Meta Enters the Living Room, Amazon Aggregates Oprah, and Spotify's Fitness Pivot (Accrued Interest Update 4-27-26)

$META, $AMZN, $SPOT, $PTON

Accrued Interest TLDR: In today’s update, I explore Meta’s aggressive push into Connected TV (CTV) advertising, which proves once again that no legacy ad budget is safe from the digital giants. I also break down Amazon’s strategic licensing deal for Oprah Winfrey’s video podcast, highlighting how I see Prime Video evolving into a premier aggregator. Finally, I look at Spotify’s new partnership with Peloton and explain why I remain fundamentally bearish on audio-first platforms attempting to climb the video value chain.

Please subscribe to read the rest of the Accrued Interest Daily Update for April 27.

A) Meta’s Inevitable Push Into Connected TV

I’ve been tracking today’s Digiday report, which reveals that Meta has been holding exploratory meetings since early 2025 with supply-side players, including Magnite and Comcast-owned FreeWheel, to assess how it could access CTV inventory at scale. I see this as an “audience extension” model—essentially building the “Meta Audience Network” but for the living room. This would allow advertisers to use Meta’s targeting to reach users on third-party streaming inventory beyond its owned-and-operated apps. Digiday notes that “Meta’s core strength lies in performance advertising, particularly among small and mid-sized businesses”, and I believe moving to CTV unlocks a massive new pool of spend for them.

This move would perfectly align with Meta’s existing strengths: deterministic user data, cross-device identity, and AI-driven optimization. Bringing these tools to the living room capitalizes on the “CTV-to-mobile” loop, where ads viewed on television drive measurable, direct-response actions on mobile devices. They are also facing pressure as competitors like Pinterest (which purchased tvScientific) and Amazon move into the same space.

Today’s news is important because it demonstrates how powerful Meta is that they can go after ad budgets in almost every format. It’s almost as if no company is truly safe from competing with Meta. This is why it is so easy for me to be bullish. Due to their sheer size and dominance in digital advertising, it is inevitable that they are going after TV advertising budgets.

Discussing this inevitably brings up the competition from YouTube. But as I have been saying on Accrued Interest, both can win. There are still tens of billions of dollars being spent with legacy media players that Meta, YouTube, and Netflix can still take away before they even begin cannibalizing each other.

I think it is a huge mistake when people define “Streaming” as a distinct category. The way ad budgets are actually allocated in the real world—there is only one category, and that is VIDEO. As I detailed in my article on the Pokémon Theory of Media Investing, this is yet another reminder of the fundamental strength of Meta’s business model.

I am still bullish on Meta. With the stock at $676 per share, I am eagerly awaiting their Q1-26 earnings this week.

B) Amazon Expands Prime Video’s Value with Oprah

I read in the New York Times today that Amazon reached a multiyear licensing deal with Oprah Winfrey. Beginning this summer, she will produce twice-a-week video podcasts and specials for Amazon. The Times quoted Steve Boom saying they are happy to be along for the ride. I see this as a clear signal of where the market is headed; more video being viewed on Prime.

This partnership is deeply integrated into Amazon’s retail ecosystem. The deal includes a dedicated landing page on Amazon.com for her “Favorite Things“ holiday list, and the two parties will share sales and advertising revenue. Amazon plans to leverage its Audible, Kindle, and Goodreads platforms to expand the reach of Oprah’s Book Club as it approaches its 30th anniversary in September. This fits into Amazon’s recent podcast unit restructuring, where they split their Wondery podcast division, moving talk-show style video podcasts into a newly named “Creator Services” division.

The news regarding Oprah is significant because it represents more than just a platform shift for a show that already commands nearly a million YouTube subscribers and seven-figure viewership per episode. The true narrative lies in Amazon’s effort to broaden the distribution of a premier talk show brand, effectively positioning Prime Video as a dominant aggregator in the evolving digital video landscape.

This shows why you can’t focus on strict legacy categories like “streaming” or “podcasting.” Oprah Winfrey’s video “podcast” is literally just the digital incarnation of the Oprah Winfrey Show. The episodes are video-first and even feature a full studio audience—something you almost never see for a traditional podcast, but a staple of the classic talk show format.

The show will still be available on YouTube, meaning Prime Video is growing its utility not exclusively through walled-garden exclusives, but by bringing disparate video services into one cohesive streaming environment. In some ways, Prime Video is acting similar to Roku, in that millions of people use it to manage and aggregate their other SVOD subscriptions.

I currently have no stock recommendation on Amazon, though I remain bullish on the entire digital video landscape. Prime Video, which I believe is significantly underappreciated by investors in the “streaming wars” discourse, has achieved substantial growth by aggressively leaning into free, ad-supported video.

AMZN 0.00%↑, GOOGL 0.00%↑, GOOG 0.00%↑, ROKU 0.00%↑

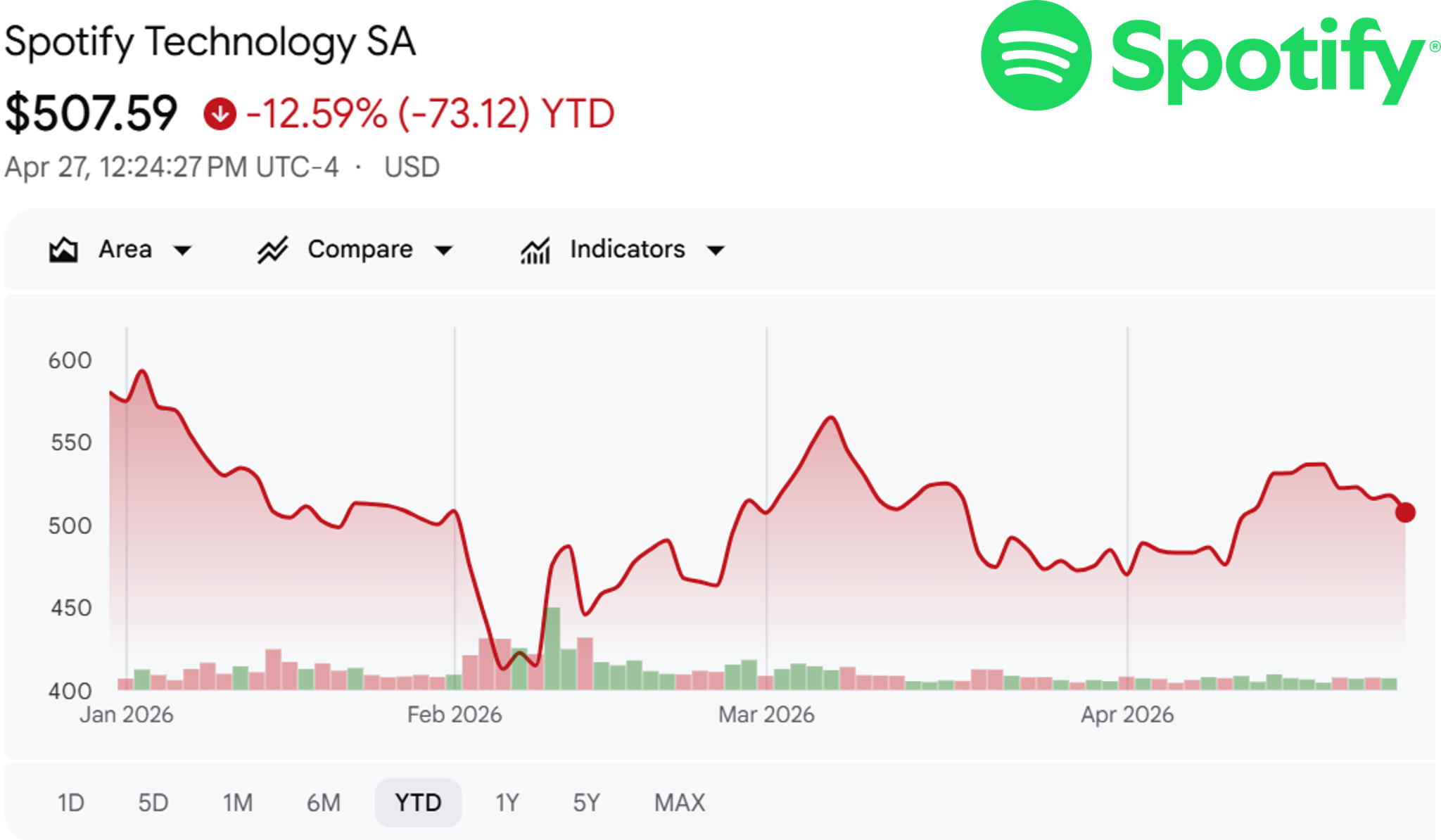

C) Spotify’s Fitness Push Highlights Its Audio-First Problem

I saw the Bloomberg report that Spotify Premium now includes Peloton classes, which I consider to be the music pioneer’s first major push into fitness content. This new partnership brings access to over 1,400 on-demand classes. Bloomberg quoted Roman Wasenmüller stating that they are expanding Spotify to become a wellness companion—a shift I find very interesting.

This deal is a distribution play for Peloton, which currently operates in only six countries; this partnership will expand its footprint to the majority of Spotify’s 180-plus markets. For Spotify, which boasts 290 million paid members and recently raised its US premium subscription to $13, it represents another attempt by co-CEOs Gustav Söderström and Alex Norström to add value beyond audio. Söderström noted the opportunity, stating that while people have always exercised to Spotify, “they never watched Spotify doing yoga in front of it”.

Today’s news is about Spotify striking yet another partnership in an attempt to expand outside of audio-only and become a more general entertainment media service. However, my point of view is that these partnerships with Peloton and others are simply not enough. Peloton as a company has struggled over recent years after the Covid-boom wore off. I am bearish on Spotify because audio-first companies have historically not been successful when trying to move up the value chain and expand into video and other broader interactive formats.

Spotify has spent years trying to make video happen, but it just hasn’t moved the needle. It’s tough to sell people on a video experience when you’ve already trained them to use your app for audio. History shows it’s much easier to start with video and move downstream—just look at YouTube. They’ve had way more success becoming a music destination than Spotify has had trying to be a video platform. YouTube Music is growing fast and is a massive driver for their overall business.

I think that Spotify, and other audio-first entertainment stocks, should be avoided for all of the above reasons.

-Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.

Great article. Interested in your opinion on $IMAX. Stock was up 44% in 2025 while almost all the cinemas did not meet investors expectations and underperformed heavily. I believe that market starts treating it as a tech and brand licensor rather than an exhibitor. The business model has a big reliance on China and ~85% flow-through box office, with the hidden revenue stream from upgrades they make for cinemas turning old Xenox Model (more than a half of their systems) into a new Laser Model. The stock is at 45x forward P/E. Does it deserve these multiples or is one disappointment slate enough to return it back to upper teens? Thanks