The Mispriced Victor: Why I’m Reaffirming My $120 Netflix Target

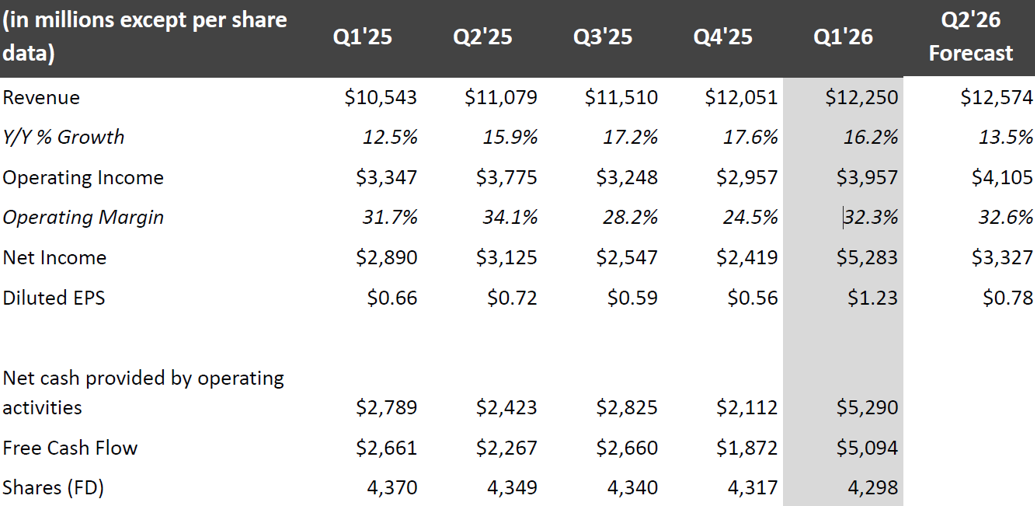

Q1 revenue grew 16.2% despite a quiet content slate and Olympic headwinds. This isn't a slowdown; it’s a masterclass in pricing power.

Accrued Interest TLDR: Netflix’s post-earnings -10% dip is a shortsighted mistake. While the Street panicked over “light” guidance, the fundamentals reveal strong pricing power: +16.2% YoY revenue growth achieved without a single tentpole release and despite wall-to-wall Winter Olympic competition. With 60% of sign-ups hitting the ad tier and an industry-low $0.48 cost-per-hour viewed, Netflix is effectively scaling the “unscalable.” From daytime share grabs via podcasts to programmatic ad growth, the undisputed victor of the streaming wars is just getting started. Subscribe to read my full Q1 2026 earnings breakdown.

Introduction

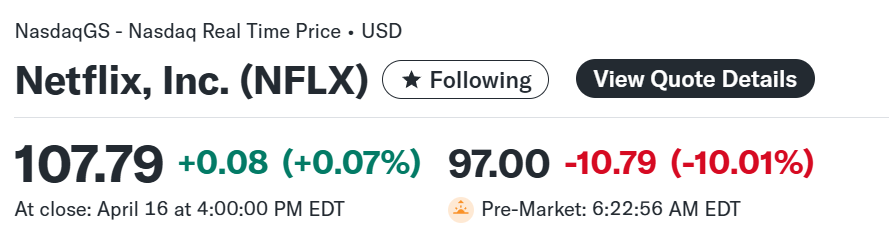

Look, the market hated Netflix’s Q1 earnings, sending the stock down 10% after hours. Investors are spooked by soft guidance and Reed Hastings stepping down, but I think they’re missing the forest for the trees. This dip feels like a classic short-term overreaction to a company that is still fundamentally miles ahead of all its competitors, except for YouTube.

The monetization engine is humming. Revenue hit $12.25 billion, up 16.2% year-over-year (14% on a FX-neutral basis), with a fat 32.3% operating margin. That’s solid. I’m staying positive here—Netflix still has plenty of room to run.

The Post-Earnings Selloff Misses Netflix’s Underlying Resilience

The post-earnings selloff was primarily driven by two bearish talking points. First, Q2 revenue growth guidance of +13.5% YoY came in slightly weaker than what some investors were expecting. Second, the announcement that founder and board member Reed Hastings is stepping down gave others an excuse to hit the sell button.

What this selloff overlooks is Netflix’s impressive growth despite significant headwinds. Achieving a 16.2% revenue increase during a relatively light content cycle is a testament to its scale. NFLX maintained stable engagement per household even while competing against major global events like the Winter Olympics. A platform that can drive mid-teens growth during quieter periods demonstrates a level of pricing power that provides a substantial buffer against broader industry shifts.

The Ad Tier Strategy is Working

While some may look for higher growth rates, Netflix’s projected 12% to 14% full-year 2026 revenue growth remains healthy. Management appears to be using pricing strategically to maintain low churn across premium tiers. Currently, the priority seems to be growing engagement within the advertising tier to diversify revenue streams.

A key indicator is that Netflix said over 60% of new sign-ups in available markets are opting for the ad tier. Priced at $8.99 in the United States, this provides an accessible entry point. While this may impact short-term average revenue per user (ARPU), it helps build a larger user base for future monetization. Management indicates that ad revenue is expected to grow significantly, reaching approximately $3 billion by 2026.

Netflix’s Inherent Advertising Technology Advantage

Netflix said on the earnings call that it increased its advertiser base by 70% year-over-year, now partnering with over 4,000 advertisers. This represents a growing footprint in the digital advertising market with potential for further scaling.

By moving to sell 50% of its non-live ad inventory programmatically, Netflix is seeking greater efficiency and scalability. This technological approach to ad sales contributes to the company’s competitive operating margins compared to traditional media networks dealing with legacy structures. This is another thing I think investors miss when they only think of a spreadsheet. If you think about all the people needed to operate a global Ad sales business, it will be inherently more expensive, and less scalable than what Netflix is currently building.

Video podcasts represent a calculated daytime share grab

Skeptics might view the platform’s push into video podcasts as a distraction from prestige television, but it is a highly calculated, smart maneuver. The strategy targets daytime viewing hours—a daypart where Netflix has historically underindexed. This is a key way to take share from traditional television, especially as U.S. broadcast networks continually pull back budgets and abandon the daytime talk show format.

Just look at the graveyard of syndicated daytime hits lately: Access Hollywood, canceled after 30 years, The Steve Wilkos Show, wrapped its final 19-season run, The Kelly Clarkson Show, ending its run later this year, among others.

During the earnings call, management emphasized that podcasts are naturally driving increased engagement on mobile devices. With Netflix currently holding only a 5% share of global TV viewing and reaching less than 45% of its 800 million addressable broadband households, video podcasts serve as a strategic tool to widen its moat and capture a larger slice of the total addressable market.

A highly targeted sports strategy is proving to be efficient

Netflix’s live sports strategy is proving to be highly efficient and regionally targeted. Management highlighted how the World Baseball Classic in Japan helped drive substantial viewing hours, proving the company can successfully execute large regional events outside the United States. Co-CEO Ted Sarandos specifically noted this event, stating that the company is “adding more regional live sports events, like the incredible event we just did in Japan with the World Baseball Classic“.

Further validating this model, earlier this week it was reported that Netflix secured the rights to the CONCACAF soccer tournament for Mexico. Momentum is also building for their coverage of the 2027 Women’s World Cup, which serves as another prime example of this highly efficient, targeted sports model in action.

The anchor service boasts the ultimate value proposition in streaming

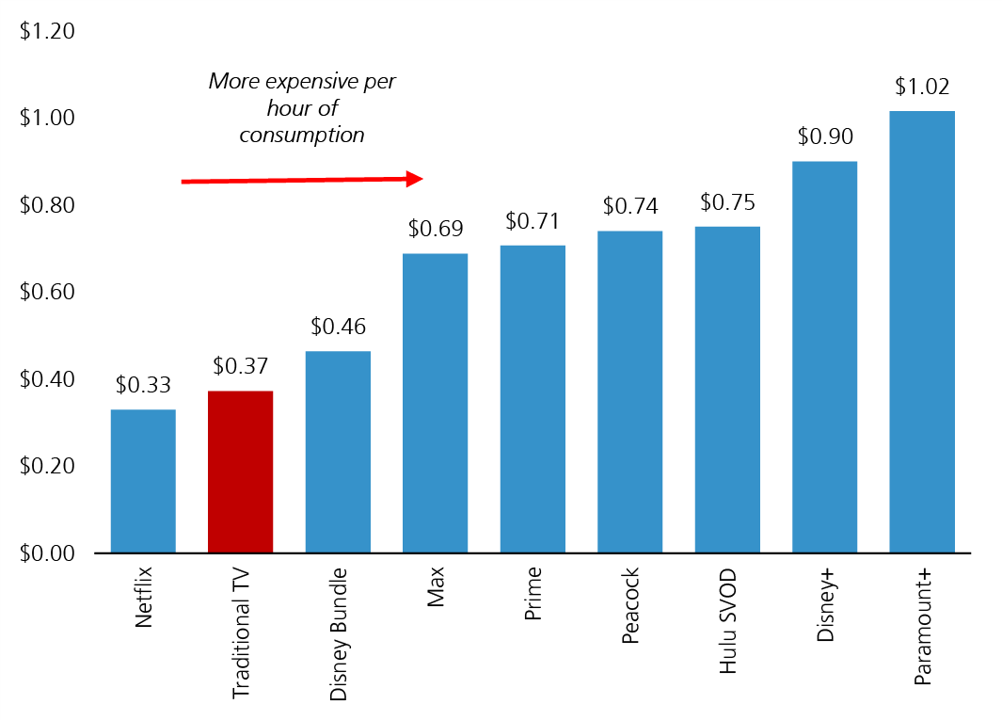

On the call, NFLX drove home a point that I think too many investors overlook - Netflix is the only global streaming service with a value proposition. When you rank the streaming landscape on a cost-per-hour-watched basis, Netflix remains the cheapest major service on the market.

Co-CEO Greg Peters on pricing advantage: “In the U.S. right now, Netflix subscribers are paying the least per hour of viewing compared to other SVOD offerings. So in some cases, you’d have to pay 2x per hour to get a competitive service.”

Management is not exaggerating here - outside estimates from different analysts have also been pointing out Netflix’s quiet cost advantage. As reported by Variety - According to MoffettNathanson’s estimates, Netflix delivers the best bang for the buck in the cohort, pulling in just $0.48 per hour viewed. This is significantly lower than Disney (Disney+ and Hulu), Peacock, HBO Max, or Paramount+, which range from $0.64 to $0.93 per hour viewed.

Even with recent and upcoming price increases, Netflix will maintain a sector-low metric in the roughly $0.50-per-hour range. MoffettNathanson estimated that “Netflix delivers significant value to its subscribers that has room to be better monetized over time.”

Now while I do not have a copy of the MoffettNathanson report from 2026, I was able to find a similar analysis done by UBS from last year that came to the same conclusions. Back in Jan 2025, Business Insider covered this same concept in their article - “Netflix is raising prices again. These charts show why.” For context - back in early 2025 NFLX raised the U.S. price of a standard plan to $18 a month, up from $15.50, and its ad-supported plan to $8 from $7. The article cited a note from the UBS media analyst John Hodulik which also said Netflix was “by far the cheapest service on a per-hour-of-consumption basis,”

UBS Jan 2025 Estimates - Cost Per Hour Watched (Ad-Free Plans)

Jan 2025: “Before Tuesday’s increase, customers on Netflix’s ad-free plan paid an average of $0.33 a month per hour they watched, a UBS analysis of Nielsen and company data found. That suggests the average customer is watching the service for a staggering 47 to 70 hours a month. That’s cheaper on a per-hour basis than Netflix’s major streaming rivals and traditional TV, UBS found.”

This unbeatable value proposition ensures Netflix will remain the “anchor streaming service”—the default utility people keep while selectively churning through the rest of the pack.

Q1 was a highly solid quarter that demonstrated consistent execution.

Netflix is showing tangible signs of an improving monetization engine that continues to expand its economic moat into new dayparts and targeted live events. The broader industry narrative is playing out exactly as predicted. Each year, it becomes increasingly clear that the streaming landscape is a two-horse race between YouTube and Netflix, and then everyone else.

I’m staying bullish, but I understand why the stock took a pause after a strong run up to $108 per share. It is going to take time for Netflix’s ad engine to get fully ramped up, but as value investors, we should focus on the fundamentals, which are simply too strong to ignore. Forget the short-term noise—Netflix’s profitability and market share make it the clear long-term winner. I’m maintaining my $120 price target, which represents approximately 30x 2027 GAAP EPS of $4 per share.

NFLX 0.00%↑ GOOG 0.00%↑ GOOG 0.00%↑ PSKY 0.00%↑ DIS 0.00%↑

-Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.

Is nflx starting to get priced more and more like legacy media as it starts to get closer to ex growth? And the multiple is starting to reflect that?