Why Nvidia Will Outperform in 2026

12 Days of Pitch-Mas Day 11

For Day 11 of Pitch-Mas, I am recommending Nvidia ($NVDA) as an outperform. Ignore the “peak AI” headlines and “law of large numbers” worries. While bears search 2025 charts for a top, Nvidia is trading at its cheapest valuation relative to growth prospects in years. My core thesis is that the market is fundamentally mispricing the durability of this cycle. This is not a bubble, but the start of a structural re-architecting of global computing. The emergence of cheaper “intelligence” is fueling an explosion of new AI use cases, like Agentic AI, which are continuously escalating demand for compute.

Recent strong Q3 results, including a +162% YoY spike in Networking sales, precede another wave of revenue acceleration. Counter to bear arguments, the global compute shortage ensures no chip becomes obsolete; older units simply transition from the training to the high-volume inference market, disproving claims of a looming inventory problem. Finally, the planned late 2026 launch of the Vera Rubin architecture will drive revenue growth higher into 2027 and beyond.

Here are four reasons why I expect Nvidia to outperform the market (again) in 2026.

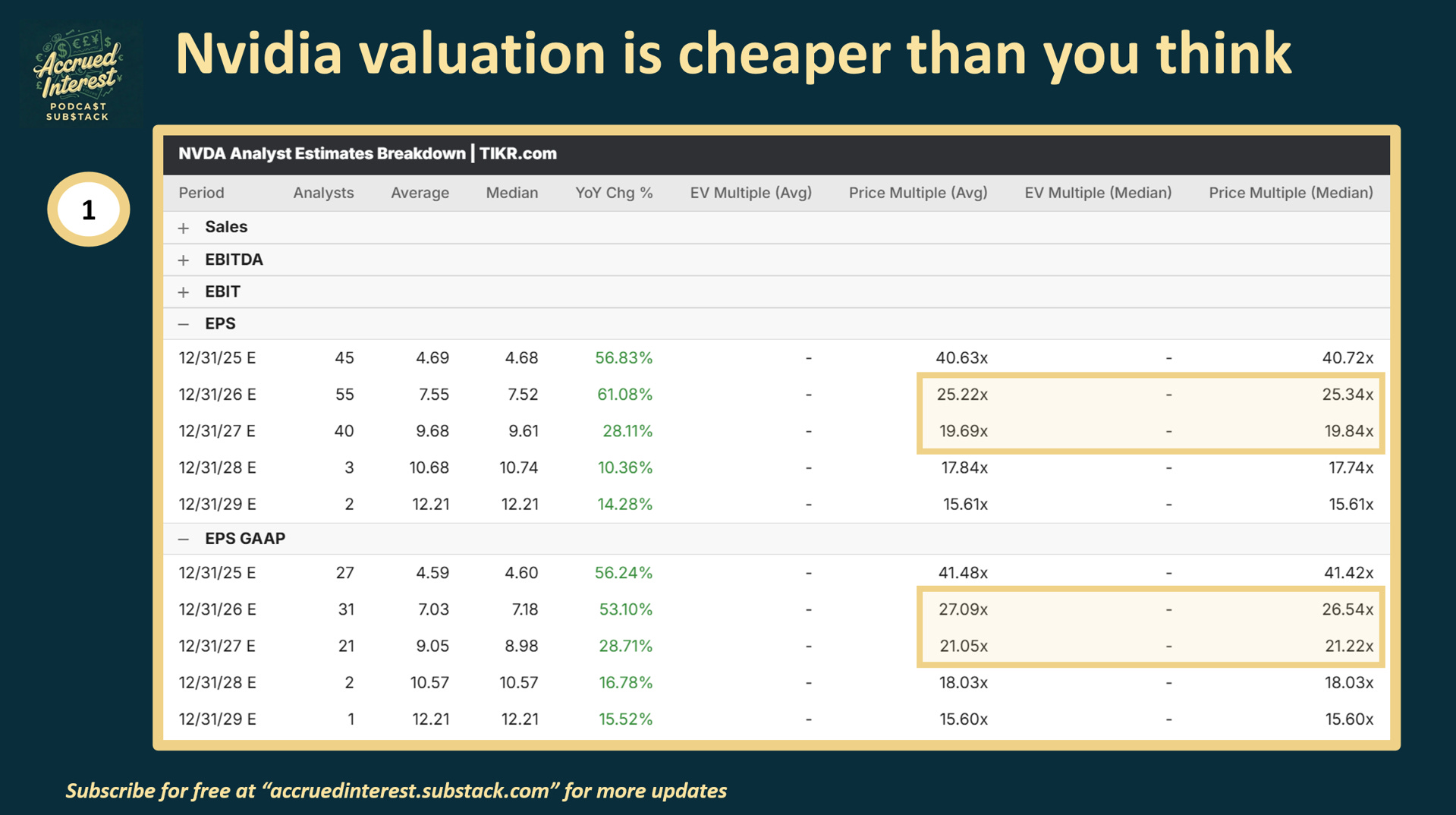

1. Valuation math says it’s cheap (really)

I 100% understand that recommending a stock that has run this much feels like chasing. But the financials have held up despite recent skepticism. And the valuation does not tell the story of a radically expensive stock.

Current valuation is not demanding - For all the talk of a bubble, Nvidia stock at $188 a share is trading at approx. 27x 2026 GAAP EPS and 21x 2027 GAAP EPS.

It is not often that you find a market leading stock trading at less than 30x next year’s earnings. This discrepancy is what initially got me interested in pitching Nvidia stock after not publishing a dedicated write-up for all of 2025.

An “11th Percentile” situation : Stacy Rasgon at AllianceBernstein recently highlighted a metric that shows how cheap the stock has become in a historical sense:

“For this company, 25x forward EPS would suggest the shares are trading in the 11th percentile of valuation over the last 10 years,” Rasgon said.

“Investors buying Nvidia’s stock at current levels have historically done very well,” the firm said, adding that purchases below 25x forward earnings over the past 10 years delivered “average 1-year returns of over 150% with zero instances of a negative drawdown.”

SOX discount – Even more telling than its absolute valuation, NVIDIA is currently trading at a ~13% discount to the Philadelphia Semiconductor Index ($SOX). The company with the fastest growth, the highest gross margins (~74%), and the strongest moat is trading cheaper than a basket of its slower-growing peers like Texas Instruments TXN 0.00%↑ or Intel INTC 0.00%↑ .

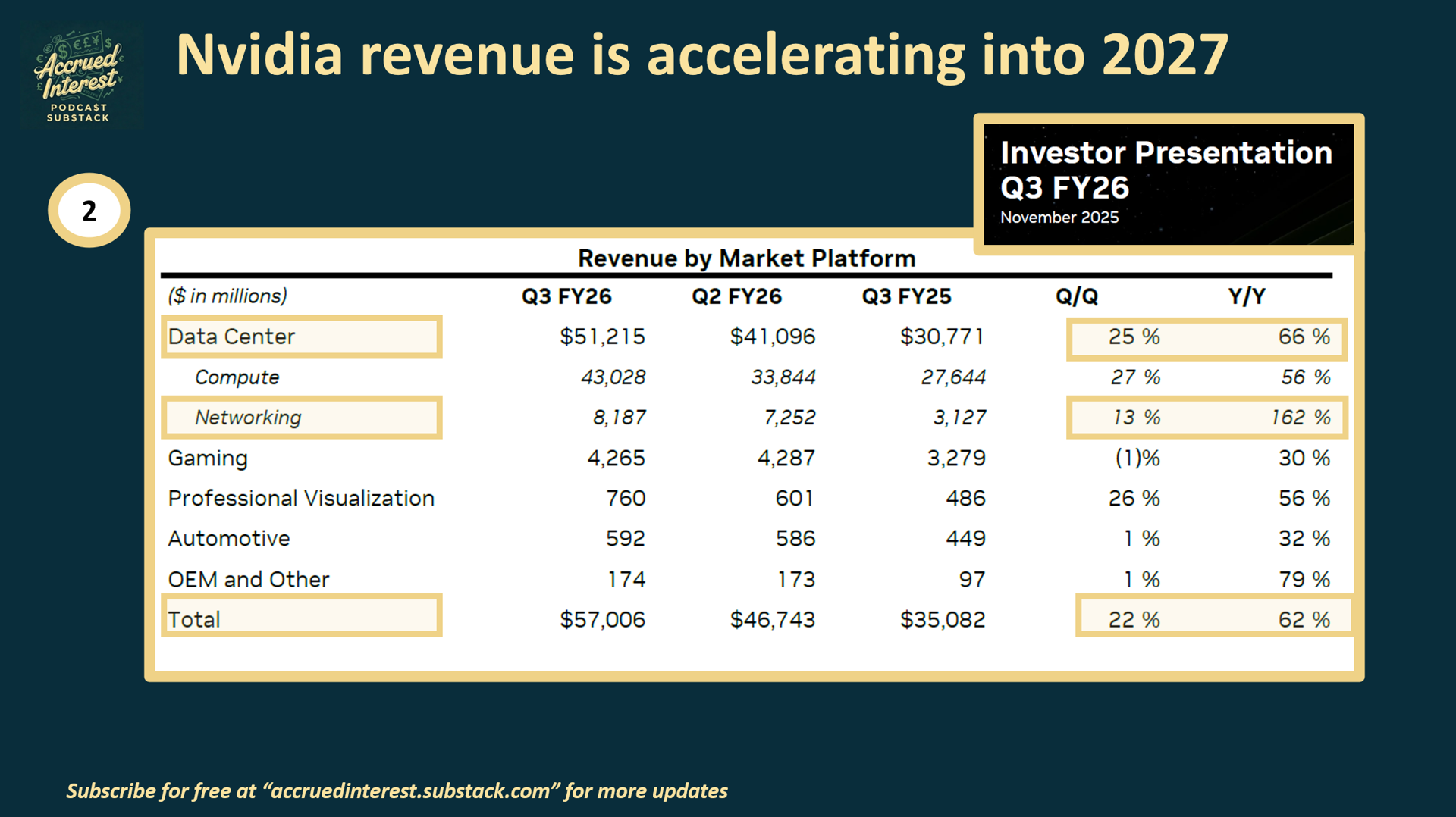

2. The return of revenue acceleration

In the Q3 FY2026 NVDA report - the most important number was not the headline EPS beat. It was the Networking revenue, which hit $8.2 billion, up +162% YoY.

Network revenue as precursor to more data centers - You cannot build a massive “AI Factory” (clusters of 100,000 GPUs) without laying the fiber optics and switches first. When you see a spike in networking revenue, it is a leading indicator of data center construction.

“Growth Cliff” myth is dead - Bears spent the last three months terrified that NVDA’s growth was flattening and that the “law of large numbers” was finally catching up to Nvidia. In Q2, revenue growth was only +6% QoQ (sequentially). Q3 blew that theory out of the water with revenue re-accelerating to +22% QoQ.

NVDA proved that the Q2 lull wasn’t a demand problem; it was a supply timing issue as they transitioned products.

Management confirmed that Blackwell is sold out well into fiscal 2027.

3. We are nowhere near “Peak AI”

The most common bear argument I hear is some version of this - “Once the big models like GPT-5 are trained, demand will crater.” This is a fundamental misunderstanding of how software works, and it ignores the Jevons Paradox: when you make a resource (intelligence) more efficient and cheaper, consumption doesn’t go down—it explodes because you find new ways to use it.

We are moving from “Generative AI” (chatbots) to “Agentic AI” (digital employees). This shift changes the math on compute entirely.

Multiplier effect: If you ask ChatGPT a question, it uses a small burst of compute to answer. But an “AI Agent” that is tasked with “planning a travel itinerary” or “refactoring code” might “reason” for 10 minutes, browse the web, check its own work, and iterate before giving you an answer. This “Test-Time Compute” requires 10x to 100x more inference power per query than we use today.

“Big 4” hyperscalers: Companies such as Microsoft MSFT 0.00%↑ , Meta META 0.00%↑ , Google GOOGL 0.00%↑ , Amazon AMZN 0.00%↑ are projected to spend over $500 billion in combined Capex in 2026. And Nvidia has no shortage of customers who still see value in accelerating their capex spend.

Sovereign AI: Nations like Japan, France, and Saudi Arabia are spending billions to build “Sovereign Clouds” because they cannot rely on US tech companies for national intelligence. Deloitte estimates “Sovereign AI” will top $100 billion globally in 2026.

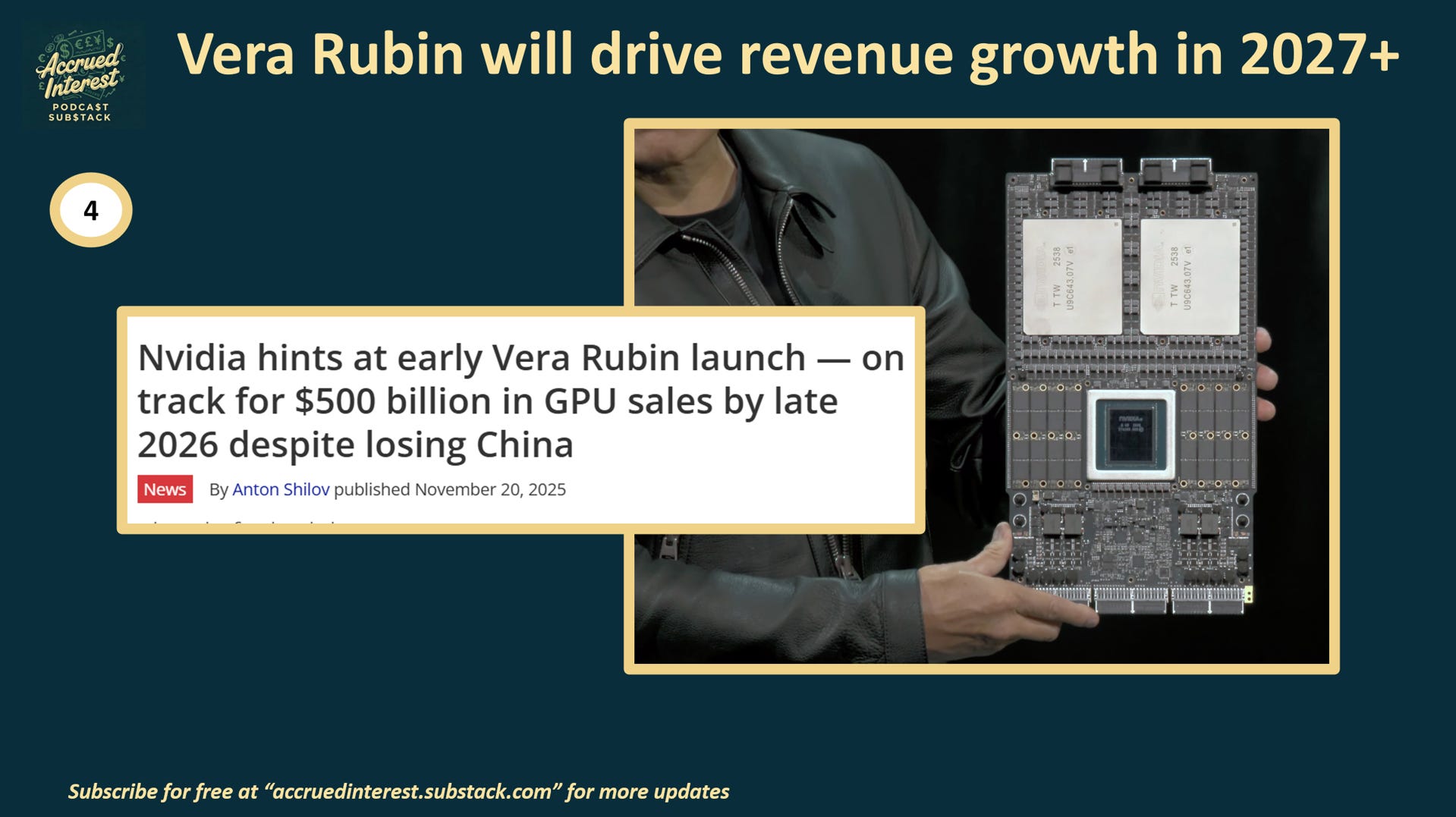

4. Vera Rubin will drive revenue growth in 2027+

The bear case often relies on the idea that competitors are catching up. “Google’s TPUs are good enough,” or “AMD is cheaper.” And while the market is obsessed with Blackwell (2025 tech), NVDA is already taping out its next-generation architecture, Vera Rubin, which will launch in late 2026 and drive 2027 revenue. This isn’t just a faster chip; it’s a platform shift that again leapfrogs Nvidia ahead of the competition.

3nm leap: Rubin moves from the 4nm process to TSMC’s 3nm process, delivering a projected 3x leap in performance-per-watt.

“Superchip” lock-in: NVDA is pairing the new Rubin GPU with its own custom Vera CPU. By selling an integrated “superchip” (CPU + GPU combined), they are physically evicting Intel and AMD from the server rack.

HBM4 dominance: Rubin will utilize HBM4 (High Bandwidth Memory), and supply chain checks indicate NVDA has already pre-booked the vast majority of HBM4 supply from Hynix and Micron.

Bears are worried about Google catching up to the H100. By the time Google optimizes for that, NVDA will be selling Vera Rubin, keeping the competition in the rearview mirror.

CONCLUSION

Despite Nvidia being one of the most covered stocks on the planet, you can still take advantage of investor doubts by going long the stock when its earnings multiple compresses.

In 2026, expect the NVDA 0.00%↑ critics to get louder. But successful investing is often about blocking out the noise and focusing on the few variables that matter. Valuation is reasonable, and arguably cheap, for such a high quality company. Nvidia’s moat is widening with the release of Vera Rubin which will help drive revenue growth for 2027 and beyond.

Like my pitch on Google, there are no bonus points for creativity. Sometimes the best compounders are hiding in plain sight.

If you found this interesting, do not forget to subscribe. And please come back for Day 12 of Accrued Interest’s 12 Days of Pitch-Mas! You can find prior days here:

Day 1 - Why Netflix Should Acquire Warner Bros. NFLX -1.49%↓ , WBD -0.24%↓

Day 2 - Why Paramount Skydance Won’t Win Warner Bros, PSKY 0.07%↑

Day 3 - No Bonus Points for Creativity—Just Buy Google, GOOGL 0.56%↑ , GOOG 0.48%↑

Day 4 - Nexstar + Tegna: Capped Upside and Regulatory Risk, NXST -0.85%↓ , TGNA -0.77%↓

Day 6 - Why Disney Stock Will Underperform in 2026, DIS 0.50%↑

Day 9 - Why Duolingo Will Underperform in 2026, DUOL -0.52%↓

Day 10 - Why Pinterest Will Underperform in 2026, PINS 0.00%↑

-Accrued Interest