Zuckerberg’s Middle-Age Metabolism: Trimming Fat to Fund Superintelligence

Meta is trading like a slow-growth utility, but acting like an AI monopoly. Don't let multiple contraction blind you to over 40% upside.

Accrued Interest TLDR: At $595 per share, Meta is a market-leading growth stock priced like a value trap. While Wall Street panics over AI infrastructure costs and macro jitters, Meta is executing a ruthless “middle-aged” transition defined by deep cost discipline and aggressive market share acquisition. With ad impressions accelerating (+18% YoY) and a highly resilient auction model, the fundamentals are incredibly strong. Furthermore, a newly filed executive compensation plan tying massive payouts to a staggering $9 trillion market cap proves management’s absolute conviction in the AI supercycle. Applying a fair 25x multiple to 2027 GAAP EPS estimates yields an $850 price target— at least 42% upside. Read the full breakdown below to see exactly why the market is completely mispricing this AI winner.

I. Introduction: A Contrarian Bet in a Jittery Market

We are about a month away from Q1 earnings in late April, and right now, the market is offering us a massive disconnect. META 0.00%↑ is currently down about 10% year-to-date, trailing the S&P 500, which is down 4%.

The Macro Mirage

I imagine a fair amount of this sell-off is being driven by broader macroeconomic anxiety. Oil prices are up and expected to stay elevated as the market braces for further conflict with Iran. With news breaking of the Pentagon deploying elite army units to the Middle East, the fear of consumer weakness and broader escalation is palpable across the tape.

The Superintelligence Sticker Shock

But that macro noise is only half the story. The real reason Mr. Market is aggressively selling off Meta is the prevailing narrative that Mark Zuckerberg is overspending on his quest for superintelligence. The headlines are dominated by massive AI infrastructure bills and the billions being thrown around in the form of lavish $100M pay packages for poached engineers. Wall Street is terrified that this spending is purely ego-driven and will ultimately not be profitable.

That fear hit a fever pitch over the last couple of weeks with reports that Meta is delaying the rollout of its newest flagship AI model, code-named “Avocado,” from March until at least May. Internal tests reportedly showed it lagging behind competitors, sparking rumors that Meta’s leadership is actually considering temporarily licensing Google’s Gemini to power its own AI products as a stopgap. For a company that guided for up to $135 billion in CapEx this year to build its own AI infrastructure, the mere suggestion that they might have to rent a competitor’s model is exactly the kind of headline that sends weak hands running for the exits.

A Midlife Clarification

However, if you look closely at the filings that hit the tape late Tuesday night (3/24), the board just sent a massive, bullish signal to the contrary through an unprecedented new executive compensation package. Meta is a company where both the organization and its leadership are approaching middle age.

But contrary to the market’s knee-jerk reaction, they are not in the middle of a crisis. Meta is consistently misunderstood by both investors and its users.

Because I want Accrued Interest to be a mix of value investing theory and tactical execution, I figured now was the perfect time to talk through why you have to be contrarian on this setup.

II. Evolve or Die: Meta’s “Middle Age” Transition

The $80 Billion Proof of Concept

Before we can accurately price Meta’s AI future, we have to look at the immediate past. For the last five years, Wall Street has obsessed over the cash bonfire happening inside Reality Labs. Between 2021 and early 2026, Meta burned roughly $80 billion on its Metaverse and VR ambitions.

But as I have pointed out to readers before, the most important takeaway from the Reality Labs saga isn’t the wasted capital—it is the proof of concept. The fact that Meta’s core Family of Apps could swallow an $80 billion speculative tangent without breaking the company’s underlying earnings power is staggering. It proves that the core digital advertising enterprise is so dominant, and the network effects are so deeply entrenched, that the business thrives in spite of Mark Zuckerberg’s most expensive hobbies, not just because of them.

Now, Zuckerberg is pivoting the machine toward artificial intelligence, but he is doing so with a completely different operational playbook.

Not Another “Year of Efficiency”

Recently, reports have surfaced that Meta is planning a headcount reduction of up to 20%. The instinct for many investors is to read layoffs as a distress signal, but it is vital to distinguish this current round of cuts from the highly publicized “Year of Efficiency.” The 2023 “Year of Efficiency” layoffs were, in reality, just a crude correction for the massive, undisciplined over-hiring that occurred during the COVID-19 boom. It was right-sizing a bloated tech giant back to its pre-pandemic trajectory.

This time, the situation is entirely different. This is a fundamental shift in operating philosophy.

Managing the Organizational Metabolism

Meta is officially embracing its middle age. When you are a young tech startup in your twenties, your hyper-growth metabolism can hide a lot of bad habits. You can carry excess organizational fat, hire aggressively, and still see the stock climb.

But being a middle-aged adult means you can no longer rely on that youthful metabolism to just magically carry you through. You have to take active, deliberate steps to trim the fat, watch your diet, and optimize your routine to stay healthy.

Meta isn’t slashing 20% of its workforce because they are facing a crisis or missing revenue targets. They are proactively shedding weight. By aggressively deploying automation and leveraging the very AI tools they are building to increase engineering output, they are actively managing their operational metabolism. They are taking the painful but necessary steps to fund their massive AI infrastructure build-out internally, ensuring they don’t have to sacrifice their margins to fund their next chapter.

III. Expanding the Moat: Politics & The AI Arsenal

Meta’s management of its operational metabolism is only half the equation; the other half is a ruthless expansion of its competitive moat. While the media fixates on Mark Zuckerberg’s long-term vision for superintelligence, they are entirely missing the tactical, ground-level warfare Meta is currently winning.

Political Content Push

Take the political landscape. For years, Meta has actively tried to distance itself from politics, going so far as to algorithmically deprioritize political content in the News Feed to avoid controversy. But the threat of TikTok has changed the calculus. Meta recently executed a quiet but massive about-face, rolling out financial incentives that pay top political creators up to $268,000 a month to post on their platforms.

This is a profound shift. Meta is explicitly prioritizing market share and audience capture over its previous desire for platform neutrality. As I have noted before, the audience will ultimately dictate who wins the media wars, and Meta is aggressively following that demand, weaponizing its balance sheet to poach creators from TikTok ahead of the midterms.

The Enterprise AI Stealth Play

But they aren’t just buying creators; they are building an entirely new infrastructure to lock them—and the advertisers who fund them—into the ecosystem.

This brings us to the recent acquisitions of Manus and Moltbook.

If you only read the mainstream tech press, you would think Meta’s AI ambitions are strictly about building consumer-facing chatbots to rival ChatGPT. That completely misses the enterprise play. Moltbook brings a dedicated social network for AI agents and top-tier talent into Meta’s Superintelligence Labs.

More critically for the stock’s valuation, the integration of the Manus tool is a game-changer for the actual revenue engine.

Manus isn’t a toy; it is an agentic AI built specifically for media planners and buyers to automate campaign analysis, audience research, and competitor tracking using Meta’s massive Ad Library. By integrating autonomous AI agents directly into the workflow of creators and media buyers, Meta is creating an incredibly sticky, high-utility toolset. They are transforming from a platform where you simply buy ads into the autonomous operating system you use to run your entire digital marketing business. That kind of utility typically commands a massive premium. It makes leaving the Meta ecosystem virtually impossible, which makes it all the more ridiculous that Meta is currently trading at a steep discount to the broader market multiple.

IV. The Fundamentals Engine is Still Roaring

The ATT Myth and the Revenue Floor

To fully appreciate the absurdity of that discount, you have to look at the resilience of the core business. There is a widely misunderstood narrative on Wall Street regarding Meta’s sensitivity to the broader economy. The truth is, Meta has never actually faced a revenue decline driven by macroeconomic events.

The only period of sustained pressure on their top line occurred when Apple introduced its App Tracking Transparency (ATT) framework. That wasn’t a macro issue; it was a structural signal loss. Meta was forced to rebuild its advertising signal from the ground up for advertisers without relying on Apple’s ecosystem. As their recent performance proves, they succeeded spectacularly.

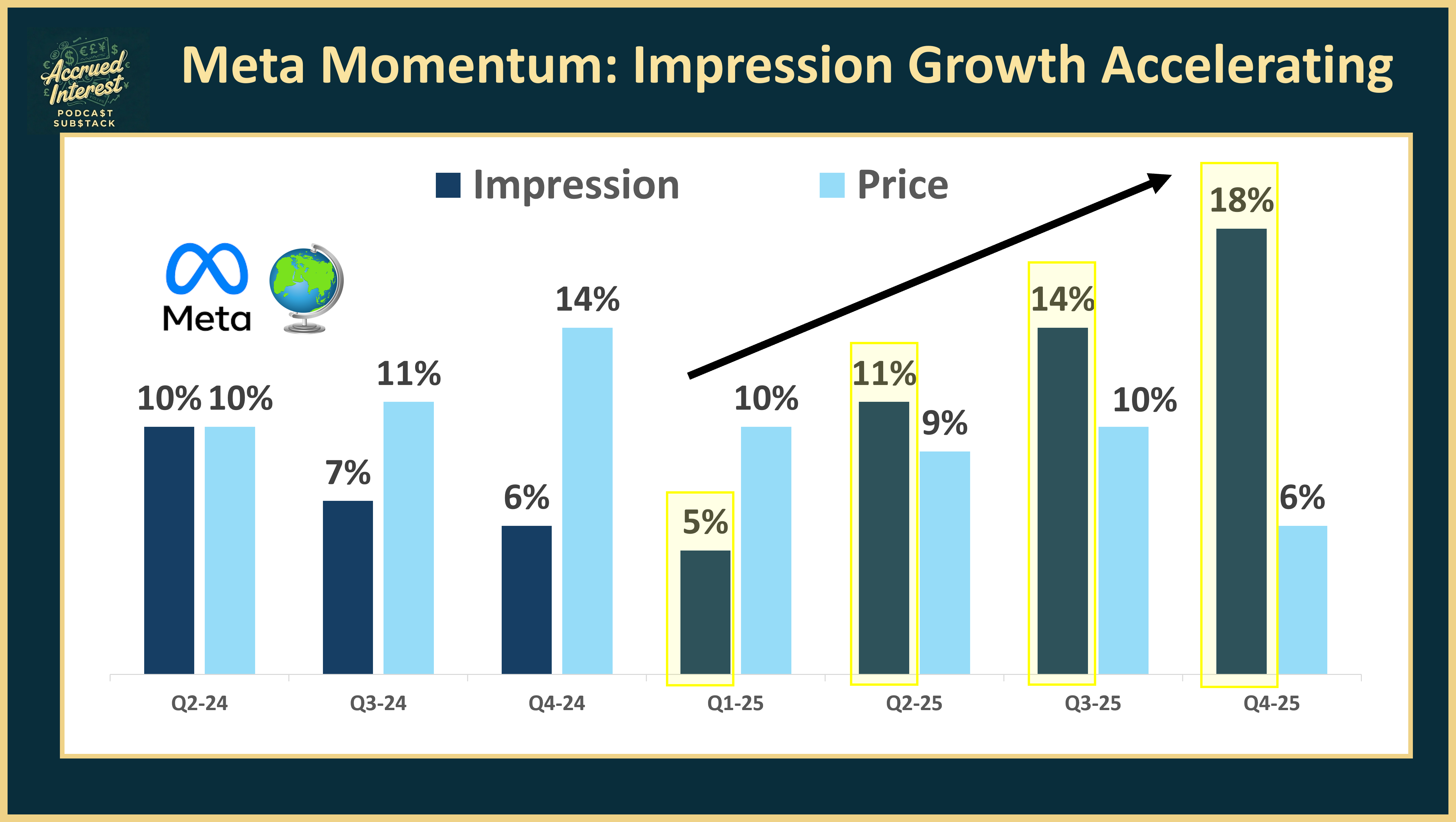

The Metric That Matters

As a reminder from my Q4 2025 earnings recap, the single most important metric for evaluating the health of this machine is ad impression growth. In Q4, ad impressions grew an incredible +18% year-over-year. That wasn’t an anomaly; it was the continuation of a trend where ad impression growth has accelerated sequentially over the last three quarters. The AI is working. It is keeping users engaged longer and creating more inventory.

Furthermore, the very nature of Meta’s auction-based model provides a massive structural hedge against the consumer weakness the market is currently fearing. If rising oil prices or geopolitical anxieties cause one major advertiser to pull back their spend, the auction doesn’t break—the next bidder in line simply steps up to clear the inventory.

The financial guidance tells the same story. For Q1 2026, management guided for revenue between $53.5 billion and $56.5 billion. If Meta continues to grow its top line at around +20% year-over-year, they can easily fund their AI ambitions out of free cash flow. All they have to do is execute, and Wall Street will inevitably forgive the CapEx.

(A quick note to all of my free subscribers—which, as of right now, is 100% of you! In the future, this is exactly the type of section where I might apply a selective paywall as we get into the harder valuation mechanics, EPS breakdowns, and technical modeling. But in the meantime, please enjoy the free analysis below, and if you haven’t already, make sure to hit that subscribe button!)

Now, let’s get into the numbers and see why the multiple is completely disconnected from reality.

V. Valuation: A Growth Giant Priced Like a Value Stock

Multiple Contraction Meets the AI Supercycle

The most critical thing to understand about Meta’s current stock price is that the recent sell-off has not been driven by a deterioration in fundamental earnings power. The earnings are still there. The sell-off is entirely a function of multiple contraction. Mr. Market has decided to punish the stock because of the headline sticker shock of the CapEx guidance.

But when you zoom out, this panic has created an absolute gift for investors willing to look past the next quarter. It is genuinely insane for a company as dominant as Meta—a company that is actively shaping up to be one of the definitive winners of the AI arms race—to trade at a discount to the broader market multiple.

The Path to $850 per Share

Let’s look at the actual math, referencing the latest estimates from the TIKR Terminal:

Current Price: ~$595

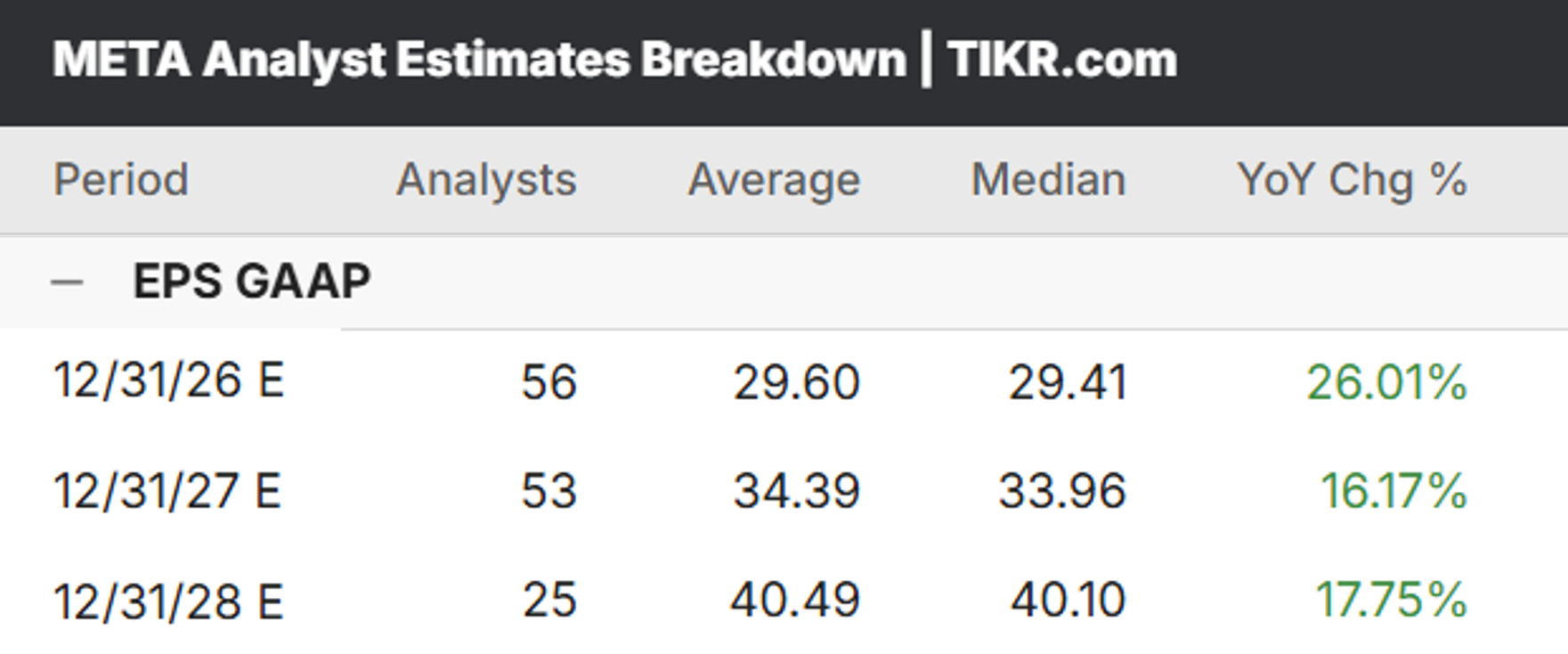

2026 Valuation: The stock is currently trading at just 19.8x consensus 2026 GAAP EPS of roughly $30 per share.

2027 Valuation: Looking one year further out, it is trading at a staggering 17.5x consensus 2027 GAAP EPS of roughly $34 per share.

I see a clear, structurally sound path to $850 per share. If the market wakes up and simply applies a fair, market-level 25x multiple to those 2027 earnings of $34 per share, we get to $850. That represents an upside of over 42% from today’s levels.

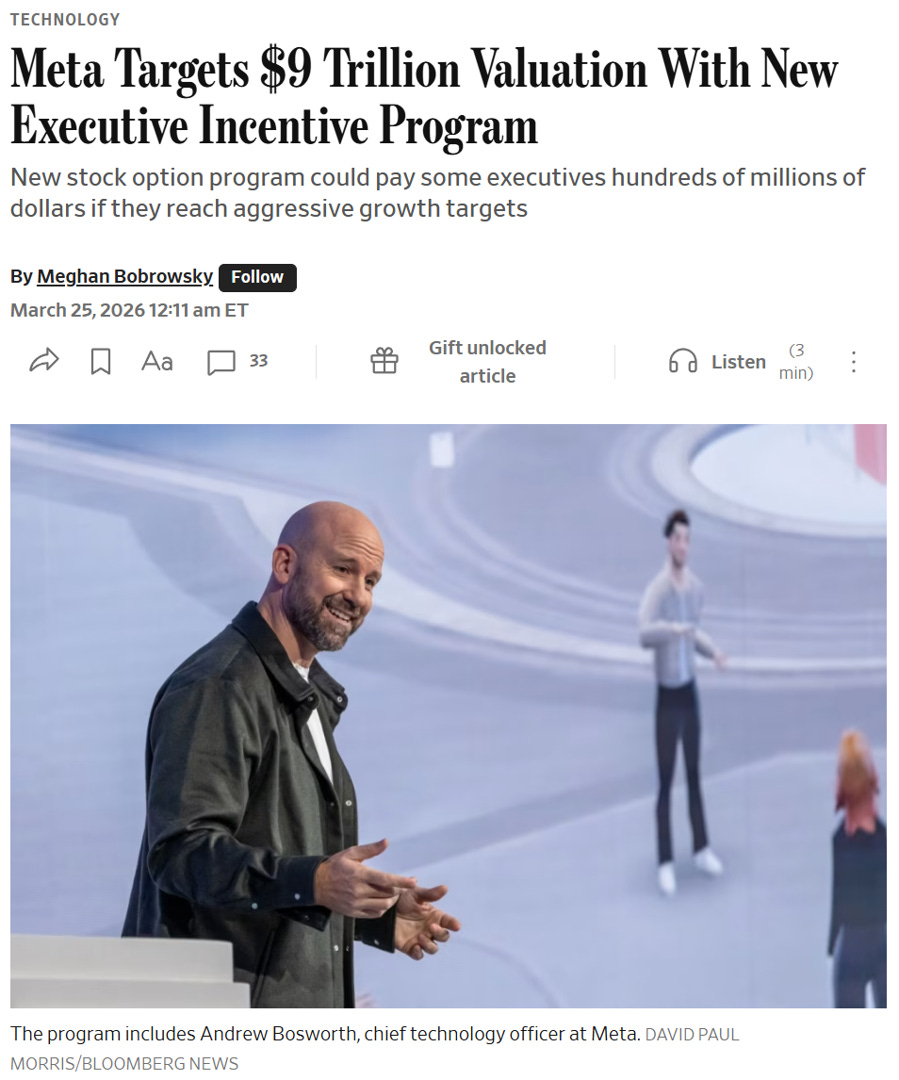

The $9 Trillion Declaration of Intent

If you need further proof of management’s conviction in this trajectory, look at the SEC filings that hit the tape this week detailing a new executive incentive program. The program is designed to vest in tranches, culminating in a full payout only if Meta reaches a $9 trillion market capitalization by 2031. For context, that requires the stock to surge over 500% to $3,727.12 per share. The floor is equally telling: the very first tranche doesn’t even begin to pay out until the stock hits $1,116.08—an 88% premium to today’s trading levels, representing a ~$2.82 trillion market cap.

The options cover the core operational brain trust: CFO Susan Li, CPO Chris Cox, COO Javier Olivan, CTO Andrew Bosworth, CLO C.J. Mahoney, and Vice Chairman Dina Powell McCormick. Alongside these options, Meta is boosting RSU grants for these execs by $170 million. This highlights the sheer cost of the ongoing AI talent war; in 2025, cash costs tied to employee stock awards consumed 96% of Meta’s free cash flow ($42 billion), necessitating massive buybacks just to offset the dilution.

The Tesla Playbook on a Compressed Timeline

This options package acts as a massive neon sign confirming management’s internal modeling for the AI supercycle. First, it forms a direct bridge past my $850 price target. This new incentive plan essentially confirms that management views the $800-$900 range not as a terminal plateau, but as a stepping stone. By setting the absolute minimum payout threshold at $1,116.08, the board is signaling that the fundamental engine is expected to push earnings power significantly higher as the 2026/2027 CapEx investments come online.

Second, it is the Tesla “moonshot” playbook, but on a compressed timeline. Meta’s board is demanding growth from $1.5 trillion to $9 trillion in just five years.

This aggressive 2031 deadline tells us that management believes the transition from a traditional social media ad platform to an autonomous, agentic AI ecosystem will trigger a violent, structural multiple expansion much faster than the market currently anticipates.

Finally, it serves as a brilliant hedge against the “CapEx shock” narrative. This compensation structure is the board’s way of locking in the executive team and aligning their wealth entirely with shareholder value. If the CapEx buildout turns out to be a cash incinerator, these options expire worthless. The executives are now financially handcuffed to the success of the infrastructure moat they are currently spending billions to build.

This isn’t a standard retention package; it is a declaration of intent.

Conclusion: The Tactical Play

You have to be contrarian here. The market is incorrectly handicapping this AI winner, pricing it like a value-trap utility rather than a compounding growth engine. I strongly recommend considering adding to common stock at these levels. Alternatively, for those looking to maximize leverage on this mispricing, consider looking at LEAPS (long-term options) expiring in late 2027.

Starting in late 2026, as the midterms approach and political ad spending shifts into overdrive, many investors are going to wake up and realize just how massive a share of those political ad dollars are flowing directly into Meta. Between that influx of cash and the fully realized efficiencies of their AI infrastructure, everyone is going to remember just how necessary this machine is, and the multiple will violently re-rate.

Don’t bet against the machine when the engines are just getting warmed up.

-Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.

I also think that the market is overreacting. The current price is already close enough to my bear case I built in November.

But I am cautious about the valuation. With massive AI spending, actual FCF deviates from earnings much more than before, so it is hard to draw conclusions based on the 25x multiple. And massive SBC also eats shareholder value; it's just better masked in the P&L.

I’m waiting for the new filings to refresh my models.