Gulf Capital Cannot Save Paramount, Einhorn is Dead Wrong on Versant, and Nielsen Caved to Streamers (Accrued Interest Update 4-14-2026)

$PSKY, $WBD, $VSNT, $CMCSA

Today, I am looking at how foreign money is trying to prop up legacy media, while some of the sharpest minds in finance are still falling for value traps in the cable ecosystem. In this update, I am breaking down the massive influx of Saudi capital into the Paramount-Warner Bros. Discovery megamerger, and why it ultimately will not save the company. Then, I am pivoting to David Einhorn’s recent bullish bet on Versant, and why I believe he is completely misreading the long-term structural risks of the business. Finally, I will touch on the drama behind Nielsen’s delayed February Gauge report.

Please subscribe to read the rest of the Accrued Interest Daily Update - for April 14, 2026.

Please subscribe to read the rest of the Accrued Interest Daily Update. My objective is to grow this into a premier TMT research platform, and securing your subscription today ensures you maintain uninterrupted access to my ongoing analysis.

A) Gulf Capital Cannot Save Paramount

The details behind the financing of the massive Paramount Skydance and Warner Bros. Discovery merger are finally coming to light, and it should not come as a surprise if you have been following my coverage here on Accrued Interest. According to a recent cover story by The Hollywood Reporter, Saudi Arabia and other Gulf states are pouring billions into the Ellisons’ takeover, with sovereign wealth funds from the region contributing around $24 billion to the deal. Saudi Arabia’s Public Investment Fund alone is putting up approximately $12 billion of that total. This represents an incredible shift in how Hollywood is being bankrolled, but if you look past the sheer dollar amounts, the motivations become incredibly clear.

This is not simply a soft-power play designed to rebrand the image of the Kingdom in the West. As The Hollywood Reporter’s deep dive into the transaction highlights, this strategy is ultimately about courting political influence in Washington and giving a young, restless domestic population “bread and circuses” to distract them from political participation and human rights concerns. The benefit of having this foreign money backstopping the new media conglomerate is that these sovereign funds ultimately do not care about the day-to-day stock price. I have long suspected this was the case, and the recent reporting makes it explicitly clear: they are there for the power, the proximity to American media infrastructure, and the political influence.

However, the public is absolutely right to be concerned about these developments. American viewers deserve to know exactly what entities are funding and controlling the media they watch, particularly when it comes to vital news organizations like CNN and CBS News. Despite these looming regulatory and political vulnerabilities, I am not banking on the new PSKY/WBD being broken up if there is a shift to a different presidential administration in the upcoming years. For now, my base case is that the combined company continues exactly as it is.

Foreign Capital Cannot Overcome Shifting Audience Trends

But structurally, PSKY is deeply troubled. As I have said elsewhere on Accrued Interest, financial engineering and sovereign wealth cannot force viewers to tune in. The audience ultimately decides who wins. No matter how many billions the Saudis or other wealthy investors pump into this legacy portfolio, audience trends are rapidly and permanently moving away from the linear content that PSKY and WBD rely on, shifting heavily toward Netflix and user-generated content on YouTube. They are outgunned in the streaming wars, and a massive war chest of foreign capital cannot reverse a secular decline.

Relevant Accrued Interest articles on PSKY 0.00%↑ and WBD 0.00%↑:

2026.04: CBS Rents Out Late-Night, Netflix’s Danny Go! Distribution (Accrued Interest Update 4-7-2026)

2026.03: Dead on Arrival: 8 Reasons the Paramount-WBD Merger Will Fail

B) David Einhorn’s Versant Thesis Ignores the 2028 Cliff

Over in the value investing world, the first-quarter letters are starting to drop, and I noticed that David Einhorn’s Greenlight Capital has initiated a new, medium-sized position in Versant. (I must explicitly state here that I have not yet obtained a full digital copy of David Einhorn’s Greenlight Capital letter, so if any readers have one floating around their inbox, please send a digital copy my way!) Greenlight’s stated rationale is that while the legacy cable business is facing ongoing cord-cutting, over 60% percent of Versant’s programming is tied to live news and events. In their view, this makes the portfolio much more resistant to subscriber losses than general entertainment networks.

I strongly disagree with Greenlight’s thesis here. If you truly believe that news and sports are core to the Versant investment case, then you should be extra concerned about their impending separation from the NBC Universal family. As I detailed during my recent appearance on the Yet Another Value Podcast, Versant’s financials are currently over-earning because they operate under the protective halo of the NBC ad sales department. Their sports portfolio is essentially a collection of leftover rights that NBC did not have room for on its main broadcast network. When that umbilical cord is permanently cut in 2028, Versant is going to lose immense leverage in carriage negotiations with pay-TV providers, and their sports rights are going to be severely devalued on the open market.

I admit that I was genuinely surprised to see Versant’s stock rally recently, currently trading back up around $41 per share. When I originally pitched the stock as an underperform, it was trading around $34 and was suffering from a wave of forced, indiscriminate selling. It looks very much like Einhorn, and I would assume a few others, stepped in to buy this as a deep value or special situations play.

The reality is that the stock looks optically cheap based on 2026 and 2027 estimates, but the massive risk waiting in 2028 has not disappeared. I am perfectly fine if the broader market does not agree with me in the short or medium term. At the end of the day, I will stick to my analytical process and point out exactly where a company’s true earnings power is headed, regardless of who is buying the stock today.

Relevant Accrued Interest articles on VSNT 0.00%↑ and CMCSA 0.00%↑ :

2026.03: Interview: Yet Another Value Podcast and the Shifting Media Landscape

2026.01: Is Versant (VSNT) Worth More Dead Than Alive?

2026.01: Is Versant (VSNT) Cheap or Just Cheaply Valued? The Case for $27

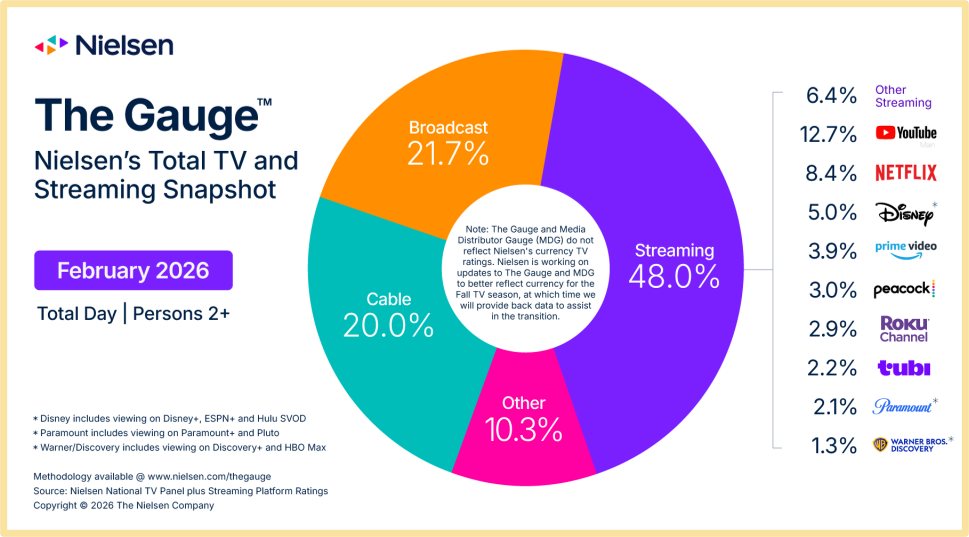

C) Nielsen’s Delayed Gauge Report Reveals Industry Paranoia

Nielsen is finally out with their latest Gauge report covering February 2026 TV viewership, and I will be doing a full, rigorous deep dive on this data just as I have in the past with my monthly series. Before we look at the numbers, you have to understand the drama behind the delay. Nielsen was originally supposed to release this report weeks ago, incorporating new data from the Advertising Research Foundation (DASH) to better track how households actually consume digital video. However, when clients realized this new methodology was going to show a sharper-than-expected decline for streaming view share—and a bump for legacy broadcast and cable—there was an industry uproar. Rather than stand by the new data, Nielsen caved to the complaints of tech giants and streamers, pausing the methodological updates until the fall to “minimize trend breaks”.

As for the actual takeaways using the old methodology, February was completely dominated by live events. Unsurprisingly, the Super Bowl and the Milan Cortina Winter Olympics were massive windfalls for NBCUniversal and Versant. The two companies combined for 13.1% of all TV viewing, officially dethroning YouTube to take the top spot on the Media Distributor Gauge. Over on the streaming side, Peacock had an astronomical month, jumping 64% in viewership to capture a record 3% share of all TV time, heavily driven by its simulcast of the Super Bowl.

Relevant Accrued Interest articles on Nielsen / TV viewing trends:

2026.02: Media Stock Insights from Nielsen’s Jan-26 TV Snapshot

2026.01: Media Stock Insights from Nielsen’s Dec-25 TV Snapshot

-Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.