The Street Missed the Q1 Signal: Why Meta’s AI Engine is Worth Every Penny

The market panicked yet again over CapEx, but the $META ad machine is accelerating.

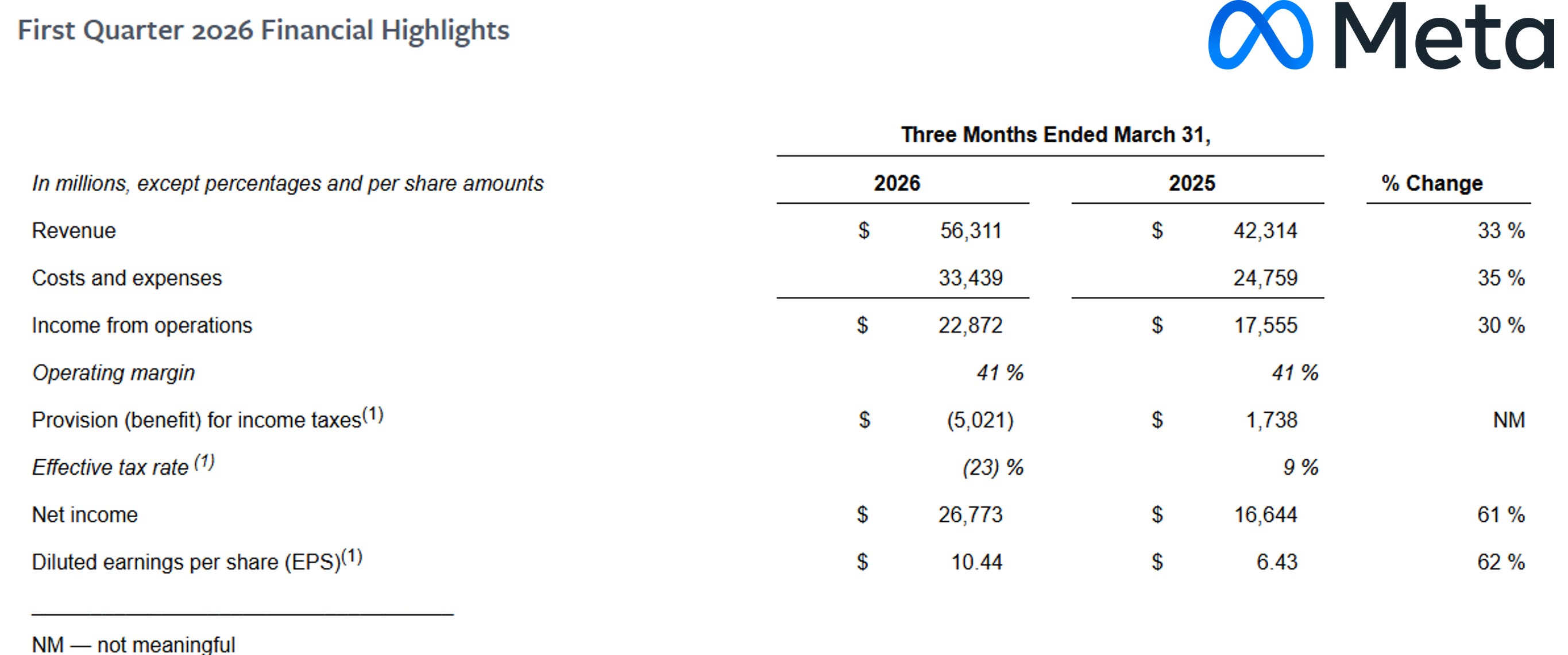

Accrued Interest TLDR: Wall Street balked at Meta’s staggering $125–$145 billion CapEx guidance, sending shares down nearly 10% after-hours. However, Meta is achieving the holy grail of digital advertising: effectively raising prices and improving algorithmic targeting right alongside a massive influx of new ad inventory. Q1 revenue grew 33% YoY, driven by a 19% increase in global ad impressions and 12% in pricing. Engagement is reaching multi-year highs, and AI is generating multi-billion-dollar revenue streams. Management is strategically shifting investment from human payroll to compute infrastructure to build a formidable moat. I am maintaining my Outperform rating. At $600 per share, this business is undervalued at 17.4x 2027 earnings, representing a discount to the market multiple. Meta is the most misunderstood of the Magnificent Seven.

I. The After-Hours Disconnect Masks a Highly Profitable Reality

Let me be absolutely clear right out of the gate: This was a strong quarter for Meta. The operational metrics demonstrate a business actively accelerating its dominance.

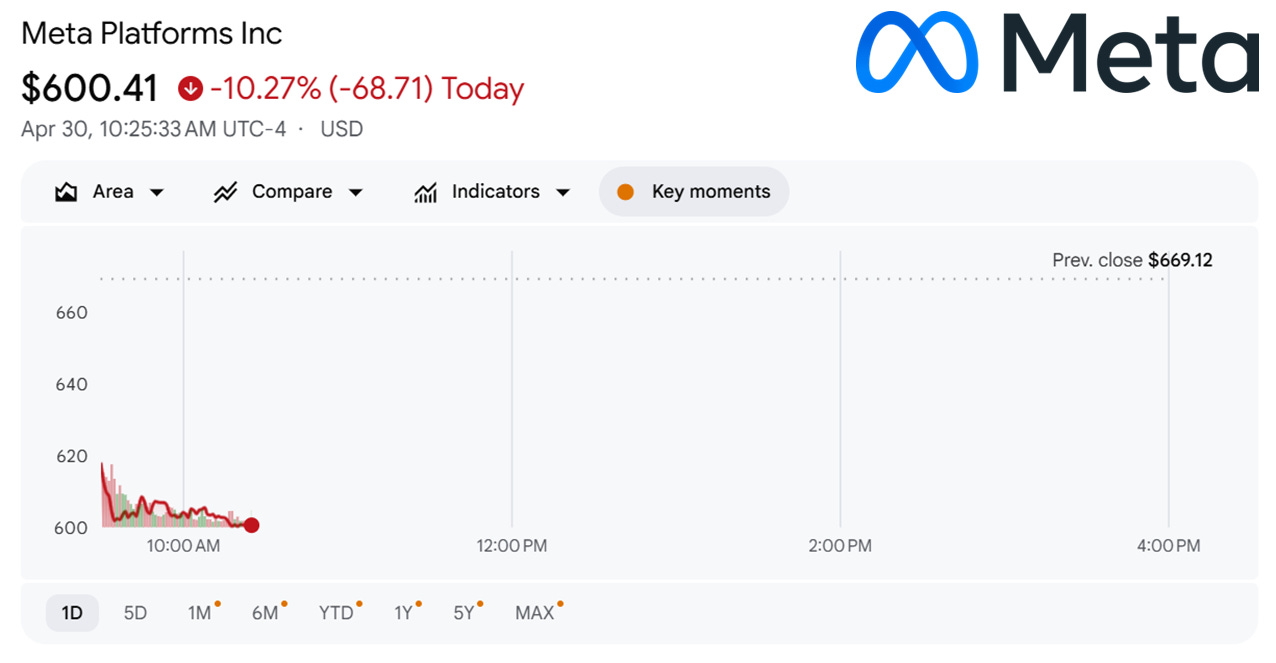

If you only watched Meta’s stock price plummet in after-hours trading, you would be forgiven for thinking the company’s core business was imploding. Wall Street took one look at the elevated capital expenditure (CapEx) guidance and hit the SELL button. But before we address the infrastructure spending, we need to talk about the actual earnings generated by the business.

To establish an accurate baseline, we must first adjust for one-time items. In Q1, Meta recognized an $8.03 billion income tax benefit. This partially offsets the $15.93 billion non-cash tax charge recorded in Q3 2025 due to the “One Big Beautiful Bill Act.” Excluding this benefit, Meta’s adjusted EPS would have been $7.31, which is $3.13 lower than the headline $10.44 figure. Nevertheless, this still represents impressive 13.69% YoY growth compared to the $6.43 EPS in Q1 2025.

But the market is currently treating Mark Zuckerberg’s infrastructure spend like a reckless cash incinerator, completely missing the fact that Meta’s organic growth drivers and profit margins are already being demonstrably and sustainably enhanced by their artificial intelligence deployments.

II. The Core Volume Engine is Accelerating Despite Geopolitical Shocks

I have consistently maintained that ad impression growth is the North Star metric for Meta. It serves as undeniable proof of strong consumer demand, high user engagement, and expanding platform inventory.

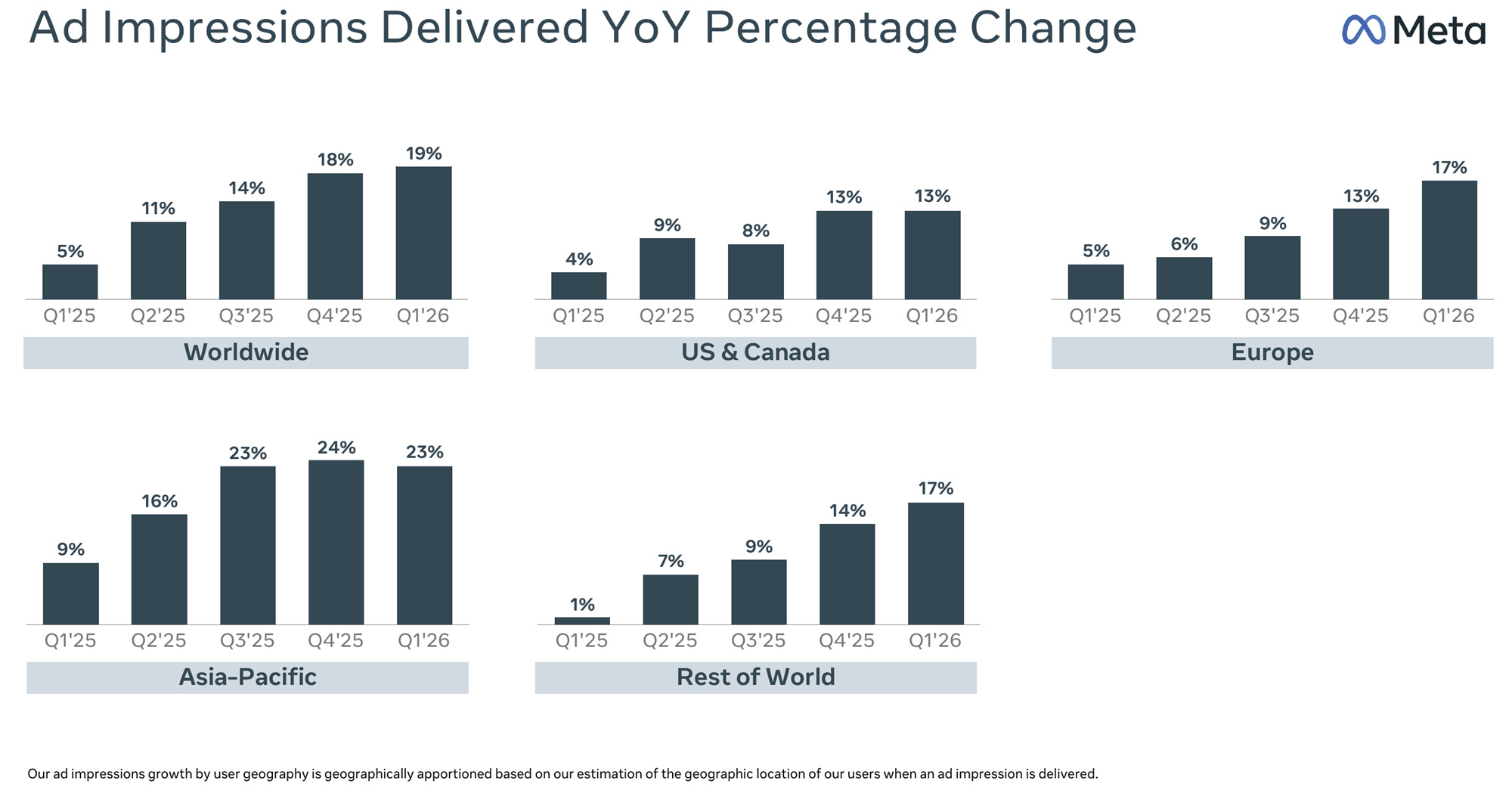

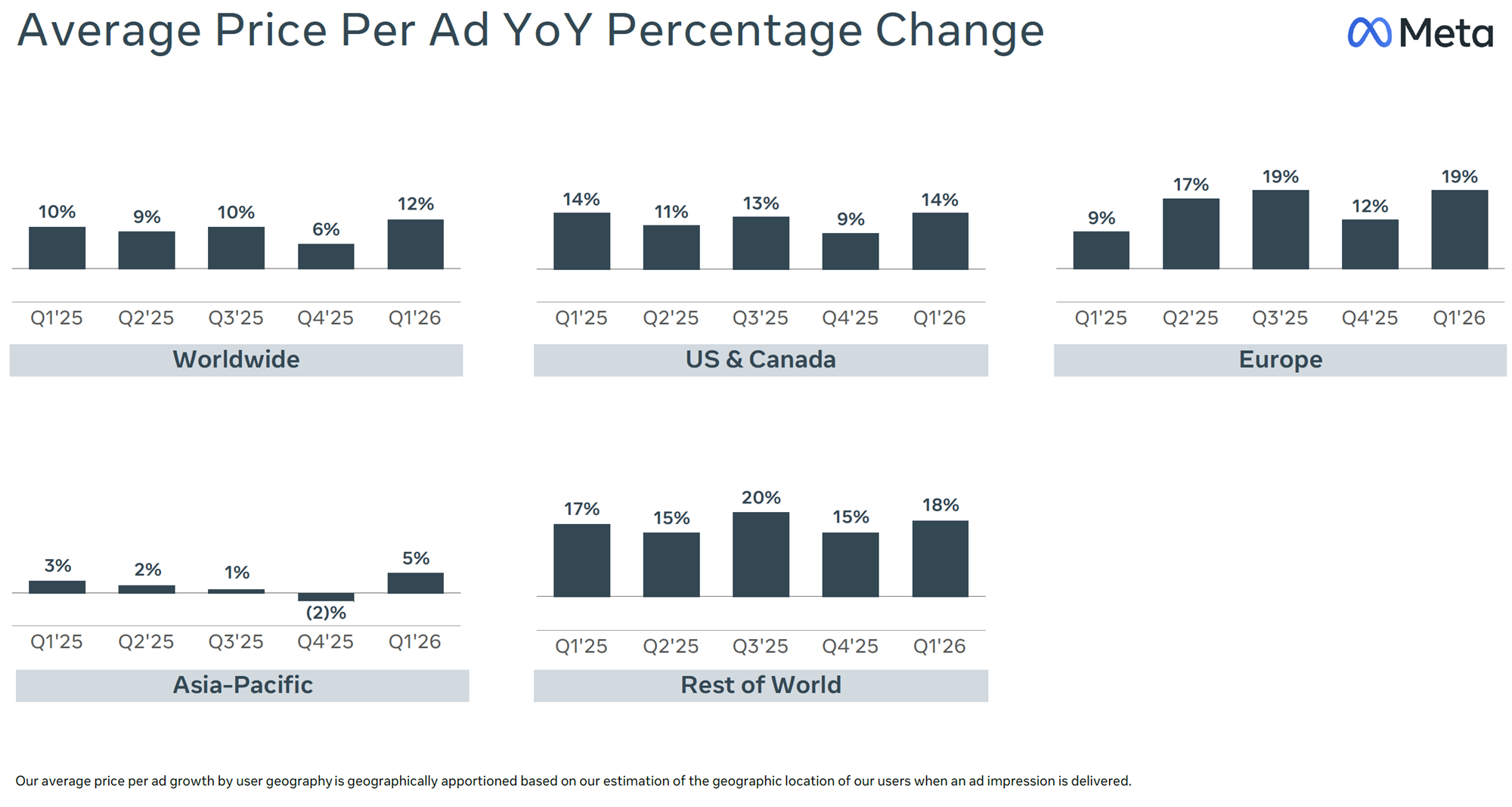

In Q1, worldwide ad impressions accelerated by +19% YoY. Let me reiterate: It is exceptionally difficult for a trillion-dollar company to grow volume at that absolute level. When you are already serving billions of users daily, finding 19% more inventory to sell is a notable engineering feat, yet they are doing it cleanly and efficiently across the entire globe.

The U.S. & Canada region matched its blistering Q4 pace, growing at +13% YoY.

Europe showed acceleration, jumping from previous trends to a 17% growth rate.

But there is a specific detail from the follow-up Q&A call that makes this volume growth—and the resulting 33% YoY revenue growth (or 29% on a constant currency basis)—so incredibly impressive. CFO Susan Li revealed that advertiser spend actually softened mid-quarter due to the sudden geopolitical conflict in Iran:

“We did see reduction in advertiser spend coinciding with the beginning of the conflict in Iran at the end of February, and that continued through the quarter. We saw the most pronounced impact within the Middle East user region, but we also saw some softer trends in markets outside the Middle East, including in the U.S. and Western Europe. I would say we’ve begun to see some signs of improvement in demand... coming into April.”

Meta successfully navigated these mid-quarter geopolitical headwinds, with advertising demand rebounding strongly into April. This pivot is a significant indicator for investors, as it derisks the robust Q2 revenue guidance of $58–$61 billion. Compared to Q2 2025 revenue of $47.5 billion, this guidance implies a 22% to 28% YoY growth rate. I remain more bullish than the consensus, believing Meta can sustain a 20%+ annual revenue growth rate for several years.

III. Meta’s AI is Breaking the Fundamental Laws of Digital Ad Economics

As I have covered before here on Accrued Interest, in the advertising sector, revenue is driven by a very simple equation: Volume (Ad Impressions) multiplied by Price (CPM, CPC, etc).

Historically, these two forces share an inverse relationship. For instance, if a platform aggressively increases ad load by flooding the market with inventory, the average price typically collapses as supply outstrips demand.

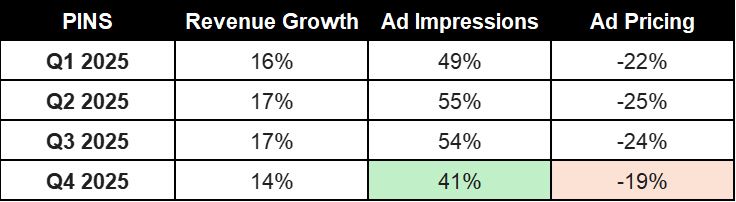

In several of my Accrued Interest deep dives, I have made it a point to highlight this exact value trap play out in lower-quality social media businesses. For example, as I noted in my recent Q4 deep dive, Pinterest grew its ad impressions by a massive 41%, but their pricing collapsed by -19%. This proved they were merely masking weak organic demand by dumping cheap, unoptimized inventory onto the market.

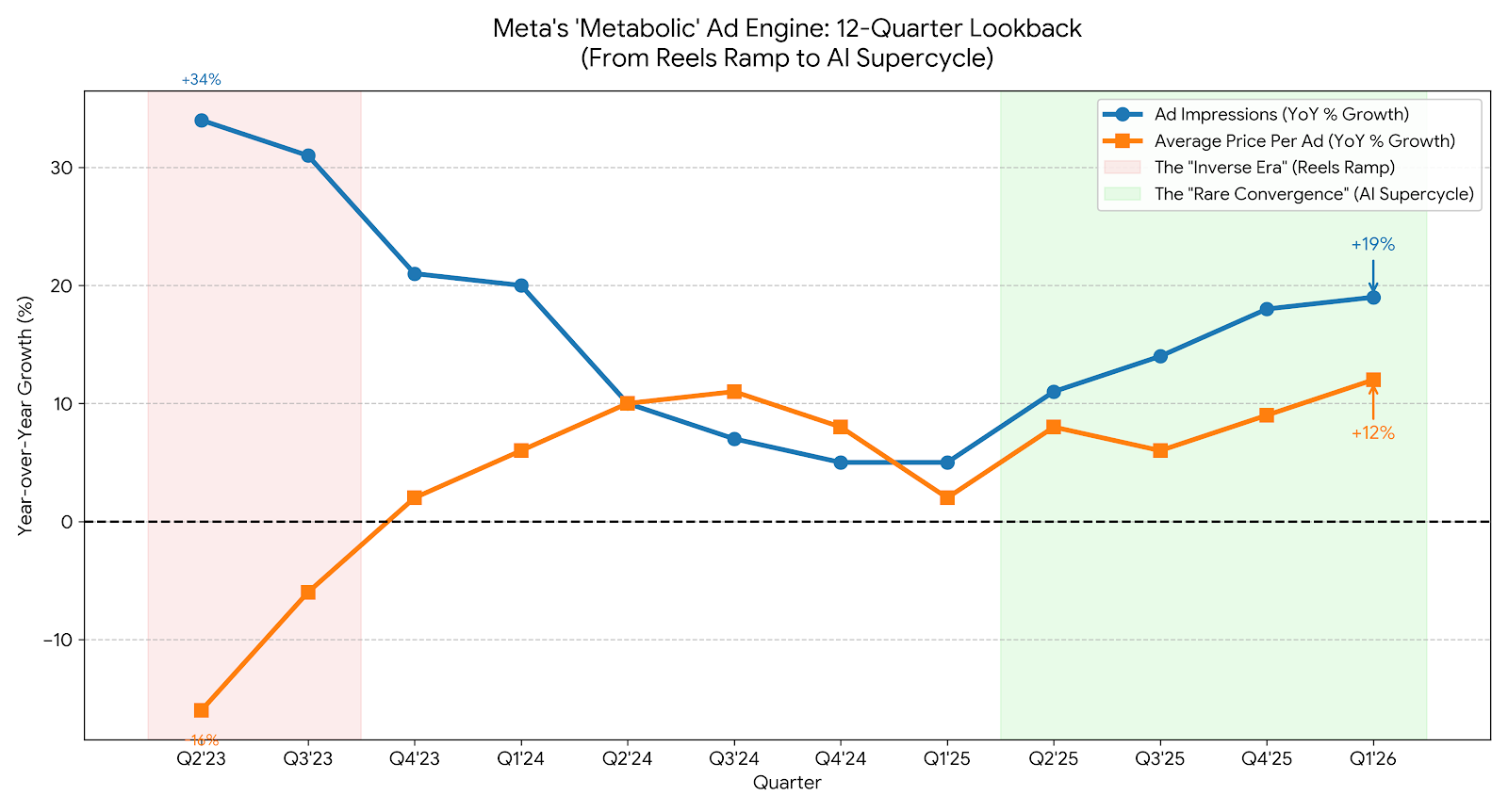

Meta, however, is doing the exact opposite. Over the last four quarters, Meta has achieved a rare feat, which once you chart it out it looks almost as if they are breaking the fundamental laws of digital ad supply and demand. Please see the chart here.

If we look back to the “Reels Ramp” of 2023, Meta’s impressions surged, but pricing fell as they forced new, under-monetized short-form video inventory into the feed. Fast forward to what I am dubbing the “AI Supercycle” of Q1 2026, now Meta expanded its overall ad supply by 19% while simultaneously hiking the average price +12% YoY.

This dynamic is precisely why I believe Meta’s future will be so bright! Meta’s recommendation engines have made their ad targeting so precise—and the resulting conversions for brands so high—that advertisers are willingly bidding up the price of ads even as Meta adds new inventory. They are extracting more money from brands because the AI ensures a better return on ad spend (ROAS).

IV. Strong Engagement KPIs Prove Meta’s Algorithm is Winning

Regardless of whatever anecdotal data you hear from your friends and family - one fact is no longer in dispute. Meta’s algorithm is winning the war for consumer attention. For years, I used to hear people complain that they missed the “old Facebook” but clearly their behavior says otherwise! Artificial intelligence has largely solved the content discovery problem, transforming the platforms from simple social networks into daily, high-frequency entertainment habits.

During the earnings call, management explained how their AI models are keeping users scrolling longer than ever:

Instagram Reels: Ranking and recommendation improvements in Q1 drove a 10% lift in total Reels time spent.

Facebook Video: Total video watch time increased more than 8% globally in Q1, representing the largest absolute QoQ gain the company has seen in four years.

Freshness as a Feature: Same-day posts now represent over 30% of all recommended Reels served to users. This metric is more than double the levels seen just a year ago.

AI isn’t just serving engaging content; it is serving fresh content faster and more accurately than ever before. Meta is fighting back competitors like TikTok and ensuring its own platforms remain the daily default for billions of people.

But the returns on their AI investments aren’t strictly limited to the core social feed. We are seeing alternative, high-margin monetization engines catch fire across the company.

Business Messaging: Conversations facilitated by WhatsApp Business AIs grew to more than 10 million per week in Q1, up 10x since just January 2026.

Partnership Ads: More than doubled YoY to a $10 billion revenue run-rate.

This quarter’s commentary validated my recent thesis regarding Meta’s aggressive structural cost discipline. As I wrote in “AI Tracking Employee Keystrokes Validates Meta Bull Case,” management is actively trading human payroll for compute infrastructure.

During the call, CFO Susan Li confirmed Meta plans to downsize its employee base in May. She explicitly stated that this “leaner operating model” will allow the company to move quickly and help offset their substantial infrastructure investments.

V. The $145 Billion Infrastructure Bill is a Moat Enhancer, Not a Liability

Now, we have to address the primary cause of the stock sell-off - the forward CapEx guidance. Meta anticipates its 2026 capital expenditures will be in the range of $125-$145 billion, a notable increase from their prior range of $115-$135 billion.

Bearish analysts view this multi-year investment as a financial liability; I view it as a strategic moat. By outspending competitors, Meta is effectively securing the global AI supply chain through 2027, creating significant barriers to entry.

To counter concerns regarding margin collapse, one only needs to look at the profitability guardrails established by management. Susan Li explicitly guided that 2026 operating income will exceed 2025 levels. I believe the market will tolerate elevated CapEx as long as the core advertising engine generates enough cash to outpace rising costs.

When you map this reality against the findings in my recent deep dive, “Back to the EBITDA: Decoding Meta’s $1,116 Executive Playbook,” the picture becomes crystal clear. The board’s newly issued executive compensation structure demands immense value creation before the C-suite sees a dime. I now see where the Meta Board gained the confidence to set such aggressive stock option targets. This quarter demonstrated to me that Zuckerberg and the management team know exactly what levers to pull to kick the company’s profits into high gear.

VI. The Multiple Expansion Case: The Meta Discount Will Not Last Forever

The strong Q2 revenue outlook of $58–$61 billion, supported by the April rebound in ad demand, proves that this momentum is sustainable. The market is overlooking the fact that the ROI on Meta’s CapEx is already manifesting in user engagement, ad volume expansion, and structural efficiency.

Meta at $600 is a compelling long precisely because it is a rare opportunity when you can buy one of the top 2 most dominant advertising businesses on the planet at a below market multiple.

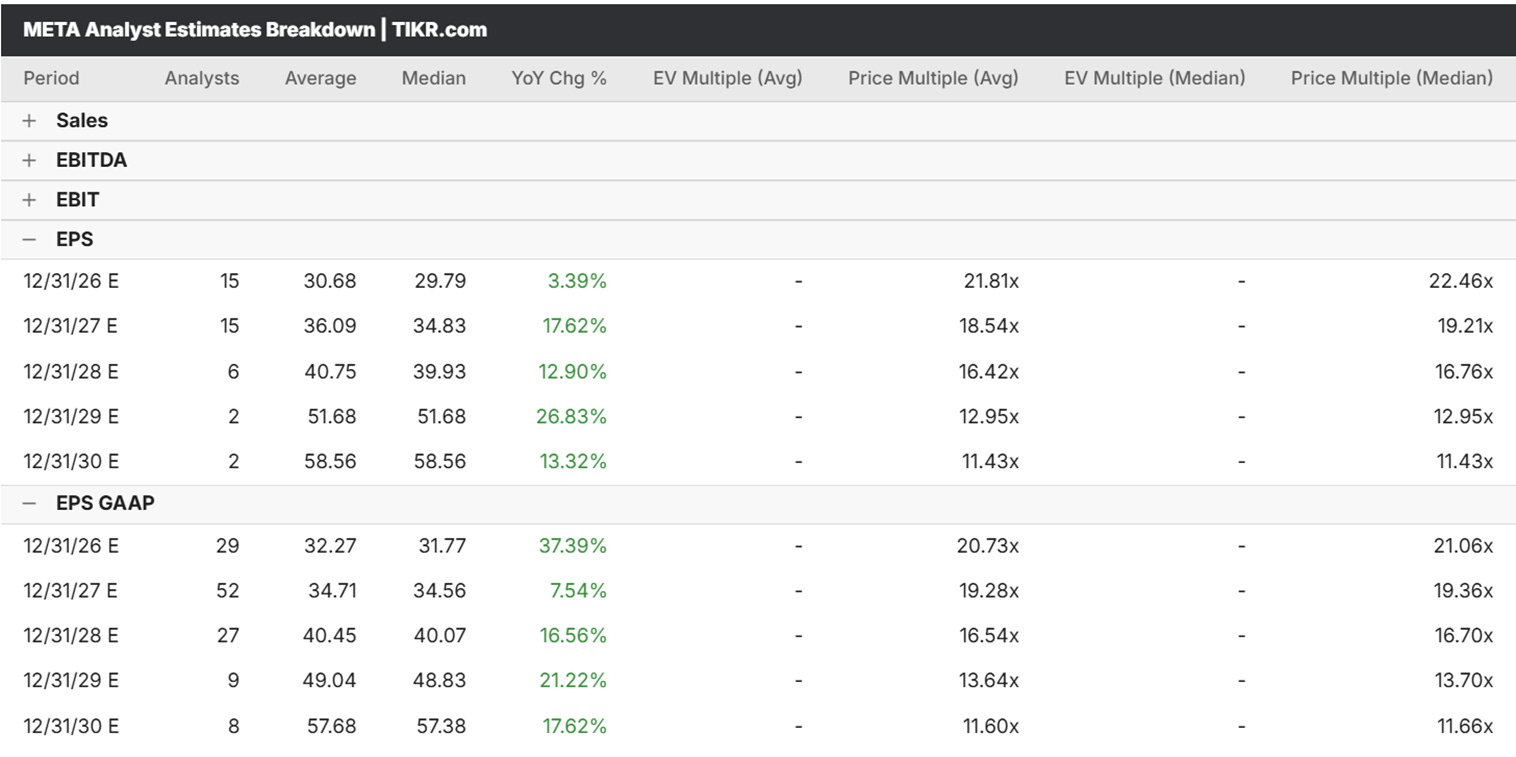

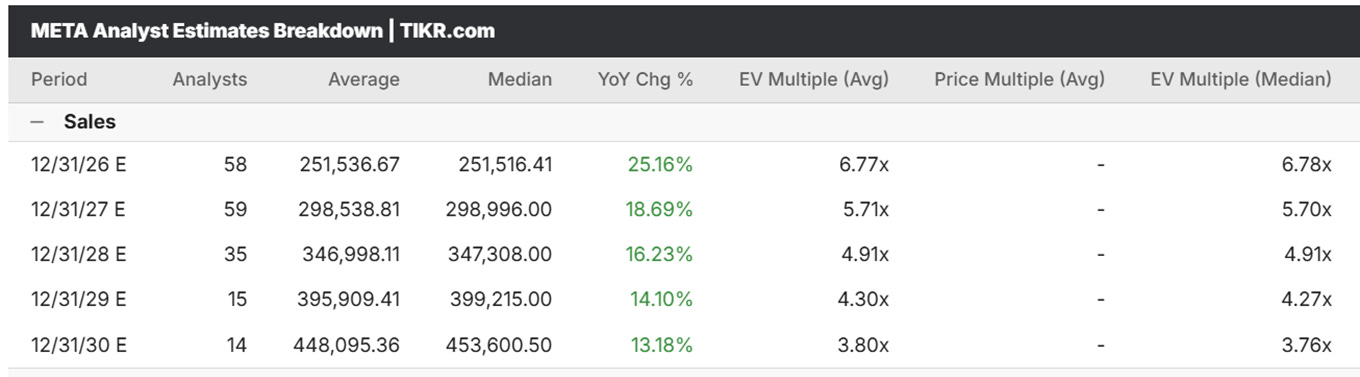

Using a stock price of $600 for Meta, it trades at approximately 18.75x 2026 GAAP EPS of about $32.00 per share, and at 17.4x 2027 earnings GAAP EPS of about $34.50 per share. For context, the S&P 500 trades at 2026 P/E of 22.2x and 2027 P/E of roughly 19.2x. (Estimates below from TIKR, pricing above using market price.)

While Meta is a buy on valuation alone, I also believe the Street’s 2027 and 2028 revenue estimates are still far too low. Consensus calls for +25% YoY revenue growth in 2026, but is forecasting deceleration to less than 20% in subsequent years. I think time will prove this to be overly pessimistic.

As I detailed in my recent analysis of the $1,116 executive stock options, Meta’s underlying engine has the pricing power, the volume expansion, and the new AI revenue streams required to sustain 20%+ YoY growth for the next several years. This Q1 print proves that thesis is intact.

I firmly believe that Meta stock does not deserve to trade at a discount to the broader market, and will not stay this way forever. When management tells you exactly how they are going to build a trillion-dollar moat, and the real-time data shows the plan is working, you don’t sell in after-hours due to a CapEx spike. I am maintaining my Outperform rating on Meta.

META 0.00%↑ , GOOG 0.00%↑, GOOGL 0.00%↑, PINS 0.00%↑

-Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.

Great article man, actually interesting which is rare to find

Subscribed, would love to have you along too🙂