Monetizing the Habit: Meta's Enterprise Land Grab and Roku's Living-Room Billboard (Accrued Interest Update 5-28-26)

$META, $ROKU

Accrued Interest TLDR: Today I am looking at two tech/media giants that are fundamentally changing how they monetize deeply ingrained consumer habits. Meta is rolling out paid subscriptions across Facebook, Instagram, and WhatsApp while standing up a dedicated enterprise org to embed its AI inside large corporate customers — exactly the “Other Revenue” diversification I argued for in my $1,116 deep dive. Meanwhile, Roku is overhauling its homescreen for the first time in over a decade to open up premium ad inventory at the single most valuable point of entry in streaming. One quick housekeeping note up top: I am formally dropping coverage of Fubo and reallocating that bandwidth to Roku, a pure-play CTV distributor.

Please subscribe to read the rest of the Accrued Interest Daily Update for May 28.

A Quick Housekeeping Note: Goodbye Fubo, Hello Roku

Before we get into today’s news, a formal change to the Accrued Interest coverage universe. I am officially dropping coverage of Fubo TV. The fundamental risks are simply too high, and the platform remains sub-scale in a market that increasingly demands massive reach to matter. I previewed this back in my April 16 update, and today I am making it official.

In its place, I am expanding coverage of Roku ($ROKU) — the premier pure-play connected-TV distributor and, in my view, the toll booth at the entrance to the streaming ecosystem. Section B below is the start of that deeper commitment. As always, if there are other publicly traded TMT names you want me to dig into, drop them in the comments!

A) Meta Is Finally Building Its Second Revenue Engine

Meta is moving aggressively beyond its traditional ad-supported model on two fronts at once.

First, on the consumer and creator side, the Wall Street Journal reported that Meta has begun rolling out paid subscription tiers across its core apps to help recoup the cost of its enormous AI buildout. Rather than burying these inside a dense paragraph, let’s lay out exactly what this new monetization matrix looks like:

Facebook & Instagram Plus: $3.99 / month

WhatsApp Plus: $2.99 / month

Meta AI Basic: $7.99 / month

Meta AI Premium: $19.99 / month (unlocking higher structural limits on Thinking Mode, long-form video, and high-fidelity image generation)

Crucially, Meta’s product chief Naomi Gleit framed these plans as including not just consumer features but “premium tools for businesses and creators.” Notably, after the announcement the stock closed up 3.7% — a tidy contrast to the more than 5% after-hours drop the company took last month when it told investors it would spend even more on AI.

Second, and more important to my thesis, The Information reported that Meta is standing up a new internal organization called Enterprise Solutions — staffing product managers, data engineers, and software engineers to embed directly inside large corporate customers and integrate Meta’s AI tools into the legacy systems those companies actually run their operations on. This is the classic “forward-deployed engineer” playbook, the same high-touch model Google, OpenAI, Nvidia, and Anthropic are all racing to build out. Gleit’s internal memo explicitly cites the goal of building “repeatable playbooks and tooling along the way so the work can scale over time.”

For context on the starting line: last quarter Meta reported just $885 million in non-advertising “other revenue” against roughly $55 billion in ad revenue, and last year a stunning 98% of total revenue came from advertising. This is a company taking its very first real steps off a one-legged stool.

The Accrued Interest Take: Set Aside the Noise

Let me start where I always do with Meta: separate your personal feelings from your investment thesis. People love to air their political grievances and personal outrage about social media companies, and about Mark Zuckerberg specifically. That is fine for cocktail parties. It is useless for portfolio construction. The brutal, repeatable truth is that consumer habits persist regardless of what people say — they keep using the platforms, no matter how loudly they complain. Underwrite the behavior, not the discourse.

Meta is not a “social media company.” It is critical infrastructure for small and medium businesses worldwide. If you run an SMB in 2026, Meta is simultaneously your global storefront, your targeted marketing agency, and — increasingly — your automated customer service rep and ad-creative studio. That is not a novelty. That is a utility you cannot turn off without losing customers.

And this is the part the bears keep missing: Meta’s AI is not a chatbot for making funny images. It is a super-computer in your pocket that solves real logistical and conversion problems for businesses. It supercharges the advertising tools that already dominate the market, delivering a positive, measurable ROI on Meta’s gargantuan AI capex today, not in some hand-wavy 2030 terminal-value fantasy. The Enterprise Solutions org is simply Meta putting engineers in the room to make sure that ROI shows up on the customer’s P&L — and, in turn, on Meta’s.

The $20 Billion Bridge. As I outlined in my deep dive, Back to the EBITDA: Decoding Meta’s $1,116 Executive Playbook, management’s incentive structures require massive, sustained growth to clear the $1,100+ stock-price hurdles where executives actually get paid. In that piece I specifically flagged “The $20 Billion ‘Other Revenue’ Bridge” as the critical alternative revenue stream Meta would need to hit those targets — scaling a roughly $3 billion “Family of Apps – Other Revenue” line toward $15–$20 billion, built on buckets like a WhatsApp Business communication toll-bridge, AI-agent SaaS, and in-thread commerce.

These Announcements Are That Bridge Under Construction. These new enterprise AI subscriptions and the Enterprise Solutions org are exactly how Meta builds that bridge. Every dollar of recurring software revenue diversifies the income statement and makes Meta a more economically durable machine — one that is no longer 100% hostage to ad pricing. Stack that on top of the strong ad-impression growth I expect to continue compounding through 2026, and you have a top line being attacked from two directions at once.

Valuation & Rating: Meta ($META)

Meta currently trades around $637 per share. On forward earnings, that is just ~18x 2027 consensus GAAP EPS of roughly $35, and an almost comically cheap ~16x 2028 consensus GAAP EPS of roughly $40 (estimates via TIKR).

Let me be blunt: these multiples are far too cheap. A business with this level of free cash flow, this much operating leverage, and genuine utility status for millions of advertisers should not be trading below the broader market multiple. The market is still pricing Meta like a cyclical ad name with a capex problem. I am pricing it like an indispensable utility that is quietly bolting a recurring-revenue engine onto the side of the best ad machine on the planet.

Accrued Interest Rating: I continue to expect Meta to outperform vs. the S&P 500.

Relevant Accrued Interest articles on META:

2026.04.30: The Street Missed the Q1 Signal: Why Meta’s AI Engine is Worth Every Penny

2026.04.21: AI Tracking Employee Keystrokes Validates Meta Bull Case

2026.03.27: Back to the EBITDA: Decoding Meta’s $1,116 Executive Playbook

2026.03.25: Zuckerberg’s Middle-Age Metabolism: Trimming Fat to Fund Superintelligence

2026.02.10: Meta Q4 2025 Recap

B) Roku Is Rebuilding the Front Door of the Living Room

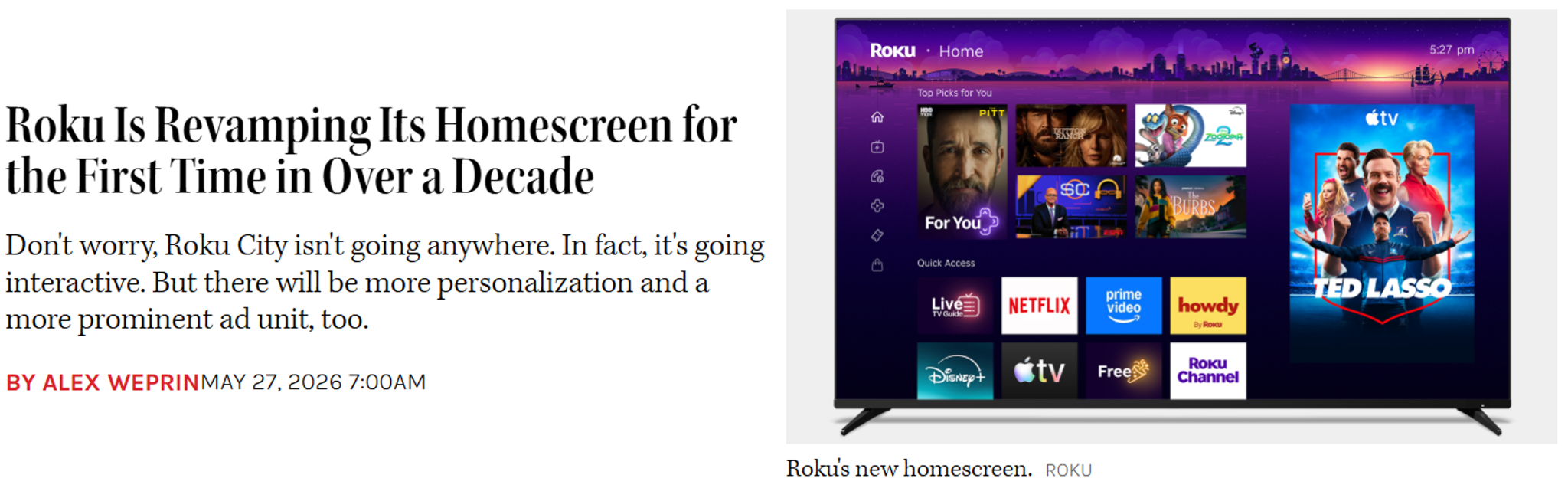

Roku is overhauling its homescreen — the iconic app grid — for the first time in over a decade.

The Hollywood Reporter detailed the user-experience side: the static grid is becoming a dynamic, personalized, content-forward discovery hub. Your most-used apps get featured more prominently, a “Top Picks for You” section surfaces recommended apps and programming, and — the key commercial detail — a large “marquee” ad spot now sits front and center to promote apps or shows. Roku City survives (and goes interactive), there are new genre-based destinations, and the homescreen will even adapt by household, showing a different layout on the kids’ playroom TV than on the adult bedroom set. Founder and CEO Anthony Wood said the redesign “puts entertainment at the center of everything.”

Bloomberg covered the financial mechanics behind the redesign: a new AI-powered, personalized homescreen that learns user habits, shifts throughout the day based on who is watching, and — critically — “opens up more ad opportunities.” VP of viewer product Preston Smalley was careful to stress that Roku won’t get aggressive to the point of alienating users: “we’ll never shove it in people’s faces.” That balance matters, because advertising is already the engine here — of Roku’s $4.74 billion in total 2025 revenue, $4.15 billion came from its high-margin platform segment.

The Accrued Interest Take: The Power of Habit

Here is why this matters more than a typical UI refresh: Roku has become the ingrained, habitual “first destination” for the modern television viewer. Turning on a Roku TV in 2026 is the behavioral equivalent of flipping on the cable box in 2006. It is muscle memory. And Roku shares that elite, default-destination status with only a tiny handful of names — essentially Netflix and YouTube. When you control the very first screen a hundred million households see every night, you control the most valuable real estate in the living room.

The 100 Million Milestone. As I wrote in the April 16 Accrued Interest update, Google Drops the Halo, Ad-Tech Desperation at OpenAI, and Roku’s 100 Million Milestone, crossing the 100-million active-household threshold proved Roku is a major, undeniable player in digital video — a proxy for close to full distribution in North America. To quote that piece directly:

“Hitting this milestone tells marketers that the Roku platform can reach almost every single home. This critical scale opens Roku up to more brand-focused advertisers who previously relied on legacy linear television to reach a nationwide audience.”

Unlocking the Prime Real Estate. The homescreen is Roku’s single greatest promotional asset, and frankly it has been under-monetized for years. Historically, Roku has leaned heavily on distribution revenue — taking a recurring cut or bounty on SVOD sign-ups routed through its billing system.

This redesign represents an aggressive tactical shift. By turning the home screen into a dynamic billboard, Roku is directly pursuing high-margin top-of-the-funnel brand advertising revenue captured right at the point of entry, before the viewer has even clicked open an app. This is Roku’s most valuable impression in the connected TV ecosystem. It allows Roku to step directly into the legacy-TV upfront infrastructure and intercept brand dollars before they dissolve into individual content libraries. It is the necessary next step to fully monetize the massive distribution scale they have already won.

Tie that back to the financials: the entire bull case for the stock rests on driving higher average revenue per user (ARPU) against that ~$4.15 billion platform-revenue base. A premium, brand-friendly marquee unit on the homescreen — sold to exactly the legacy-TV advertisers who now need Roku to reach a national audience — is the most direct ARPU lever the company has.

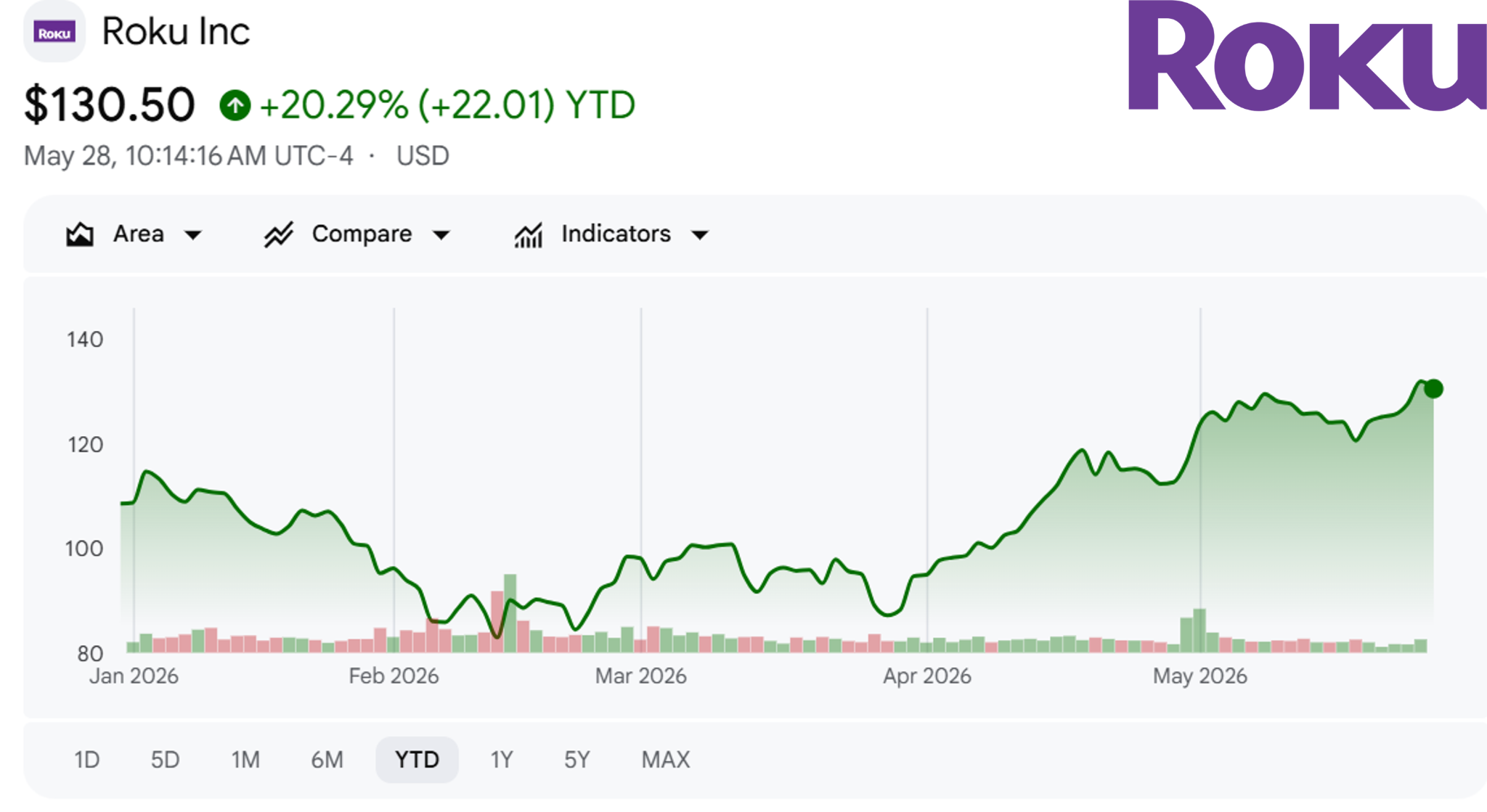

Valuation & Rating: Roku ($ROKU)

Roku currently trades around $130 per share. That works out to roughly 37x 2027 GAAP EPS of about $3.50, and ~25x 2028 GAAP EPS of about $5.20.

I will be honest: this is not optically cheap. But I read it as growth at a reasonable price (GARP) for a company that has cemented itself as a major, toll-collecting gatekeeper in the new digital distribution regime. The scarcity value of being one of only a few true “first destinations” in the living room deserves a premium — I just don’t think today’s price leaves enough margin of safety to be banging the table. As the homescreen redesign actually shows up in ARPU over the next several quarters, the multiple becomes a lot easier to defend.

Official Rating: Market Perform, ROKU 0.00%↑

Relevant Accrued Interest articles on ROKU:

2026.04.16: Google Drops the Halo, Ad-Tech Desperation at OpenAI, and Roku’s 100 Million Milestone

CONCLUSION

Two different companies, one identical strategy: find a habit consumers already can’t quit, then build a new, higher-margin meter on top of it. Meta owns the habit of how the world’s businesses reach customers, and it is bolting a recurring software-and-subscription layer onto an ad engine the market still refuses to fully credit — which is exactly why it stays an Outperform at a below-market multiple. Roku owns the habit of how a hundred million households start watching television, and it is finally turning that first screen into premium inventory — a real and durable advantage, even if the Market Perform valuation already reflects a good chunk of it.

The through-line for subscribers is the same one I keep coming back to: ignore the noise, underwrite the behavior, and follow the cash flow. The habits are sticky. The monetization is just getting started.

- Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.