No Bonus Points for Creativity—Just Buy Google ($GOOGL)

12 Days of Pitch-Mas Day 3

Accrued Interest has been positive on Google all year before it was cool. Therefore, it should come as no surprise I am recommending Google as an Outperform for Day 3 of Pitch-Mas. Despite it being one of my top performing stocks for the year, the future still looks very bright for the company and I do not believe that all its earnings potential has been priced into the stock. Alphabet’s investments in innovative AI (Gemini 3.0), its conquest of the media landscape (YouTube), and the accelerating commercial viability of its autonomous driving technology (Waymo) position the company for resilient and long-term growth well past 2026.

1. Google Search and Gemini: AI Dominance Undeniable

For a while, everyone thought Google Search was going to lose ground, and that the company was just too slow to catch up in AI. But, with the successful launch and execution of the Gemini 3.0 models, Google has clearly shown they have superior capabilities, putting them right at the front of the AI race. Google is currently top two in AI technology, and they are NOT number two.

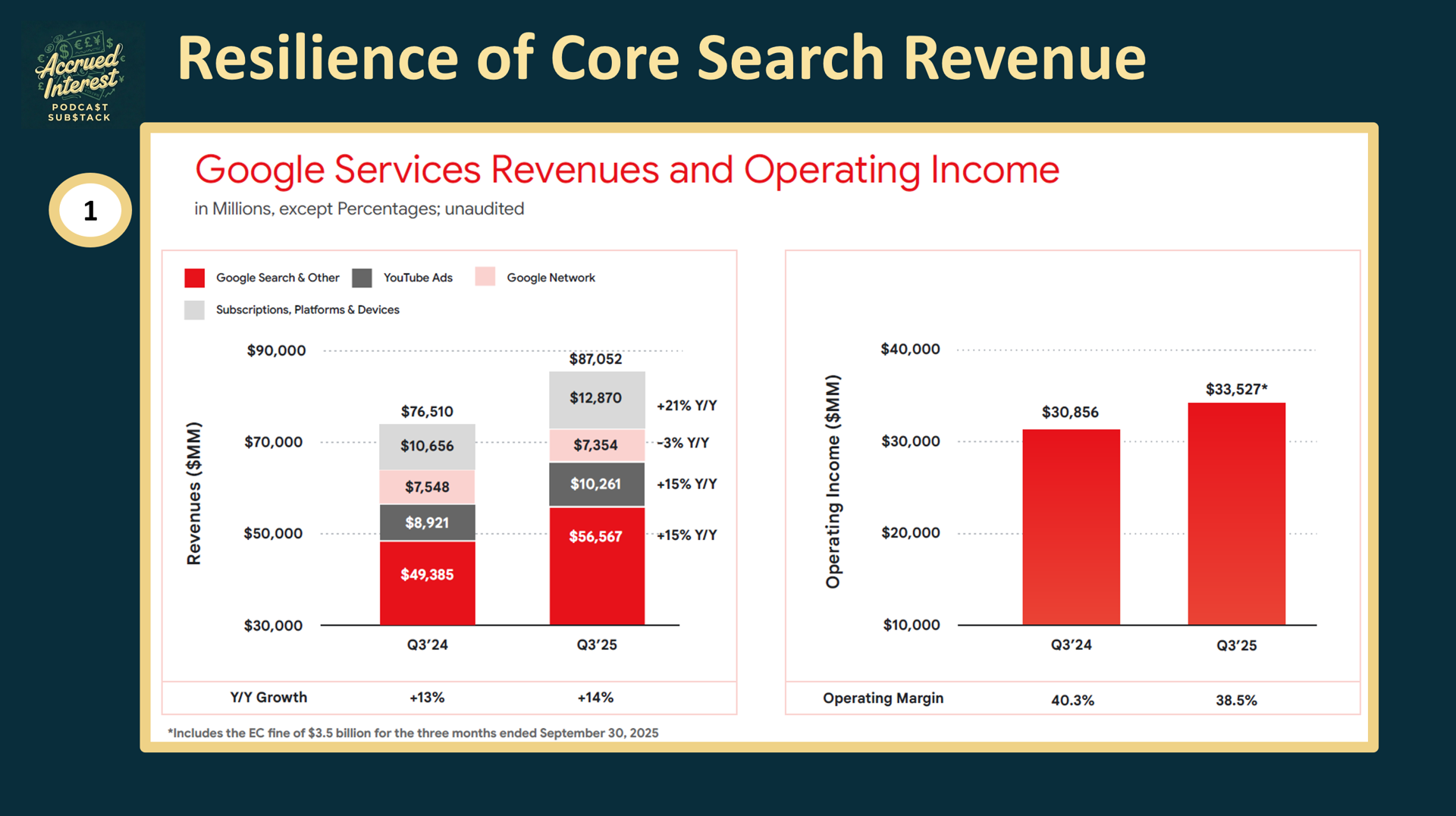

Resilience of Core Search Revenue: Contrary to fears of a “melting ice cube,” Search revenue growth has not been decelerating, growing +15% YoY for Q3-2025, maintaining its status as a robust core business. Google Search & Other revenue reached $56.6 billion in Q3 2025. It is incredibly impressive for GOOGL 0.00%↑ to be able to grow at a double digit rate from such a large revenue base.

AI Leadership and Technological Depth: Google is really establishing itself as a technical leader with successful model releases like Gemini 3.0 and the powerful Nano Banana Pro. They can do this because they use their own specialized hardware, like the 7th-gen Ironwood Tensor Processing Units (TPUs), which are custom-built for handling AI tasks on a massive scale. It shows they are committed to controlling all the tech needed to make their AI stand out.

Expanding the Total Addressable Market (TAM): Google’s AI features are enhancing Search. AI Overviews are projected to reach over 2 billion monthly users globally by late 2025 (up from 1.5B in mid-2025 and 1B in late 2024), projected to cover ~25% of the world’s population. These tools are encouraging new types of questions, significantly increasing user engagement with Search. This AI advancement is expanding search engines beyond text, allowing Google to use Search to find information in videos, images, and the real world.

Monetization Parity: Initial integration shows that AI Overviews monetize at approximately the “same rate” as non-AI Overview search, providing a healthy base for future growth and mitigating revenue reset risks. Advanced AI-powered tools like AI Max in Search are proving effective for advertisers, driving up to 14% more conversions.

2. YouTube: The Undisputed Media Titan

2025 was the “coming out year” for YouTube, demonstrating to investors and industry observers that it is the dominant global video platform, particularly on Connected TV (CTV). Having won the war for consumers’ time, YouTube is now moving aggressively to capture subscription revenue and leverage its massive scale to dramatically increase its negotiating power over legacy media companies.

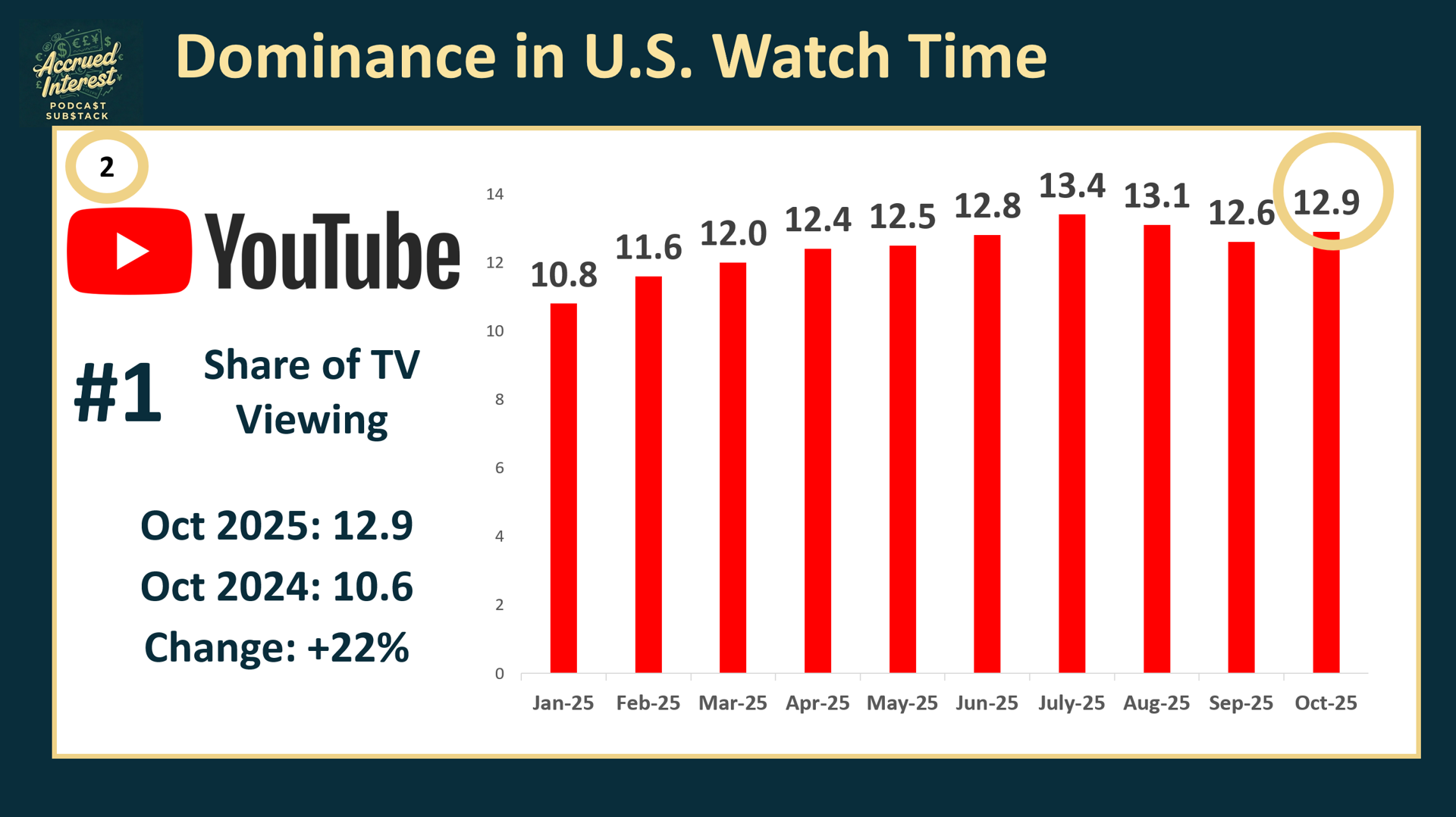

Dominance in U.S. Watch Time: YouTube is consistently ranked as the number one streaming platform in the U.S. by watch time, hitting a record high of 13.4% of total U.S. TV viewing by July 2025 (excluding mobile). This consistent growth, even from a high base, proves its accelerating traction against linear and subscription video-on-demand (SVOD) rivals.

Resolution of Shorts Monetization: Early investor concerns that Shorts (YouTube’s short-form video offering) would cannibalize revenue are dissipating. Google reports that Shorts in the U.S. now earn at least much revenue per watch hour, and arguably more, than traditional in-stream YouTube content, demonstrating that Shorts will “not dilute earnings”.

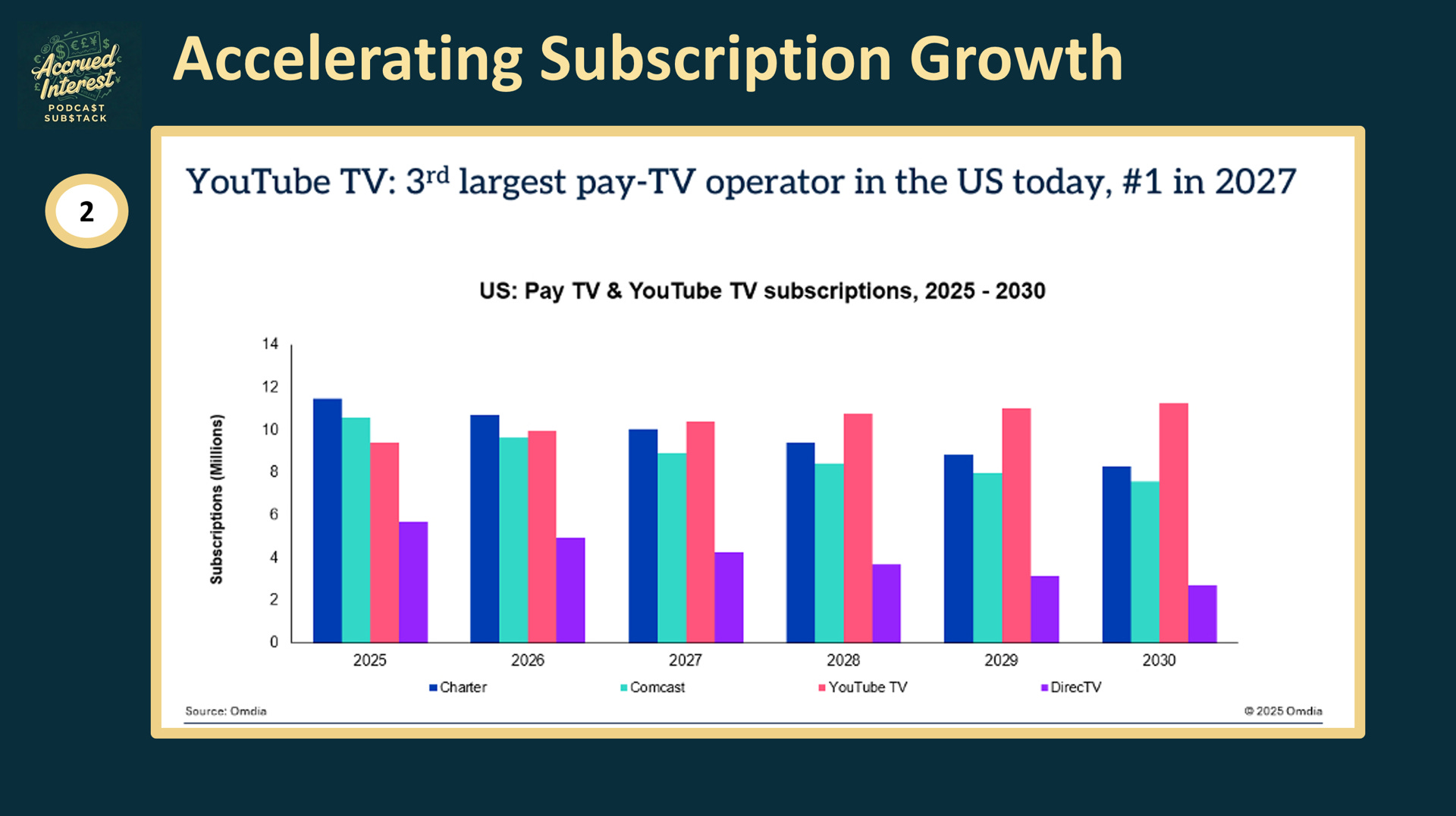

Accelerating Subscription Growth: YouTube’s subscription services (Music, Premium, and YouTube TV) are key drivers, contributing to Alphabet surpassing 300 million paid subscriptions globally by Q3 2025. YouTube TV is positioned to become the number one paid TV provider in the U.S., capitalizing on the decline of traditional cable.

Strategic Sports Content Leverage: Acquisitions like the NFL Sunday Ticket package provided access to highly valuable U.S. television inventory, anchoring consumption and making it an easier sell for other media items. The recent carriage dispute resolution with Disney, DIS 0.00%↑ provided YouTube TV users access to all ESPN live sports content directly within the app, solidifying a win that boosts its long-term product desirability.

Direct Attack on Cable Subscribers: YouTube TV plans to launch genre-specific linear streaming packages (including a Sports Plan) in early 2026. This should be viewed as a “code red” for subscale competitors like Fubo, FUBO 0.00%↑ and represents a massive DIRECT attack on the lucrative subscriber fees held by legacy cable owners like Disney DIS 0.00%↑ , Comcast CMCSA 0.00%↑ , Paramount Skydance PSKY 0.00%↑ , and others.

3. Waymo: Hidden Value and Autonomous Future

I think Waymo, which is lumped in with Alphabet’s “Other Bets,” is seriously underestimated in GOOGL’s stock price right now. It is the clear global leader in self-driving tech, and it is long past the “proof of concept” stage. Waymo is rapidly expanding its commercial services and making smart alliances, which tells me it is absolutely going to be a major player as self-driving taxi services go global.

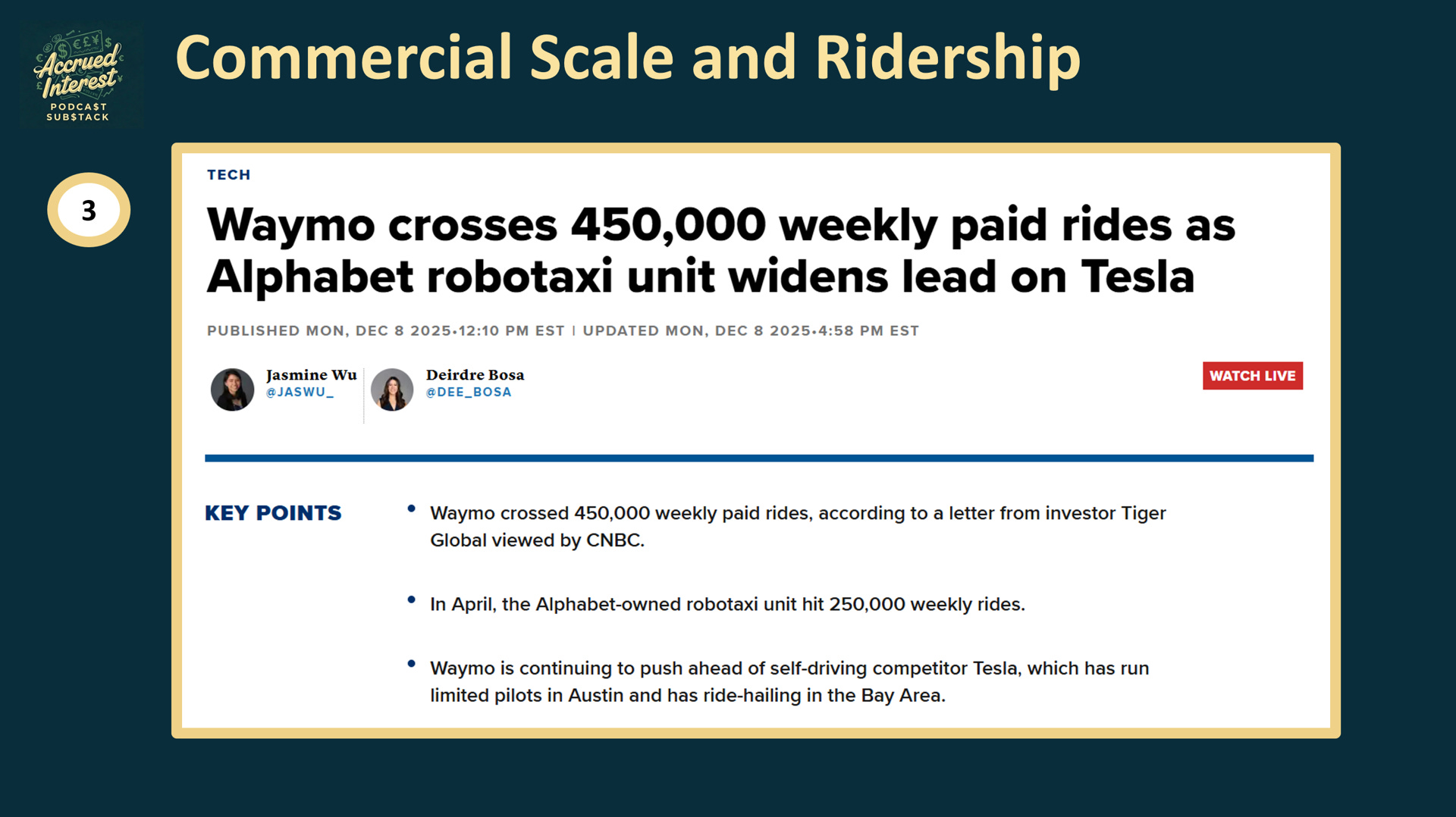

Commercial Scale and Ridership: As of December 2025, Waymo robotaxis have completed 14 million trips throughout the year, which is triple the number of fares from 2024. This operational achievement positions Waymo far ahead of competitors, such as Tesla.

Strategic Partnerships Over Competition: Instead of engaging in unnecessary competition, Waymo is intertwining its “fates” with Uber, partnering for commercial launches in major new markets like Austin and Atlanta. This approach recognizes that the companies are “complementary services” where Uber provides the user platform and Waymo provides the autonomous technology, allowing both to avoid the capital-intensive business of fleet management.

Aggressive Geographic Expansion: Waymo is expanding quickly beyond its initial core markets (Phoenix, San Francisco, Los Angeles). The company is initiating groundwork for Miami in 2026, and targeting international expansion (Tokyo, London in 2026).

CONCLUSION

Let me be clear that I do not expect Google’s massive 65% year-to-date performance to repeat in 2026. However, at Accrued Interest I want to focus on fundamentals and not try the time the market. For all the reasons I have laid out above Google has many fantastic businesses under its purview, each with its own unique set of positive catalysts to further realize value in 2026 and beyond. In investing you do not win bonus points for creativity! So, while it is not my top pick, I feel secure recommending Google having a permanent place in your portfolio.

If you found this interesting, don’t forget to subscribe. And please come back tomorrow, for Day 4 of Accrued Interest’s 12 Days of Pitch-Mas!

-Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

Strong thesis on Google's fundamentals. The Waymo partnership strategy with Uber is especially smart becaues it sidesteps the fleet ownership burden while still capturing the autonomy upside. Most analysts are sleeping on how valuable that optionality is compared to Tesla's vertically intgrated approach. Genre-specific YouTube TV packages in 2026 could be a real inflection point for subscription growth too.