding isn’t over. DUOL is still clinging to a premium 2026 P/E multiple for a business model that has fundamentally stalled. Nothing in this earnings report suggests a turnaround is imminent—in fact, management just explicitly promised the opposite.

I don’t deal in hyper-precise price targets, but I fully expect DUOL to contract to a discounted multiple of 17x to 19x this year’s GAAP EPS to accurately reflect its structural limitations. That puts the stock in the $71 to $80 range, implying another 20% to 29% downside from current levels.

I’ll be tracking the wreckage closely in the coming months, but for now, the DUOL 0.00%↑ bull case is broken.

-Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.

An intersting view - I'm a Duolingo shareholder and now wondering whether this is a hamster wheel or a value creator.