Same Script, Different Cast

Is $WBD & $PSKY (2025) the sequel to $DIS & Fox (2017)?

Given the news that Paramount Skydance ($PSKY) is preparing a bid for all of Warner Bros. Discovery ($WBD), I wanted to offer some preliminary thoughts. This article presents my initial impressions of this evolving M&A situation and is not intended to be the definitive statement.

Here are 7 points to consider regarding a potential WBD/PSKY merger:

1) Investors are explicitly factoring into their analysis the fact that PKSY’s CEO, David Ellison, is the son of Larry Ellison, the 2nd richest person in the world.

Some investors believe that PSKY 0.00%↑ will make aggressive acquisitions in the coming years due to the CEO's significant wealth, enabling a buying spree. Bulls are willing to hold the stock even if earnings decline, prioritizing management's long-term vision over current financial results.

You do not have to look hard to find a ton of headlines like these:

Over at Business Insider, they are just saying the quiet part out loud - “Larry Ellison's $100 billion day reminds us why David Ellison could buy Paramount”.

However, it is imprudent to base investment decisions solely on the assumption that a wealthy individual will perpetually rescue a company from mediocre performance. While fervent shareholders who believe in a CEO's vision can prop up a stock in the short term, as seen with Tesla TSLA 0.00%↑ , this dynamic is not sustainable.

The stock price will always *eventually* reflect the intrinsic value of the business. As the saying goes, "the stock market in the short-term is a 'voting machine,' but in the long-term it is a weighing machine."

If the Ellison family and the PSKY board were to offer an all-cash takeover bid for WBD after years of poor execution, it would be advisable to accept the deal.

2) The proposed merger of Warner Bros. Discovery and Paramount Global bears a striking resemblance to Disney's acquisition of 20th Century Fox and most of its affiliated cable networks.

When it comes to large cap media strategy, there is nothing new under the sun. Any and every strategy has been tried already with both WBD and PSKY - including doing splashy M&A. I think the M&A deal most like today is Disney’s 2019 acquisition of 21st Century Fox.

Deadline: Sizing Up a Possible Paramount-WBD Merger, Hollywood Wonders If This Episode Is a Repeat

The prevailing rationale, then as now, centered on the belief that Disney DIS 0.00%↑ could enhance its competitiveness against Netflix and other digital streaming services by rapidly achieving significant scale. This merger was predicated on the idea that owning the most "valuable" content would enable the combined entity to maximize its intellectual property throughout the entire media distribution chain.

The acquisition of Fox is widely regarded as a disappointment, if not a complete failure. It is noteworthy that what was once Disney's largest acquisition is no longer considered the strongest aspect of its investment strategy, merely five years later.

The Wrap: Did Disney Buy a Dud with Fox? The $71 Billion Deal Is Weighing Bob Iger Down

By 2025, Disney investors have shifted their perspective, no longer viewing "bigger as inherently better" when it comes to media assets. Instead, Disney optimists believe that the company's theme parks, cruises, and other live experiences represent the healthiest segments of the business.

Hollywood Reporter: Disney Bets $60B Its Parks Will Power the Future

Consequently, Disney is no longer focused on pursuing low-margin growth through the expansion of Disney Plus and its other streaming services.

3) The audience decides for themselves what they want to watch.

While money can acquire content assets (studios, networks, shows, talent), it cannot buy a true audience. Acquiring subscribers is different from gaining legitimate fans who will consistently consume content.

Even with vast marketing budgets, paid endorsements, and industry awards, an audience cannot be forced to tune in if they lack interest. Simply combining media assets does not guarantee sustained audience engagement.

The combined WBD / PSKY will have a lot of marketing resources at their disposal in a way that one could assume will be hard to beat. However, new company ownership of a channel does not automatically alter consumer media tastes based on boardroom decisions.

4) This deal does nothing to address the shift in attention to user generated content.

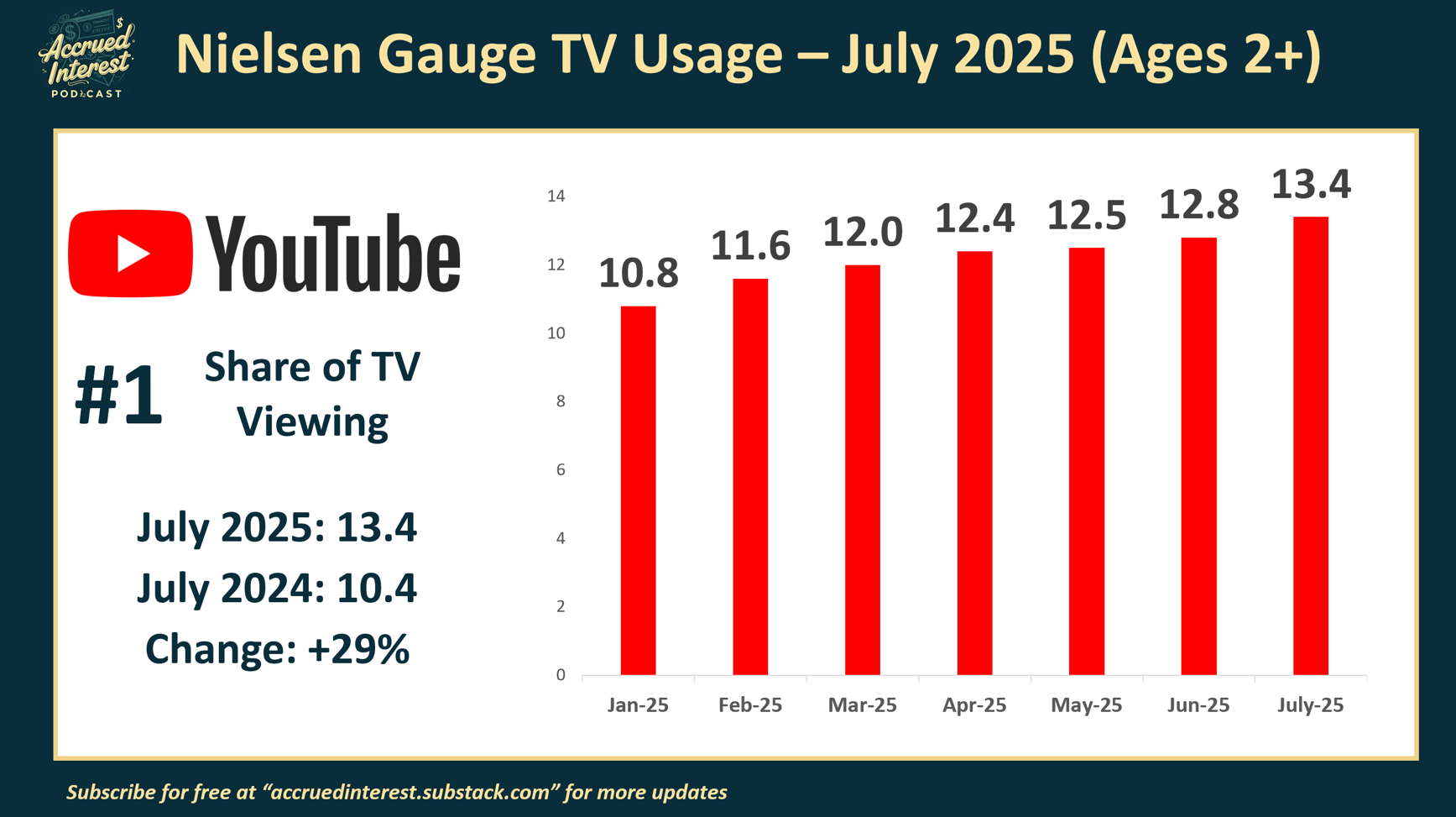

Legacy’s media’s biggest competition is from user generated content (UGC). M&A will not stop viewers from going to YouTube.

Content is king, but YouTube is eating everyone’s lunch. As I explained in my last update for July - Media Stock Insights from Nielsen’s July-25 TV Snapshot, YouTube is still growing viewing share even as Netflix share growth has plateaued.

From last month’s update:

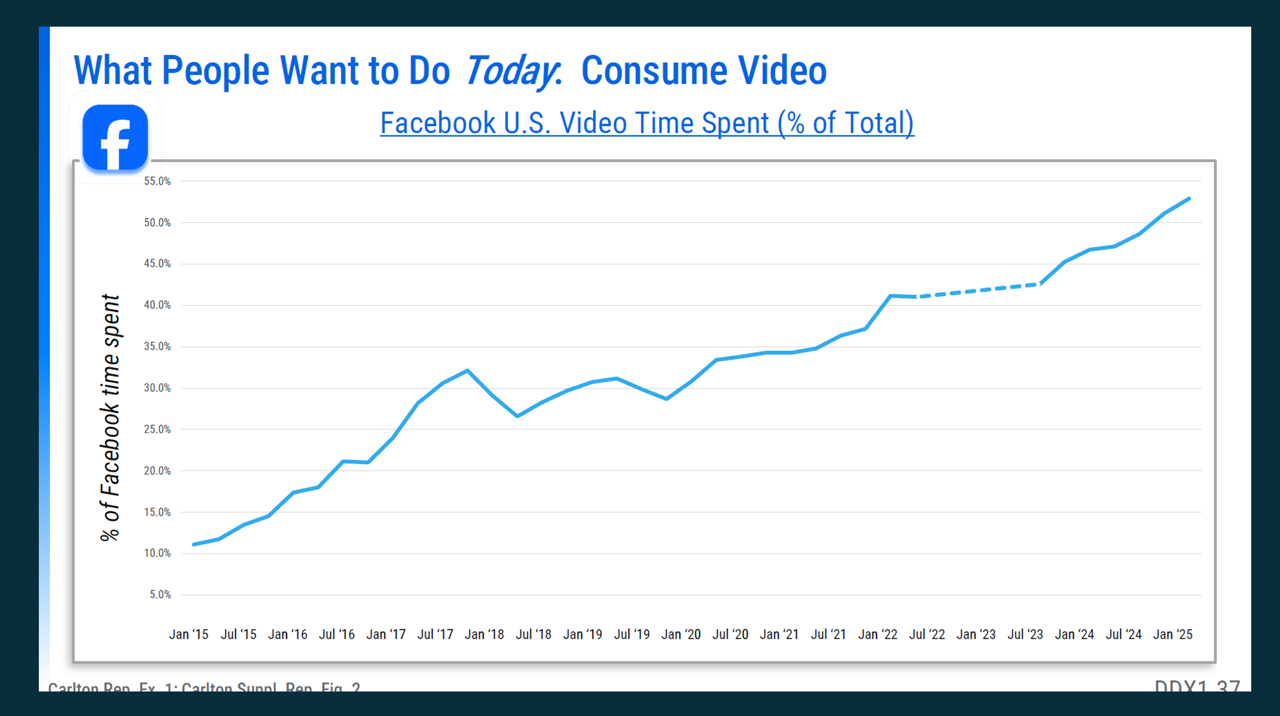

Also, watching TikTok, and other videos on Facebook META 0.00%↑ and other social media also counts as user generated content taking share away from TV.

In my article from April, “3 Things We Learned About Media Stocks from Meta vs. FTC”, I explained how “video is still gaining share in terms of time spent online, vs. static pictures or text”.

5) Financial engineering is not a strategy.

I consider creating cost synergies through M&A to be a form of financial engineering. From my article - Decoding the Nexstar M&A Deck ($NXST):

All the projections about the cost synergies are factually correct. My issue is that these large broadcast M&A deals never create the revenue synergies to drive organic growth. Financial engineering is not a long-term sustainable strategy.

WBD and PSKY bulls are raising their 2026 / 2027 EBITDA estimates based on massive cost savings that will occur once WBD is sold.

It is difficult for me to get too excited about cost synergies when an all-cash deal is going to leave the buyer with a high debt load and interest payments. Not to mention I have yet to hear any strategy on how to stem the declining ratings of the linear networks.

Let me be blunt — the press is being too accepting of the WBD and PSKY management narrative and is not scrutinizing the assumptions here.

Last week the WSJ reported that “Paramount Skydance plans to revitalize its cable networks, including MTV, Comedy Central and Nickelodeon.” Somehow “executives aim to revamp cable networks without increasing spending on them”.

I honestly do not know how it is possible to integrate two massive media conglomerates, stem the declines from the linear networks, all while cutting programming expenses. Management will have to show, not just tell.

6) 1 +1 does not always equal 2 when it comes to merging subscription services.

Investors overestimate the value creation of media M&A because they fail to think about INCREMENTAL subscriber growth.

After decades of U.S. media consolidation, most consumers subscribe to more than one TV/video service. It should be intuitive that a sizable number of subscribers to HBO Max and Paramount+ already subscribe to both services.

Therefore, 1 +1 does not necessarily equal 2 when you combine the subscriber bases for WBD 0.00%↑ and PSKY 0.00%↑ , because Paramount would be acquiring a lot of accounts they already reach today. This explains why revenue synergies are rarely mentioned as part of the investment case.

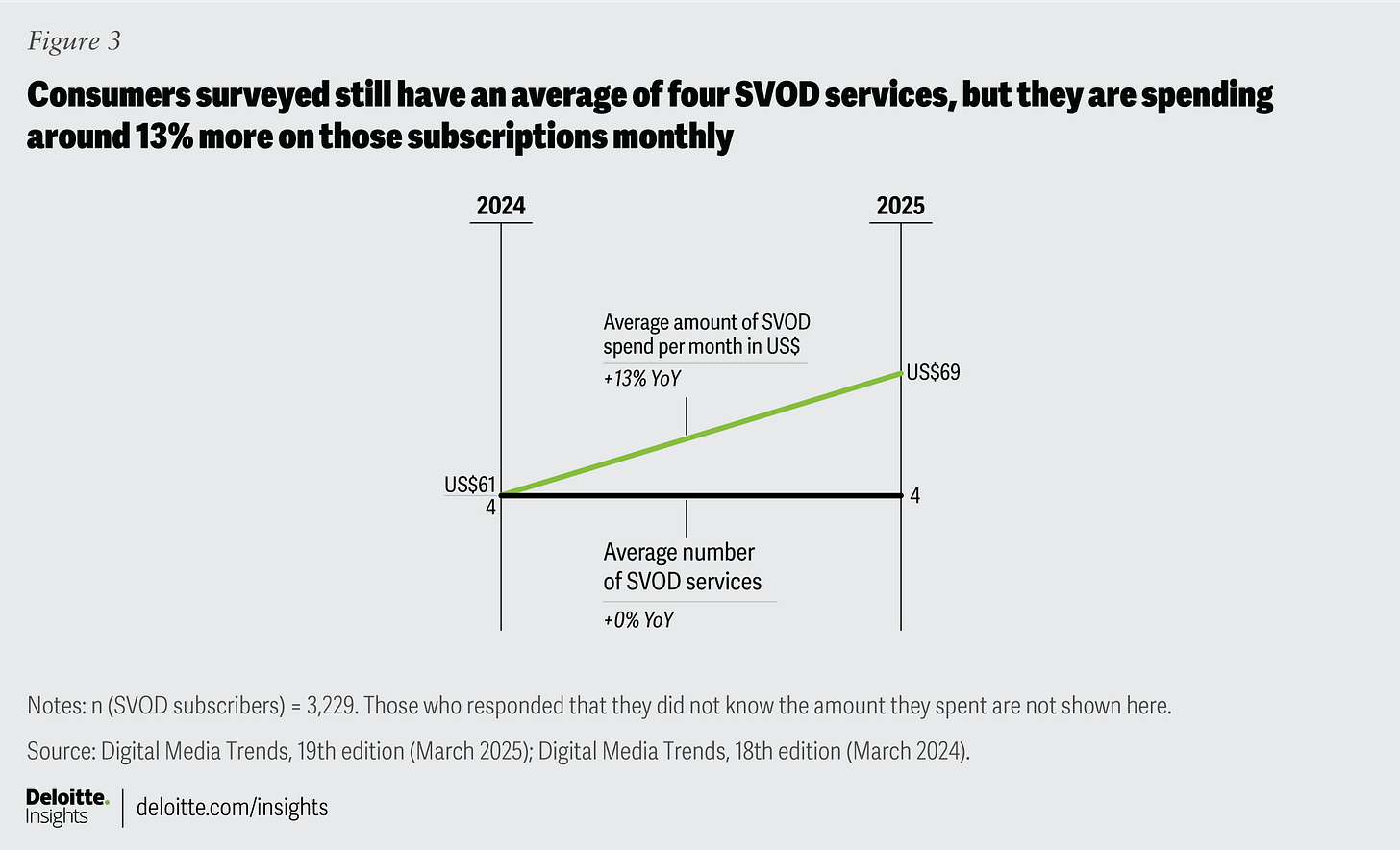

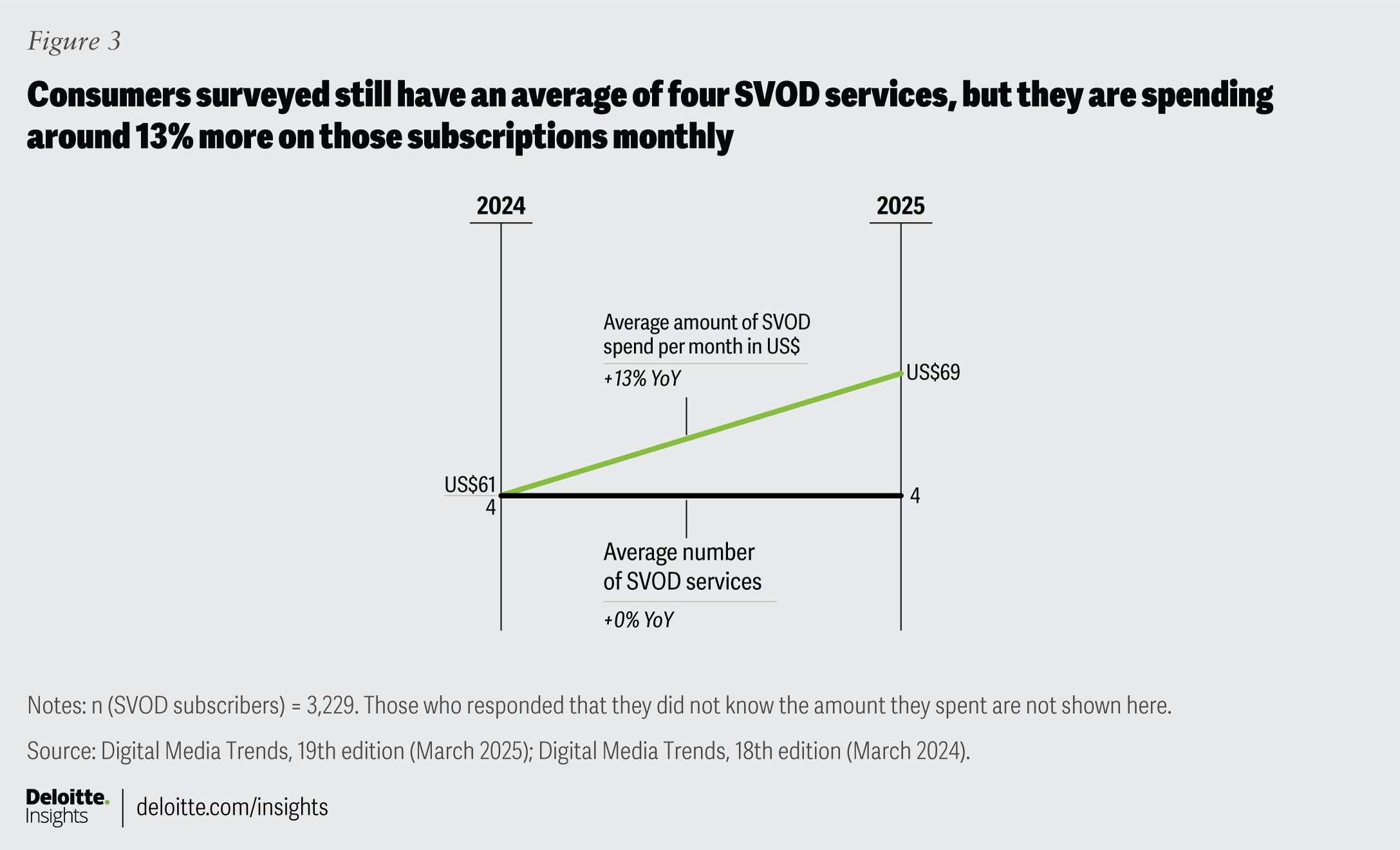

According to the Deloitte 2024 Digital Media Trends report, the average number of video-on-demand services in the U.S. has been stable at around 4 per consumer since 2020, on which they spent on average $69 per month.

Netflix NFLX 0.00%↑ has won already and is the standard “general entertainment” streaming service. Surveys have shown that consumers consider other streaming services complementary to Netflix.

Both HBO Max and Paramount+ are general entertainment streaming services. Paramount Skydance just recently made a big bet on UFC, but that has yet to take effect and does not matter in the short term. (See “UFC fighting is coming to CBS and Paramount+” from my article “Media Valuation Tracker Update – Week of Aug 12, 2025”.

7) The stock price of WBD and PSKY is going to be driven entirely by M&A speculation, not earnings reports, until a deal is officially closed.

I will be covering the strategy implications of this M&A saga and will keep focusing on the fundamentals because that is what we do here at Accrued Interest.

But until further notice, neither is going to trade based on their reported financials because at any given moment there could be a news alert about a deal happening. When, or if, that news comes is something that as an outsider one cannot reliably predict.

Neither of these stocks I would recommend to long-term investors with a time horizon for over a year. I do not like recommending short-term trades because they are taxed as ordinary income at a high rate, so keep that in mind if you are playing either stock for a short-term pop.

CONCLUSION

The track record for past deals like this is not great for the buyer. Remember to think critically for yourself and not blindly take what management tells you at face value. Just because Warner Bros. Discovery CEO David Zaslav wants a bidding war for his media giant, does not mean he necessarily will get it on his own terms.

Check out my piece from June (WBD Spin-Off: My Quick Take on the Announcement), where I made annotations on the WBD investor deck where they explained why the company was splitting into two.

Remember, the reason WBD was doing a spin-off was because no rational buyer would want to own BOTH Global Networks and the Streaming & Studios businesses. (See WBD investor deck below) If such a deal made all this strategic sense, it would have happened already.

The burden is still on PSKY to prove why they believe they can be successful with these assets after other owners have decided they were better off without them.

I will not be giving precise price targets going forward. WBD stock, in the short term, will be worth whatever the PSKY board decides to offer. But just know that if there is a risk of no deal, WBD stock could fall back down to $12, where it was before the latest M&A speculation came out recently.

I cannot in good conscious recommend either of these stocks because I do not see their financial situation (combined or individually) becoming materially better in two years. Doing an M&A transaction buys companies time because it allows them to fire large swaths of people quickly and lock in the savings. But these integrations also damage employee morale and distract people at all levels of both organizations from doing their day-to-day jobs on which the future of the enterprise rests.

Until I see credible evidence that this NewCo can grow organically faster than it did before, I will leave this trade to the gamblers. And should PSKY emerge as the winner of the WBD kingdom, it will also inherit a corporate enigma that no one else has yet been able to solve.

For investors looking for a stock they can hold for two years and forget about it, I would suggest looking elsewhere.

-Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.