Paramount Skydance Q3-25 Review

Buzzwords & UFC Hopes Mask a Decade-Old Strategy

On November 10th, Paramount Skydance ($PSKY) reported their Q3-25 earnings, their first full quarter under new management. This article is my breakdown of their shareholder letter and the earnings call.

TLDR - David Ellison is a CEO who is 10 years too young, with a strategy that is 10 years too late to save Paramount shareholders from subpar returns, unless they can win WBD. However, there is reason to worry that winning the current crown jewel in media will still not be enough for $PSKY to outperform the S&P500 in 2026.

For background - I recommend you see my September article Same Script, Different Cast, where I compared $WBD and $PSKY with Disney going after Fox’s film and television assets back in 2017.

Now here are my highlights from the Q3-25 shareholder letter and conference call.

Q3-25 SHAREHOLDER LETTER – 5 KEY TAKEAWAYS

1)Management leans on buzzwords to spin an old-strategy as new

As I have shared before - when I worked in Corporate Finance roles inside media companies for a decade, I used to write investor decks and earning scripts for CEOs. I am familiar with standard business communication. However, I was quite struck by how much the shareholder letter’s tone resembled something generated by an AI agent trained on McKinsey consulting material. The Q3-25 shareholder letter is filled with buzzwords like “North Star”, “Creative Engines”, “100 Day Plan”.

Let us drop the MBA-speak. The focus needs to be a clear articulation of the strategy to not only reverse the current audience declines but to achieve long-term, sustainable growth.

Just as a side note, Ellison mentioned “North Star” eight times during the call. Maybe we should turn it into a drinking game for the Q4 earnings call!

2)UFC is their plan to keep you subscribed all year

PSKY’s push for more “year-round programming” hinges on sports, specifically leveraging events like UFC fights, which occur throughout the year. However, this strategy raises a question regarding its alignment with the goal of achieving direct-to-consumer (DTC) profitability by 2026 (pro forma). While there may be opportunities to adjust sports-related costs to support this profitability target, the increased focus on sports will make it hard to outperform their profit margin targets.

3)Price hikes are coming for Paramount+ to pay for UFC

$PSKY previously highlighted that the Paramount+ subscription is undervalued compared to the former price of a UFC PPV event. Shareholders should be pleased that the company plans to raise prices to recapture some of this potential margin.

Raising prices for DTC subscribers is a risky move if the majority are primarily seeking general entertainment. While sports subscribers might tolerate increased costs, the willingness of other subscribers to pay more is questionable, particularly given the availability of competitors like YouTube and other media options.

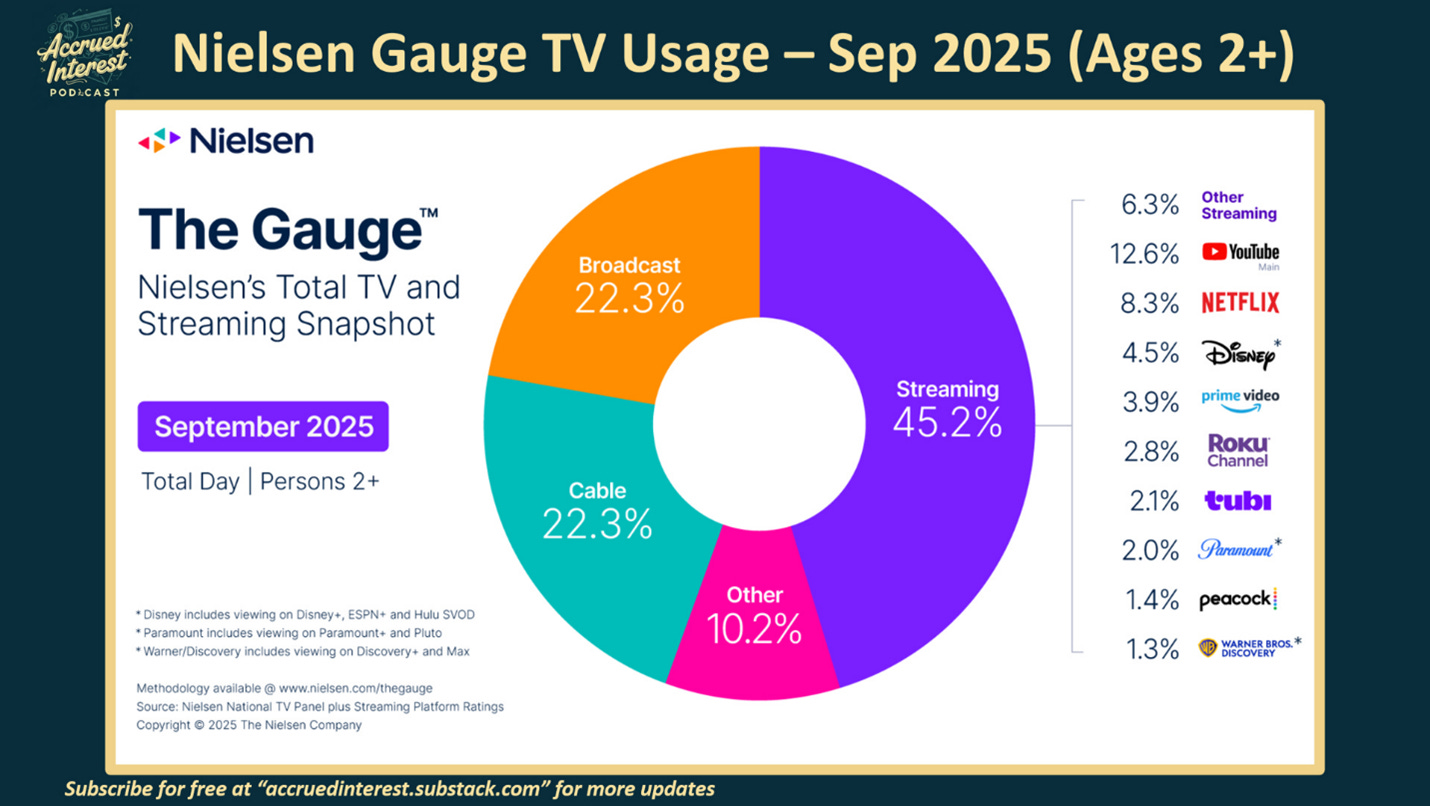

As I have said many times on Accrued Interest – the biggest threat to legacy media players like Paramount is YouTube FIRST, then followed by Netflix.

To provide some context, as I write this, the ongoing carriage dispute between YouTube TV and Disney reportedly centers on ABC’s affiliate fees, not the cost of ESPN, according to sources privy to post-negotiation details. This move by YouTube TV to take a hard line against a broadcast network on affiliate fees could be an early warning sign of broader challenges for the industry in 2026 and 2027.

4)Both linear advertising and affiliate revenue are still in decline

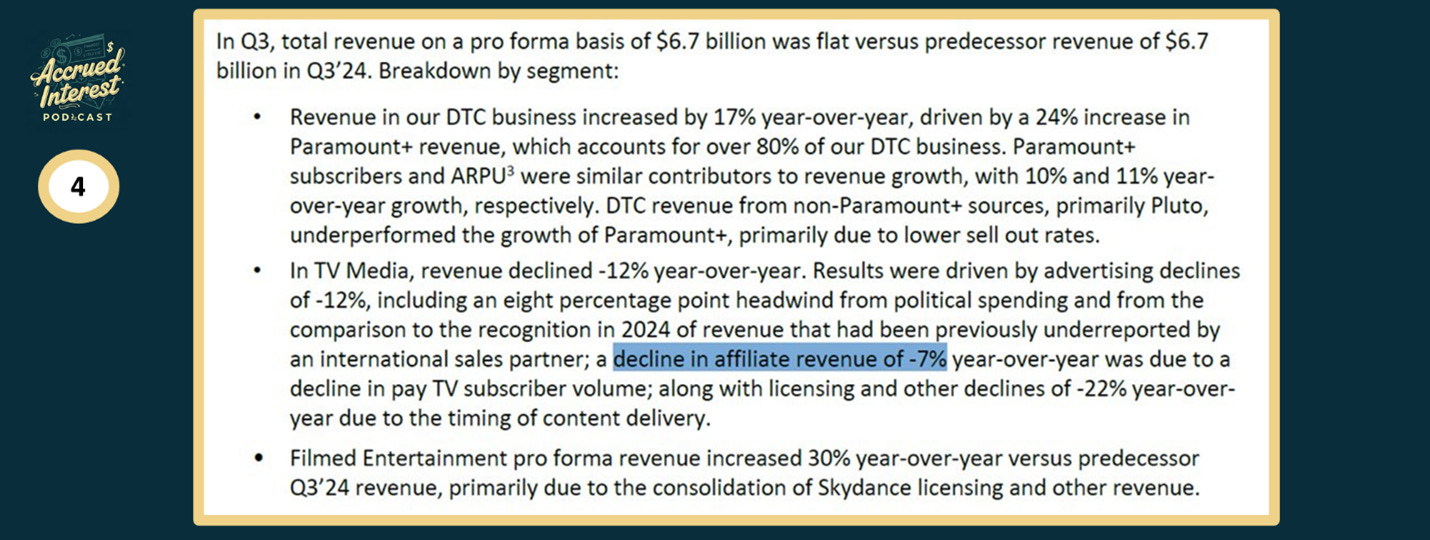

Shifting back to Paramount’s figures, management is touting DTC growth up +17% YoY. However, the -12% drop in TV media revenue is concerning, particularly the -7% decline in affiliate revenue, which management attributes to “decline in pay TV subscriber volume” (i.e., customers cutting the cord).

The structural problem is clear: Direct-to-Consumer (DTC) revenue will never monetize as effectively as a traditional cable bundle subscription, leading to structurally lower margins. Therefore, investing in this company requires a lot of HOPE.

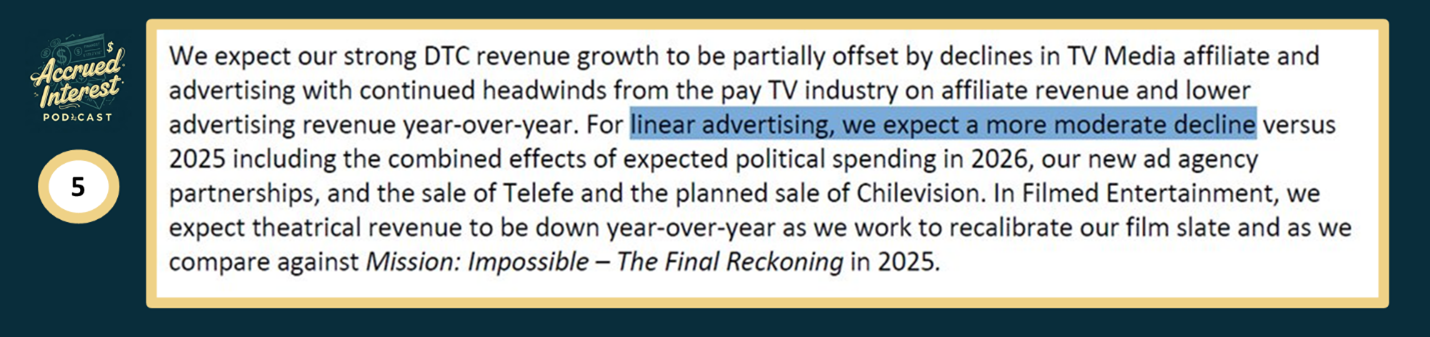

5)You need HOPE to believe that linear declines will moderate in 2026

Here is the key $PSKY assumption bulls need to come true. “For linear advertising, we expect a more moderate decline versus 2025”.

I am bearish on going long on Paramount, as I do not believe the decline in linear TV will moderate. Even optimistically, the company is only guiding to an adjusted OIBDA margin of under 12%. Efficiency is demonstrated by a company’s financial figures, not by management’s statements. To me, a sub-12% adjusted margin goal is not a compelling sign of efficiency. Ultimately, Paramount remains a “show me story” for both bulls and bears.

Now let me share my highlights from the Q3-25 conference call.

Q3-25 EARNINGS CALL – 4 KEY TAKEAWAYS

1)UFC is going to be the biggest content driver for the company.

Going all-in on UFC is by far the biggest decision New Management has made since taking over. While Management highlighted the substantial US fanbase of 100 million, my concern is whether enough of those fans will convert to Paramount+ subscribers to warrant the considerable expense of the sports programming.

Do not assume the 25% audience growth since 2019 (as per Ellison) means the sport’s expansion will continue indefinitely. While the rise of the “manosphere” likely fueled much of the UFC’s interest over the past decade, the question remains: how much more growth is realistically possible?

UFC can become a valuable asset IF it can significantly reduce subscription churn for Paramount+. Specifically, it helps retain subscribers who might otherwise cancel their service once the NFL season concludes.

2)Strategy seems to rely too much on CBS broadcast network

The constant focus on CBS during the Q&A seems based on a decade-old strategy. In 2015, using CBS as a foundational “anchor” would have been a sound approach. However, it is now 2025, and neither Comcast (with NBC) nor Disney (with ABC) has successfully managed to leverage its broadcast network as the core of its broader media operation.

3)Technology DOES NOT MATTER for Paramount

The CEO excessively focused on technology in both the shareholder letter and the Q&A—perhaps the prepared remarks were AI-generated?

While integrating the tech infrastructure for three distinct streaming services (Paramount+, Pluto, and BET+) is no simple task, this technical consolidation alone will not attract new subscribers.

4)Everything about PSKY comes down to WBD

Companies are legally barred from publicly discussing a potential Warner Bros. Discovery (WBD) acquisition while negotiations are ongoing. However, talk from PSKY that “there are no must-haves” is not serious.

The reality is that Paramount’s position in the global entertainment landscape is precarious without securing at least SOME of the WBD assets.

CONCLUSION

I said many times in my writing that M&A is not a strategy. Until the fate of WBD’s assets is settled, I cannot recommend going long Paramount stock. I am not trying to trade for a small M&A pop - I really struggle to imagine what this company’s financials will look like 2 years from now.

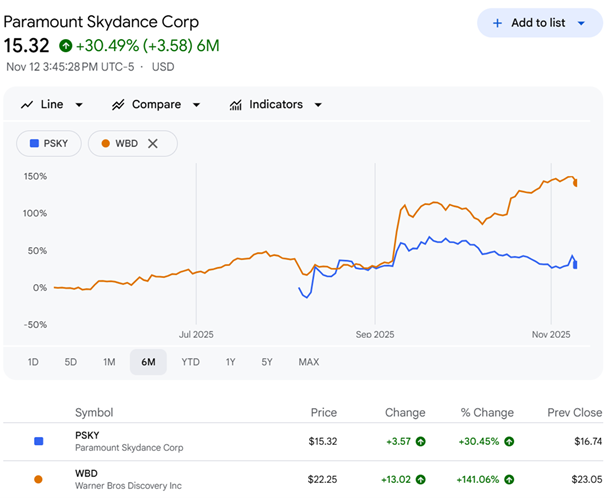

The current trading price for WBD shares is in a holding pattern, reflecting investors’ speculation regarding the eventual acquisition price.

PSKY stock price is much more volatile because we are figuring out in real time what revenue base is for this new company.

I want to be clear: I do not believe David Ellison will be a poor CEO for PSKY.

In fact, my expectation is that PSKY will ultimately secure control of the Warner Bros. Discovery assets. My core argument is this: In the entertainment sector, the CEO is ultimately secondary because the audience, through their viewing habits and spending, is the final arbiter of which content is superior.

No rating on Paramount Skydance stock. Check back for my deep dive on WBD!

-Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.

Brilliant. Your take on the "AI generated" buzzword soup in the shareholder letter is sooo spot on, total deja-vu! You mentioned winning WBD might still not be enough for PSKY. What's the main obstacle you see there, beyond just the acquisition itself?