Notes on AppLovin's Goldman Sachs Communacopia Talk ($APP)

Takeaways from the Tech Conference

Yesterday, AppLovin’s CEO and CFO presented at the 2025 Goldman Sachs Communacopia + Technology Conference held in San Francisco. Last night I shared on Twitter a mini-thread on my key takeaways which you can read here.

Today I want to do a deep dive of the event transcript to explain to you all why I have been pounding the table as an AppLovin bull ever since I started Accrued Interest.

Here are the top 8 quotes from the fireside chat and my thoughts on what it means for the stock. You can listen to a recording of the talk by going to AppLovin’s Investor Relations page link.

For new subscribers - welcome! Here are all my prior writings on APP 0.00%↑ from 2025.

Now for today’s update!

TAKEAWAY #1: AppLovin is a rapidly growing force in digital advertising, challenging Meta and other major platforms with significant ad spend.

Adam Foroughi, AppLovin's CEO, views Meta as their primary competitor. Given AppLovin's rapid growth, it is fair to say they are a significant force in digital advertising, challenging META 0.00%↑ , SNAP 0.00%↑ , and TikTok for advertisers' budgets.

As of Q1 this year (e.g., six months ago), AppLovin had already reached over $11 billion dollars in gross ad spend.

This figure represents the total advertising dollars spent on the platform, distinct from the net revenue reported in financials, which is calculated after publisher payouts.

For context, Foroughi noted that this gross ad spend was equivalent to the combined total revenues of Pinterest, Snap, and Twitter. Wow!

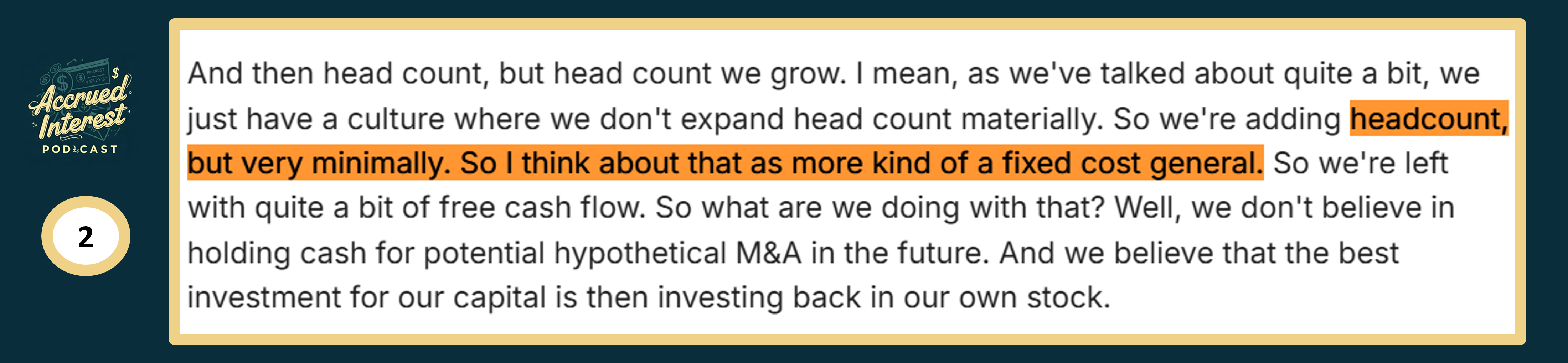

TAKEAWAY #2: AppLovin's lean operating model sets them up for sustained success.

Matt Stumpf, CFO of APP, emphasizes that the company's ability to grow revenue with minimal headcount is a significant competitive advantage.

This hyper growth in revenue without a proportional increase in full-time employees is rare in the tech industry.

In recent years, companies like Meta, GOOG 0.00%↑ , and AMZN 0.00%↑ have undergone multiple rounds of layoffs to correct for over hiring during the COVID-19 boom.

From a corporate finance perspective, it is important to highlight that layoffs can be very demoralizing for a workforce. APP's constrained hiring practices are a key reason its operating margins are unusually high and are likely to remain so, a topic that we will explore further.

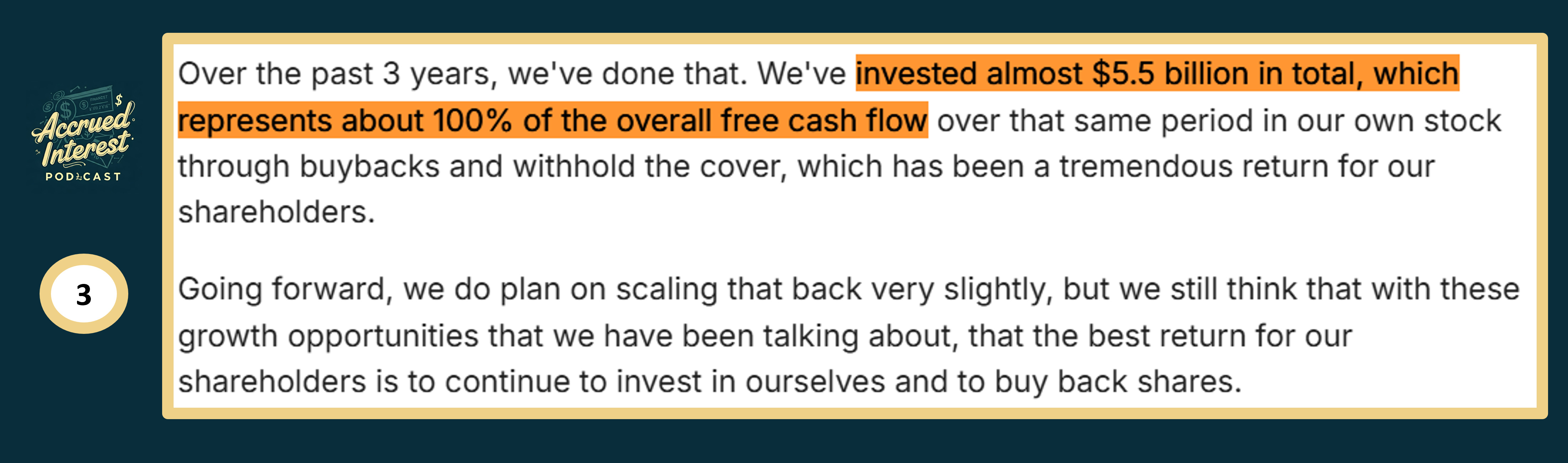

TAKEAWAY #3: Capital allocation prioritizes share buybacks during growth phase

What sets this company apart is its unique approach: it allocates all its excess free cash flow to share buybacks, even while experiencing rapid growth.

Typically, companies tend to repurchase their stock when growth has decelerated and profitable investment opportunities are scarce.

By prioritizing stock buybacks, Foroughi also indicates no immediate plans for significant mergers or acquisitions, signaling that buying back their own stock is considered the best investment opportunity.

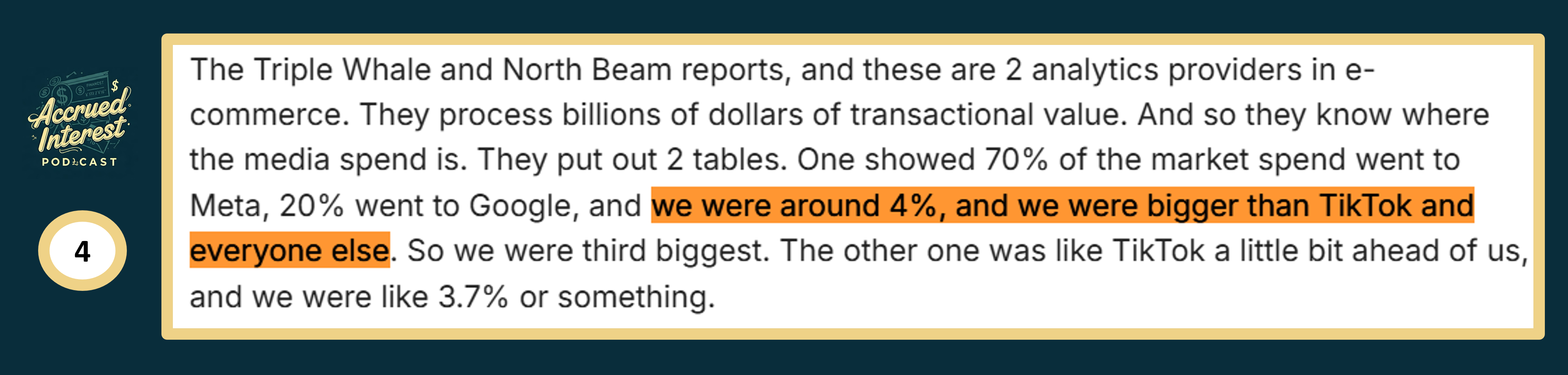

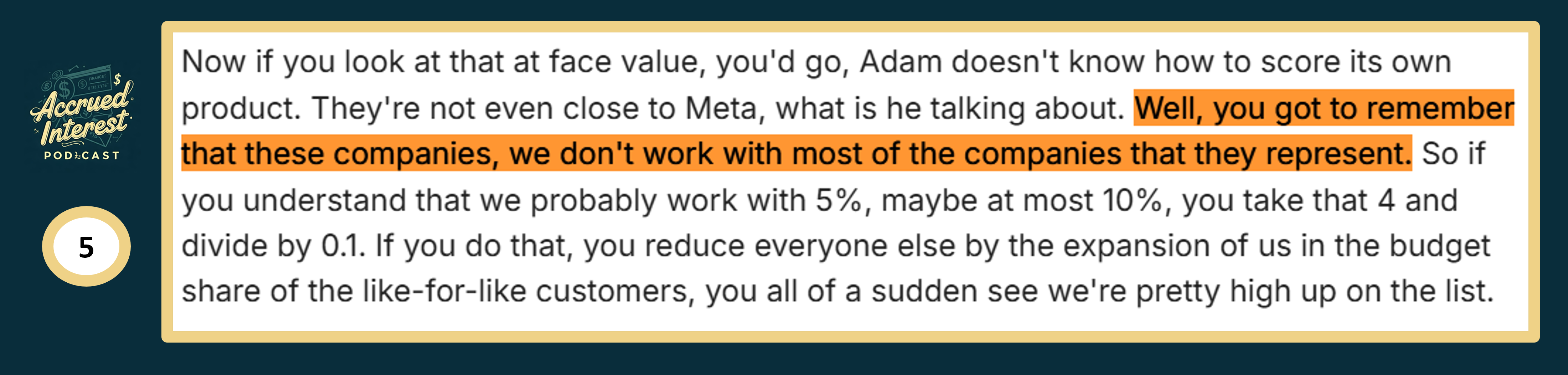

TAKEAWAYS #4 / #5: AppLovin's Underestimated Share and Growth Potential

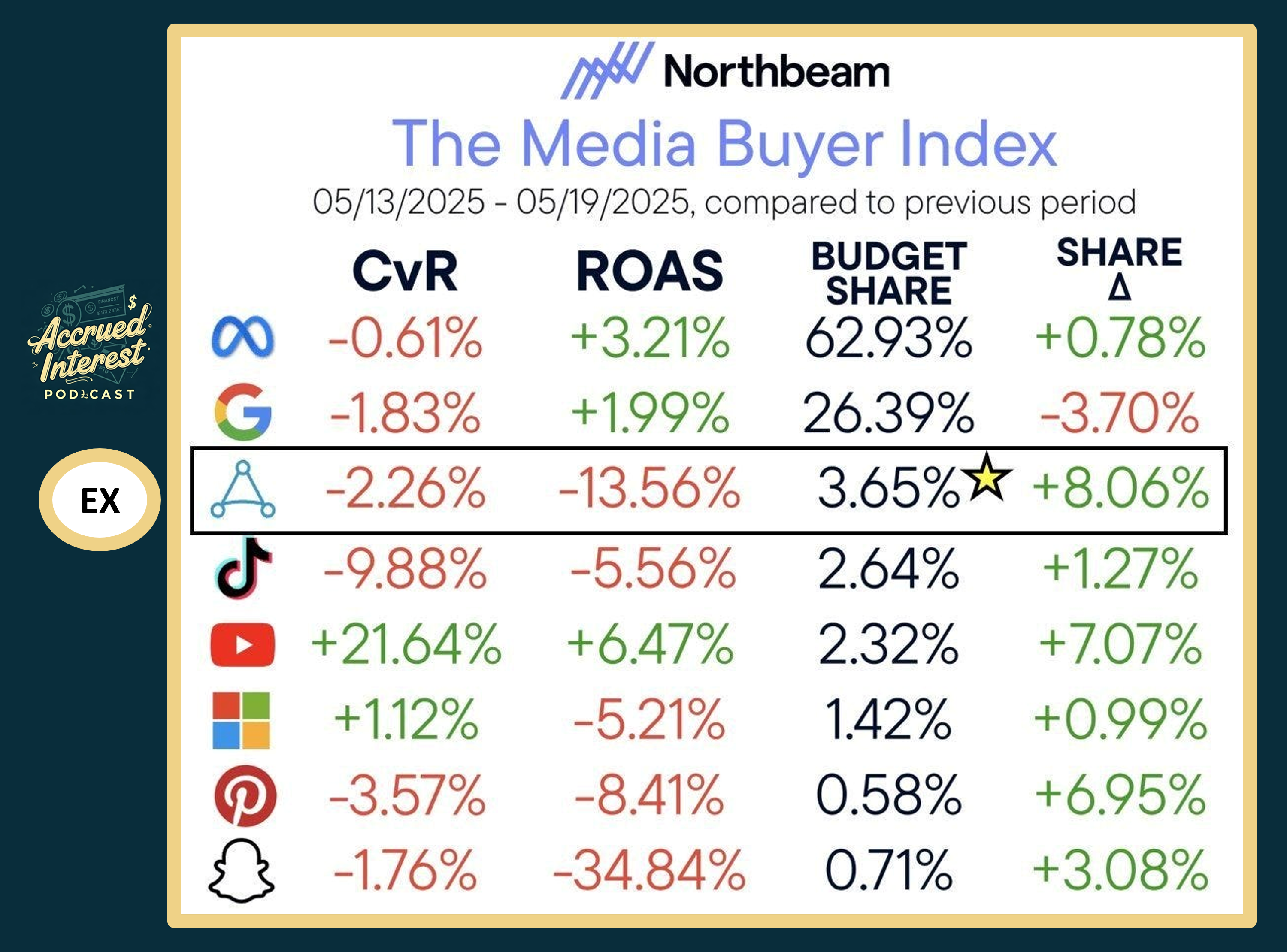

AppLovin's true strength is understated by reports from Northbeam and Triple Whale, which suggest a 3-5% budget share.

This is surprising because AppLovin only works with approximately 5% of Northbeam's customers surveyed.

Despite this limited client base, AppLovin STILL achieves a higher share of wallet than any company other than Meta or Google, surpassing competitors like TikTok, Pinterest, and Snap!

This reframing is crucial for investors to grasp AppLovin's potential for significant market share growth as they expand to more customers and geographies.

The ranking charts they reference, such as one from Northbeam posted on LinkedIn, clearly illustrate AppLovin's impressive performance. Here is an example of one below.

TAKEAWAY #6: Untapped Potential of In-Game Advertising for Gaming Publishers

AppLovin sees a significant opportunity in expanding advertising monetization among gaming publishers. Currently, most games rely on in-game purchases, which many gamers dislike. In-game advertising is less common, presenting a considerable growth area.

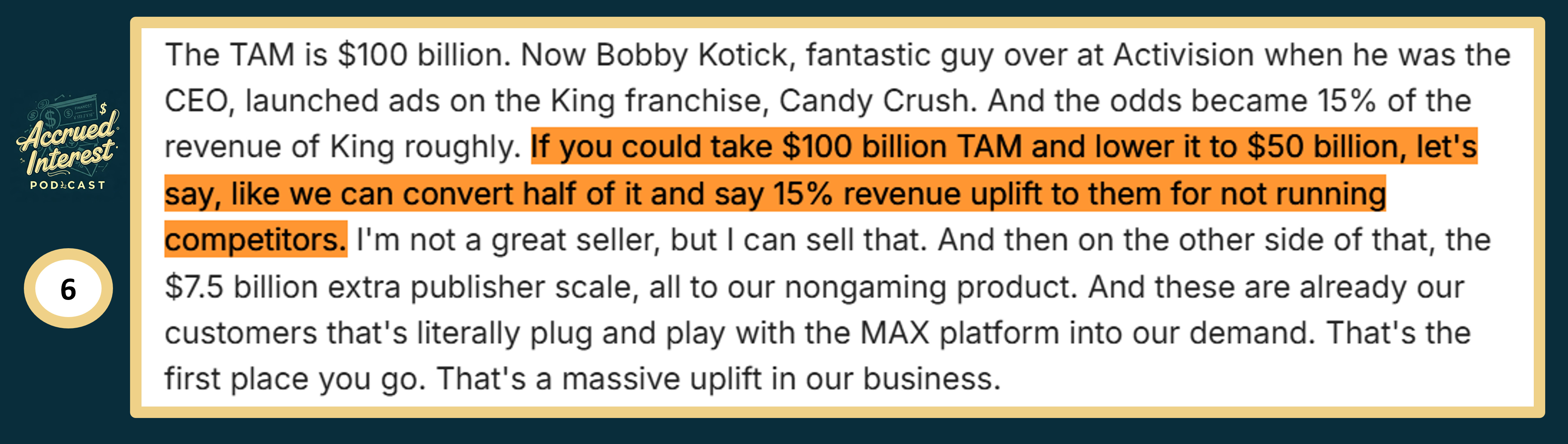

As an example, AppLovin cited how Candy Crush initially used only in-game purchases. After incorporating ads, advertising contributed 15% of their total revenue.

AppLovin estimates that enabling in-game advertising across more customer inventory could unlock an additional $100 billion in Total Addressable Market (TAM). This highlights the substantial revenue potential that game publishers are currently overlooking.

TAKEAWAY #7: Sustainable Margins and Future Free Cash Flow Generation

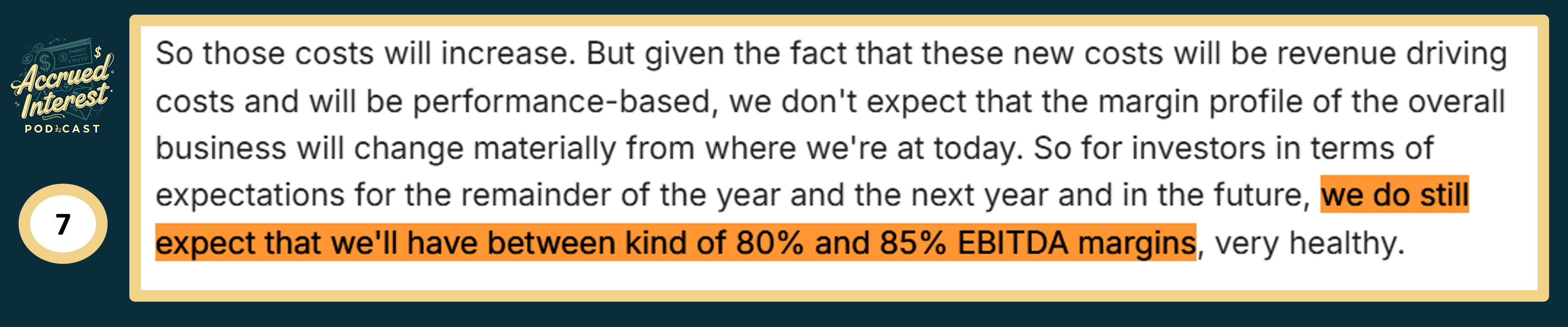

APP 0.00%↑ is expected to maintain high EBITDA margins of 80% - 85% due to its business model. The company considers employee costs to be fixed, having minimal impact from revenue fluctuations.

Datacenter costs represent ~10% of revenue, with additional new expenses attributed to ad campaign analytics and performance marketing.

Given that AppLovin converts over 50% of its EBITDA into free cash flow (FCF), the company is anticipated to be a significant FCF generator for the near future.

These strong margins are sustainable, and the stock will go higher.

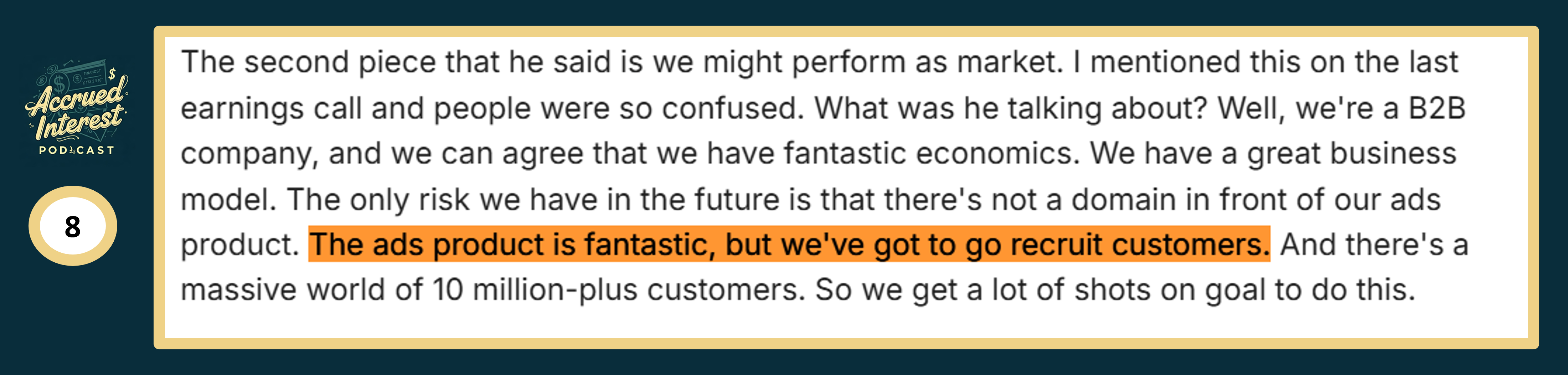

TAKEAWAY #8: AppLovin's Marketing Strategy for Customer Acquisition

AppLovin is about to start using performance marketing to attract new customers.

Unlike well-known entities such as Meta, Google, or TikTok, AppLovin lacks a widely recognized public domain name or website.

To significantly expand its customer base from "low thousands" to hundreds of thousands, and eventually millions, AppLovin requires substantial marketing.

They have even suggested that a Super Bowl advertisement could be a worthwhile investment in a few years to boost brand awareness.

Given the incredible profitability of their platform - I would agree!

CONCLUSION

Obviously, I do not love APP 0.00%↑ stock at $570 a share as much as I did closer to $320 back in January. But this is an amazing company that can still beat analyst expectations for 2026 and 2027 revenue.

If you already own AppLovin stock, I would maintain the position.

If you do not own any, I would buy a little, waiting for pullbacks to be more aggressive.

If you do not feel comfortable buying a stock that has run-up so much, just buy a low-cost S&P500 index fund. As of September 22nd, AppLovin will be added to the index.

-Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.