The Release Valve on the CapEx Bill: What Meta’s Compute Plan Actually Signals

A hedge on the biggest infrastructure bet in the company’s history.

Accrued Interest TLDR — Wall Street has spent months treating Meta’s $125–$145 billion CapEx cycle as a black hole. This morning, Bloomberg reported that Meta is standing up a business — Meta Compute — to sell access to its AI models and raw compute, and the stock rallied more than 11% to around $627. This is not a war on AWS. It is a high-margin release valve on the AI buildout that has the Street so anxious, and management has been signaling it for three straight quarters. A Wells Fargo model shows that reselling a single gigawatt of Meta’s projected 2028 AI capacity could add roughly $5.69 to EPS. I have stayed Outperform all year, and I am heading into the late-July Q2 earnings release with anticipation. Follow the earnings, not the noise.

Please subscribe (free) to read the rest of this Accrued Interest deep dive. I send these to 1,400+ investors and operators who care more about what really moves the needle than what the spreadsheet whispers.

1. Follow the Earnings, Not the Noise

Narratives shift. The media noise does not stop. But if you want to know where a stock is going over time, you follow the earnings. That has been the North Star here at Accrued Interest, and it is the lens I want to bring to this morning’s news on Meta.

Before the market opened on July 1, Bloomberg reported that Meta is developing a cloud infrastructure business to sell access to AI computing power and models. Two paths are on the table. The first is selling access to models hosted on Meta’s own infrastructure — including its Muse Spark models — in a setup that resembles AWS’s Bedrock. The second is selling access to raw computing capacity, closer to what a neocloud like CoreWeave does. Both sit inside an internal effort called Meta Compute, led by infrastructure head Santosh Janardhan, Superintelligence Labs’ Daniel Gross, and Meta President Dina Powell McCormick. The market’s reaction told you how it read the headline: Meta rallied more than 11% on the day to around $627, while CoreWeave fell nearly 10%.

I want to put that move in context, because I have been beating this drum all year. Through the first half of 2026, while plenty of investors turned skittish on the AI spend and pushed the stock down toward its 52-week lows, I kept my Outperform rating in place. Today’s rally is the market starting to catch up: with this pop, Meta is now down only about 5% year-to-date, clawing back a good chunk of the underperformance that had built up over the past six months.

I don’t think that repair is finished.

Now the reframe, because this news is being read two ways, and both are off. The bears see Meta flooding an already-nervous compute market, which is why the neocloud names sold off. Others see Meta pivoting into a non-core business — chasing Azure and AWS, straying from what it does best: serving digital advertising at scale. I think it is neither. What Meta is describing is a release valve for its AI infrastructure spend — a way to monetize excess, already-funded capacity at a high margin when internal demand does not consume all of it. Read that way, this news does not add to the CapEx worry. On the contrary, I think it is an answer to it.

2. Meta Has Been Signaling This for Three Quarters

This was not a reactive pivot dreamed up to appease Wall Street. Management has been laying down breadcrumbs for the better part of a year, and if you were listening to the calls, none of this should surprise you.

Start on the October 29, 2025 Q3 earnings call. With CapEx fears already building, Zuckerberg floated the idea plainly: “Obviously, if you got to a point where you overbuilt, you could have that as an option.” That was the first public hint that overbuilding was not a risk to fear but an option to hold.

By the April 29, 2026 Q1 call, and again at the May 27 annual shareholder meeting, he revealed where the demand was coming from: “Almost every week there are different companies that come to us from the outside asking us to both stand up an API service or asking if we have compute that they could buy from us at some premium to what we’ve bought it at.” That is not Meta hunting for customers. That is inbound demand showing up on its own, at a premium.

Then, at that same May meeting, asked directly about competing with Amazon and Microsoft in the cloud, Zuckerberg confirmed that selling excess compute is “definitely on the table.” So by the time this morning’s report landed, the only new information was that the plan now has a name and an org chart.

The strategy itself has been public for three quarters. The reaction you are seeing in the market is a reminder that not all publicly available information has already been “priced in” by Mr. Market.

3. The Compute Math: A Release Valve, Not a Dead Asset

To move from narrative to numbers, I want to walk through an exhibit I came across from a recent Wells Fargo note. (A quick note to readers: I found this as a clip on Twitter, so if you have the full research note, please send it my way!)

One of my favorite quotes about investing comes from the statistician George Box, and I keep coming back to it: all models are wrong, but some are useful. That is the way to view this Wells Fargo math. The direction is what matters, and it is hard to ignore.

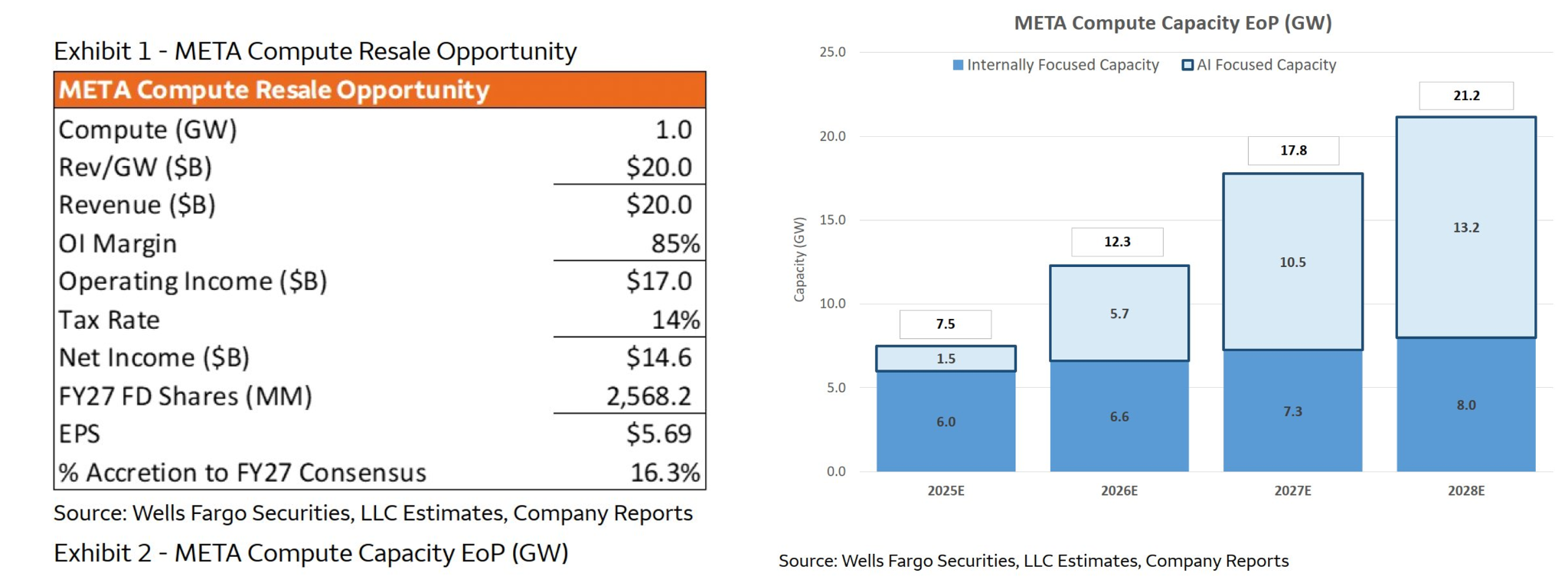

Start with the capacity picture. Wells Fargo maps Meta’s total end-of-period power footprint growing from 7.5 GW in 2025 to 21.2 GW by 2028. What makes the exhibit useful is that it splits that footprint into two buckets.

Internally focused capacity — the power that keeps the core ads and recommendation engines running — grows at a steady, unremarkable pace: 6.0 GW in 2025 to 8.0 GW in 2028.

The AI-focused capacity is the surge that has spooked the market: 1.5 GW in 2025, then 5.7, 10.5, and 13.2 GW through 2028.

That split tells you management is not spending blindly. They can see, granularly, what is required to protect the core business versus what is forward-looking AI optionality.

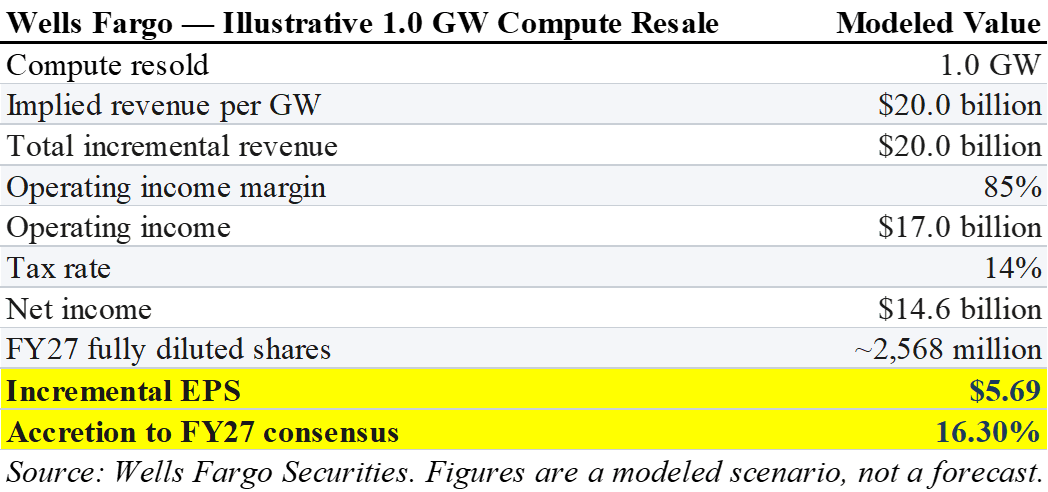

Now the unit economics. Wells Fargo reverse-engineers what happens if Meta peels off a single gigawatt of that AI capacity for third-party resale. From their exhibit, I pulled the following values to make the point:

The number that carries the argument is the 85% operating margin. It is that high for one reason: the infrastructure is already paid for. The CapEx cycle funded the buildings and the silicon, so the incremental cost of letting an outside developer run workloads on capacity you were not using is low. And note the scale of what is being modeled — one gigawatt out of a projected 13.2 GW AI footprint. Reselling under a tenth of the excess adds roughly $5.69 to EPS and a 16.3% bump to the FY27 consensus. I am not claiming Meta resells one gigawatt at $20 billion per gigawatt on any set schedule; uptake and pricing are open questions. The point is that even a fraction of this capacity, monetized, moves the earnings line in a way the current CapEx panic does not contemplate.

4. “Building a NeoCloud and Renting Capacity Aren’t Contradictory”

Here is the obvious pushback, and it deserves a real answer. If Meta has surplus compute to sell, why did it recently lock in another 1.6 GW from Crusoe across data centers in Childress, Texas and Warrenton, Missouri? Isn’t reselling compute a sign that demand has peaked?

Before I lean on the best answer I have read to that question, let me give Funda AI their flowers. Their research on Meta — and across the broader tech and AI-infrastructure names — has been some of the most consistently sharp work I follow. I am pointing you to their note because they framed this issue better than I could, and I would rather credit their thinking than repackage it as my own. The piece is titled “META: Building a NeoCloud and Continuing to Rent Capacity are not Contradictory,” and the title is the thesis.

Their read, which I share, is that this is not a story about AI compute demand peaking, but a generational shift in what compute is for. Over the past two years Meta bought and deployed large quantities of H100 and H200 GPUs. Those chips are far from worthless — they remain valuable for inference, fine-tuning, enterprise model serving, image and video generation, and traditional ML. But for training the next generation of frontier models — 3T-plus-parameter mixture-of-experts, long context, RL-heavy post-training — the cost per effective token on H100/H200 rises meaningfully versus GB200, GB300, and the coming Vera Rubin systems.

That leaves Meta with a classic asset-allocation problem. Reserve the newest, scarcest silicon for frontier training; shift the prior-generation fleet toward inference or external monetization. Seen this way, the Crusoe lock-in and the neocloud plan are not in tension — they are two sides of the same decision. The 1.6 GW from Crusoe is strategic supply for the GB200/GB300/Rubin era. The resale plan recycles capital tied up in the H100/H200 fleet that no longer belongs at the frontier. It is the same logic xAI has already run in public: it rented Colossus 1 compute — a cluster of more than 220,000 NVIDIA GPUs spanning H100, H200, and GB200 — to Anthropic while keeping its newest clusters for its own models. Bloomberg Intelligence estimates that strategy could drive xAI past $50 billion in revenue by 2028.

And if you want hard evidence that there is no glut for Meta to worry about, look at what the Financial Times reported on June 28, three days before this morning’s news. Google has capped Meta’s use of its Gemini models.

Per the FT, Google told Meta back in March that it could not supply all the capacity Meta wanted to buy, and those limits remain in place, disrupting some of Meta’s internal AI work. One of the largest, best-capitalized infrastructure owners on earth had to ration a marquee customer because it could not meet demand. Google’s own CEO said it plainly on the April call: “Obviously, we are compute-constrained in the near term.” Compute is the scarcest input in tech right now, not a surplus commodity — and that fact was reported days before the market decided Meta’s plan spelled oversupply.

That is why I think the bearish read on this morning’s news — Meta enters the neocloud space, therefore the neoclouds get crushed — is overdone. As the Funda AI note frames it, the compute market is moving from a single, undifferentiated GPU shortage into a phase of tiered pricing and tiered usage across chip generations. Older GPUs do not go to zero, and the newest GPUs stay scarce. Meta building a neocloud is not a signal that demand has collapsed. It is a signal that compute assets are being financialized — turned from a single-use training tool into a multi-generation, income-producing asset.

5. Mr. Market’s Operational Blind Spot — and the $1,116 Bridge

So why does Meta’s potential keep getting underrated? I think the analysts largely have this right — earlier in this piece I leaned on their own consensus to show how accretive the resale math would be. But Mr. Market, whose mood swings move the stock day to day, tends to misjudge Meta, and I think it is because most investors are spreadsheet jockeys who have never had to actually run a small business.

Meta’s margin story was built on self-service. Unlike legacy media or bloated enterprise-software companies, Meta never needed a large, expensive direct sales force. Millions of businesses log into the same dashboard, configure their own campaigns, and buy their own inventory — the software does the selling. That is the mechanism that allowed the company to scale revenue for years without scaling headcount at the same rate.

AI compute and hosted agents are the next generation of tools in that same dashboard. Giving a business API access to Muse Spark inside the interface it already uses every day is a low-friction upsell to a captive base, not a ground-up enterprise sales campaign against AWS. If you have never sat on the other side of that dashboard — buying ads to keep a small business alive — it is easy to miss how sticky and how natural that upsell is. That is the truth the market keeps discounting: it treats the AI spend as pure cost rather than the plumbing for the next set of high-margin tools.

This is where the compute plan connects to work I have already done. In “Back to the EBITDA: Decoding Meta’s $1,116 Executive Playbook,” I walked through the board-approved executive option packages, which do not begin paying out until the stock clears an absolute floor of $1,116.08 by February 2028, with higher tranches escalating well beyond that. Hitting the EPS required to justify that price is not something the core ad business does on its own; it requires new, high-margin revenue lanes. The compute resale model is a tangible one. Wells Fargo’s roughly $5.69 of incremental EPS from a single gigawatt is not the whole bridge from today’s $627 to a $1,100 handle — but it is a visible plank in it, and this morning I learned the company is building it.

Conclusion — The Setup Into Earnings is Attractive

Meta’s Q2 2026 results are expected at the end of July. My discipline has not changed: I do not make large portfolio moves ahead of the conference call.

But I will tell you how I read the timing. Companies do not surface plans like this from a position of weakness. Meta is letting these details out because it is confident in the underlying business. My expectation is that the upcoming Q2 earnings will confirm it — that the revenue acceleration we saw in Q4 2025 and Q1 2026, up roughly +33% year-over-year, is still intact. I think investors will soon be reminded that the earnings-growth case is stronger than many of them currently believe.

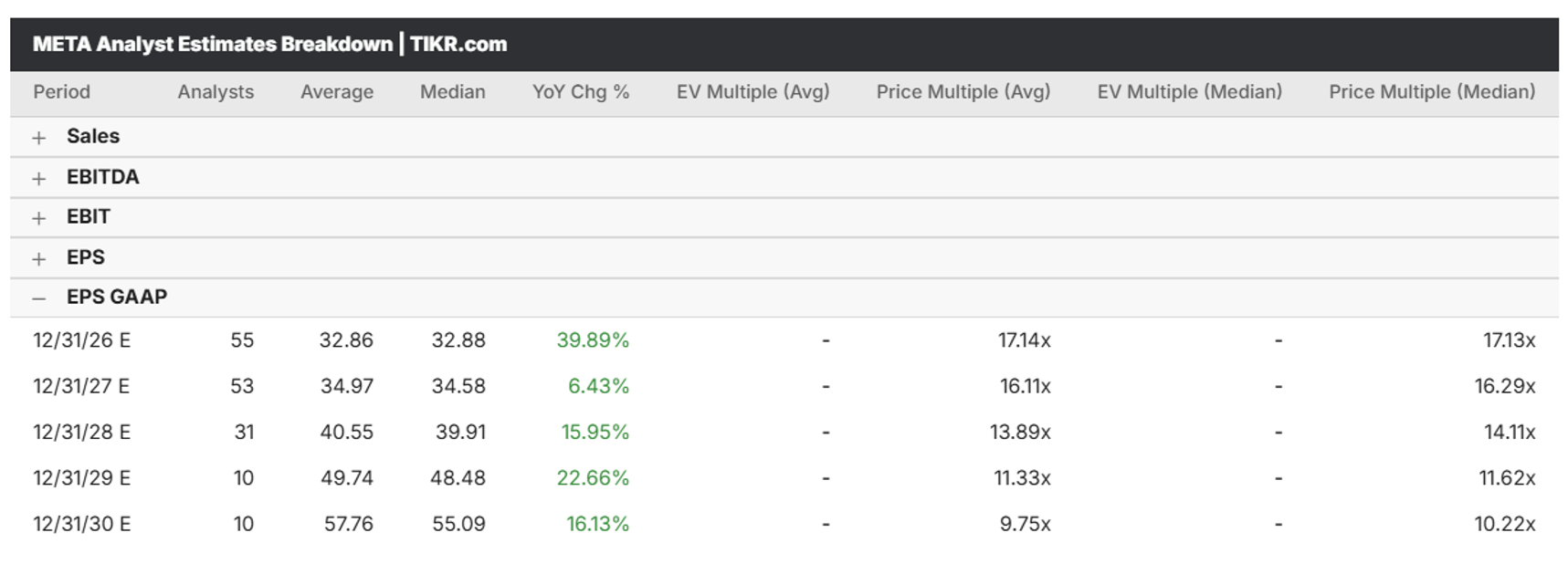

On valuation, I won’t bury the lede — Meta is still trading like a cheap value stock. As of early July, the consensus GAAP EPS I am working from (TIKR, shown in the exhibit) is $34.97 for 2027 and $40.55 for 2028. Against Meta’s prior close of $563, those estimates put the stock at about 16.1x 2027 and 13.9x 2028 earnings. Even after today’s 11% run to $627, Meta trades at only around 17.9x 2027 and 15.5x 2028 GAAP EPS. A mid-teens multiple on 2028 earnings, for a business still growing its top line north of 25%, is not an expensive stock. As I have argued before, I think these consensus numbers are still too conservative, which leaves Meta plenty of room to keep proving its doubters wrong.

Strip away the noise and the setup is straightforward. If internal products absorb the compute, the ad machine keeps compounding and pays for the buildout. If Meta overbuilds, it monetizes the excess at a high margin into a market that — as Google just reminded us — cannot get enough of it. Both roads are friendly to shareholders, and that is what a hedge is supposed to look like.

I am maintaining my Outperform, and I will be tuning in to earnings with great anticipation.

Relevant tickers: META 0.00%↑, GOOG 0.00%↑, GOOGL 0.00%↑, CRWV 0.00%↑

— Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.