US-Iran Ceasefire, Rigatoni Capital Interview, and Nintendo's IP Illusion (Accrued Interest Update 4-8-2026)

The market is breathing a collective sigh of relief today with the news of a two-week US-Iran ceasefire. It removes a massive geopolitical overhang that has been suppressing sentiment. But while the headline-readers exhale, I am using this drop in volatility to look under the hood. Today, I am explaining how to position yourself during this macro pause, highlighting my latest deep-dive interview with Rigatoni Capital covering Meta, Netflix, and AppLovin, and exploring why I fear investors are getting fundamentally lazy about Nintendo’s box office success.

Please subscribe to read the rest of the Accrued Interest Daily Update - for April 8, 2026.

Note to Readers: I am aggressively expanding my publishing cadence to match the velocity of this market. My objective is to grow Accrued Interest into a premier TMT research platform for value investors, delivering a high-alpha mix of both FREE and PAID intelligence. These updates will eventually transition behind a paywall; I urge you to subscribe now to lock in uninterrupted access and secure preferential pricing before the window closes.

A) Trading the US-Iran Ceasefire Requires Honesty About What You Do Not Know

One of the most powerful lessons I have learned trading the markets for over 20 years is that you have to be honest with yourself about what you don’t know. I am more bullish about the market today than I was yesterday because it is clear that the President does not have the intestinal fortitude to see the S&P 500 stay down. While the tail risk of nuclear war appears to be off the table, I want to remind everyone that this pointless war caused energy prices to spike all over the world and there is still a cost to be paid for all that - even if it does not show up in your portfolio.

Most of us assumed the most likely ending to this situation was TACO, (President Always Chickens Out). To give these numbers some context, the S&P 500 entered 2026 following a close of 6,845.50 on December 31, 2025. Amidst the peak uncertainty of the conflict with Iran, the real intraday low for the year occurred on March 30, 2026, when the index touched 6,316.91. This represents a total year-to-date intraday drawdown of -7.72% from the 2025 year-end close.

While the market fell more than -7% at its worst point, things began to turn around immediately afterward. The “fog of war” began to clear in early April as de-escalation hopes grew, culminating in the two-week ceasefire.

By the market close on April 7, 2026, the S&P 500 had recovered to 6,616.85, effectively cutting its YTD loss to roughly -3.3%.

So while the market is ripping higher today, realize that the market is basically back to where we were at the beginning of the year in aggregate.

To be clear, I do not think the U.S. will have a recession. The American consumer has shown that they are wealthier than they care to admit, and while higher prices sting, consumers are still spending. As a fundamental analyst, I am going to focus on what people DO with their money and not what they say. Do not get distracted by the relief rally. This is the exact window to identify fundamentally mispriced assets and evaluate true business drivers while the rest of the Street is busy trading the news cycle.

B) My Rigatoni Capital Interview Reveals What the Market is Missing on META, Netflix & AppLovin

I am excited to announce that my new interview on the Rigatoni Capital podcast is officially live! I got into the weeds on the structural shifts happening across the media and ad-tech landscape. You can watch the full interview on YouTube here: “META, Netflix & AppLovin: What the Market Is Missing | Simeon McMillan”.

Netflix, NFLX 0.00%↑ : Uncertainty is your friend because the market is mispricing the Warner Bros. Studio integration, and the recent Sony pay-one deal is a massive hidden catalyst.

Meta META 0.00%↑ : Decoding the CapEx panic reveals that Mark Zuckerberg has earned the market’s trust to spend, and massive, under-the-radar monetization buckets are forming in WhatsApp and AI agents.

AppLovin APP 0.00%↑ : The constant barrage of short reports is just noise, and the underlying earnings engine continues to compound as SMBs ramp up retail spend in Q2.

It is always a pleasure speaking with Colin. Please check him out and follow Rigatoni Capital.

Relevant Accrued Interest Articles to Read:

2026.03.27: Back to the EBITDA: Decoding Meta’s $1,116 Executive Playbook

2026.03.25: Zuckerberg’s Middle-Age Metabolism: Trimming Fat to Fund Superintelligence

2026.03.23: The Victor of the Streaming Wars: Why Netflix is a $120 Stock

2026.02.13: AppLovin ($APP) Q4-25 Earnings Review: The “Cash Machine” vs. The Market Fear

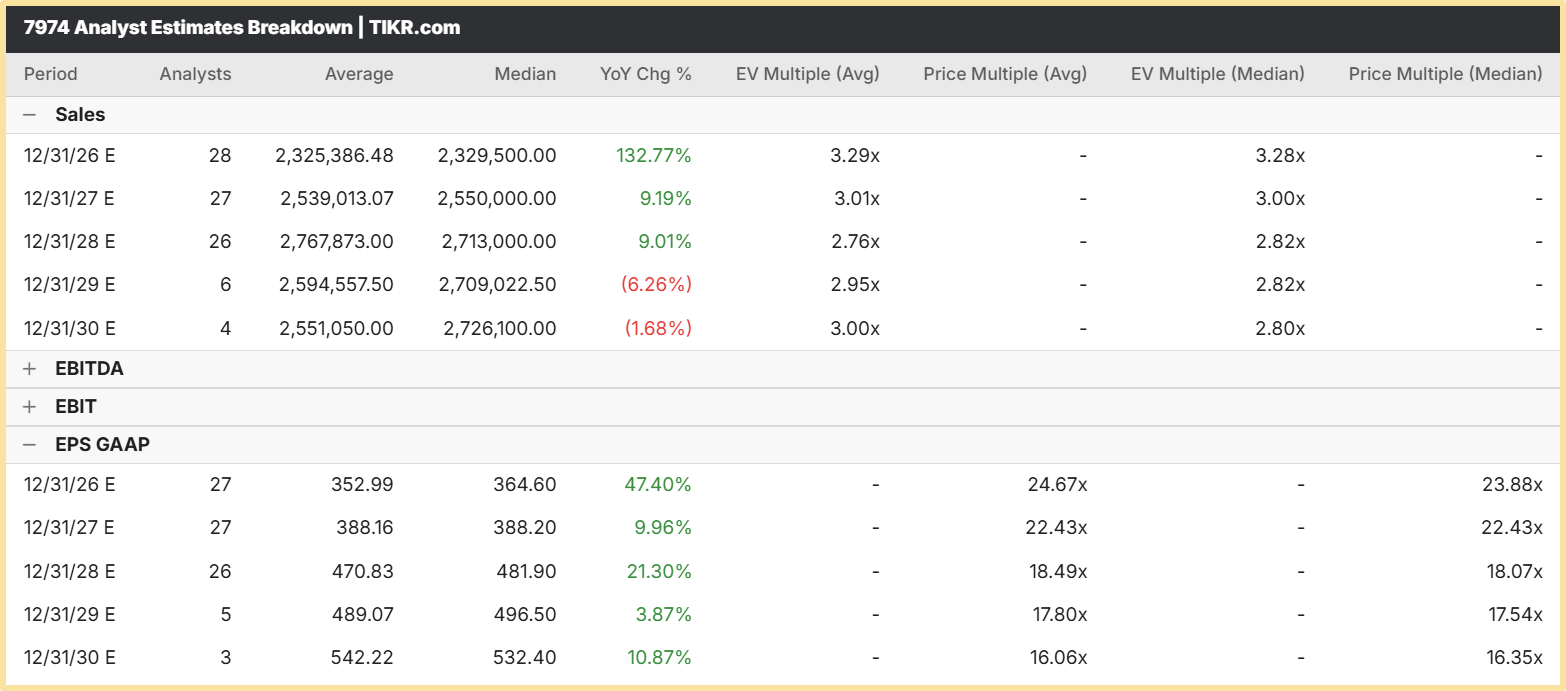

C) Nintendo’s ($NTDOY) Box Office Success is a Work-in-Progress (WIP) “Halo Effect” Reality Check

I went to see The Super Mario Galaxy Movie last week. It is a massive, undeniable hit. However, I am using this Daily Update to share my WIP thoughts because I am seeing a lot of lazy analysis from value investors and Substack writers who assume that cool movies automatically equal a higher stock price.

Let’s look at the actual numbers. Nintendo (Japanese Ticker: 7974) is currently trading at roughly 25x 2026 GAAP EPS and 23x 2027 estimates. While the console cycle isn’t as lumpy as it historically was, 25x is absolutely not cheap.

As I described in my article last month on The Pokémon Theory of Media Investing - when I look at a new stock, I want to get a sense of whether there is a mispricing in the earnings estimates, the earnings multiple, or both. This situation looks like if there is upside, it would need to come on the earnings side. As a rule of thumb, I typically use a hard ceiling of around 30x tops for the multiple on a “high-quality” company. For me to believe a stock is worth more than 30x, I need to have conviction that consensus earnings expectations are materially too low. In Nintendo’s case, I’m not quite there yet.

A common error in evaluating media companies that put out theatrical releases - is conflating the correlation between gross box office receipts with corporate net income. Nintendo co-financed the original 2023 Mario film with Universal Pictures and utilized Illumination for physical production. To model the actual cash impact to Nintendo, I must run the original film’s $1.36 billion global gross through a standard studio ultimate profit model.

Assuming a blended 55% domestic and 40% international rental yield, that leaves about $600 million in net theatrical rentals returning to the studios. Adding $150 million from home entertainment and $100 million from pay TV licensing brings total net studio revenues to $850 million. From there, I subtract a $100 million production budget, $150 million for global Prints & Advertising, $60 million for backend participation, and $40 million for overhead and interest.

This leaves a total net profit pool of $500 million. Assuming a highly favorable 50/50 split with Universal, Nintendo’s ultimate take-home profit from a top-3 all-time animated film is approximately $250 million. For a company generating $10 billion to $12 billion in net sales and holding over $15 billion in cash, a $250 million cash injection spread over 18 months of film accounting statements represents less than 3% of total revenue. It is highly profitable on a unit basis, but immaterial to the broader enterprise valuation.

According to TIKR, consensus expects revenue to grow about 9% YoY in both 2027 and 2028. I do not have a strong view on whether or not that is too low or too high, but I acknowledge there are other issues at play here.

Backwards compatibility complicates the software attach rate: It is difficult to model the video game cycle when the console life cycles get longer and longer. The Switch 2 is different from past cycles because it is the first Nintendo game console that is backwards compatible to the prior system. In past cycles when a new Nintendo system came out, none of the old games worked. Now you can still play Switch 1 games, creating uncharted territory for forecasting new software sales.

Post-COVID normalization limits the permanent gaming baseline: Nintendo now has more online sales than it did before, acting as a laggard to the industry in this way, but also we are now more than 5 years after COVID. The boom in gaming subsided and did not lead to a permanently higher pace of gaming.

The AI boom creates a component cost elephant in the room: How much can Nintendo pass on the cost of more expensive components for the Switch 2, most notably higher memory prices due to the AI boom?

The MCU fallacy proves movie success is rarely replicable: A true value investor must take into account all of these things about Nintendo. It is not simply a matter of cool movies resulting in a higher stock price. It is far from certain that a third Mario movie would perform as well, and how long it would take to come out. And this movie tells me really nothing about how a Zelda (announced in development), a Donkey Kong, Star Fox, or any other movie would do. The success of the Marvel/Disney MCU was truly 1 of 1. Many companies, such as DC (Warner Bros) and Hasbro with Transformers, thought they had scalable cinematic universes and it did not pan out.

Conclusion: Fundamentals Dictate Outcomes Over Fantasy Narratives

Whether it is looking past geopolitical headlines, ignoring short-seller noise on ad-tech, or doing the actual gross-to-net math on a Nintendo movie, the core philosophy remains the same: follow the growth in intrinsic value, not the headlines.

-Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.