Spotify ($SPOT) Q1 2026 Earnings: The Audio Illusion Unravels

Why 70% of new users are "empty calories" and the 33x multiple is a dangerous trap.

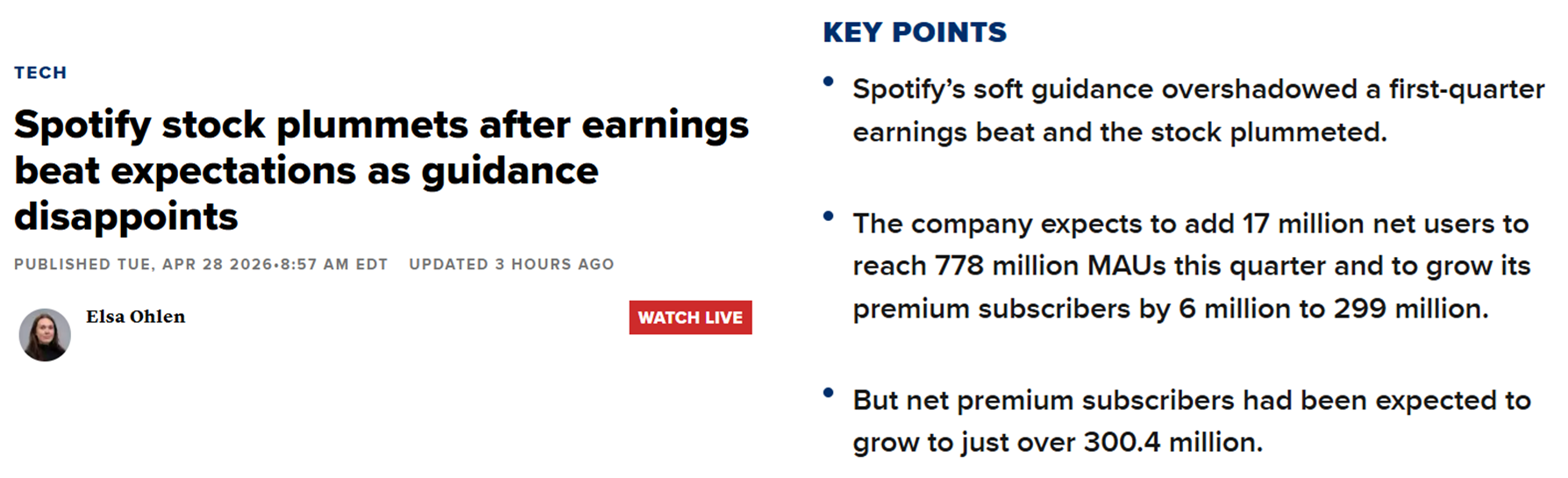

Accrued Interest TLDR: Spotify’s stock plummeted 13% post-earnings, and the sell-off is completely justified. While Q1 operating income and free cash flow beat expectations, the underlying growth engine is stalling. Q2 subscriber guidance missed by 33%, exposing a ceiling on pricing power. Worse, 70% of new users are joining the ad-supported tier, where revenue actually declined 5% year-over-year. Spotify is structurally capped by music royalties, making its 33x forward multiple dangerously overpriced compared to true media winners like Meta and Google. I rate SPOT an Underperform. SPOT 0.00%↑

Introduction

If you have been reading Accrued Interest for a while, you know my golden rule for media investing: Follow the growth in intrinsic value, not just the headlines. When a company misses the mark, I want to look under the hood to see if the market is overreacting to a temporary blip, or if it is finally waking up to a structural flaw.

This morning, Spotify reported its Q1 2026 earnings, and the market ruthlessly punished the stock, sending it down 13%. While many retail investors see this massive drop as a “buy the dip” opportunity, I see it differently.

Having spent over 15 years inside media boardrooms, I’ve learned to decipher when an investor relations deck masks a deteriorating core engine. The Q1 print revealed an audio-first business model hitting a hard ceiling. At current valuations, this stock is a value trap.

Here is why I am initiating with an Underperform rating on Spotify, and why true digital media winners like Meta, YouTube, and Netflix will leave it in the dust over the next 18 months.

I. The Q2 Guidance Whiff Signals a Top-of-Funnel Drought

Wall Street does not price growth stocks based on the customers they have already acquired; it prices them based on their future cash flows, which are dictated by the rate at which they are acquiring new users. This is where Spotify’s Q1 report was a disappointment.

Management guided for just 6 million net new premium subscribers in Q2, missing the analyst consensus of 9 million. Rather than acknowledge a slowing core engine, Spotify’s leadership attempted to downplay the Q2 weakness by framing it as a tough YoY comparison and pushing growth expectations into the second half of the year.

CFO Christian Luiga stated, “We reiterate our previous statement that we expect another full year of healthy subscriber growth, weighted more towards the back half of the year“.

As a former operator, I can tell you that promising that growth is “weighted more towards the back half” is a classic management delay tactic when current quarter numbers miss the mark. It forces investors to essentially take their word that a re-acceleration is coming months down the line. While it is true that subscriber growth is historically strongest in Q4 due to discounting and the organic marketing push of “Spotify Wrapped”, my personal point of view is this sounds like management is dialing back growth expectations.

Price sensitivity is absolutely real when it comes to Spotify. “Mr. Market” correctly interprets the soft Q2 guidance as Spotify struggling to absorb recent price hikes without sacrificing volume. If churn isn’t increasing due to price hikes, then the alternative explanation is that customer acquisition is simply drying up—which is arguably a MUCH worse structural problem for a growth stock like Spotify.

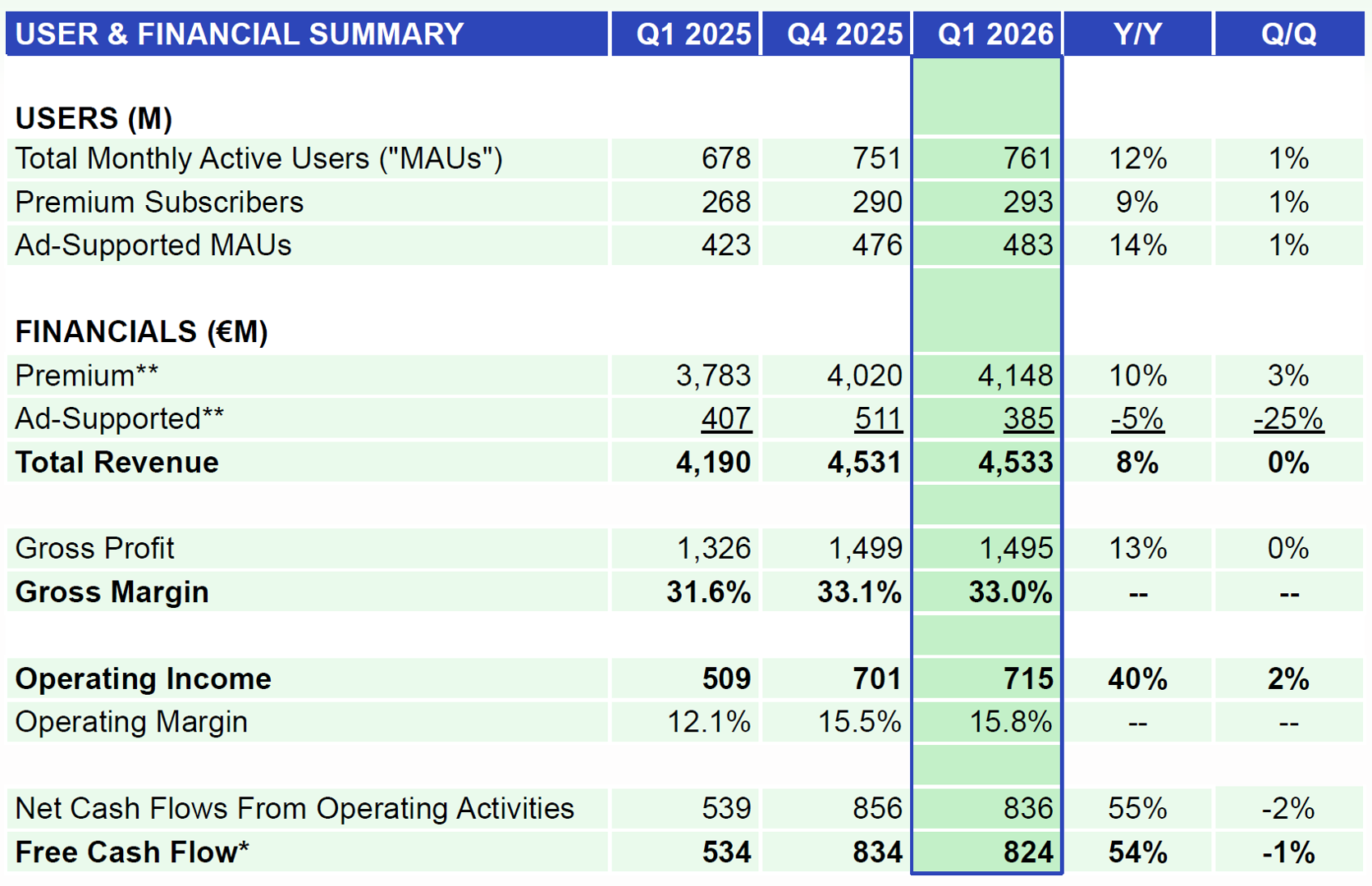

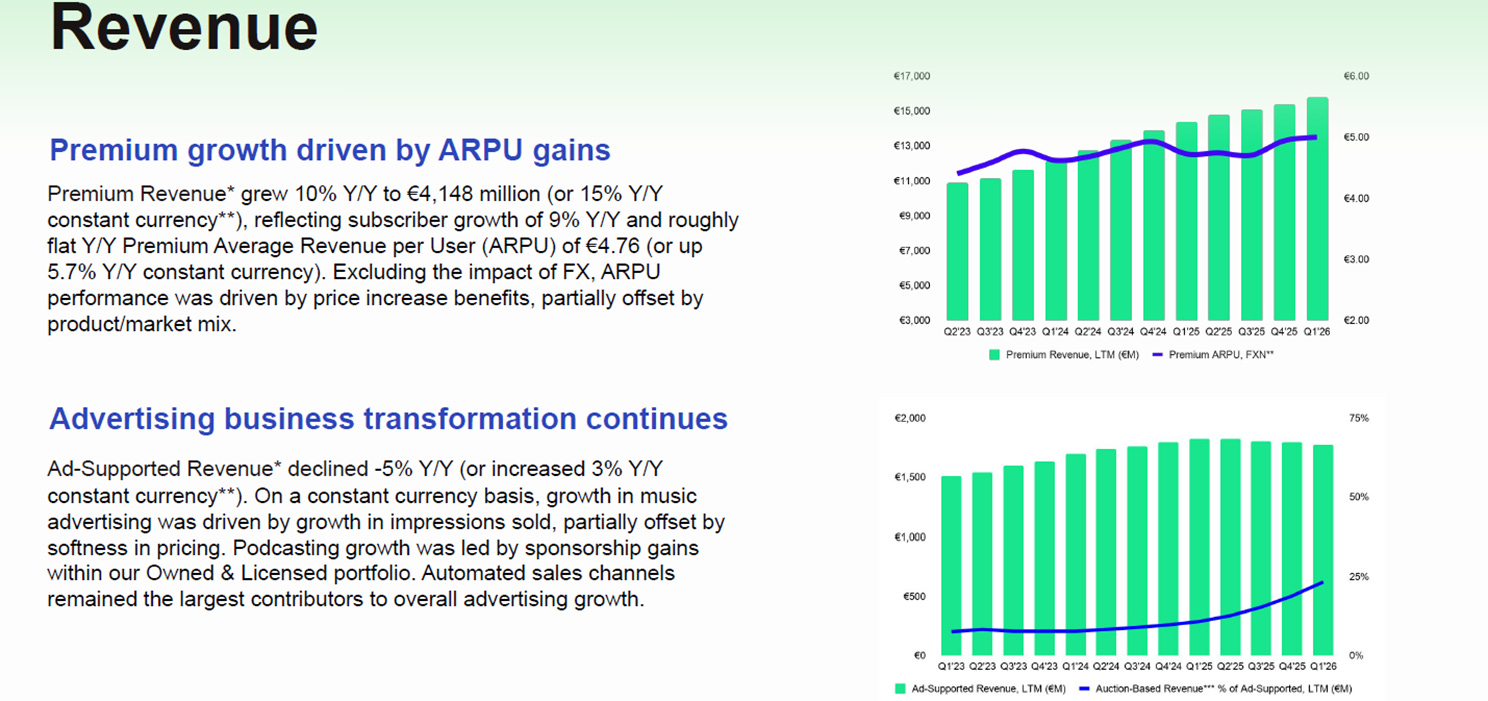

The ARPU (Average Revenue Per User) stagnation in Spotify is very clear. Despite raising prices, ARPU remained relatively flat YoY at €4.76.

Simply put, if aggressive price increases cannot meaningfully drive ARPU higher, the core growth engine is losing its torque, and the P/E multiple must come down.

II. “Empty Calorie” MAU Growth is Masking a Broken Advertising Engine

Spotify is successfully getting people to use the app, but they are struggling to get them to pay for it, leading to growth that looks good on paper but doesn’t translate to the bottom line. This creates a massive top-of-funnel bottleneck.

For Q1-26, Spotify added 10 million Monthly Active Users (beating the 8M guidance), but Premium subscriber net additions came in at a mediocre 3M. MAU growth does not pay the bills if it fails to convert into high-margin subscription revenue.

Let me explain why investors are concerned about the composition of Spotify’s user growth. The ad-supported tier is indeed growing faster than the premium tier, and the ratio of new users skews heavily toward the lower-monetizing segment.

Let’s look at the sequential growth from Q4 2025 to Q1 2026 to see exactly where the new users are going:

For Q1, 70% of Spotify’s net new users joined the Ad-Supported tier (7 million out of 10 million), while only 30% joined the Premium tier (3 million out of 10 million).

Monthly Active Users (MAUs): Grew from 751M to 761M, net addition of 10M.

Premium Subscribers: Grew from 290M to 293M, net additions at 3M.

Ad-Supported MAUs: Grew from 476M to 483M, net additions at 7M.

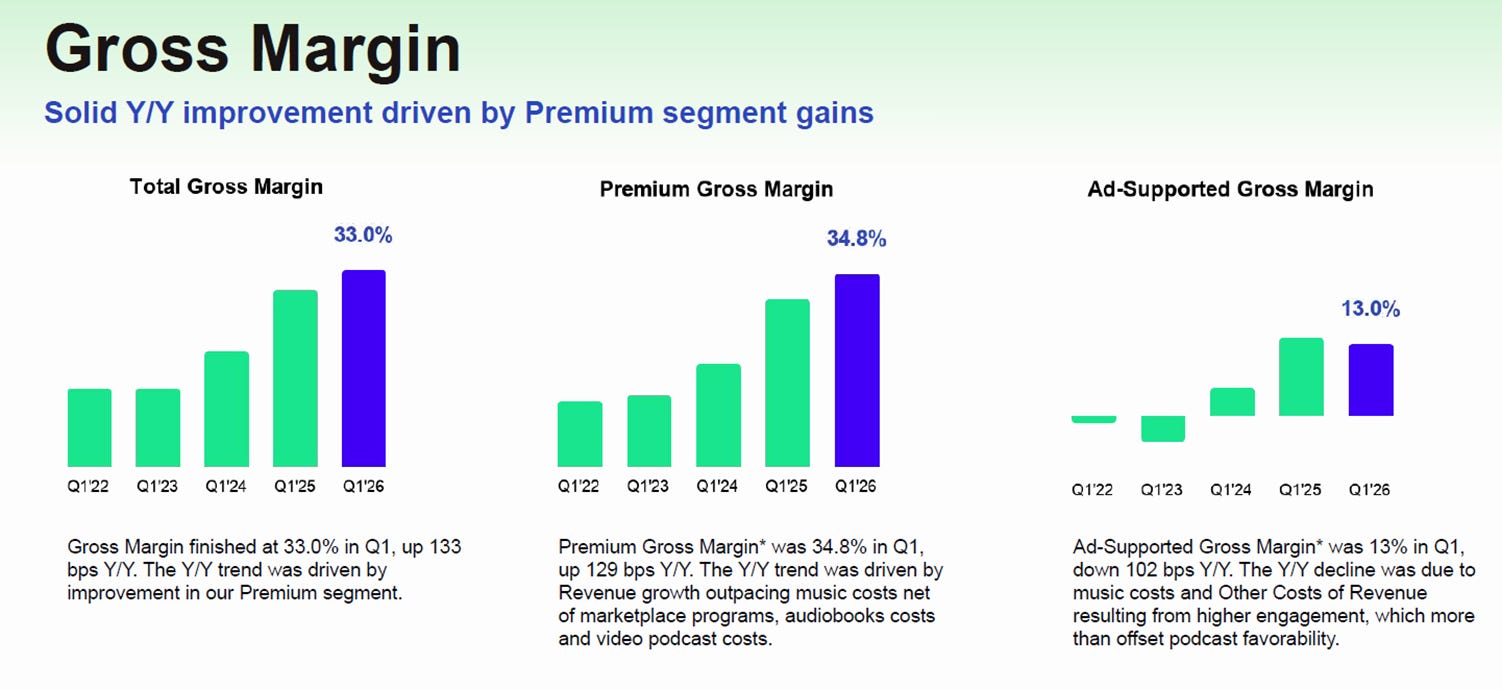

This dynamic perfectly illustrates the “Empty Calorie” MAU growth problem. Top-of-funnel growth looks great on a press release, but it is deeply problematic for the financials when you look at how these two tiers monetize. Despite 483 million users sitting on the Ad-Supported tier, that segment only generated €385 million in Q1 2026. Worse, that ad revenue actually declined by -5% Y/Y. Meanwhile, the 293 million Premium users generated €4,148 million.

Adding millions of free users costs money in streaming delivery, compute power, and royalties. Because ad revenue declined while user engagement increased, the Ad-Supported Gross Margin fell to 13.0% (down 102 basis points Y/Y). Contrast this with the Premium Gross Margin, which expanded to 34.8%.

This is a clear structural flaw that the bulls cannot simply choose to ignore. Spotify is successfully acquiring millions of new listeners, but 7 out of 10 of them are entering a tier with shrinking revenue and deteriorating margins. If they cannot convert these free listeners into premium subscribers, the sheer volume of MAUs acts as a margin anchor rather than a growth engine. Management is clearly trying to spin this story.

The Q1 2026 investor relations deck on slide 9 claims “Premium growth driven by ARPU gains”—but investors should much prefer to see growth driven by users, not just pricing.

The more alarming trend is the lack of traction in Spotify’s advertising business. The bullet point on page 9 stating “Advertising business transformation continues” is classic boilerplate for a failed headline. Even stripping away FX impact, Ad revenue grew only +3% on a constant currency basis. That 3% growth is unacceptable and lags significantly behind the +14% ad-supported monthly user growth reported elsewhere. Investors have been far too sanguine here.

A big picture point is the monetization hierarchy: Audio is the lowest on the totem pole. I have long argued that advertisers have a hard, low ceiling in terms of how much they want to invest in audio, a ceiling investors continue to underestimate.

III. SPOT Bulls Are Drunk on a FCF Sugar High

I want to be fair to the bullish investors and acknowledge that Q1 did present some optical highlights. The Q1 2026 report contained several strengths that the bulls will be using to defend the stock. Here is the ammunition the other side is working with…

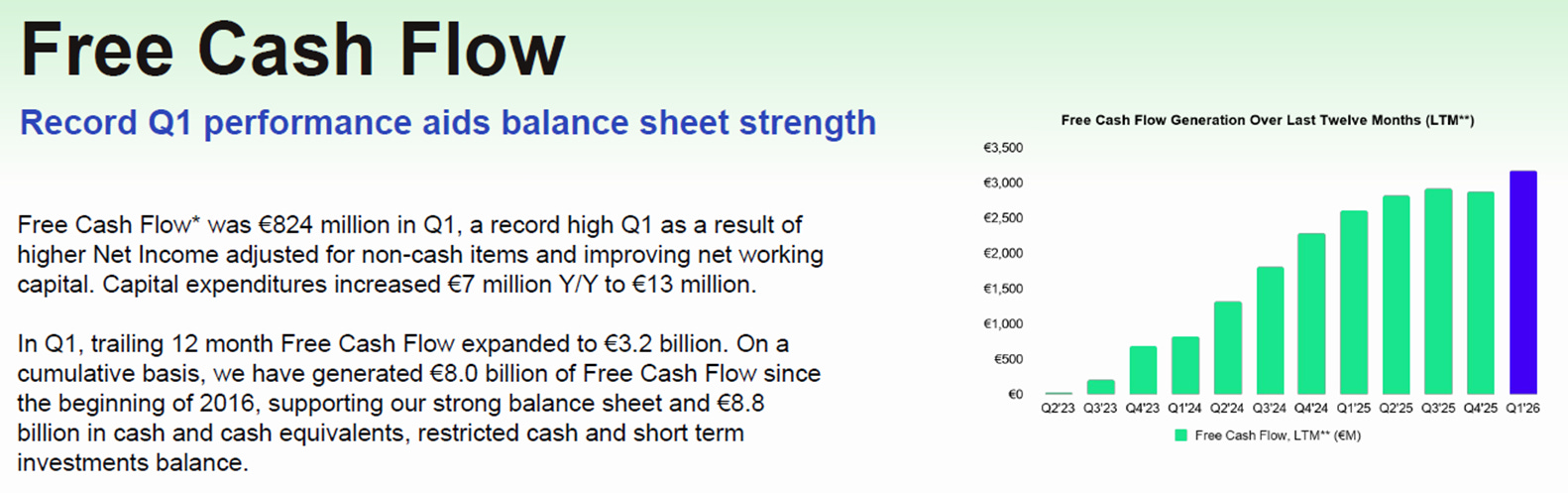

Spotify Has Strong Free Cash Flow. If there is one metric that bulls love, it is free cash flow, and Spotify is generating it at a staggering clip. Spotify delivered €824 million in FCF just in Q1. This brings their trailing twelve-month (LTM) Free Cash Flow to an impressive €3.2 billion. When a company is printing over €3 billion in cash a year, bulls will argue that management has immense optionality for share repurchases, which can artificially support the stock price and boost EPS even if top-line growth slows.

SPOT Beat Operating Income & Profitability Guidance. Despite the “Empty Calorie” MAU growth problem we discussed, management is executing ruthlessly on cost discipline. Operating Income came in at €715 million, beating their guidance of €660 million. Gross Margin also beat expectations, finishing at 33.0% against a forecast of 32.8%. This reflected a 133 basis point expansion year-over-year. Bulls will point out that even if revenue growth is decelerating, Spotify is proving it can expand its profitability profile. (I would still argue this is not enough.)

Q1-26 MAUs Actually Beat Expectations. While the composition of the user growth leans heavily ad-supported, the absolute top-of-funnel volume is still expanding faster than management initially projected. Spotify added 10 million MAUs in Q1, bringing the total to 761 million, which surpassed their guidance of 759M. This outperformance, while small, was driven by the Rest of World and North America.

Early AI Engagement appears to be Extremely Sticky. Spotify is aggressively trying to build an engagement moat using AI, and the early data is highly compelling. Management noted that their AI DJ is closing in on 100M users. A newly released feature called “Song DNA” hit 52 million users in just 4 weeks. Co-CEO Alex Norström argued that these features drive user engagement (days per month), which acts as a leading indicator for retention and long-term lifetime value (LTV).

However, these points mask deeper structural issues and a Total Addressable Market (TAM) that is much smaller than investors realize. Looking at record Q1 free cash flow gives investors false confidence; strong historical performance does not promise future returns. The market is calculating the NPV of future cash flows, and everything we’ve discussed indicates FCF growth is not going to accelerate without structural changes. Simply put, it is hard to see a path for Spotify to grow as a healthy business if ad-supported gross margins remain less than HALF the premium gross margin of 34.8%.

IV. Royalty Ceiling Makes the 33x Multiple a Value Trap

The market is waking up to the inherent limitations of the audio-first business model, especially when compared to video streaming or diversified big-tech platforms.

A simple reason many investors overlook is that audio-first services can never monetize like video because companies like Spotify are paying almost 70% of gross dollars to the record labels. Notice how Spotify’s gross margins are in the low 30%s. This creates a structural, permanent ceiling on how high their gross margins can realistically go.

At current prices in the $430s, Spotify is trading at a premium undeserved for the business they are today, and more suited for a business they will never become. When a company lacks diverse monetization levers and its primary lever (subscription pricing) shows signs of exhaustion, the market will ruthlessly compress its earnings multiple. Investors are simply refusing to pay a premium valuation for a business model with capped profitability.

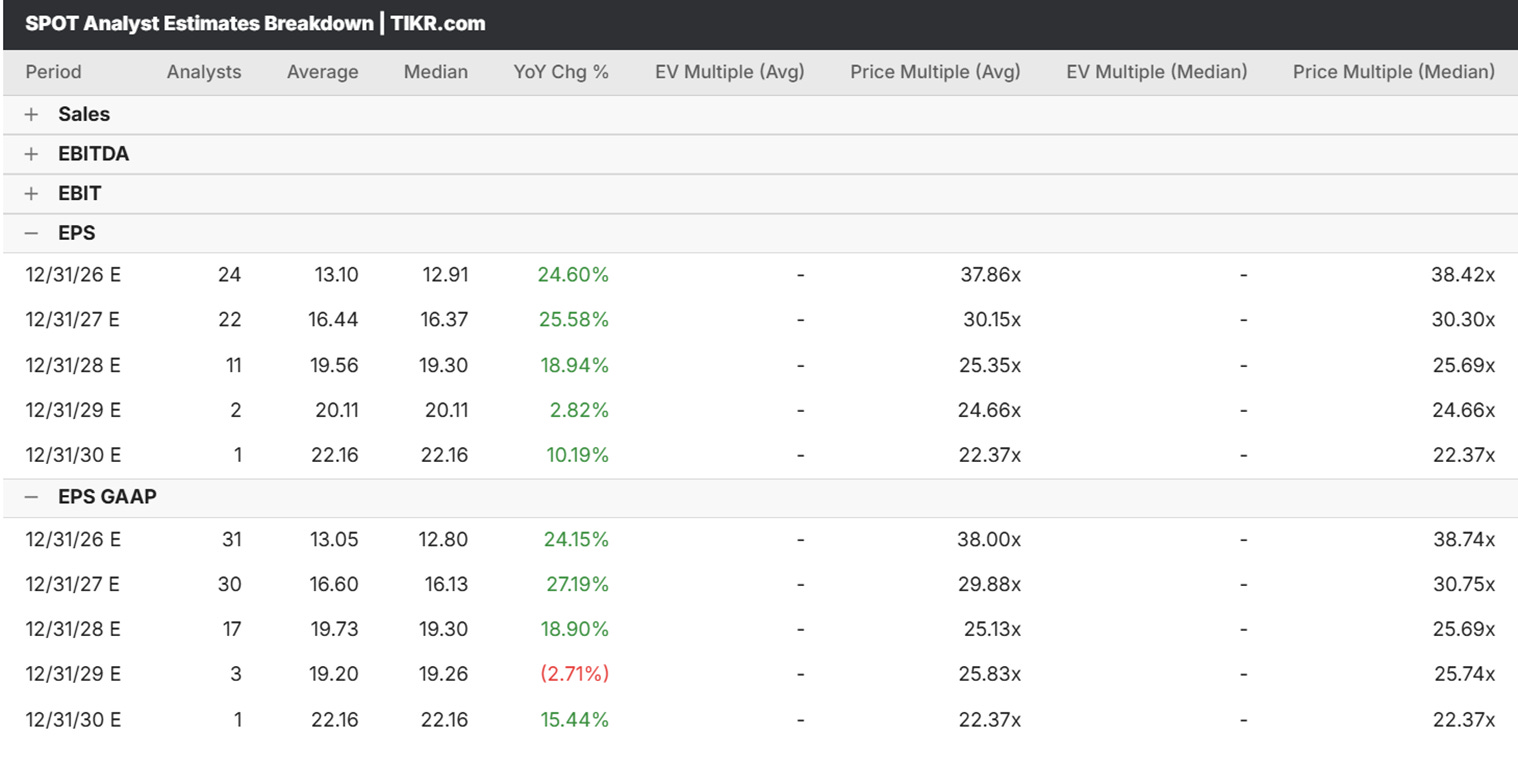

The current consensus 2026 and 2027 GAAP EPS (pre-earnings) were at roughly $13 and $16, meaning the stock is trading at P/E multiples of 33x and 27x, respectively. This is too high on an absolute basis given the future free cash flow trajectory, and it is definitely too expensive when you compare it to true digital juggernauts like Meta and Google, which are somehow trading at cheaper multiples while actually owning their underlying infrastructure and networks.

CONCLUSION

An overarching observation I have with Spotify is that because they are the undisputed #1 publicly traded audio company, I think some investors have unrealistic thoughts on their potential TAM (total addressable market). At this premium multiple, I rate Spotify stock an Underperform.

I fully expect it to lag the S&P 500 over the coming year. More importantly, I expect Spotify’s media competitors to significantly outperform them in stock price—namely YouTube (Google), Netflix, and Meta, which remains a massive leader in all things digital advertising. These platforms do not have to hand over 70% of their revenue to legacy record labels just to keep the lights on. They dictate the terms, control the inventory, and possess the pricing power that Spotify lacks.

Until Spotify can prove that its ad-supported tier is a viable, high-margin business rather than a loss-leader, the 13% drop we saw this week is just the beginning of a long, painful multiple compression. Avoid the stock.

SPOT 0.00%↑, GOOGL 0.00%↑, GOOG 0.00%↑, META 0.00%↑, SIRI 0.00%↑

-Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.

Great piece Simeon - genuinely useful bear case. Just some thoughts if I take the "bull case":

1. Royalty ceiling at 70% — but that's on a shrinking share of rev. Bundled ARPU, podcasts, audiobooks all bypass label splits (100% of rev in 2018 → ~93% in 2025). Q1 GPM at 33% (2nd highest ever) suggests the ceiling is lifting, no?

2. "Empty calorie" MAUs — the free-to-paid conversion ratio has been ~38-40% for years and was 38.5% this Q. What evidence is there it's actually deteriorating vs just being the same funnel it's always been (ie to convert to prem subs eventually)?

3. FCF "sugar high" — what breaks the structural conversion do you think though? Prepaid subs + royalty settlement lag + <0.1% capex intensity is a DSP model feature, not a cyclical anomaly.

4. 33x P/E vs META — is that really the right comp? On P/FCF (which captures SPOT's conversion advantage), post-selloff valuation looks quite different.

The ad-supported weakness you flagged is definitely the part I found hardest to pushback on. Appreciate any thoughts!