Back to the EBITDA: Decoding Meta’s $1,116 Executive Playbook

How to read SEC Form 4s like an insider and reverse-engineer the 2028 income statement.

Accrued Interest TLDR: Meta’s stock has plunged to $523 on CapEx and lawsuit fears. But while the market panics, Meta’s board just issued a roadmap for the future telling a completely different story. In today’s deep dive, I reverse-engineer CFO Susan Li’s recent SEC Form 4 to reveal the board’s true baseline target: a $1,116 share price by early 2028. I break down the math required to get there. Read the full article to learn how to decode these executive filings for yourself, and discover why this week’s selloff actually makes management’s massive payout easier to hit.

I. Introduction: Ignoring the Noise at $523

Today, we are going back to the fundamentals. We are going to look at the massive new executive compensation agreements Meta just filed. Nobody can predict the future, but I am going to show you how to read these legally binding SEC filings so we can understand the precise financial targets Meta’s own leadership is betting their wealth on hitting in the next couple of years.

It has been a brutal week to be a META 0.00%↑ shareholder.

The stock is down 13% over the last week, down over 20% year-to-date, and down 13% over the last year, currently trading around $523. Just a few days ago, when the stock was hovering near $590, I published my deep dive, Zuckerberg’s Middle-Age Metabolism: Trimming Fat to Fund Superintelligence. Since then, the market has decided to panic.

The selloff is being driven by a cocktail of headline fears. Meta recently lost a court case regarding social media harm to kids, and now some are wondering if this is the company’s ‘Big Tobacco moment’. The Wall Street Journal just published a piece noting that Meta agrees to fund local energy infrastructure for a Louisiana data center. To some investors that screams one thing: runaway CapEx.

It is incredibly frustrating to see a sea of red in your portfolio. But when you have spent enough time in corporate finance looking at how these massive transitions are actually modeled, you learn to spot these headline mirages.

These are surface-level, emotionally driven reactions vastly overstated by the market, and ultimately temporary. Nobody can time the absolute bottom of a stock chart, which is why we must ignore the noise and focus purely on the fundamentals—specifically, what the board of directors is actually doing with their money.

A quick housekeeping note: Accrued Interest is currently 100% free. However, I will soon be moving highly technical, valuation-based deep dives like this one behind a paywall. Subscribe today to ensure you don’t miss the real alpha.

II. The Masterclass: How to Read a Form 4 (The Susan Li Example)

Finding the Right Document

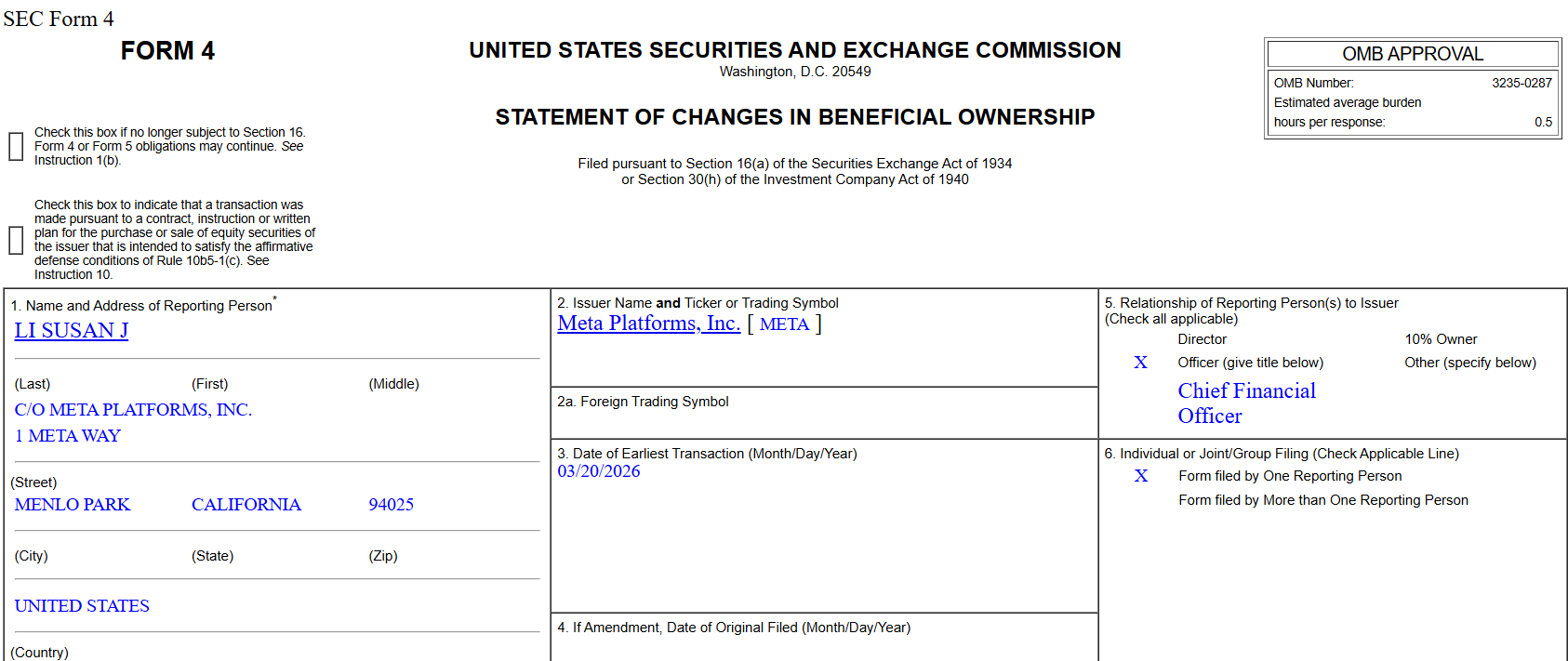

Whenever a corporate insider receives a stock grant, the SEC requires them to file a Form 4: Statement of Changes in Beneficial Ownership. Most retail investors read a blog headline that says a CFO received a bonus and scroll past. But the actual alpha is buried in the tables of that document. If the CFO is accepting a compensation package that requires a massive stock price surge to get paid, you know the internal financial projections support that reality. Let’s pull up CFO Susan Li’s recent Form 4 mega-grant and walk through it.

Filtering Out the Noise

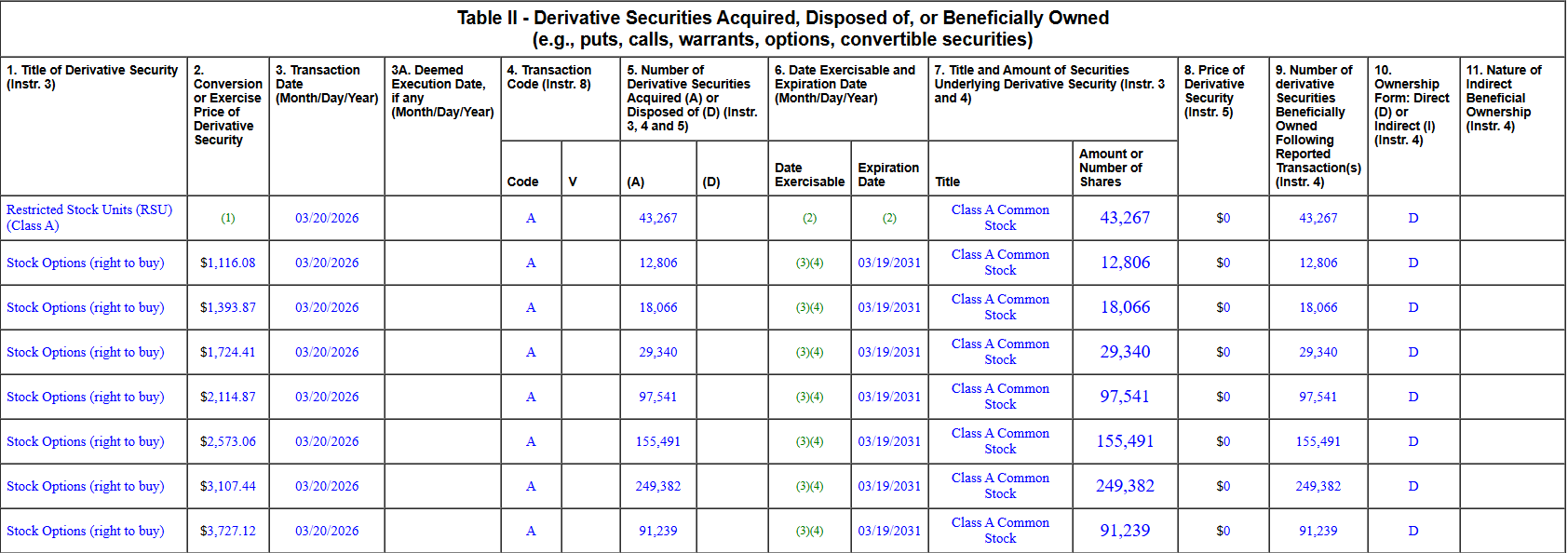

First, you need to skip the noise and go straight to Table II.

When you open a Form 4, you will see two main boxes. Table I is for “Non-Derivative Securities,” which are usually standard Restricted Stock Units that vest simply for showing up to work. We don’t care about those. You want Table II: Derivative Securities. This is where stock options live. When a board wants to incentivize a moonshot, it happens here.

Locating the Price Target

Next, you need to find the Exercise Price in Column 2. This column tells you the board’s precise definition of success. It is the specific price the stock must reach for the executive to cash in. On Susan Li’s filing, you don’t just see one number; you see a ladder. The absolute floor target sits at $1,116.08. The ceiling tranche maxes out at $3,727.12. The board is explicitly telling the CFO that she must get the stock to at least $1,116, or she gets absolutely nothing from this tranche.

The “Do or Die” Clock

Then, you check the Expiration Date in Column 6. This is the timeline. For this grant, the expiration is listed as March 19, 2031. If Meta’s stock hasn’t hit those price targets by that date, these options expire completely worthless. It reveals the absolute maximum timeline for their AI supercycle to mature.

The Secret in the Footnotes

The tables give you the what, but the footnotes at the very bottom of the document give you the how. The footnotes reveal a hidden Price Vesting Period that runs strictly through February 14, 2028. The board didn’t just give management until 2031; they put a massive early-action accelerator in place for early 2028. They also included a secondary buffer period extending to August 15, 2030, for any options that missed the early 2028 accelerator, but the primary incentive is built around that two-year sprint. This proves management is operating on an incredibly urgent timeline to drive multiple expansion.

III. Reverse Engineering the $1,116 Floor Target

The 50% Annualized Hurdle

For the sake of this exercise, let’s be conservative. We are going to ignore the $3,700 moonshot—we will revisit that $9 Trillion market cap scenario in a future article—and focus strictly on what it takes to hit that primary $1,116 floor target by February 2028.

What we are doing here is working backward from the board’s required share price to see what the actual income statement needs to generate to support that valuation.

Let’s look at the Compound Annual Growth Rate reality. To get from today’s panic-induced $523 share price to $1,116.08 in roughly 1.88 years, by mid-February 2028, requires a ~50% annualized return.

How does a company already valued at over $1.3 trillion actually compound at ~50% for two years? We have to reverse-engineer the math. I am going to start with what I believe is a standard 25x P/E multiple for Meta.

Working Backward from the P/E Ratio

1) Assuming a 25x multiple, hitting a $1,116 share price requires roughly $44.64 in Earnings Per Share (EPS). For context, Meta’s 2025 Diluted EPS was $23.49. Management is modeling to nearly double their per-share profits in two years.

2) Factoring in Meta’s historical habit of retiring shares via buybacks, which would reduce the share count from 2.57 billion down to roughly 2.48 billion by 2028, Meta needs to generate roughly $111 Billion to $115 Billion in Net Income. Again, for context, Meta’s 2025 Net Income was $60.5 Billion. They need to find an additional $50 Billion or more in annual profit.

To figure out what the top-line needs to look like, we have to gross that net income up by Meta’s forecasted tax burden.

3) Management has guided for a forward tax rate of about 15%. To clear $112 Billion in net income after Uncle Sam takes his cut, Meta needs to generate roughly $132 Billion in Earnings Before Taxes (EBT), which essentially mirrors our Operating Income target. That is a massive jump from the $83.2 Billion in operating income they generated in 2025.

IV. The Revenue Bridge to $315 Billion (And Beating the Street)

The Margin Disconnect with Wall Street

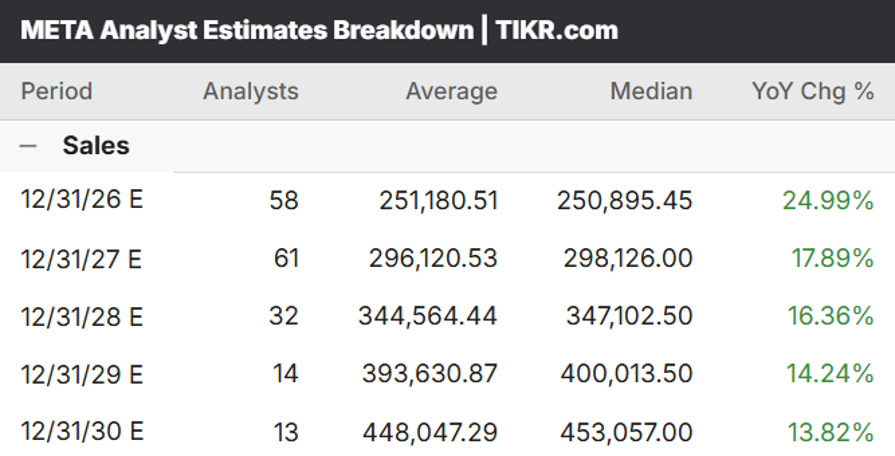

4) To generate $132 Billion in operating profit at their current 42% operating margins, Meta requires a revenue base of roughly $315 Billion by early 2028 (late 2027). This is a huge leap from the $201 Billion they did in 2025 - but not that far ahead of current Street estimates. Let’s discuss further.

5) If you look at consensus estimates, the Street expects Meta to grow well this year (2026), but then decelerate down to 17.89% in 2027 and 16.36% in 2028. The Street expects roughly $296 Billion in top-line revenue in 2027.

6) To hit the $315 Billion target required for their payout, management’s internal models imply sustaining roughly 25% annualized revenue growth. They are structurally incentivized to beat Wall Street consensus by nearly $20 Billion. I think this is very reasonable!

Next - let’s model how revenue can grow to hit these targets. This is just a thought exercise to see what is possible, but when you break down the segments, you should realize this is a very achievable outcome the market is overly discounting in the P/E multiple.

Squeezing Value from the Core Ad Engine

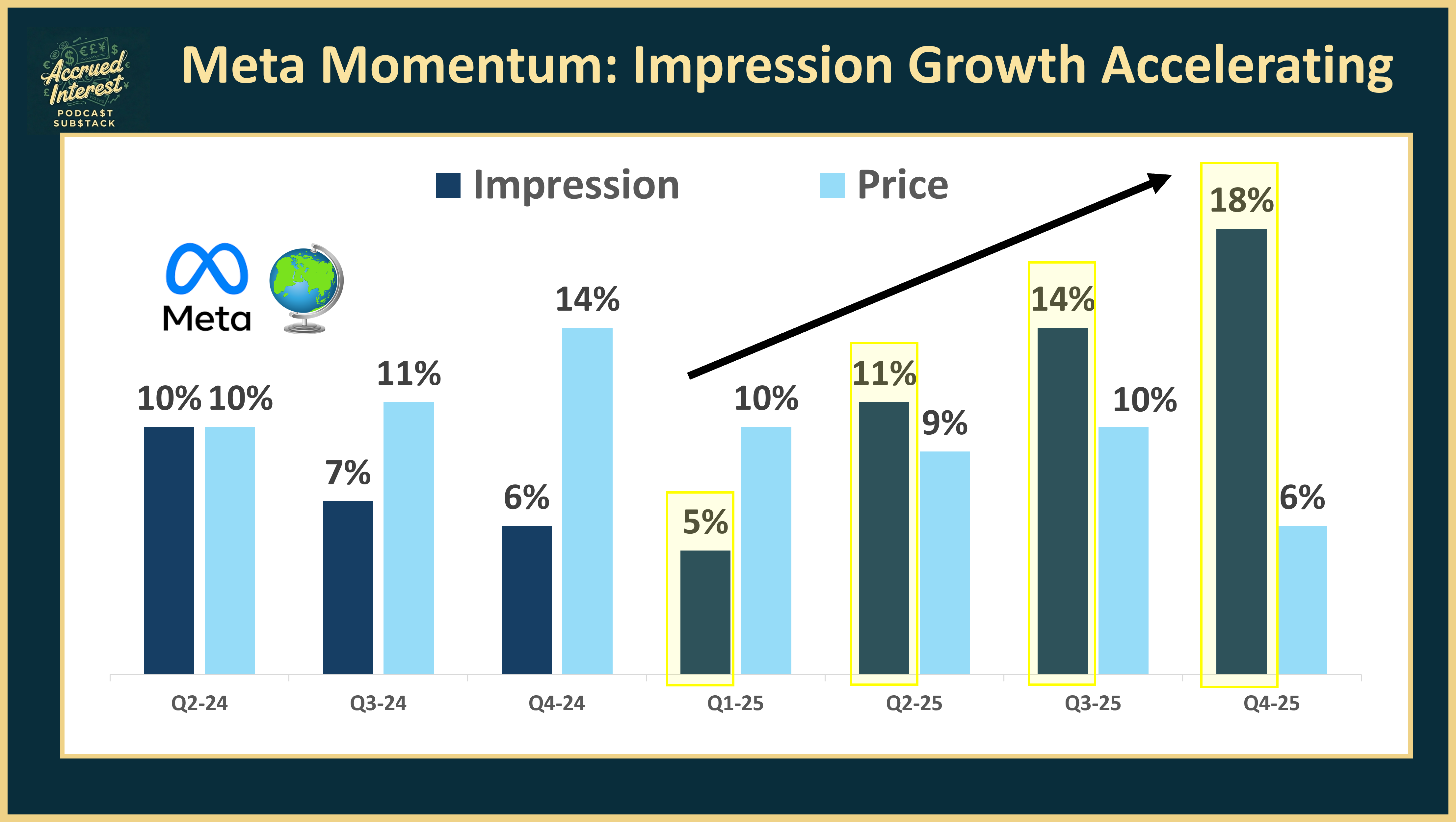

7) First, we look at the Core Ad Engine. This baseline grows through a mix of volume (ad impressions) and pricing power. I am modeling 12% to 15% YoY impression growth, driven by AI recommendation feeds keeping users scrolling longer on Reels, which matches their recent year-over-year ad impression growth.

Combine that with 10% to 12% YoY pricing growth. Historically, higher volume meant cheaper ads. But as tools like Advantage+ and Agentic AI drive significantly higher Return on Ad Spend (ROAS), Meta should be able to charge advertisers a premium.

The $20 Billion “Other Revenue” Bridge

8) Then, we have the “Other Revenue” kicker. This part is the most speculative part of my analysis, but we need this Other Revenue bridge to fill the gap to our total $315 Billion target.

Meta’s “Family of Apps - Other Revenue” segment is currently a $3 Billion baseline. Management’s 2028 trajectory likely relies on scaling this to $15 Billion to $20 Billion. Here are the buckets where Meta can potentially generate this revenue.

The first bucket is what I am calling Meta’s communication toll-bridge, which could reach $8 Billion. This involves scaling the WhatsApp Business API by penetrating the US and European enterprise markets, transitioning companies away from legacy SMS and standard email marketing.

The second bucket is AI Agent SaaS, potentially a $6 Billion to $7 Billion business. This means charging a monthly subscription or a premium per-resolution fee to provide autonomous AI agents that handle customer service and sales directly on their platforms, replacing human reps.

Finally, the third bucket is In-Thread Commerce, adding another $2.5 Billion to $3 Billion. Meta can take a small toll on Gross Merchandise Value for transactions fully executed by their AI agents within a WhatsApp or Instagram DM thread.

V. The Balance Sheet Evolution & The Metabolic Swap

The Data Center Depreciation Hit

9) I know the market is worried about expenses right now, especially with massive CapEx numbers hitting the headlines. But I see a clear, highly achievable path for Meta to keep their margins intact. That is the most important takeaway of this entire exercise: Meta does not need to sacrifice its profitability to fund its future.

Yes, the CapEx bill is huge. Spending $115 Billion to $135 Billion on infrastructure means depreciation expenses will spike higher in the future. If we assume they spend $120 Billion and depreciate it straight-line over an extended 4.5-year useful life, they are adding an incremental $15 Billion to $20 Billion in annual depreciation to the income statement by 2028.

How the “Metabolic Swap” Saves Margins

To protect the bottom line, management has structured the income statement to absorb this CapEx shock through what I call the “Metabolic Swap“ I alluded to in my last Meta article. While depreciation balloons by $20 Billion, Meta is offsetting it almost immediately in other areas.

First, there is Reality Labs’ surrender. By trimming the fat in Reality Labs—scrapping the lowest-performing hardware projects and shrinking that annual bonfire from $16 Billion down to a baseline of $5 Billion to $6 Billion—they add roughly $10 Billion to $11 Billion directly back to Operating Income.

Second is workforce reduction. Meta is reportedly looking at a 20% reduction in workforce. Cutting roughly 13,400 heads at a fully loaded cost of $275,000 per employee yields roughly $3.7 Billion in immediate, hard cash operating expense savings.

What we are seeing is Meta swapping human payroll and speculative VR hardware for hard AI infrastructure. The net margin impact is largely neutralized.

By doing this, operating margins can stay intact at around ~42%, allowing that massive $315 Billion in new revenue to flow straight to the bottom line without being entirely eaten by data center costs.

Embracing Middle-Age Leverage

Furthermore, as Meta transitions to a mature cash-flow machine, they are evolving their balance sheet. Historically, Meta carried zero debt. To fund these massive infrastructure projects, they are going to start carrying leverage. This is not a red flag. It is standard, efficient corporate finance. As long as top-line revenue is growing at a 25% clip, that debt is easily serviced and represents an optimal capital structure for a business of this size.

CONCLUSION: Conviction in the Chaos

The Board’s Legally Binding Bet

Stock prices will always be volatile. They will plummet because of courtroom drama, macro-economic jitters, and out-of-context headlines about power grids. We cannot control the noise. But we can read the tape. The fundamental reality is that the CFO and the Board of Directors have locked themselves into an incredibly aggressive, legally binding contract that pays out only if they deliver massive earnings expansion by 2028. The stock price will eventually, inevitably, follow the earnings.

The Share Repurchase Weapon

There is also one crucial corporate finance distinction to remember during this selloff: the more the stock price falls today, the easier it is for them to hit their targets tomorrow. If the stock continues to drop below $500, Meta’s massive cash pile becomes an exponentially more powerful weapon for share repurchases.

Buying back cheap stock juices the EPS, making those per-share targets much easier to achieve without needing a single extra dollar of revenue. I didn’t heavily rely on massive share buybacks for the math in this article, but if the stock stays down, that lever is absolutely on the table.

Looking Ahead to Q1

Q1-26 earnings are about four weeks away. We will get a fresh, hard look at the actual business very soon. Until then, the market can keep falling, but I will keep following the fundamentals. This reverse-engineering exercise gives me supreme conviction that my $850 price target from my previous article was actually highly conservative. Focus on the machine, not the headlines.

-Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.

First of all, great piece of work. A lot of interesting points raised about "Other Revenue". Just wanted to add a couple of points about the lawsuit that people do not understand in my opinion:

Advertisers buying attention and behavioral data on Meta's platforms aren't purchasing access to minors. That inventory was never part of the monetizable product to begin with and had never been sold. So even after court appeal (that Meta said they are working on), if regulations will be tightened in regards to kids on social media this does not harm the company's operations. I believe the core reasoning behind this massive sell off is that people do not completely understand the Meta's Business Model.

Great Deep Dive! How sustainable is Meta's “Year of Efficiency” narrative if the current expansion in Adjusted EBITDA is being driven by capitalizing massive AI infrastructure costs, and at what point does the widening gap between GAAP Net Income and these adjusted metrics signal a capital intensity risk rather than true operational leverage?