Meta Q2-25 Earnings Recap

Why AI-Driven Ad Growth Makes the Bull Case Even Stronger

Introduction

Meta exceeded investor expectations when it reported its Q2-25 earnings. As regular readers of this Substack are aware, I have been bullish on Meta ever since I began writing Accrued Interest and doing videos on YouTube.

Similar to my previous Google quarterly earnings recap, this review of Meta's earnings will highlight key insights that go beyond what AI could generate from a press release. Although I have expressed a positive view of Meta, I have not conducted a deep dive into the company previously, as the stock did not seem particularly undervalued.

I confess that I underestimated Meta, and the recent earnings report has revealed it to be a more robust company than I had previously recognized.

Allow me to elaborate….

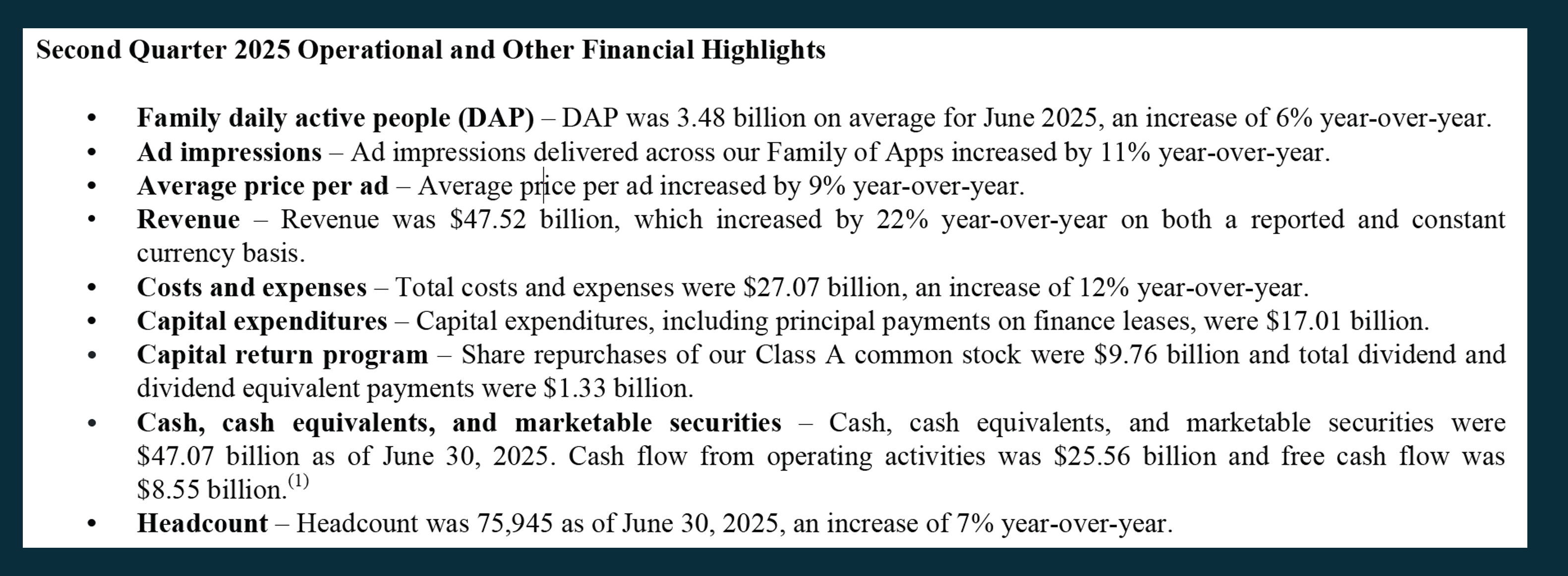

Summary Q2 Results – Meta demonstrated rapid growth across all operational metrics. For a detailed overview of operational highlights, check out this excerpt from the press release below. I am putting this up top for readers who just want the numbers, no commentary. This rest of this post will delve into the strategic insights.

Key Takeaway from Q2-25 – Meta reported a remarkable +22% YoY revenue growth, primarily fueled by an +11% YoY increase in ad impressions across its Family of Apps (FoA), which includes Facebook, Instagram, Messenger and WhatsApp. This signified a re-acceleration in impression growth after several quarters of slowdown, a trend CFO Susan Li anticipates will persist into the second half of 2025 and 2026.

I am going to be talking a lot about impression growth in this post, because it is the strongest indicator of business health at Meta. And when impression growth accelerates, it is often a leading indicator that revenue (and profits) are about to accelerate as well.

How Advertising Companies Make Money

I consider Accrued Interest my value investing syllabus that I am writing in real time with each new post. My goal is not only to tell you what stocks are likely to go up, but I want to help explain WHY stocks move the way that they do.

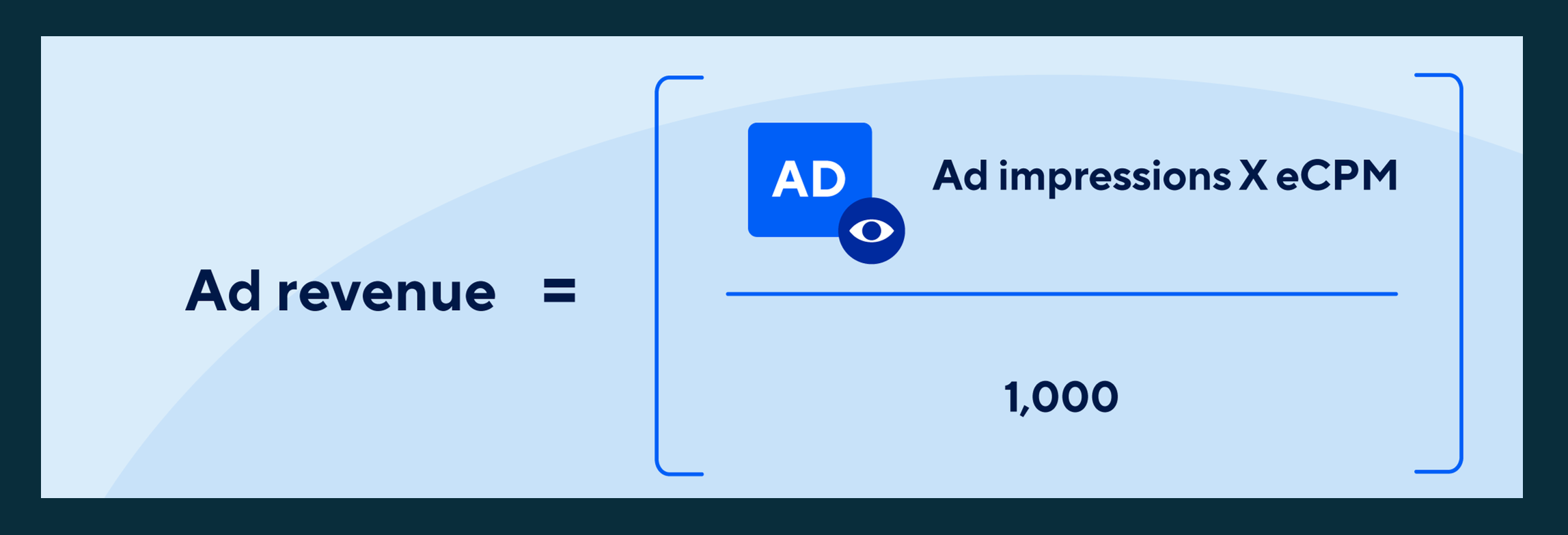

As many of you know, my professional experience lies in advertising-based media, including broadcast and cable television, billboards, radio, and digital platforms. Understanding the significance of ad impressions is crucial. The fundamental principle is that "Ad revenue equals Ad impressions multiplied by CPM." Let me break down what this means in simpler terms.

AD IMPRESSIONS MEASURE VOLUME

An ad impression is a metric that counts how many times an advertisement is displayed on a user's screen. Each time an ad is fetched and appears on a webpage, in an app, or on a social media feed, it is counted as one impression.

It is important to note that an impression does not mean the user engaged with the ad, such as clicking on it. It simply means the ad was shown. The goal of counting impressions is to measure the visibility and reach of an advertising campaign.

PRICING (CPM) MEASURES DEMAND

CPM stands for "Cost Per Mille," with "mille" being the Latin word for "thousand." It is a standard metric in advertising pricing that represents the cost an advertiser pays for one thousand ad impressions.

What Does It Mean for Meta ($META)?

An increase in Meta's daily active users (DAP) and their engagement with the company's services leads to a rise in impressions. Impressions represent the available user attention that can be monetized through advertisements.

Meta generates revenue primarily through an auction-based advertising system. Typically, this system demonstrates an inverse correlation between the supply and demand for ads.

When Meta usage grows faster than advertising demand, an increase in impression growth leads to greater supply, which in turn drives down pricing (CPMs).

However, these lower-priced ads attract more ad buyers, leading to an upward pressure on CPMs as bids increase.

Make sense?

Enough with the Lecture, How Do We Make Money?

Usually, a good time to purchase Meta stock is when ad impression growth outpaces pricing increases. Meta's success stems from its ability to continuously improve ad inventory monetization, a process accelerated by AI.

Let me illustrate with some exhibits from Meta’s Q2 earnings.

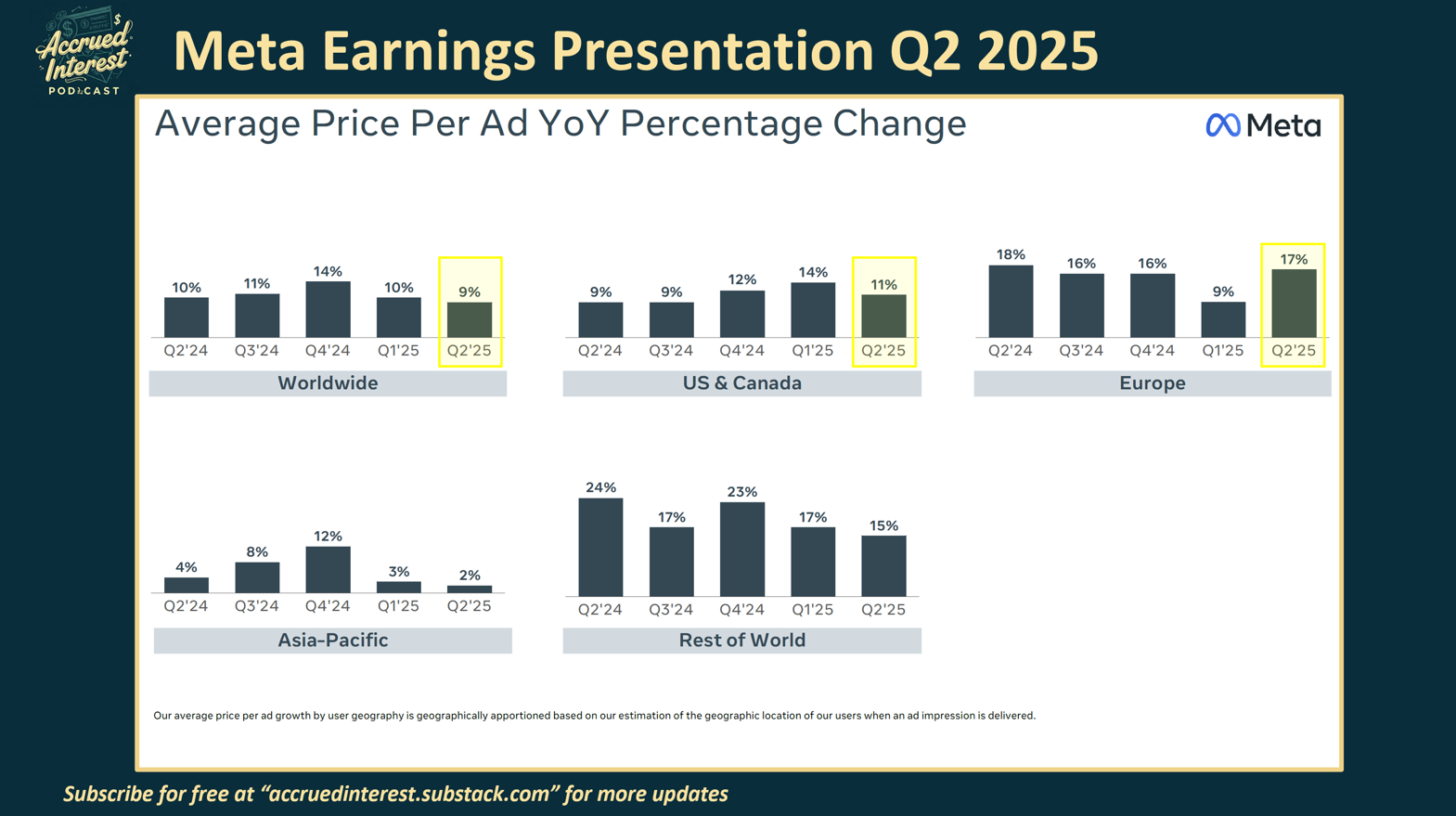

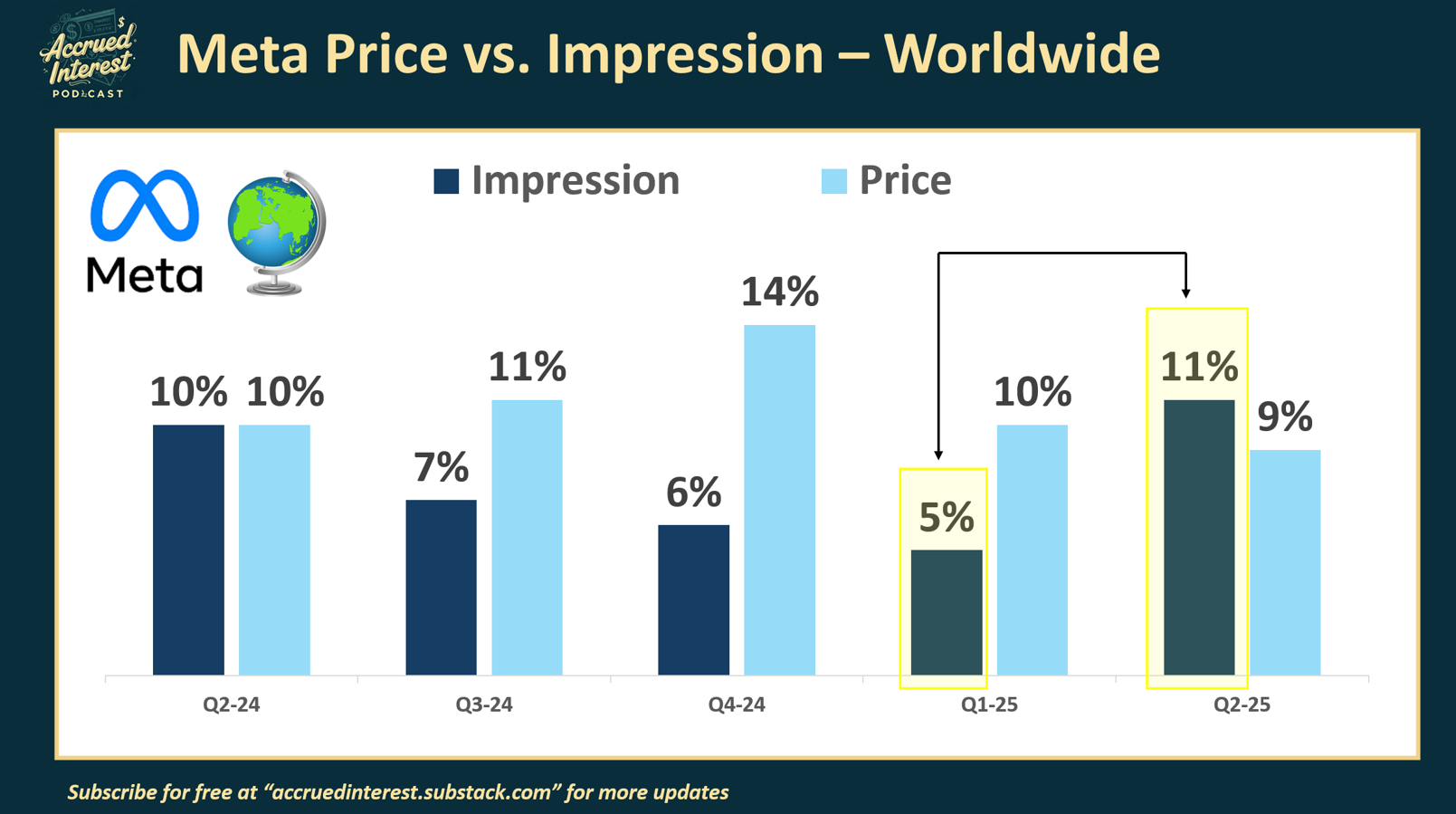

Growth in average price per ad was up a healthy +9% in Q2 worldwide for Meta. That was consistent with the last four quarters where pricing was up at least +10% YoY. Demand for Meta’s audience remains strong as advertisers see a clear ROAS (return on ad spend).

While strong ad pricing is positive, consistently raising prices by double-digits annually may not be sustainable long-term. Such increases could eventually deter demand and risk market share loss.

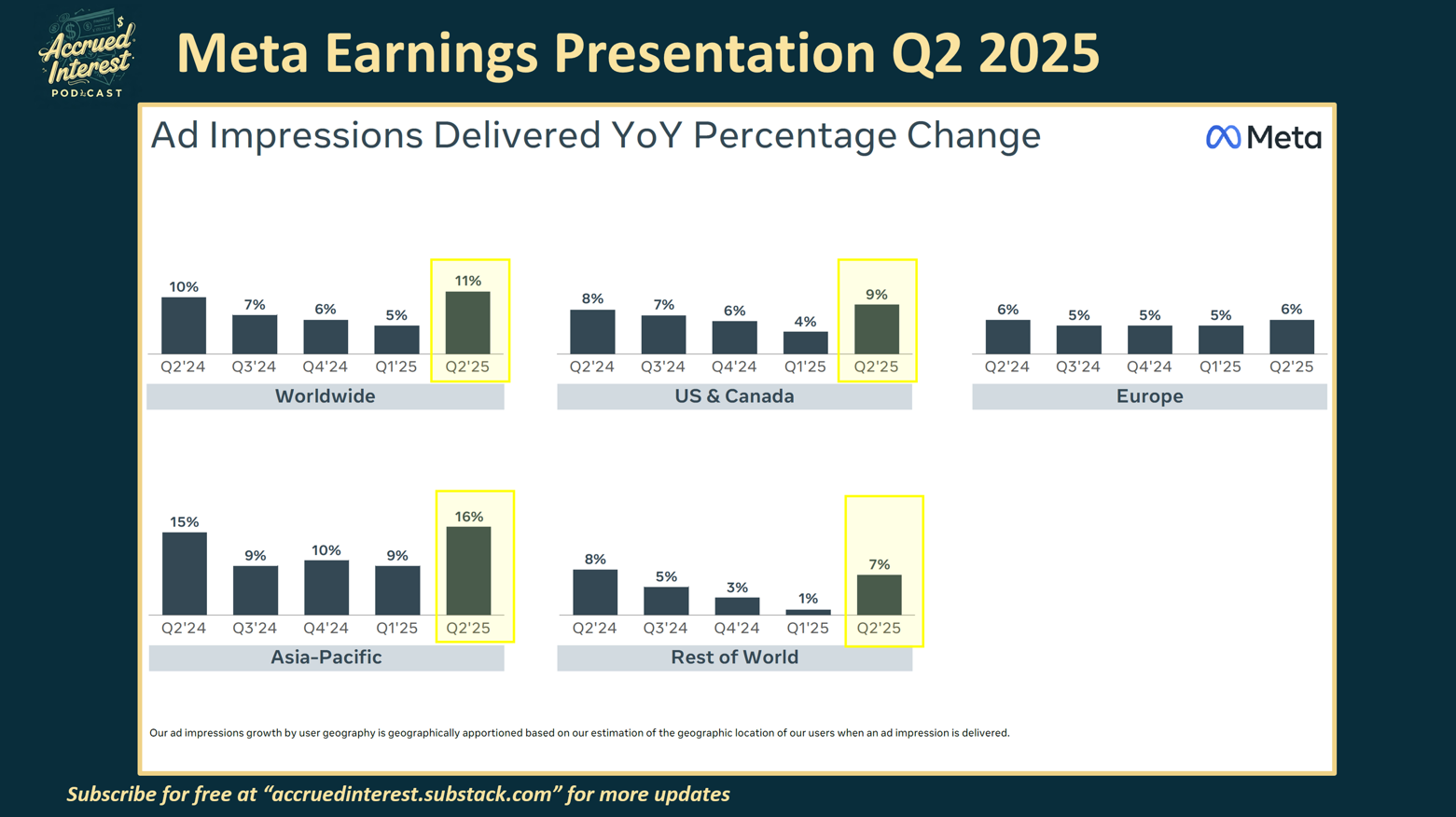

As you can see from this chart above, impression growth was up +11% in Q2, more than double the 5% YoY in Q1. Impression growth was the highest in a year.

Improved impression growth is beneficial for Meta's long-term health. A larger user base provides more opportunities to sell advertisements, reducing the need to over-saturate screens with ads. This explains the strong investor confidence following the earnings report.

A Different Point of View

Now let me show you the same two variables – impression growth and pricing growth – together in some custom charts I made. I think viewed this way you more clearly see the spike in impression growth.

Historically, impressions and pricing for Meta have often moved in opposite directions. However, this past quarter was an exception, with both metrics showing near double-digit growth: impressions increased by 11% and pricing by 9%. Meta last experienced such balanced growth in Q2-24.

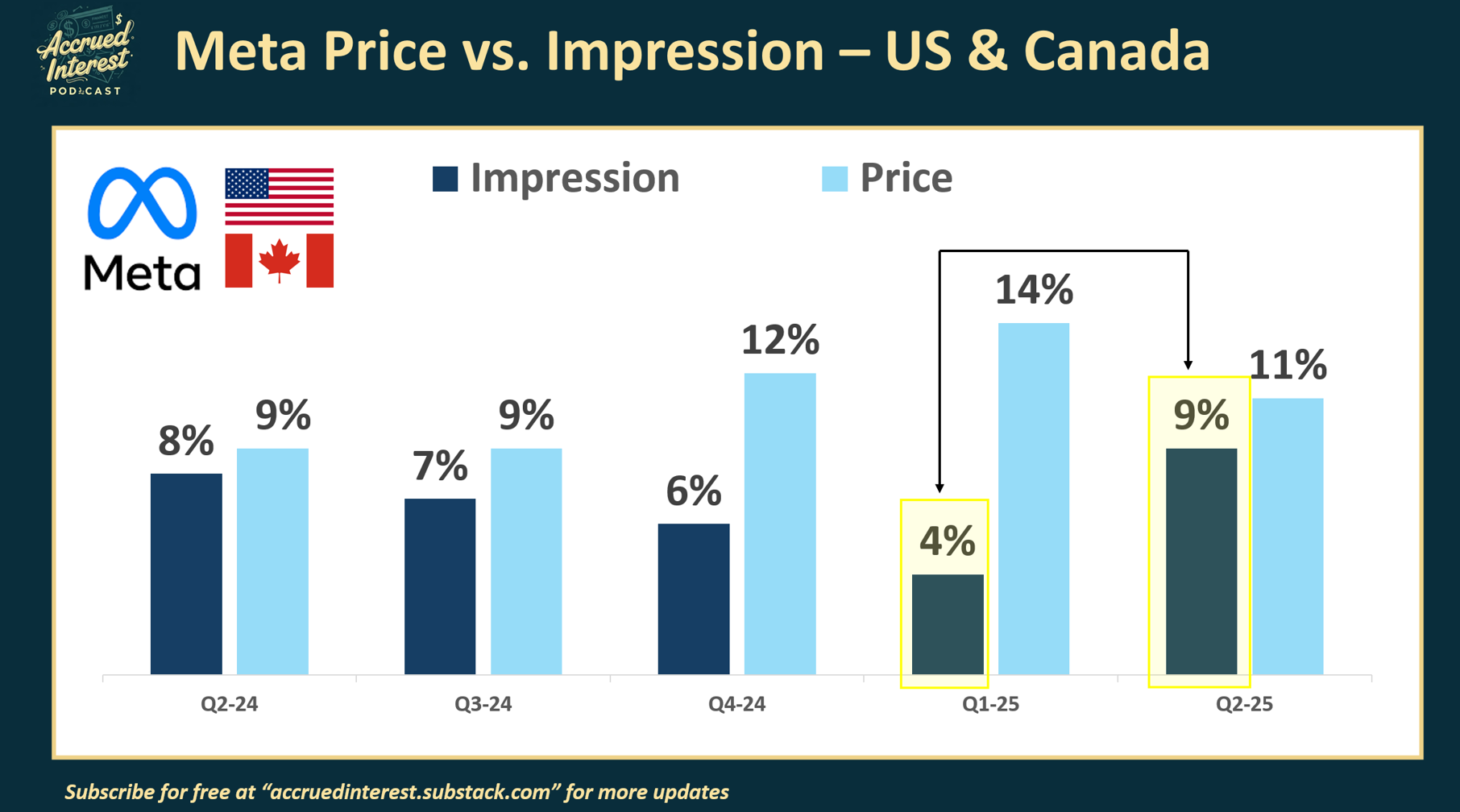

The trend is similar when you zoom in on the US & Canada, Meta’s largest source of revenue and operating profit.

This is excellent news for Meta shareholders and a compelling reason to hold onto the stock, or to consider purchasing it if it is not already part of your portfolio.

This is the Part Where We Talk About AI

The re-acceleration of impressions after a period of deceleration for many quarters is a significant positive signal for the health and reach of Meta's platforms. This is attributed to ongoing investments in AI and machine learning capabilities that improve content recommendations and ad relevance.

Susan Li, Meta's CFO, explicitly confirmed that the worldwide impression growth acceleration in Q2 was primarily fueled by "incremental engagement on video and Feed surfaces," which benefited from "ranking optimizations" to content recommendations on Facebook and Instagram. Ad load optimizations also played a lesser role.

Meta's management is clearly leaning into AI as the fundamental driver of these improvements. The significant investments in AI infrastructure and talent are not just for future "personal superintelligence" (as Zuckerberg framed it) but are already yielding "compelling returns" in their core advertising business and organic engagement.

Analyst Reactions

Below are summaries of analyst reactions to Meta's Q2 earnings, presented as clippings from sell-side research notes published after the announcement. They are listed by price target, from least to most bullish. Please note that full reports are not available here.

Scotiabank (Sector Perform, PT: $685)

"Meta posted its largest beat in several years. 3Q revenue guidance was well above Street. FY26 capex guide — ~$107B — is ~10x Street’s prior expectation. Investors should be excited about the AI 'all-star' team and chatbot monetization potential. We stay on the sidelines pending visibility on ROI from heavy spending."

DA Davidson (Buy, PT: $825)

"Strong 2Q earnings beat. Meta’s Family of Apps growth is accelerating. Management emphasized that they have all the ingredients to build and deliver superintelligence, supported by increasing compute capacity over the next few years."

Morgan Stanley (Overweight, PT: $850)

"2Q results and 3Q guide reflect GPU-enabled algorithmic gains driving higher engagement and monetization. META’s investment is increasing, but improving core performance supports higher profitability. We see a growing list of long-term optionalities: Meta AI, content tools, business agents, search, and devices — all feeding into the longer horizon superintelligence opportunity."

Guggenheim (Buy, PT: $875)

"Meta posted 2Q OI 19% above consensus, with strong ad product performance and AI tool impact. Management committed to sustained investment — 2025 opex unchanged, but 2026 opex and capex likely to exceed consensus. We see Meta as uniquely positioned to deliver long-term technological transformation in both consumer and enterprise AI."

BofA Securities (Buy, PT: $900)

"A strong 3Q outlook suggests AI investments are delivering results. We raise 2026 revenue by 9%, expenses by 8%, and EPS by 12%. A growing list of ad capabilities reinforces confidence in Meta’s AI ad engine. We see multiple upside drivers in 2H — AI ad stack integrations, Threads/WhatsApp ads — and believe Meta is well positioned to lead in the emerging agentic AI ecosystem."

Citizens JMP (Market Outperform, PT: $900)

"Meta is uniquely positioned to benefit from AI — it has the scale (data) and distribution (users) to quickly realize algorithmic gains. Content recommendation is a complex AI problem at Meta’s scale, and the company is still early in realizing benefits. AI-powered ad creative, personalized content, and superintelligence remain longer-term drivers."

Susquehanna (Positive, PT: $900)

"Q3 revenue guide of +21% y/y at midpoint beats our +13% estimate. FY26 capex guidance implies ~$99B — significantly above consensus. META acknowledged risks tied to EU regulatory rulings and rising U.S. tax rates, but reiterated commitment to scaling Llama 4 and monetization across FoA. We raise 2025 and 2026 revenue, EBITDA, and EPS by 5–8–12% respectively."

Cantor Fitzgerald (Overweight, PT: $920)

"Meta beat revenue and EPS estimates by 6% and 21% respectively. Ad revenue accelerated to +22% y/y ex-FX. Capex and opex are rising materially, but the core business is funding long-term AI investments. Meta is well-positioned with capital, infrastructure, and talent to pursue superintelligence. We revise FY26 revenue and EPS up 4% and reiterate our Top Pick."

Deutsche Bank (Buy, PT: $930)

Rosenblatt (Buy, PT: $1,086) - Street High

"Meta's 2Q25 is turning out to be a pivotal quarter, with dramatically stepped up investment plans paired with accelerated growth. We see the return of +20% ad growth (on a $160B base in 2024) supporting capex trending toward $100B. Our $1,086 PT reflects 20x 2026E Adj. EBITDA and a 24% EBITDA CAGR. EBITDA is becoming the more appropriate core cash flow metric given Meta's capex today appears likely to generate return tomorrow and eventually level out."

Again, these are just summaries of sell-side headlines I saved post-earnings. I do not have any of the full reports as I build my valuation models around consensus averages.

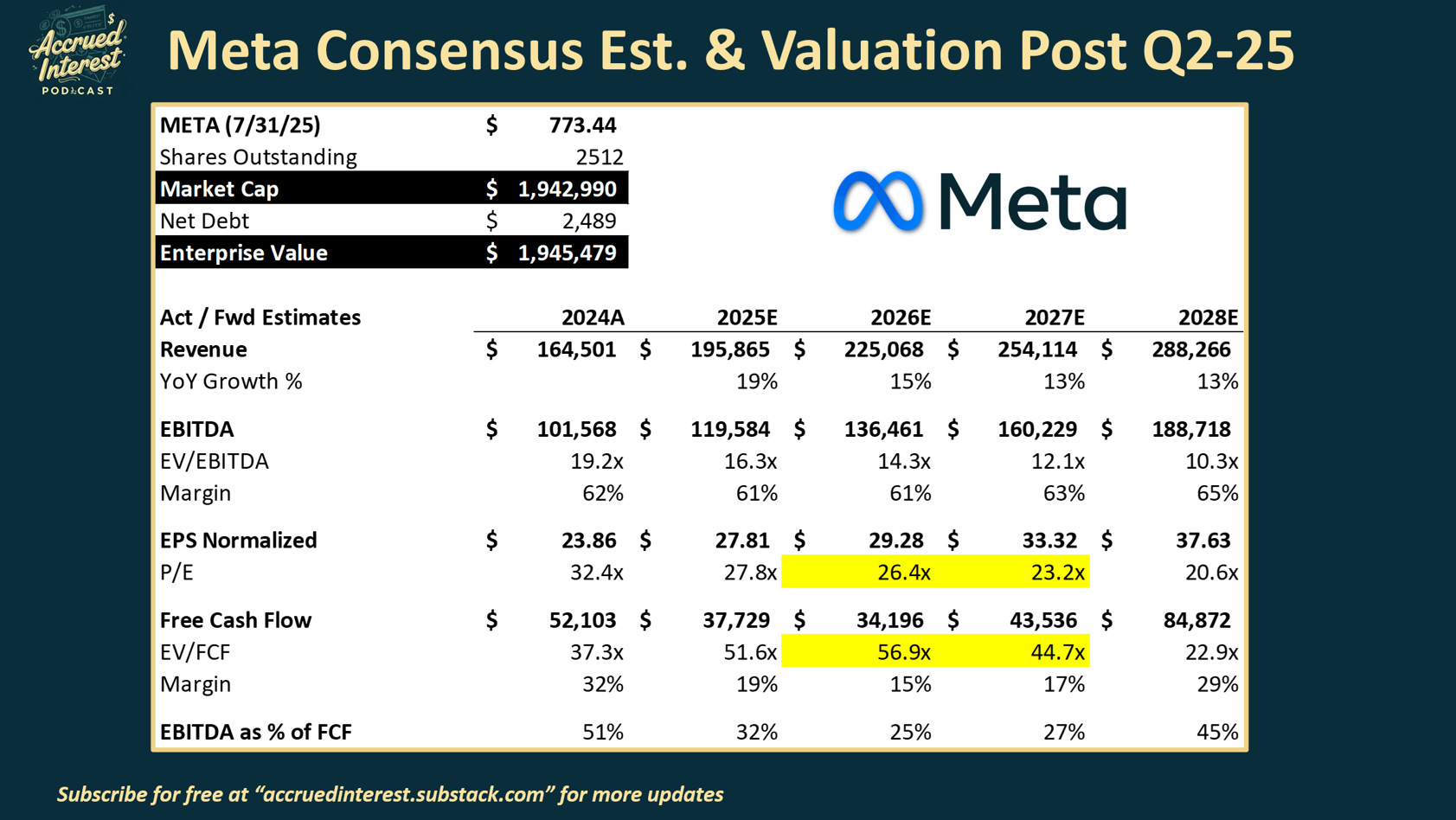

Updated Valuation

Below is my updated view of Meta’s valuation post Q2-25 earnings. As of the market close on 7/31, $META traded at $773 per share. Based on consensus adjusted EPS, it has a P/E of 26x 2026 estimated earnings and 23x 2027. Please note - because Meta is ramping up its capital expenditures for AI investments, analysts lowered their free cash flow (FCF) forecasts for 2025 and beyond. Analysts now expect FCF to fall in 2025 and 2026, and won’t return to 2024 levels until at least 2028. Based on new estimates $META trades at 57x EV/ 2026E FCF and 45x EV/ 2027 FCF.

Conclusion

Meta's Q2 2025 ad performance highlights a core business benefiting significantly from AI-driven optimizations, leading to re-accelerating impression volume and sustained strong pricing, even as newer product monetization scales gradually. The strategic AI investments are central to this narrative, offering a potentially long runway for efficiency and growth in their established advertising segments.

My outlook on Meta remains strong, and I recommend holding the stock. While its current valuation (EV/FCF) is at a premium compared to other major tech advertisers, I would advise against aggressive buying until a pullback occurs. In the long term, market timing is less crucial if you maintain an overweight position in the market's strongest companies — and Meta is certainly among my top ten.

-Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.