The Victor of the Streaming Wars: Why Netflix is a $120 Stock

While legacy media burns billions on doomed mergers and melting ice cubes, Netflix has built a global monolith insulated from geopolitical risk.

Accrued Interest TLDR: While legacy media burns billions on doomed mergers, Netflix has already won the streaming wars. Operating in over 190 countries with ruthless capital discipline, surgical sports investments, and a localized content engine, Netflix has become the ultimate geopolitical haven. I see a clear, structurally sound path to $4 in EPS by 2027, driven by high-margin ad revenue expansion and share buybacks. Applying a full but fair 30x multiple yields a $120 price target— 27% upside from today’s $94 level. This is a classic time arbitrage play. Read the full breakdown below to see exactly why the capital flows here next.

Introduction

A few days ago, I published a piece breaking down exactly why the Paramount-WBD merger is a slow-moving trainwreck. The reaction to that post across the internet was massive, but the core takeaway of that thesis was incredibly simple: when you bolt together two melting ice cubes with a $79 billion debt anchor, you don’t get a dominant digital platform—you get a liquidity crisis. PSKY 0.00%↑, WBD 0.00%↑

The logical follow-up question: what does this mean for NFLX 0.00%↑ ?

Here at Accrued Interest, we ignore the noisy media narratives. We focus purely on market structure. And the fundamental structure of the global entertainment market proves that the “streaming wars” are officially over. It is now absolutely a two-horse race between Netflix and YouTube. Everyone else is just fighting for third place, and they are burning billions of dollars of shareholder equity to do it.

The contrast in forward-looking runways couldn’t be starker. While legacy media spends the next three years paralyzed by integration issues, boardroom infighting, and regulatory hurdles, Netflix operates with absolute, unencumbered clarity. We are witnessing the execution of a pure tech monopoly leaving its legacy peers in the dust.

The Competitor’s Curse and the Organizational Paralysis

When you look at the landscape today, the competitor’s curse is very real. As Netflix Co-CEO Ted Sarandos recently pointed out regarding the fallout of the WBD bidding war, whoever won that debt-laden prize will be forced into making operational cuts “in the excess of $16 billion.”

Think about what that actually means inside a corporate structure.

For the next 36 months, the newly merged entity will be stuck in endless committee meetings figuring out which middle-management layers to fire, which tech stacks to sunset, and how to satisfy their bondholders. This creates a state of perpetual organizational paralysis.

When future premium content comes up for licensing—whether that is a hit television show from a third-party studio or a highly coveted piece of intellectual property—Netflix can move swiftly and aggressively. They have the balance sheet and the operational clarity to write the check and move on, while their biggest competitors are still trying to figure out who has the authority to approve the budget.

The “Harry Potter” Infrastructure Gap

But the biggest structural advantage Netflix possesses isn’t just a clean balance sheet; it’s their underlying technology footprint.

Wall Street often misjudges media companies on the volume of their content library. But in the digital age, a content library is useless if you do not have the delivery infrastructure to monetize it seamlessly across borders.

Even if David Ellison had Harry Potter’s magic wand and could instantly integrate Paramount and WBD’s tech stacks today with zero friction, they still do not have the infrastructure to stream globally at the scale of Netflix.

Let’s see the actual footprint. HBO Max is currently available in roughly 100 countries—but crucially, it is still locked out of massive, high-ARPU English-speaking markets like the UK and Australia due to legacy licensing deals. Paramount+ is even worse; it operates as a standalone app in fewer than 35 countries. To get into Europe, they were so sub-scale they had to form a joint venture just to distribute their content.

Netflix, on the other hand, operates natively in over 190 countries. They own the entire tech stack, the billing architecture in local currencies, and the content delivery networks (CDNs) almost everywhere on earth.

We just saw the ultimate proof of this impeccable execution. Last weekend, Netflix exclusively livestreamed the BTS Comeback concert. While legacy streamers regularly struggle with app crashes, latency issues, and buffering during live events, Netflix seamlessly broadcasted the world’s biggest pop group live from Seoul to 190 countries, instantly hitting #1 in 77 of them. Legacy media is playing a localized game with borrowed money. Netflix is playing a global game with massive operating leverage.

The Macro Safe Haven: Hedging Geopolitical Risk

If you noticed that I took a two-week break from publishing recently, it was because the sheer level of geopolitical uncertainty had effectively frozen the broader markets. We all understand that traditional hardware, semiconductor, and manufacturing stocks are heavily exposed to supply chain shocks and tariffs. But what is dangerously underappreciated by the Street is that legacy media has its own set of geopolitical landmines.

Take James Gunn’s recent Superman as a warning sign.

While the domestic box office for the film was a strong $356 million, it severely underperformed internationally, dragging its global haul to just $617 million. The fanboys might not care, but WBD shareholders can reasonably point the finger at a very real problem: geopolitics. Anti-US sentiment definitely hurt the commercial reception of such a patriotic-coded American character. Gunn himself explicitly admitted this, noting to Rolling Stone, “we have a certain amount of anti-American sentiment around the world right now. It isn’t really helping us.”

Even Ted Sarandos, while recently testifying under oath before the Senate Judiciary Committee regarding theatrical exclusivity windows, openly cited the film’s underperformance as evidence of shifting global consumer behavior.

The structural flaw here is that legacy media relies almost entirely on exporting American cultural icons to generate a return on invested capital. That makes them highly vulnerable to geopolitical whims. We’ve seen the precedent over the last decade, where unilateral government decisions in regions like China can instantly block certain Western films, wiping out hundreds of millions in regional monetization overnight. When your balance sheet requires a traditional American superhero to overperform globally just to service your debt, you are taking on massive sovereign risk.

This is why Netflix is the ultimate defensive play in the media space. They don’t just rely on exporting American blockbusters; they invest heavily in sourcing local content in every respective market they operate in. Regardless of shifting political winds or sudden anti-US backlash, Netflix’s content pipeline is already localized by design.

We already saw the proof of concept for this decentralized production pipeline during the COVID-19 shutdowns. When US domestic production ground to an absolute halt, legacy studios starved for new releases. Netflix effortlessly pivoted, utilizing its massive international backlog to push high-quality foreign content to US and global audiences who had never seen it before. Combine this decentralized, globalized content engine with a “zero supply chain” digital subscription model—where you are shipping pixels, not physical goods—and you have a company uniquely insulated from physical borders and political blowback.

Cost Control as Alpha: The Live Sports Hedge

If you want to understand the trap that legacy media is currently stuck in, look no further than live sports rights.

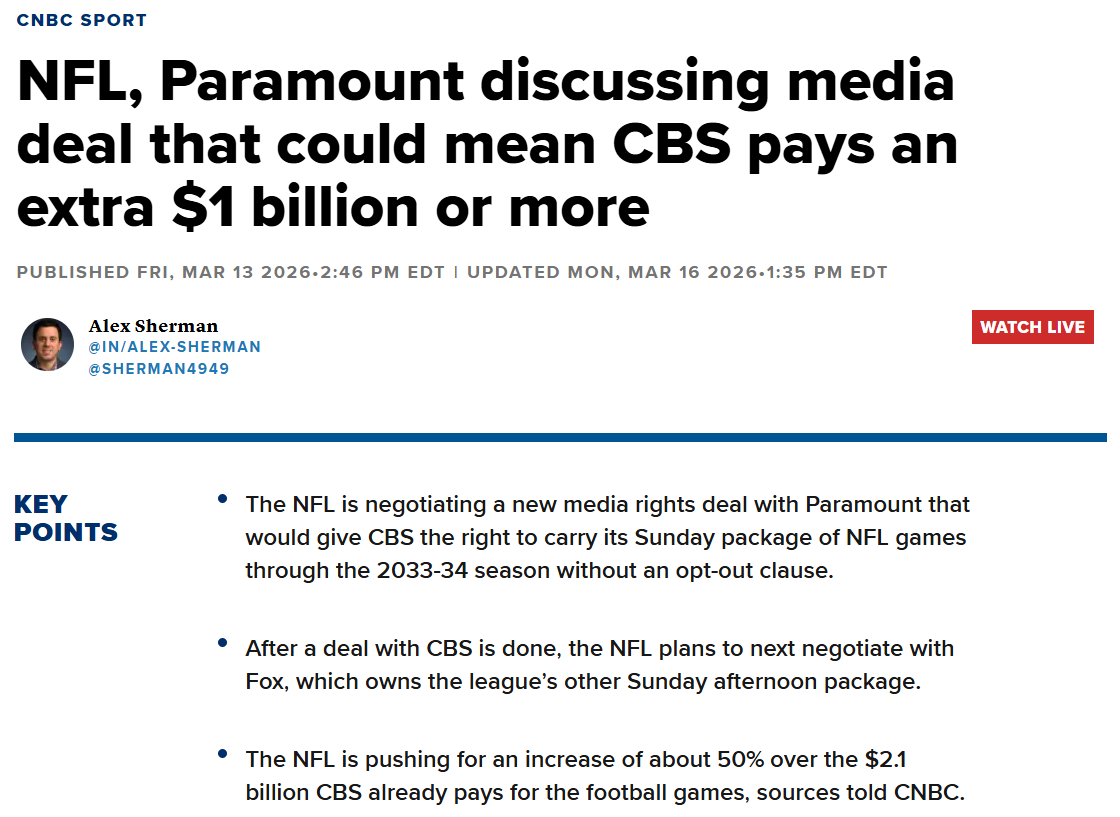

Right now, the NFL is reportedly pressuring Paramount’s CBS to eliminate their 2029-30 opt-out clause. In exchange for extending the deal, the league is demanding a 50% fee increase. That means CBS is looking at an additional $1 billion per year—pushing their annual payment to over $3 billion—just to keep the exact same Sunday afternoon package they already have. Legacy networks are effectively being held hostage. They have to pay margin-crushing premiums just to maintain their existing viewership baselines.

So, how do you hedge against the risk of rising NFL fees? The best way to hedge the risk of rising NFL fees is to not have a full slate of NFL regular season games to begin with!

This is where Netflix’s surgical approach to live sports becomes a massive driver of alpha. They have wisely added sports without taking on full-season commitments. By securing only high-impact, select holiday events—like their Christmas Day NFL games—they pick and choose the exact spectacles that maximize viewership ROI. They get the cultural event status and the advertising surge without inheriting the massive fixed costs of a 17-week broadcasting schedule.

We just saw another brilliant execution of this strategy with the 2026 World Baseball Classic. Netflix secured the exclusive rights to stream all 47 WBC games in Japan. Because sports broadcasting rights are heavily regionalized, Netflix was able to bypass the local Japanese terrestrial networks entirely and secure exclusivity in one of the most hyper-valuable baseball markets on earth. Furthermore, by targeting just the Japanese region, they didn’t have to engage in a ruinous, ego-driven bidding war against Fox for the U.S. broadcast rights.

While legacy media companies are bleeding cash to rent sports rights in saturated markets, Netflix is deploying capital surgically to drive localized dominance.

(A quick note to all of my free subscribers—which, as of right now, is 100% of you! In the future, this is exactly the type of section where I might apply a selective paywall as we get into the harder valuation mechanics, EPS breakdowns, and technical modeling. But in the meantime, please enjoy the free analysis below, and if you haven’t already, make sure to hit that subscribe button!)

The Valuation Engine: The “Pokémon Theory” of Margin Expansion

If you want to understand how to generate outsized equity returns, you have to subscribe to the “Pokémon Theory” of investing: a company must evolve. Margin expansion—the holy grail of earnings growth—only happens when a company can make a sub-segment’s revenue grow significantly faster than its underlying fixed costs.

For Netflix, that evolutionary engine is advertising.

Management’s 2026 guidance projects top-line revenue growth in the low double-digits to mid-teens (roughly 12-14%).

But the real story is that their operating margin is forecast to expand to 31.5%. Because Netflix already spent the last decade building and paying for its massive subscription infrastructure, the fast-growing ad business—expected to hit roughly $3 billion—is incredibly high margin. That ad money drops almost straight to the bottom line.

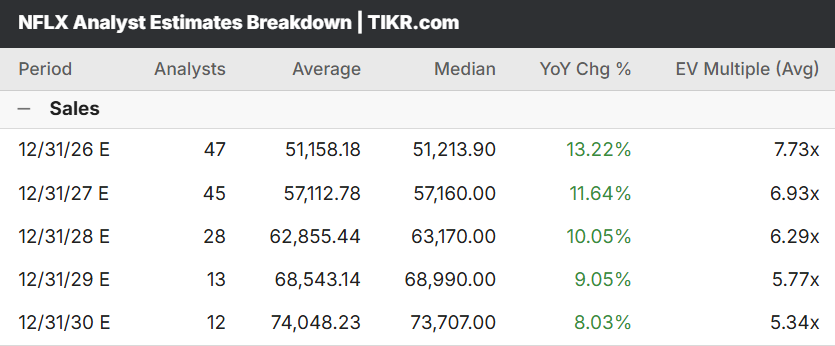

Looking at the latest Street consensus estimates via TIKR, the analyst modeling is highly reasonable and, if anything, slightly pessimistic. The Street is forecasting median Sales of roughly $51.2 billion for 2026, representing YoY growth of 13.2%. They then project a steady, gentle deceleration down to 11.6% growth in 2027 and 10% in 2028.

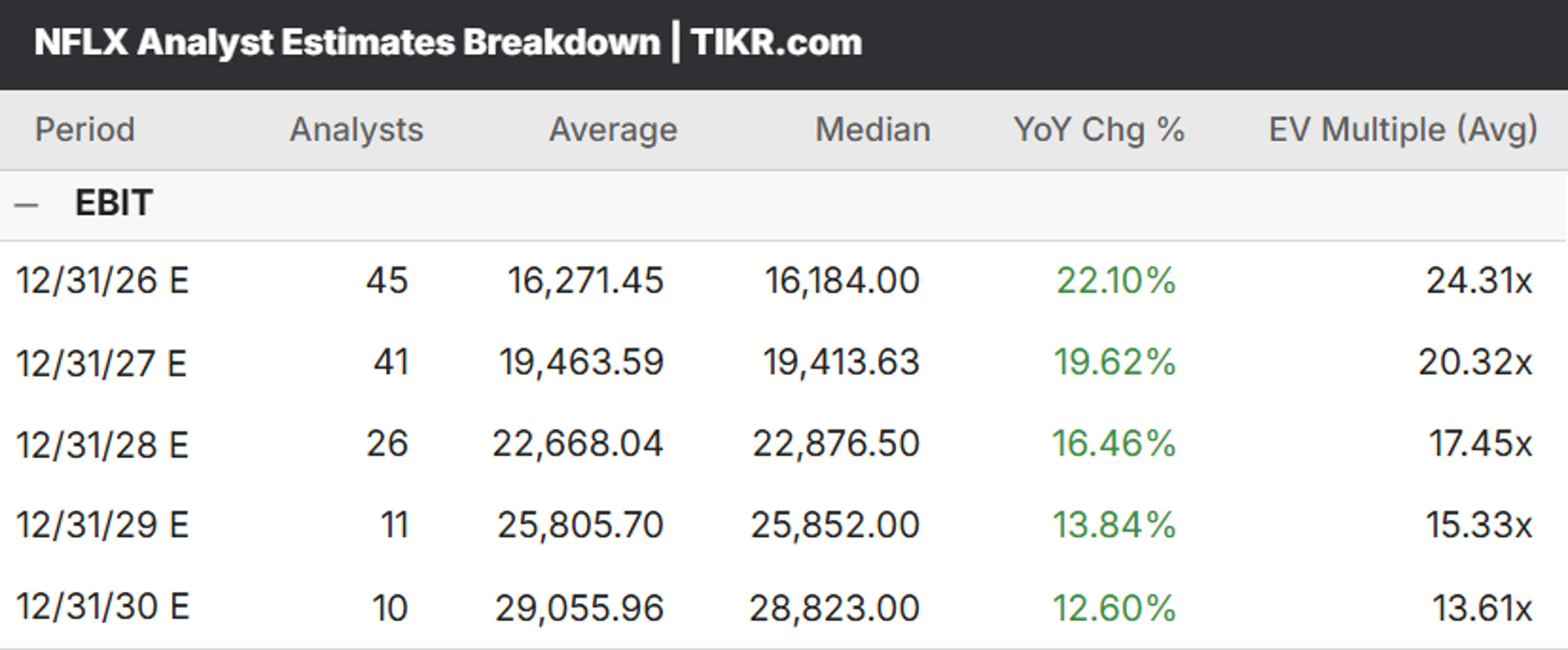

The 2026 EBIT forecast sits right around 31.6%, matching management’s guidance. I believe there is upside here. If that high-margin ad revenue scales faster than expected, that margin expansion will pull forward much sooner than the Street anticipates.

This margin expansion is compounded by their ruthless capital discipline. When the Warner Bros. bidding war reached peak irrationality, Netflix simply walked away—taking a massive $2.8 billion breakup fee just for showing up. As Ted Sarandos pointed out, “We’re builders, not buyers.” Instead of burning cash on ego-driven M&A, that $2.8 billion goes straight to accelerating their share buyback program, artificially shrinking the float and mathematically boosting EPS.

Conclusion: The Time Arbitrage Play

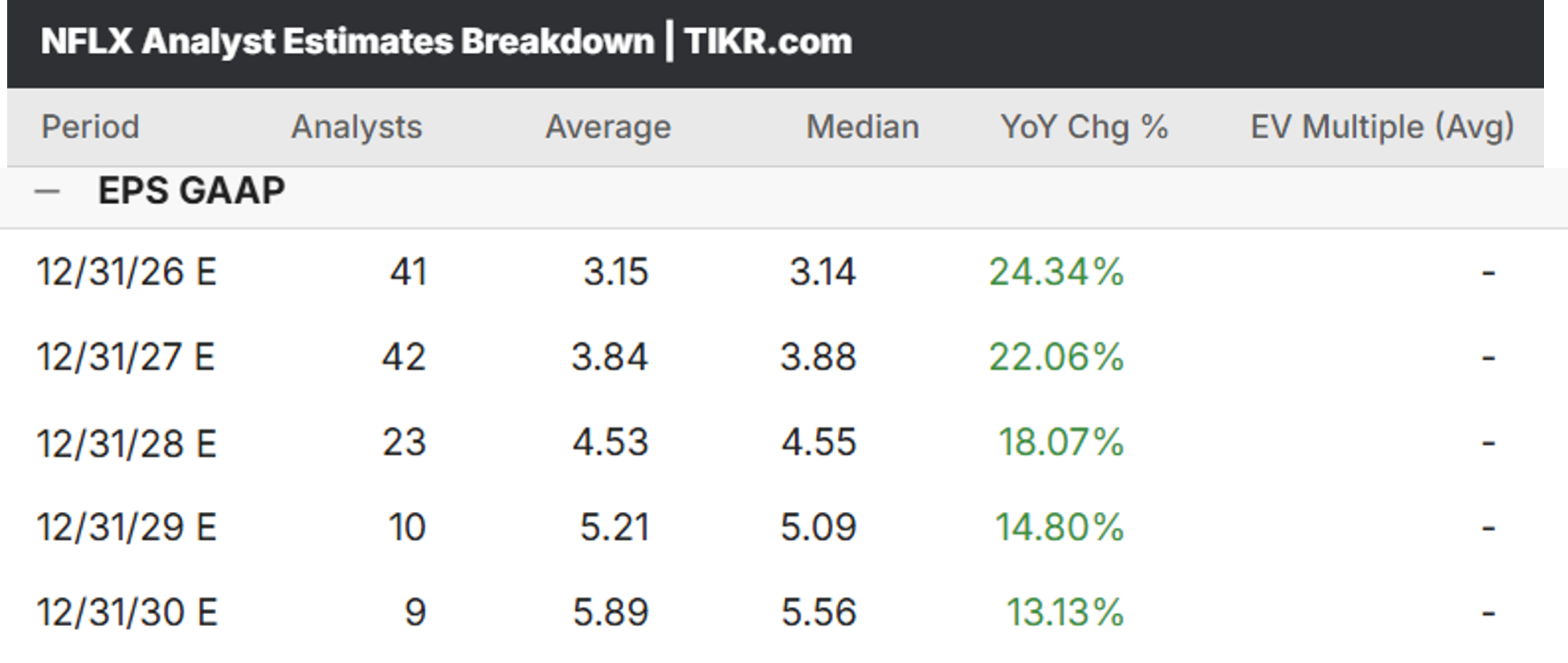

The stock is currently trading around $94.00, which prices it at roughly 30x the 2026 GAAP EPS consensus of $3.14. I believe 30x is a full, but entirely fair, multiple for a dominant, defensive, digital-first global entertainment platform. I would NOT base my price target on a multiple higher than 30x unless I had immense conviction that top-line revenue was going to violently obliterate Street estimates.

Because the current multiple is fundamentally correct, this is a classic Time Arbitrage play.

“Time arbitrage refers to an opportunity created when a stock misses its mark and is sold based on a short-term outlook with little change in the long-term prospects of the company.”

I have high conviction that Netflix will easily meet or beat their future earnings estimates, so I am willing to take on the risk of the stock today to buy it at a discount to its 2027 and 2028 earnings power.

By applying that full 30x multiple to roughly $4.00 in earnings—which sits just slightly ahead of the Street’s $3.88 median estimate for 2027—we arrive at a $120 Price Target. That represents an absolute return of over 27% from today’s $94.00 price.

Legacy media is playing a desperate game of defense just to survive another quarter. Netflix is playing offense while returning capital to shareholders. It is time to allocate accordingly.

What do you think is the biggest threat to this $120 price target? Let me know in the comments below!

-Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.

Hey! Just saw your post and thought I’d reach out—I really respect what you’re doing. I write about trading, mainly SPY and VIX, so it’s not exactly the same niche, but I think there’s still some overlap in audience. I’d appreciate your support, and if you like the content, maybe even a sub. Here’s one of my latest posts—curious to hear what you think.