Why Uber Will Outperform in 2026 ($UBER)

12 Days of Pitch-Mas Day 7

The market is currently pricing Uber as if the robotaxi apocalypse is imminent. It is not. In fact, the rise of autonomous vehicles (AVs) is likely the biggest tailwind Uber will see this decade. Here are the five key reasons why I am bullish on Uber for 7th Day of Pitch-Mas on Accrued Interest.

Accrued Interest TL;DR on Uber

Since it has been almost 6 months since I did a dedicated write-up on Uber - let me expand on my thesis below. For context, I recommend you read my July pitch - Uber’s 2025 Performance: Why $UBER Stock Soared and What’s Next. Here is how my thoughts have evolved.

The “Hybrid Network” Moat: The future is not binary (Human vs. Robot); it is hybrid. Demand is volatile. Robots are a fixed supply. Human drivers are the “flex” capacity that makes the math work. Uber is the only player capable of dispatching a Waymo for an afternoon ride and a human driver for a chaotic rainy Friday night.

The Aggregator Wins the War: History shows that in fragmented markets the aggregator captures the value. Uber is building an “operating system” for local commerce. They do not need to own their own robotaxi fleet. AV companies are great at technology but lack the global distribution network to acquire customers cheaply. They need Uber.

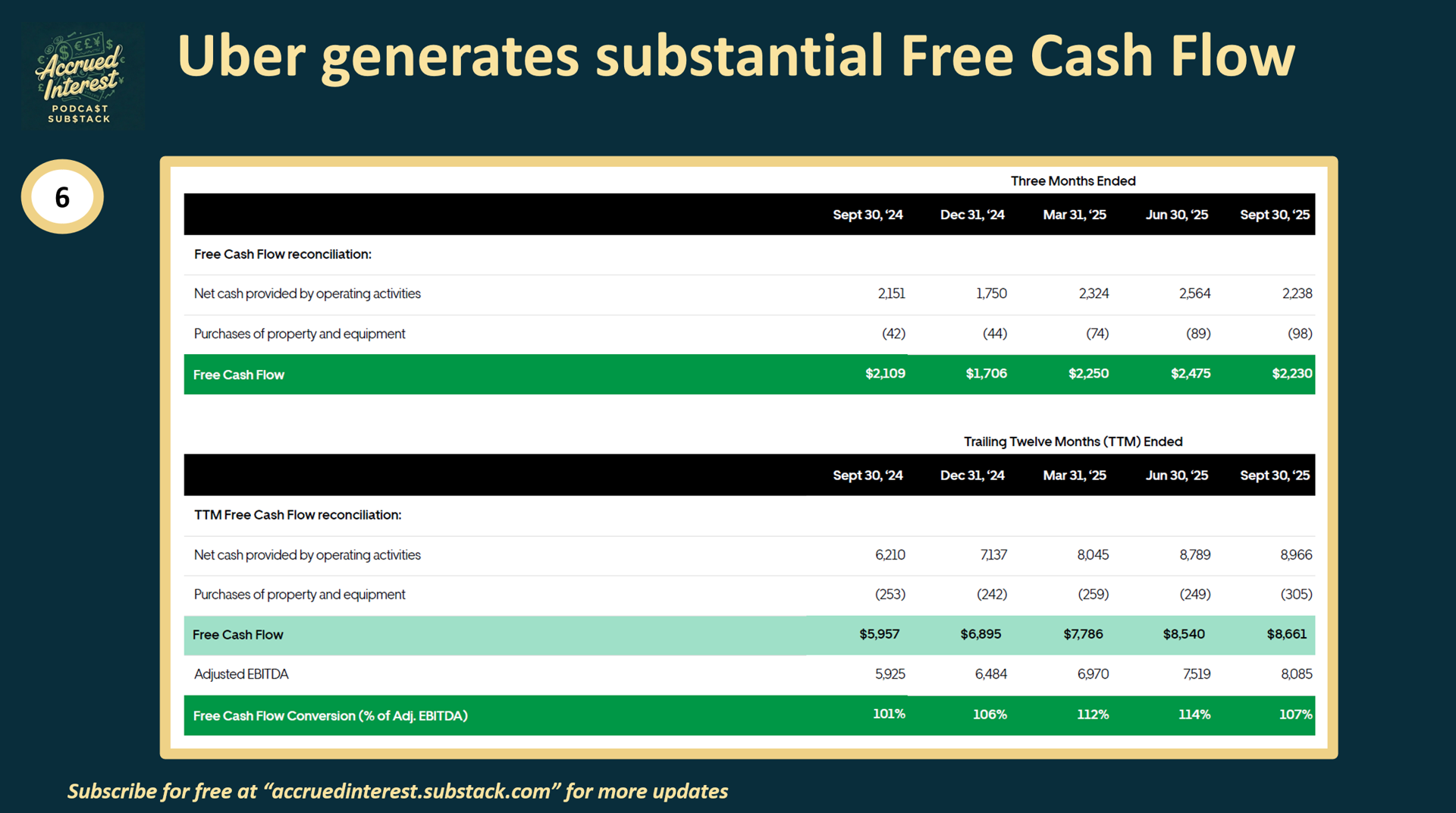

Financials are Solid: The days of "cash incineration" are over. Q3 2025 proved the model continues to work. Adjusted EBITDA grew 33% year-over-year to $2.3 billion. Free Cash Flow is converting at a high clip, hitting $2.2 billion last quarter.

Delivery is Future Upside: While everyone watches robotaxis, Uber’s delivery arm is setting up the company for growth for years to come. Delivery Gross Bookings grew 25% YoY in Q3 2025. New verticals like grocery and retail are now running at a $12 billion annual rate.

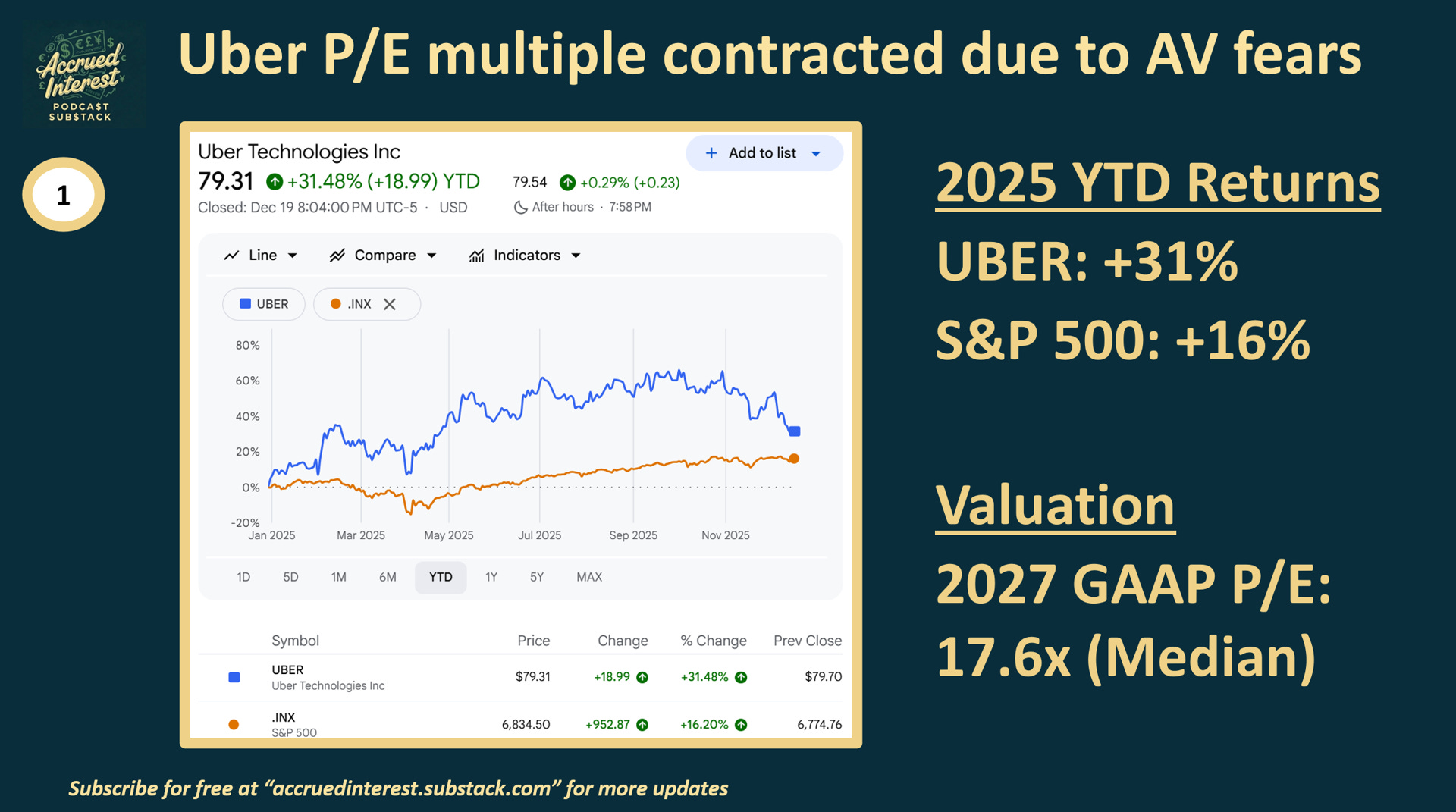

Valuation Disconnect: I like investing in situations where the fear is priced in, but the growth is not. Uber is a classic GARP (Growth at a Reasonable Price) play, trading at roughly 17x–18x 2027 earnings. As earnings grow, the “robotaxi discount” will vanish.

Now let us dive in and dissect some of the qualitative aspects of the Uber story.

Uber Bear Thesis vs. Reality

My variant perception on Uber is simple: The stock is experiencing multiple contraction because investors fear autonomous vehicles (AVs) will steal market share and cannibalize Uber’s unit economics.

Based on the trajectory of Waymo and the broader industry, my thesis from my Uber writeup over the summer still stands firm: Uber will be the dominant, preferred platform. It will be the network that every AV provider—Waymo, Cruise, etc. —must join to get utilization rates high enough to survive.

But here is the problem with the fear around AV’s: It will take at least a decade to prove or disprove.

We are in the “fog of war” phase of AV development where it is not a foregone conclusion how the industry will develop. But I want to remind readers that successful investing requires us to make predictions before the dust settles. As Warren Buffett once said, “the future is never clear; you pay a very high price in the stock market for a cheery consensus.” Being contrarian requires you to realize that uncertainty is the friend of the long-term investor.

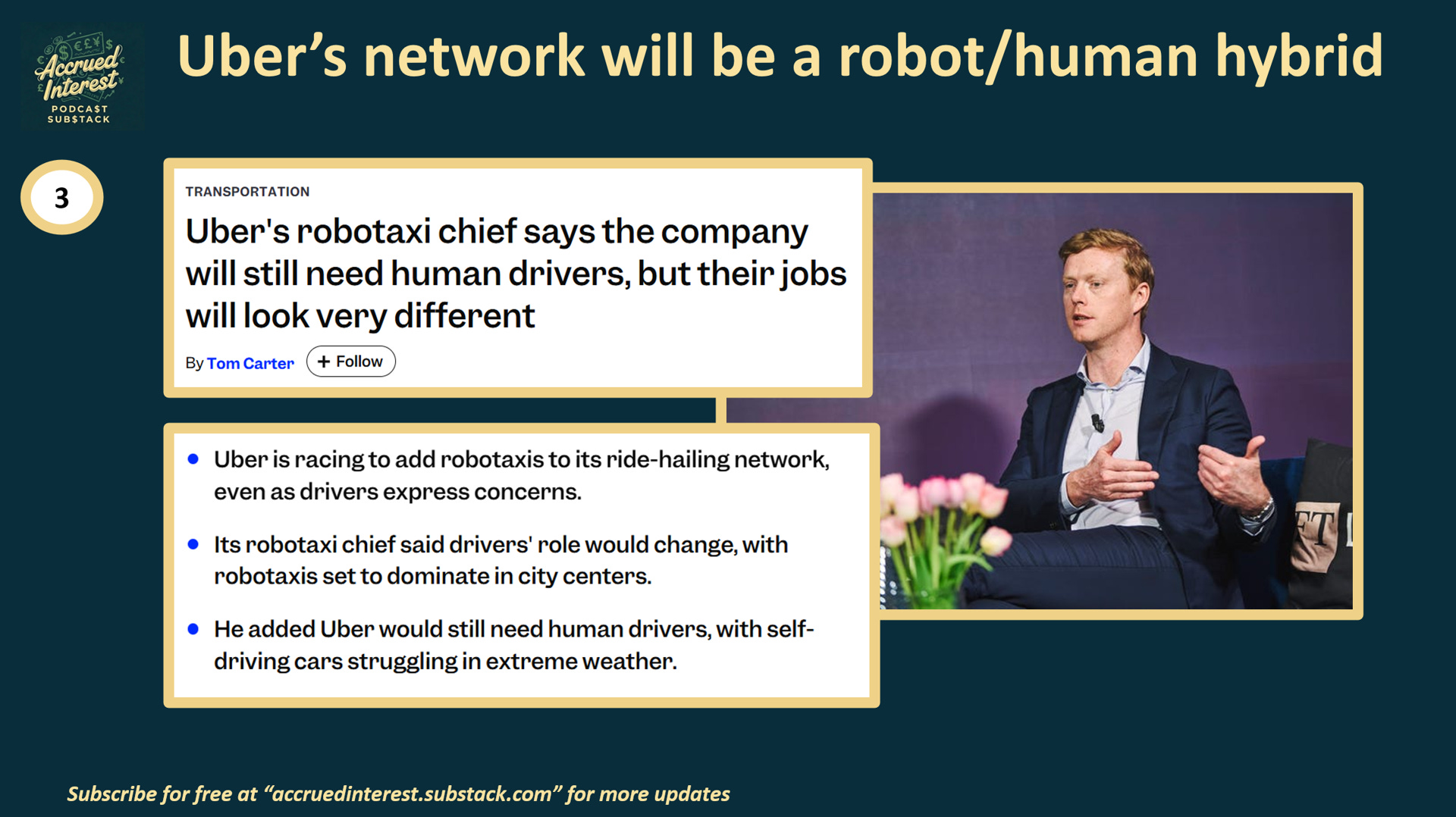

The Hybrid Robot-Human Future

Bears argue that as AV safety records improve, human drivers will go the way of the dodo. I disagree. Let us kill the “all-or-nothing” narrative.

For the next decade of transition (or longer), the market will demand a hybrid network. Because managing a rideshare platform is a logistical nightmare. You must match volatile supply with unpredictable demand across thousands of cities, weather conditions, and major events.

Robots do not like rain. They do not handle “surge” demand well because you cannot magically spawn more robotaxis for an hour after a Taylor Swift concert. Human drivers are going to be the elastic supply when the rideshare networks add robotaxis.

Uber is uniquely positioned to dominate because it controls both layers. To maximize fleet utilization, Uber will use its platform to match riders with the best option. For example, if a customer is too price sensitive, they can request a human driver. If they are a tech enthusiast, they can order a Waymo. And if they are indifferent and just want to avoid the rush hour surge, then the algorithm can find whichever option is closest.

Uber management has been explicit: they view themselves as complementary to Waymo and other robotaxi providers, not a competitor.

Waymo as a “Tourist Attraction”

The Uber bears love to point at San Francisco rideshare market as evidence that Waymo is stealing share. As of late 2025, reports indicate Waymo has captured approximately 27% of the San Francisco market, effectively passing Lyft to become the number two player. Meanwhile, Uber’s share in the city has dipped from 66% to around 55%.

But let us zoom out. Extrapolating the demise of Uber from a single, dense, tech-obsessed city is shortsighted. Right now, AVs in San Francisco are essentially tourist attractions. A lot of the demand is coming from people downloading the app just to say they rode in a ghost car.

More importantly, we must acknowledge that Waymo’s owner, Alphabet (e.g., GOOGL 0.00%↑ ) has modified its capital allocation strategy over the last decade. The “Other Bets” division is no longer a charity for cool science projects; they want profitability. Google knows that building a global operations team to manage millions of riders is low-margin hell. I do not think they even want to be Uber.

I expect Waymo to eventually license its software or “white label”. Like Uber, Waymo wants to be asset-light. Owning, cleaning, charging, and repairing a fleet of 10 million vehicles is a headache Google will happily outsource to fleet managers who plug into Uber’s network.

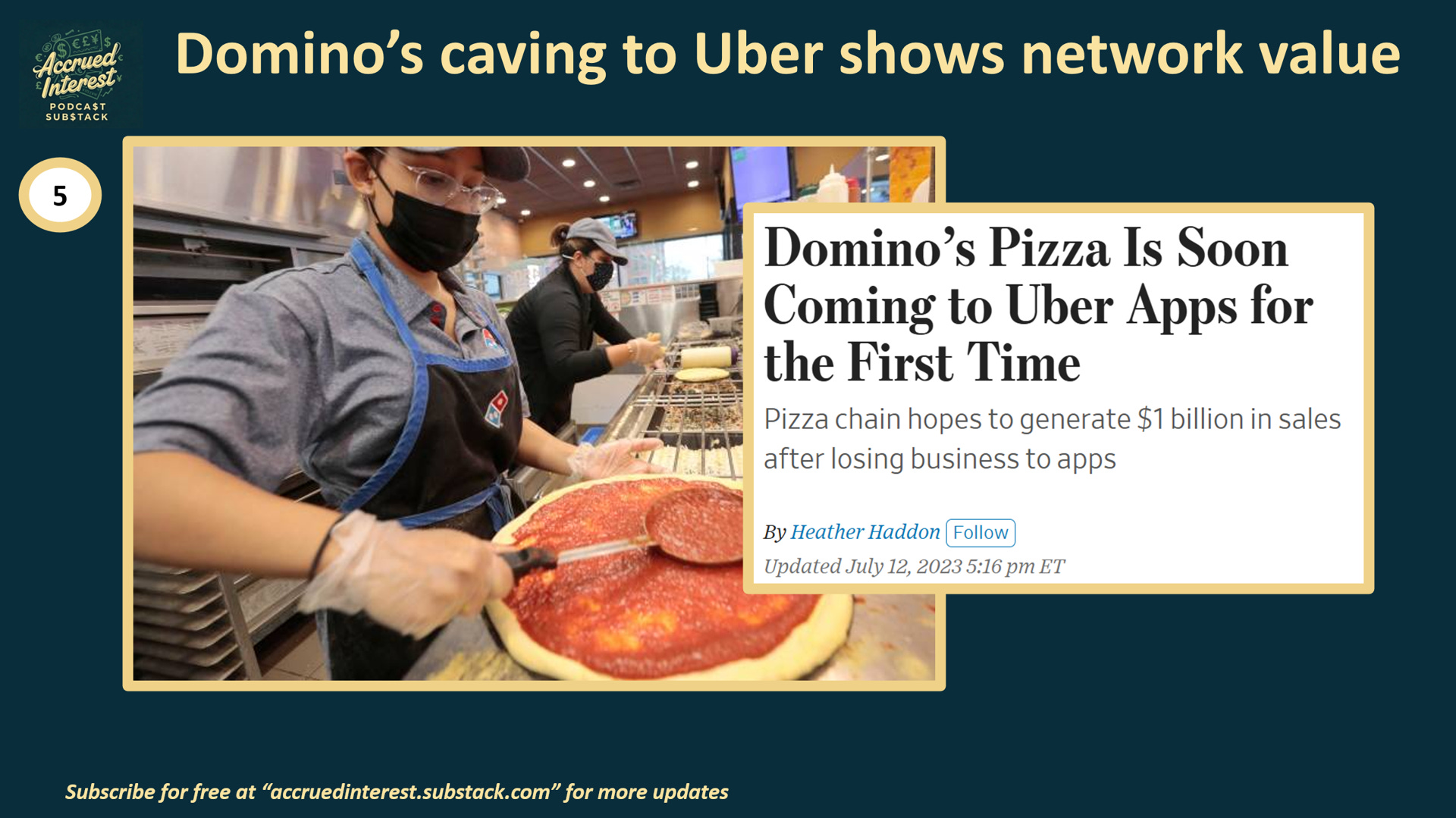

Uber is the “Netflix of Transportation”

Uber’s moat is not just technology; it is scale. If a new AV company wants to go global, they have two choices:

Spend 10 years fighting regulators, building local operating teams, and burning billions on customer acquisition.

Partner with Uber and turn on the revenue tap instantly.

Think of Uber as the Netflix of transportation. Netflix is the only streamer (besides YouTube) that is dominant in 100+ countries. That distribution power is leverage. Neither Lyft nor any robotaxi upstart can match it.

We are already seeing this platform power play out in food delivery. Domino’s Pizza—a company that famously refused to use third-party apps— caved and partnered with Uber in late 2023 with a goal of reaching new customers. If a best-in-class operator like Domino’s needs Uber’s network, robotaxis eventually will, too.

Q3-25 Financials Remain Strong

Every few quarters it is worth reminding readers that Uber is no longer the perennially cash-burning startup many remember from the 2010’s. Uber’s Q3 2025 demonstrated that the organic growth engine is still strong:

Growth Continues: Gross Bookings hit $49.7 billion, +21% YoY, landing on the high end of management’s guidance range for the quarter.

Network is Expanding: Total trips reached 3.5 billion, up +22% YoY. That is the fastest trip growth the company has posted since 2023. The growth in trips was supported by a +17% increase in Monthly Active Platform Consumers (MAPCs), reaching a total of 189M. And each MAPC completed an average 6.2 trips per month, +4% YoY.

Profitability is Real: Adjusted EBITDA was up +33% YoY to a record $2.3 billion. Even better, Uber generated $2.2 billion in free cash flow (FCF).

Delivery is Evolving: Delivery is not just for Friday night pizza. Gross bookings were up +25%, driven by an expansion into grocery and retail that is now operating at a $12 billion annual run rate.

Loyalty Lock-in: The Uber One membership program has swelled to 36 million members. These riders spend more and churn less.

My investment thesis is not predicated on Uber crushing consensus estimates next year. Uber’s performance is great and just needs to continue the current trajectory to demonstrate to their non-believers that the business is real and not being disrupted.

CONCLUSION

The market is distracted by the “Human vs. Robot” noise, missing the bigger picture: Uber is the platform that wins regardless of who is driving the car. If earnings keep growing, the “robotaxi discount” will vanish and the stock price will eventually catch up to reality. Right now, the fear of AV disruption is being priced in, but the growth potential is not. Uber is a classic GARP (Growth at a Reasonable Price) play, trading at roughly 17x–18x 2027 earnings. I can easily see this returning to a $100 stock in 2026. With the stock at $80 currently, that’s +25% potential upside. So next year let us ignore the sci-fi fearmongering and let Uber’s earnings tell the story.

Therefore, I am recommending UBER 0.00%↑ as an Outperform for 2026.

If you found this interesting, do not forget to subscribe. And please come back for Day 8 of Accrued Interest’s 12 Days of Pitch-Mas! You can find prior days here:

Day 1 - Why Netflix Should Acquire Warner Bros. NFLX 0.00%↑ , WBD 0.00%↑

Day 2 - Why Paramount Skydance Won’t Win Warner Bros, PSKY 0.00%↑

Day 3 - No Bonus Points for Creativity—Just Buy Google, GOOGL 0.00%↑ GOOG 0.00%↑

Day 4 - Nexstar + Tegna: Capped Upside and Regulatory Risk, NXST 0.00%↑ , TGNA 0.00%↑

Day 6 - Why Disney Stock Will Underperform in 2026, DIS 0.00%↑

-Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.