Meta's Muse Spark Rollout, OpenAI's $100B Ad Dreams, and Uber's Latest Robotaxi Deal (Accrued Interest Update 4-9-2026)

Meta stock is rising sharply today as the company unveils its first natively multimodal AI model, signaling that its aggressive AI bets are beginning to deliver tangible results. Meanwhile, OpenAI is revising its ad sales forecasts to project a near-flawless five-year sprint to the top of the advertising world, and Uber is quietly securing its future intrinsic value without blowing up its balance sheet. Let me break down the mechanics of what is actually happening behind these headlines and what it means for our portfolios.

Please subscribe to read the rest of the Accrued Interest Daily Update - for April 9, 2026.

Before I dive in, a quick reminder: Accrued Interest’s daily updates will soon be moving behind a paywall. Please subscribe today to ensure you don’t miss out on my ongoing TMT stock analysis, media industry commentary and deep-dive financial breakdowns.

A) Meta’s latest cloud deal and “Muse Spark” model release validate my core bullish thesis.

Meta stock is popping today, up +3% to $633, following the dual announcement of their new “Muse Spark” model and a massive $21 billion cloud capacity deal with CoreWeave. If you have been reading Accrued Interest, you know my ongoing thesis: Meta is a market-leading growth stock that the market has occasionally mispriced due to short-term panic over capital expenditures.

Meta has officially announced a $21 billion agreement with CoreWeave to secure AI cloud capacity all the way through 2032. Simultaneously, they have taken the wraps off “Muse Spark,” which is the first natively multimodal AI model to emerge from their highly compensated, elite Meta Superintelligence Labs (MSL) team. This represents a significant strategic pivot for the company. In a departure from their open-source Llama heritage, Meta is keeping Muse Spark strictly proprietary. This signals a fundamental shift from treating AI as an open ecosystem play to recognizing it as a core, proprietary margin-driver that must be fiercely protected.

I look at this CoreWeave deal as a defensive play. Meta is basically locking up the compute power they need for the next decade. Sure, it means CapEx is going to stay high for a while, but here is the difference: Meta has the scale to pull it off. Meta can spread those massive costs across billions of users in its core media business without breaking a sweat—something smaller tech startups just can’t do.

Artificial intelligence is fundamentally upgrading the invisible plumbing of Meta’s massive advertising machine.

Meta’s massive capital expenditures are a calculated bet by Mark Zuckerberg. Management clearly sees these AI investments directly boosting the profitability of their core advertising machine.

By optimizing infrastructure and scaling ad efficiency, Meta is turning high CapEx into a closed-loop engine for revenue growth, proving that market concerns over their spending were misplaced.

Relevant Accrued Interest Articles to Read on META 0.00%↑:

2026.03.27: Back to the EBITDA: Decoding Meta’s $1,116 Executive Playbook

2026.03.25: Zuckerberg’s Middle-Age Metabolism: Trimming Fat to Fund Superintelligence

B) OpenAI’s projection of $100 billion in ad revenue relies on an audaciously aggressive global ARPU target.

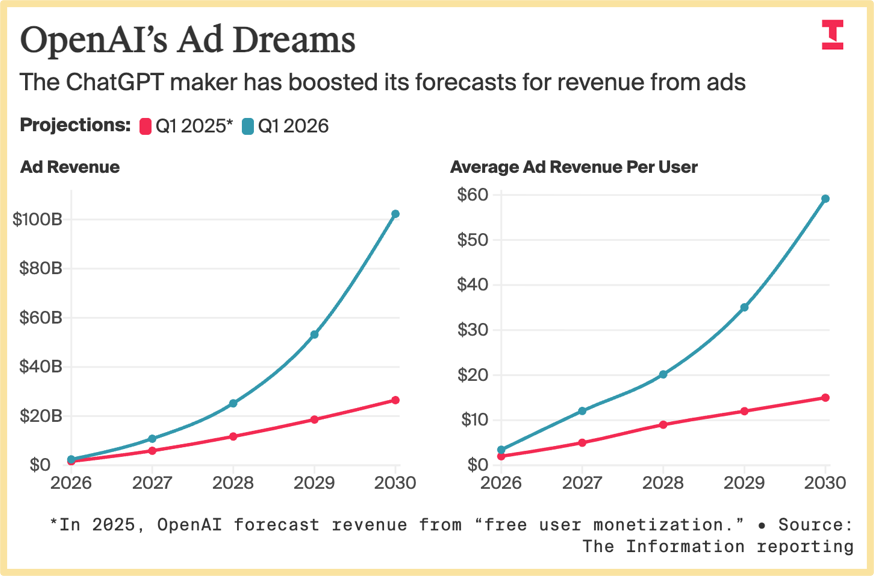

While Meta is proving its model today, the Information reported this morning that OpenAI is aggressively revising its long-term financial forecasts higher. Internal projections show OpenAI leadership expects advertising to eventually become their largest revenue driver. They are modeling a massive leap from roughly $11 billion in the near term to over $102 billion by 2030. To justify this figure, OpenAI is banking on generating a global ARPU (average revenue per user) of approximately $60 by 2030.

Anyone who has ever worked in a corporate FP&A (financial planning and analysis) role recognizes EXACTLY what is happening here. Pushing a massive, hockey-stick growth curve out to the end of the decade is a classic financial modeling maneuver. It is designed to justify an astronomical private valuation today, buying leadership breathing room while distracting from the slow and bumpy rollout of their early advertising products.

I did some back-of-the-envelope math, and to hit $100 billion in ad revenue, OpenAI cannot mathematically rely on skimming the cream off a premium, highly lucrative North American user base. To get the sheer volume of impressions required, OpenAI must scale heavily into the Asia-Pacific and “Rest of World” regions.

Matching Meta’s two-decade-old global monetization efficiency in under five years is a financial modeling mirage.

This is where the reality of digital advertising mechanics throws a wrench into OpenAI’s overly-promotional pitch deck. Once a platform expands globally, its geographic mix inevitably begins to mirror the broader internet population, meaning lower-monetizing international regions will drastically drag down the blended global ARPU.

(Sidebar - This is exactly like the “empty calorie” growth problem I wrote about in my February Pinterest deep dive. You can read that here: Pinterest ($PINS) Q4 Earnings: The “Value Trap” Trap Door Opens)

Let’s look at Meta’s actual, reported geographic ARPU data from 2025 to understand why OpenAI’s forecast is such a massive stretch. In the US and Canada, Meta generated roughly $78 billion in revenue in 2025. When you divide that by their active user base in the region, it translates to an annualized ARPU of over $298 per user. If OpenAI’s user base were strictly limited to Western, high-income professionals, a $60 ARPU would actually be highly conservative. However, that total market is mathematically capped. The easy monetization region is already fully saturated, meaning there simply is not $100 billion of unallocated, high-margin ad spend sitting in North America waiting for OpenAI to claim it.

Now, when you evaluate Meta GLOBALLY, the picture changes entirely. In total, Meta generated roughly $135 billion in 2025 with a blended global ARPU of just $57.03. Reaching this global benchmark requires balancing those highly lucrative, premium US users with hundreds of millions of active users in international growth markets where digital advertising rates are literally pennies on the dollar.

By targeting a $60 global ARPU for the year 2030, OpenAI is implicitly telling the market that their completely unproven search-and-chat advertising network will somehow achieve parity with Meta’s highly-optimized, two-decade-old global monetization engine in less than five years. Scaling an ad-exchange requires building a global sales infrastructure, developing robust attribution tech, and convincing sticky advertisers to move their budgets. Assuming OpenAI can reach instant maturity is a huge stretch, and long-term investors should view that $100 billion ad revenue target with intense skepticism. I will leave it up to the readers whether or not they are willing to give Sam Altman the benefit of the doubt.

Relevant Accrued Interest Articles to Read:

2026.03.12: The Pokémon Theory of Media Investing

C) Uber is widening its autonomous moat in Los Angeles without sinking billions into CapEx.

While Meta is spending its way to dominance and OpenAI is forecasting its way there, Uber is executing a capital-light strategy to protect its intrinsic value. Uber just announced a partnership with MOIA (a Volkswagen Group company) to deploy a fleet of autonomous “ID.Buzz” vehicles on the Uber platform in Los Angeles by late 2026.

This is a big reason why I think people are still getting Uber wrong. For years, the bears argued that Waymo or Tesla would just build their own apps and make Uber obsolete. But that’s not what’s happening. Instead, Uber is setting itself up as the go-to, asset-light brain that handles the routing for the entire autonomous future.

By letting Volkswagen handle the actual hardware, Uber doesn’t have to sink billions into manufacturing or maintaining a physical fleet. They’re basically just plugging third-party robotaxis into their massive, ready-made network of riders.

As self-driving cars take off, this strategy lets them pocket high-margin routing fees without getting stuck with the “depreciation nightmare” of owning the cars themselves.

Pivoting to Amazon’s custom AWS silicon is a heavy margin-protection play for Uber’s compute-intensive future.

Alongside the VW news, it was announced that Uber is expanding its Amazon Web Services (AWS) deal to run its complex ride-matching algorithms on Amazon’s custom Graviton4 and Trainium3 chips. As Uber scales its autonomous network, the compute power required to match riders, optimize routes, and predict pricing in real-time will skyrocket. By migrating away from standard, expensive commercial GPUs and utilizing Amazon’s custom-built silicon, Uber can lower its backend infrastructure costs.

As value investors, we must be patient. These moves are not going to show up in next quarter’s EPS, and they won’t make for flashy consumer headlines. However, they fundamentally improve the long-term intrinsic value of the business. Uber is widening its moat exactly the way long-term value investors should want them to. Currently $70 per share, Uber is still an inexpensive stock, trading at 16x consensus 2027 GAAP EPS. I remain bullish despite the stock being down -13% YTD.

Relevant Accrued Interest Articles to Read on UBER 0.00%↑ :

2025.12.21: Why Uber Will Outperform in 2026 ($UBER)

Conclusion

I want to send a huge THANK YOU to all the new readers and subscribers out there. If you found any of my research helpful - please like and share so we can help grow the Accrued Interest community!

-Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.