Google Drops the Halo, Ad-Tech Desperation at OpenAI, and Roku’s 100 Million Milestone

$GOOGL, $ROKU

Accrued Interest TLDR: This Wed, I am watching Big Tech rapidly shed its altruistic research-lab persona in favor of operating like ruthless, margin-obsessed conglomerates. Google is trading its ethical halo for defense contracts, while OpenAI frantically builds out a surveillance-grade advertising stack to subsidize its staggering compute costs. Then, I want to talk a bit about Roku. The little streaming-stick-that-could just crossed 100 million users, which could help open the floodgates for mass-market ad dollars.

Please subscribe to read the rest of the Accrued Interest Daily Update for April 16, 2026.

A) Google Trades Principles for Pentagon Billions

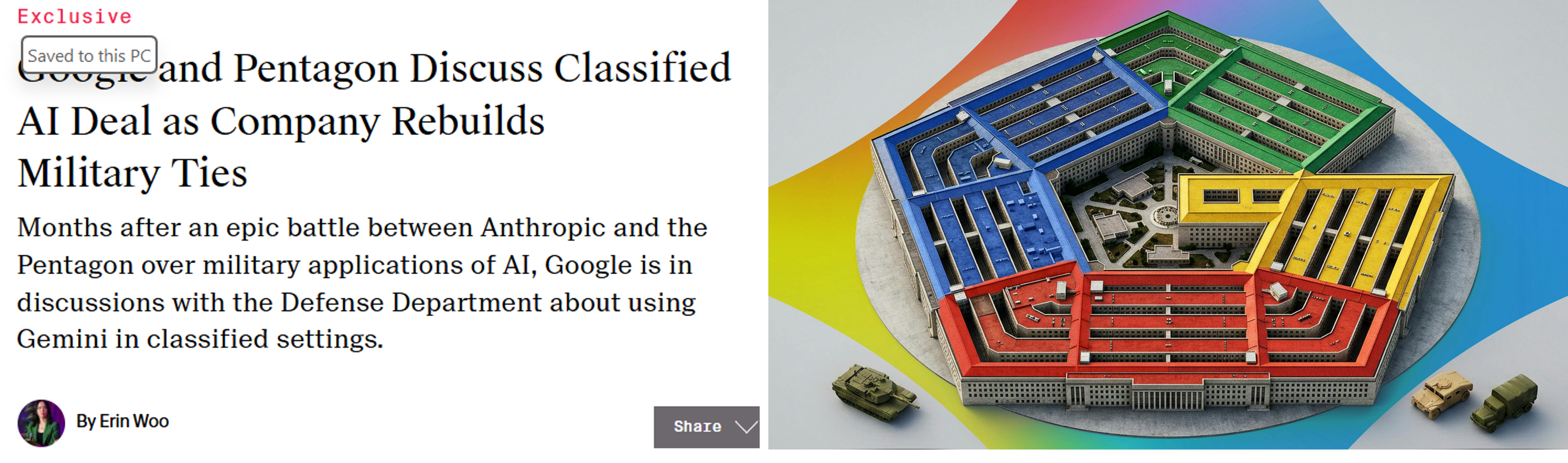

The era of “Don’t Be Evil” is officially dead and buried. According to The Information today, Google is currently in discussions with the Defense Department over a classified AI deal. This represents a massive, calculated reversal from 2018, when massive internal employee outcry forced the company to withdraw from the military’s Project Maven. Google is now aggressively going after growth wherever they can find it, completely regardless of their past principles.

Google has spent years rebuilding its relationship with the Pentagon, even setting up a dedicated Public Sector division in 2022 staffed with military veterans and former government contractors. This unit is not just a side project. They have a strategic plan to grow bookings to roughly $6 billion over a three-year period through 2027, with $2 billion of that specifically accounted for by defense contracts. The culture inside this unit is so distinct that members have reportedly coined the nickname “Big Google” for the rest of the company to maintain a sense of separateness and shield their work from the scrutiny of activist employees.

Google is also moving to ensure its hardware is ready for the front lines. The company’s secure cloud product, Google Distributed Cloud, has been accredited for classified work, and discussions are now focused on adding racks of graphics processing units to run Google’s specialized tensor processing units—its specialized chips—for the first time in classified environments. This aggressive pursuit of military dollars was signaled internally when Google quietly removed explicit provisions against using AI for weapons and surveillance from its principles early last year. As one attendee noted, the move was perceived as a “green light” for the public sector team to finally chase a wider array of lethal deals.

This strategy stands in stark contrast to Anthropic’s current predicament. The Pentagon recently declared Anthropic a “supply chain risk” and effectively excluded them from new military contracts after CEO Dario Amodei refused to drop safety safeguards that prohibited the use of their AI for mass domestic surveillance and fully autonomous lethal weapons. While Anthropic is suing the Pentagon over this designation, Google has successfully capitalized on the resulting hostility toward the startup. By removing its own safety-first ban provisions, Google has positioned itself as the more compliant, and therefore more profitable, partner for a Defense Department that is increasingly impatient with “agentic” ethical concerns.

My view on this is pure realpolitik. The President’s second-term reality is that defense spending is going to be rising, and Google is positioning its public sector team to capture those billions. I remain bullish on Google stock because its services are so indispensable that the company acts as a toll-collector for the entire internet. As I laid out in my previous article on the Pokemon Theory of Media Investing, Google has a Tier-S business model. Working with them is simply inevitable, no matter how much they pivot their ethical framework. Google remains an Outperform, and at $338 per share, the stock is up about 8% YTD.

B) The Conversion Pixel Exposes OpenAI’s Desperate Search for Margins

As I have discussed before, OpenAI is racing to transform themselves into an ad-selling machine. It was reported by Digiday, that the company is actively building the measurement layer required to prove their ads actually work, specifically testing a JavaScript conversion tracking pixel that fires when a ChatGPT user clicks an ad and completes an action on an advertiser’s site, like a registration or a purchase. They are rolling out a self-serve ads manager to replace their rudimentary insertion orders, and they are expanding their programmatic inventory through partnerships with ad-tech platforms like StackAdapt, Criteo, and Smartly.

In AdAge today, they reported that advertiser reactions to this rollout have been characterized by a mix of curiosity and skepticism. While early data suggests high engagement rates—with clicks on par with “brand search” on Google—media buyers still view the channel as largely experimental. The shift from OpenAI’s initial demand for premium $60 CPMs to the current “crude auction” environment is a clear signal that they are struggling to maintain pricing power. Agencies are currently seeing rates drop as low as $15 to $25 in less competitive categories, and many have barely been able to spend their initial commitments because there is simply not enough inventory yet. To combat this, OpenAI has slashed the minimum spending threshold to enter the pilot from the original $200,000–$250,000 range down to just $50,000, a move agencies see as a necessary step to lure in more experimental budgets and prove the platform’s viability.

The economics behind this pivot reveal a company scrambling for cash. OpenAI is projected to lose $14 billion this year alone, making them chase any revenue stream that can support the top line. My read on this situation is that OpenAI has absolutely no choice but to follow the same self-serve playbook written by Meta and Google. The compute costs associated with continuous, agentic AI are astronomically high. You simply cannot fund a global superintelligence infrastructure on $20 monthly consumer subscriptions. They need billions in ad revenue, and they need it immediately.

However, even with this aggressive shift toward performance-based advertising, OpenAI’s goal of hitting $100 billion in ad revenue by 2030 remains fundamentally unrealistic. As I argued in my previous update on April 9th, “Meta’s Muse Spark Rollout, OpenAI’s $100B Ad Dreams, and Uber’s Latest Robotaxi Deal (Accrued Interest Update 4-9-2026),” such a target would require OpenAI to capture roughly 8% of the entire global digital ad market in record time—a feat that assumes established giants like Google and Meta will simply stand still while their high-intent search and social budgets are cannibalized.

I cannot wait for OpenAI to finally go public, hopefully this year, so we can all better benchmark them against Meta and Google.

META 0.00%↑ , GOOGL 0.00%↑ GOOG 0.00%↑

C) Roku Hits 100 Million and Opens the Advertising Floodgates

Roku officially surpassed the 100 million streaming user milestone worldwide this week, a figure they announced via a pre-earnings press release to highlight their massive scale and momentum. They remain the number one TV streaming platform in the U.S., Canada, and Mexico by hours streamed. Alongside this massive scale, they recently expanded their value-focused offerings with the launch of Howdy, a low-cost, $3 per month ad-free subscription service. On a personal note, readers can expect more Roku coverage in the coming months. Now that I have officially dropped coverage of Fubo TV, I will be reallocating that bandwidth toward the San Jose-based streaming leader. (FYI - Please let me know in the comments if there are any publicly traded TMT companies you want to hear more about.)

Big picture - this 100 million mark is meaningful because it acts as a proxy for close to full distribution in North America. Hitting this milestone tells marketers that the Roku platform can reach almost every single home. This critical scale opens Roku up to more brand-focused advertisers who previously relied on legacy linear television to reach a nationwide audience. According to Comscore data, Roku already drives more than three times the engagement of the next leading TV operating system in the U.S., making its home screen the undisputed starting point for how a massive portion of the population discovers TV.

Roku currently trades at about $110 per share, up about 2% YTD. While I am very optimistic about the company’s strategic positioning, the stock is not exactly cheap. Trading at roughly 34x 2027 GAAP EPS, I believe this is a fair multiple that has a good amount of this positive news already priced in. More to come on Roku.

Tonight kicks off the start of Q1 2026 earnings season here on Accrued Interest. Netflix earnings are coming out today right after the bell. I will be reviewing the earnings results and the conference call tonight, and I encourage readers to check back for a full update once I’ve had time to digest the print. Subscribe to Accrued Interest now so you receive my updated Netflix take the moment I publish it. You can read my last NFLX deep-dive here, Why Netflix is a $120 Stock.

-Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.