Fox + Roku Part 3: The 11x FCF Chokepoint

Part Three of an Accrued Interest Deep Dive on Roku’s Valuation

Accrued Interest TLDR: At today’s price of $135 for Roku, Fox is acquiring one of the most important streaming distribution assets in American television for roughly 11x to 15x 2028 free cash flow, counting the deal’s stated cost synergies and not assuming any revenue synergies to Fox. I get there by running three different scenarios for my 2028 Roku forecast, ranging from a pessimistic floor to a moderate integration case. And because 40% of this deal floats with Fox stock, the sell-off in FOX shares has compressed the price for Roku to about $19.5B in enterprise value. The market’s skepticism only makes the deal cheaper for Fox shareholders. Mr. Market is fixated on a 2027 closing timeline and an arbitrage spread, but neither tells you anything about what this asset is actually worth. Buying Fox equity today is the cheapest, most asymmetric way to own Roku’s future. For Part 3 of my Roku series, I am reiterating my Outperform rating on the pro forma Fox + Roku ($FOXA / $ROKU).

Please subscribe (free) to read the rest of this Accrued Interest deep dive. I send these to 1,400+ investors and operators who care more about what moves the needle than what the spreadsheet whispers.

From Strategic Logic to Hard Math

In Part 1, “Fox + Roku: A Brilliant Pivot from the Cable Bundle to the Living Room,” I walked through Fox’s strategic masterstroke: trading its reliance on the dying linear cable bundle for direct control over connected-TV distribution, right as CTV’s share of the TV ad pie raced past 40%. The Murdochs sold entertainment cable to Disney at the top in 2019, and they are deploying that capital into the dominant CTV platform at the bottom.

In Part 2, “The Strait of Roku,” I argued that Roku controls the definitive chokepoint of the living room. It is the front door to streaming for tens of millions of American households, the one piece of real estate where content discovery actually happens, and it has held that ground against Amazon and Google for over a decade.

Now for Part 3, I will give you my take on what I think Roku is actually worth, and why I think Fox is not overpaying.

Mr. Market has the valuation backwards, but the skepticism is understandable, and I want to be fair to it. This deal will not close until the first half of 2027. Bank of America’s Jessica Reif Ehrlich has a Sell on Fox and warned about a “catalyst gap,” the better part of a year where capital is tied up just to earn a single-digit arbitrage spread. As a trade, I understand the hesitation. But the arbitrage spread tells you nothing about what this asset is worth in 2028. The distance between what the market is reacting to today and the FCF this combined company will actually generate is the entire opportunity.

Now let me explain exactly why I am comfortable disagreeing with Mr. Market.

The Deal Got Cheaper While Nobody Was Looking

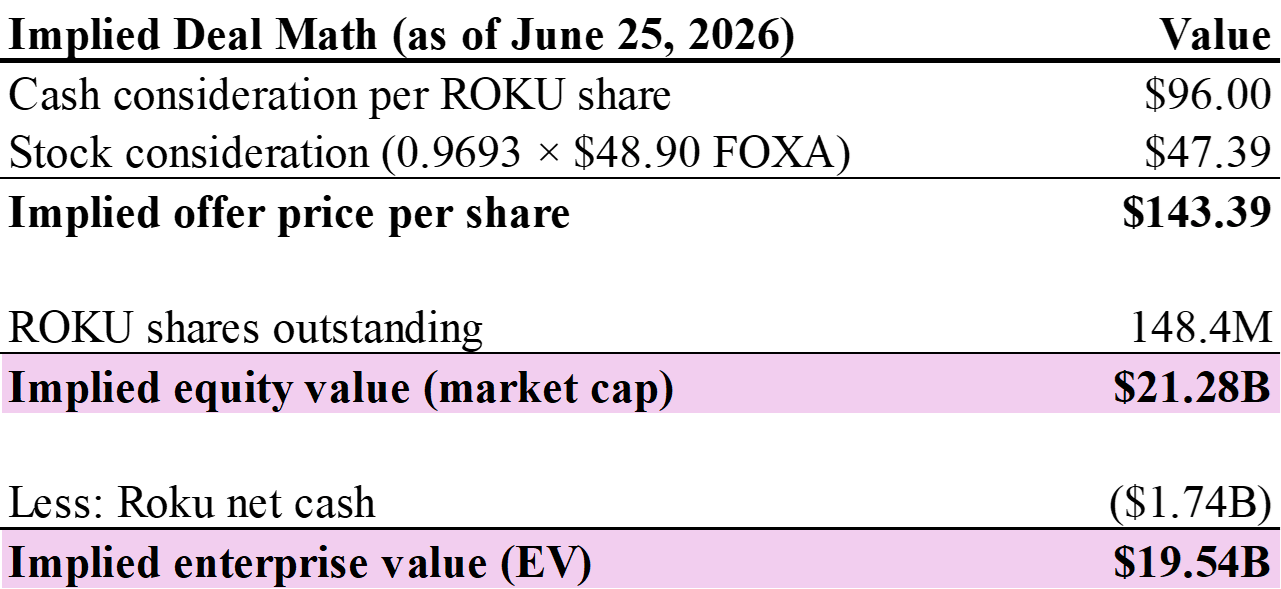

Let’s start with what Fox is really paying today, because the headline number is stale.

The deal was struck at $160 per Roku share, a roughly $22B enterprise value, financed 60% cash and 40% Fox stock. But 40% of the consideration floats with FOXA, and FOXA has kept falling. As of June 25, 2026, Fox trades at $48.90 and Roku at $135.01. Run the current math and the implied offer is no longer $160.

Roku is trading at $135.01 against a $143.39 implied price, which is your roughly 5.8% arb spread right there. Look at what has happened to the acquirer’s cost. Because Fox’s stock has sold off from its $66 reference price, the equity portion of the consideration has compressed, and Fox is now effectively acquiring Roku for about $19.5B in enterprise value instead of the $22B everyone keeps quoting. The acquirer’s stock falling has made the asset cheaper. That is the number every multiple in this piece runs against: $19.54B in implied EV, $21.28B in implied market cap.

I want to give Fox credit for how it structured the deal in 60% cash, 40% stock. Paying the majority in cash means Fox is not giving away the upside. Roku shareholders will own only about 27% of the combined company, which leaves roughly 73% of every future dollar of synergy and growth in the hands of Fox. Had Fox financed this entirely in stock, it would be handing a far bigger slice of the prize to the other side of the table.

And the 40% stock piece quietly does something else that is playing out in real time: it turns the purchase price into a floating number that falls when Fox stock falls. So the very sell-off that has investors nervous is, mechanically, lowering the effective price Fox pays for Roku. The market’s skepticism is discounting the deal for the buyer.

Across the three scenarios I am about to walk through, that roughly $19.5B price works out to somewhere between 11x and 15x the free cash flow this asset generates in 2028, before a single dollar of revenue synergy. Hold onto that range. It is the whole argument, and everything below is just me showing my work.

The Operator’s Lens: Three Scenarios for 2028

Before I show you the scenarios, here is the lens I built them through. I forecast this the way an operator would think about the business, from the segment level up, with conservative assumptions anchored to targets Roku management has already put on the record.

The engine of the entire model is Roku’s revenue mix.

Devices, the streaming sticks, are a deliberate loss leader that Roku runs at a negative gross margin to pull households into the ecosystem.

Platform, the advertising and subscription tollbooth, is where the money actually lives, at roughly 51% gross margins.

As the low-and-negative-margin hardware shrinks and the high-margin platform dollars grow, the blended margin expands on its own and falls straight to the bottom line. That is the whole cash flow story, and the beauty of it is that you do not need aggressive top-line growth to make it work.

I decided to model three scenarios.

1) The Operational Floor asks what Fox is paying if Roku merely limps to its own stated target.

2) The Execution Midpoint asks what happens if Roku keeps a fraction of the advertising momentum it is already posting.

3) The Integration Flywheel asks what happens once Fox’s content starts actively driving Roku’s subscription engine. For each one, I will show you the price Fox is paying on a standalone basis, and then once you layer in the merger’s cost synergies.

(Two housekeeping notes on the math, because I would rather be conservative than too cute. First, every growth rate I cite is a three-year compound annual rate measured from Roku’s 2025 base out to 2028, a ’25–’28 CAGR. Second, Roku carries a low cash tax rate today thanks to its accumulated net operating losses, which I reflect in the standalone cases, and I tax the merger synergies at a full 25% corporate rate before counting them as cash.)

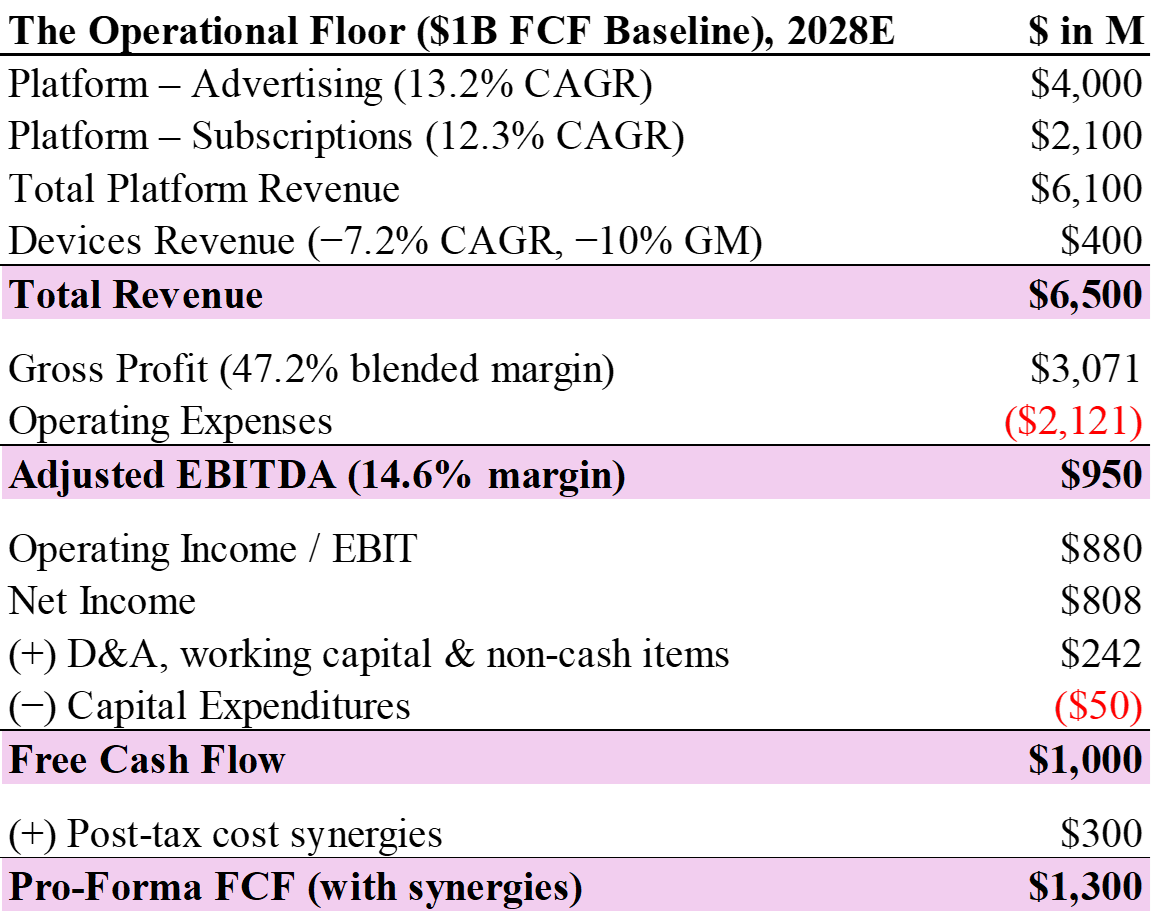

Scenario 1: The Operational Floor. Even Hitting the Bare Minimum, Fox Is Paying a Fair Price

The premise here is deliberately pessimistic. I am anchoring to the one forecast number Roku management has repeatedly committed to in public: $1.0 billion in standalone free cash flow by 2028. I consider this the baseline case.

To get there, I do not need heroic growth. I need $6.5B in total 2028 revenue, an 11.1% compound rate off Roku’s 2025 base of $4.73B. Remember, Roku grew platform revenue 28% year over year in Q1 2026. This model assumes that blistering pace nearly halves into the low double digits and the company still clears a billion in cash, purely on the strength of the mix shift.

Devices keep shrinking to $400M and keep running at a deliberate negative 10% gross margin. Remember, that hardware loss is a feature, not a bug. Roku eats it to acquire households and feed the ecosystem. Meanwhile Platform, the actual tollbooth, grows to $6.1B on decelerated-but-steady advertising (13.2% CAGR) and subscriptions (12.3% CAGR).

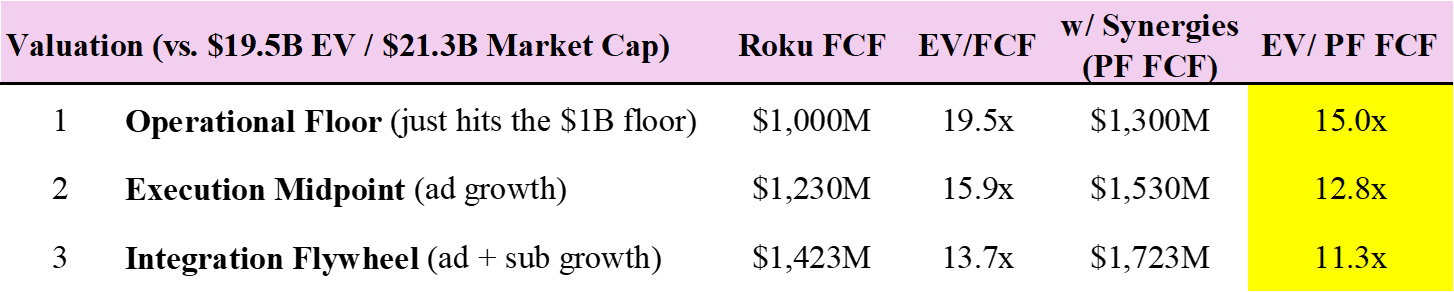

So what does that buy Fox? On the standalone $1.0B, Fox is paying 19.5x EV/FCF and 21.3x price-to-FCF. Layer in the $300M of post-tax cost synergies the merger unlocks and the pro-forma multiple drops to 15.0x EV/FCF and 16.4x P/FCF.

Let me reiterate, this is the conservative case. This is Roku’s current growth trajectory halving, barely limping to its self-imposed floor. And even here, Fox is paying roughly 15x cash flow for a platform that owns 100 million households and 44% of all U.S. CTV viewing hours, about 3x its nearest competitor. 15x free cash flow for a dominant tech platform is not expensive, it is a fair market price. And I believe the downside is heavily protected.

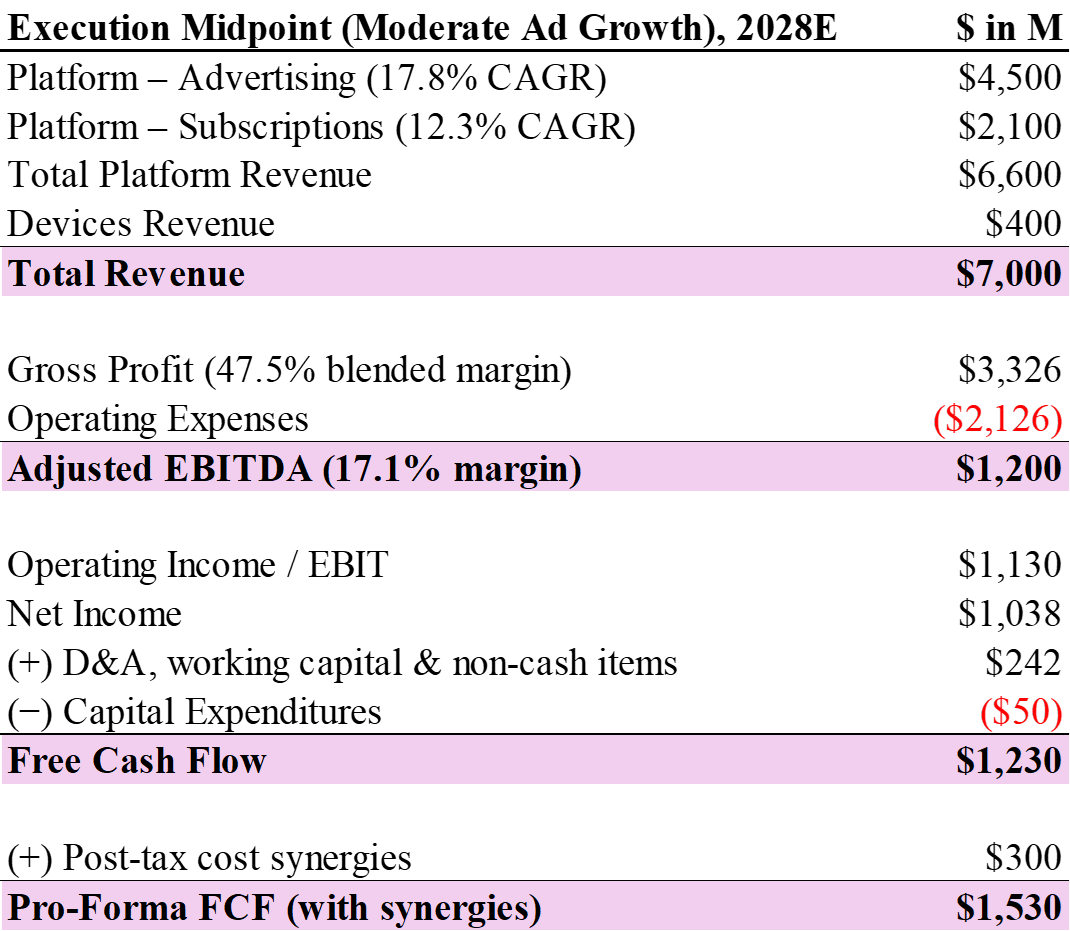

Scenario 2: The Execution Midpoint. A Little Ad Momentum and the Multiple Drops Below the S&P

Now in my second scenario I give Roku a fraction of the momentum it actually showed in its most recent print, and only on the advertising line. Nothing else changes from the base case.

In Q1 2026, Roku advertising grew 27% year over year. My baseline assumed that decelerated to 13.2%. For the midpoint, I split the difference and model a 17.8% ad CAGR, which is still a sharp slowdown from the current run-rate. That lifts 2028 advertising to $4.5B and total revenue to $7.0B, almost exactly the Street’s consensus number, though I get there through high-margin advertising rather than hardware, which means meaningfully cleaner cash conversion.

The reason this matters so much is operating leverage. That incremental $500M of ad revenue is not like incremental hardware revenue. Once the fixed costs of the platform are covered, advertising dollars are intensely cash-generative. I add a little variable OPEX for sales commissions to be realistic, and the rest falls to the bottom line.

Raising one growth assumption by a few points moves standalone free cash flow from $1.0B to $1.23B, a 23% jump. That is the asymmetry of this business in a single number. On the standalone $1.23B, Fox is paying 15.9x EV/FCF and 17.3x P/FCF. With the cost synergies layered in, the pro-forma multiple compresses to 12.8x EV/FCF and 13.9x P/FCF.

Roku does not have to be a rocket ship. It just has to execute moderately well on monetizing its new homescreen real estate, and Fox’s effective purchase multiple falls below the S&P 500 average.

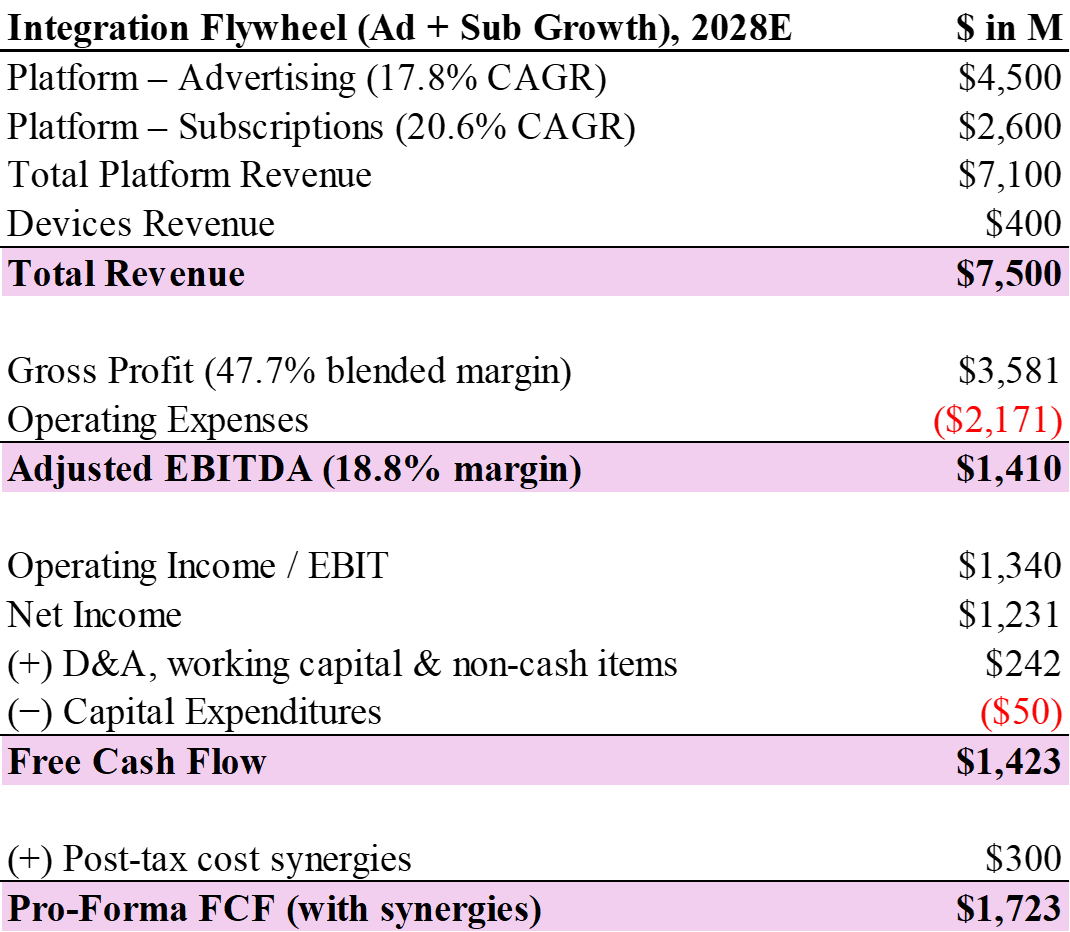

Scenario 3: The Integration Flywheel. The Upside the Market Isn’t Pricing

This is the kind of upside the market is not yet pricing, precisely because it lives out in 2028.

For Scenario 3, I keep the moderate ad growth from Scenario 2 and add a moderate acceleration on subscriptions. Subscriptions grew 30% year over year in Q1 2026. My baseline cut that to 12.3%, and using the same midpoint logic, I model a 20.6% subscription CAGR (’25–’28), lifting 2028 subscription revenue to $2.6B and total revenue to $7.5B.

I am comfortable modeling faster subscription growth for a specific reason, and it is not the obvious one. The bull case is not that millions of people are suddenly going to subscribe to Fox’s own services through Roku, though some will. It is that Roku becomes the aggregator of choice, the hub where consumers re-bundle their scattered streaming subscriptions onto a single bill, with a single interface, the way the old cable bundle used to work.

Management said plainly on the M&A call that the company still has a long list of monetization levers it has barely begun to pull, and the overhauled UI, paired with a deeper focus on content discovery across the ecosystem, is exactly what nudges a viewer to add and manage subscriptions through Roku rather than app-by-app. This is the re-bundling thesis I have hammered since Part 1, where I argued that Roku, alongside Amazon’s Prime Video Channels, is one of the very few players positioned to own that re-aggregation. Amazon has already proven how powerful it is to control the billing relationship and become the place people consolidate their streaming. Roku Pay is Roku’s version of that mechanism, and it is the lever underneath this scenario.

Standalone, this case throws off $1.42B in free cash flow, putting Fox at 13.7x EV/FCF and 15.0x P/FCF. Now layer in the $400M of management-guided run-rate cost synergies. Tax those at a full 25%, and $300M of clean post-tax cash drops to the bottom line. That brings pro-forma 2028 free cash flow to $1.72B, and the effective purchase multiple to 11.3x EV/FCF and 12.4x P/FCF.

When you underwrite the operating leverage of the platform alongside the post-tax deal synergies, my math indicates that Fox is acquiring some of the most important real estate in American television for roughly 11x my 2028 free cash flow forecast.

And to be clear about how I got here, every input in this scenario is a conservative midpoint between Roku’s decelerated baseline and the actual growth rate it posted last quarter. If Roku simply keeps doing a watered-down version of what it is already doing, this is the number Mr. Market is leaving on the table.

The Valuation Ladder: Execution Is the Only Variable

Put the three cases side by side and I think the opportunity becomes obvious. Depending on how well management executes, we will look back and find the purchase price paid for Roku to be quite reasonable, and maybe even cheap.

A business throwing off growing, high-margin, recurring free cash flow, sitting on the most important distribution chokepoint in American television, is the kind of asset that comfortably earns a mid-teens multiple on forward cash flow in any rational market. In two of my three scenarios, Fox is buying it below that. In the third, it is paying right around fair value for what is close to a worst-case outcome. So the entire realistic range lands between roughly 11x and 15x 2028 FCF, and every one of those multiples already counts the cost synergies. Those are below-market prices for an above-average asset.

Unlocking the Upside: The Levers Roku Has Yet to Pull

A model is only as good as the operating story underneath it, so let me close the loop on how Roku actually delivers the growth in Scenarios 2 and 3. This is the part the spreadsheet cannot show you. Since much of Part 1 and Part 2 covered the strategy of both companies, I’m going to be brief with some topics that I have touched upon before but need to be spelled out yet again.

The advertising engine. The 17.8% ad CAGR is not a hope, it is the natural consequence of two levers Roku is only now pulling. As I mentioned in Part 2 of my Roku series, for years, founder Anthony Wood resisted putting non-TV advertising on Roku’s landing page, an aesthetic discipline that quietly cost the company hundreds of millions in foregone revenue. That changed starting in 2023, and the recent UI overhaul turns the most valuable real estate in the living room, the screen every viewer sees before they choose what to watch, into a dynamic, monetizable feed without disrupting the experience.

The second lever is non-endemic demand. Traditional linear advertisers in auto, CPG, and travel have historically been slow to move budgets into programmatic CTV. Roku’s scale combined with Fox’s decades of linear ad-sales relationships is exactly the bridge that finally moves those sticky, billions-of-dollars budgets onto the platform.

The subscription engine. The 20.6% subscription CAGR runs on Roku Pay. When a viewer can subscribe to a new streaming service with a single click of the remote, with their billing already on file, conversion goes up and friction goes to zero. Roku becomes the billing relationship for the streaming wars, and owning the billing relationship means taking a steady, high-margin rev-share cut from whoever wins. That is the single most underrated position in media, and it is precisely the kind of recurring, high-margin, low-churn revenue that deserves a premium multiple.

The wild card: Tubi. Here is a lever I am deliberately not putting a number on, because Fox does not break out Tubi’s financials, but I refuse to let it go unmentioned.

Fox owns Tubi outright, and Tubi has quietly become one of the largest free, ad-supported streaming services in the country. I have been tracking its climb in Nielsen’s Gauge report for over a year now (see my monthly TV viewing snapshots), and it pulled that off without the Fox name attached.

On the M&A call, management was clear that it intends to keep Tubi and the Roku Channel as separate brands rather than merging them, and I think that is exactly the right call. The two are complementary, with only about a one-third audience overlap.

Tubi is over 90% video-on-demand, while the Roku Channel is over 80% FAST, the free linear-style channels you flip through. The viewer will likely never see a connection between them. But the synergy here is not on the screen, it is in the back office, and you only catch it if you think like an operator. Fox’s ad sales team can now walk into the upfronts and offer advertisers two complementary inventory pools under one roof, on-demand and FAST. That is a more complete pitch to a media buyer than either service makes alone, and it is the kind of go-to-market advantage that never shows up on a slide but absolutely shows up in ad dollars.

Conclusion: The Cheapest Way to Buy Roku’s Future

I am not naive about M&A. Given how much of it destroys value, healthy skepticism should be your default reaction when a legacy player makes a big technology acquisition, and I understand exactly why the market is wary of this one.

But I write Accrued Interest to show investors how to think like an operator, not just a trader. The whole point of this exercise is to demonstrate that once you underwrite the cash flow from the segment level, the deal is heavily de-risked: by 2028, Fox is paying somewhere between 11x and 15x real free cash flow for the entire asset.

And remember, every one of those multiples counts only the cost synergies, the $400M of redundant tech stacks, back-office overlap, and consolidated ad-sales teams. I have given Fox zero credit for revenue synergies, and the potential there is significant. Picture Fox’s ad sales team at the 2028 upfronts selling advertisers the Roku Channel and Tubi side by side, the FAST audience and the on-demand audience in a single conversation. Picture Fox’s first-party sports and news data flowing into Roku’s targeting engine. None of that is priced into Fox’s stock today. It is all free optionality.

So my conclusion is the same as it was in Parts 1 and 2, except now I have the model to back it up. Cord-cutting is not reversing, and the cable bundle is not coming back. At today’s price, buying Fox equity is the most asymmetric, value-driven way to own Roku’s future cash flow engine. I am reiterating my Outperform rating. You are welcome to argue with me in the comments, just bring a model.

Relevant tickers: FOXA 0.00%↑, ROKU 0.00%↑, DIS 0.00%↑, NFLX 0.00%↑ , GOOGL 0.00%↑ , AMZN 0.00%↑

— Accrued Interest

Relevant Accrued Interest Articles:

2026.06.22: The Strait of Roku: How Fox Seized Streaming’s Chokepoint Without Firing a Shot

2026.06.16: Fox + Roku: A Brilliant Pivot from the Cable Bundle to the Living Room

2026.05.28: Monetizing the Habit: Meta’s Enterprise Land Grab and Roku’s Living-Room Billboard

2026.04.16: Roku’s 100 Million Milestone