Media Valuation Tracker Update – Week of July 21, 2025

Notes on $GOOGL, $WBD, $TTD, $PINS, $GTN and $SSP

This is the third week in an ongoing series in which I update my Accrued Interest Multiple Tracker. As I said last time, the point of these trackers is to 1) observe “consensus” opinion on key stocks, 2) decide if we have a variant perception that may lead to 3) an actionable investment move. I am building Accrued Interest as a research service that provides ACTIONABLE information. Used properly, my trackers can help explain WHY stocks move the way they do over time.

Last week, Netflix ($NFLX) was the first company on my list to report Q2 earnings. As the remaining 18 reports are released over the coming weeks, estimates and valuations are expected to shift. For the moment, I'd like to draw attention to a few stocks that have moved since last week's update and share my current perspectives.

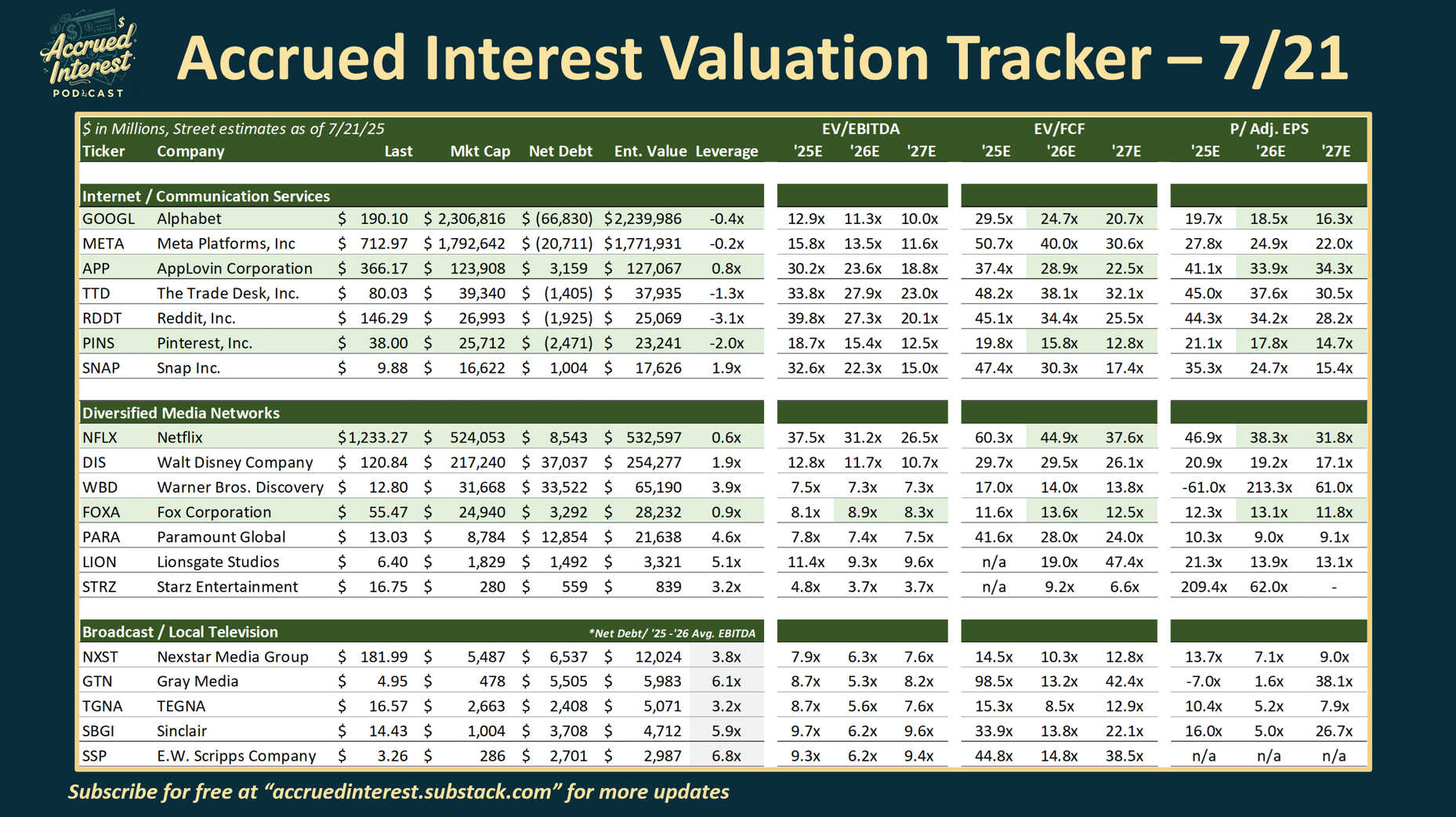

Valuation Tracker Update – Week of July 21

Internet / Communication Services

Google ($GOOGL) up +4.7% vs. last week:

I noticed that Google was quietly up almost +5% last week, now near $190 and approaching its recent all-time high of $207. There was no major news for the company, but a number of research analysts had put out positive notes ahead of Q2 earnings today, Wed 7/23.

Here’s a brief summary of analyst commentary. I don’t have the full reports, so I am posting key quotes below so you get a sense of sentiment:

Goldman Sachs: Buy rating and $225 price target

“We continue to highlight GOOGL as one of the most compelling risk/reward skews (based on our upside/downside work) from current levels,”

“We continue to view GOOGL’s ability to distribute AI solutions (Gemini being at the center) across an array of existing desktop/mobile computing applications (Gmail, Search, Chrome, Drive, Maps, YouTube, Photos) as underappreciated.”

Bank of America: Buy, price target up $10 to $210

“2Q positives could include: 1) Commentary suggesting ad spend has accelerated since April, 2) Strong search results suggesting AI integration aiding monetization (lowering revenue reset risk), 3) YouTube beat on easy y/y comps, and 4) Cloud strength from added capacity & Workspace AI integration,”

I’ve been super bullish on Google as long as I’ve had my Substack and podcast. In my piece last week Media Stock Insights from Nielsen’s June-25 TV Snapshot, I explained how YouTube reached a new all-time high of 12.8% of all TV viewing in America.

I think the most impressive aspect of YT’s new high of 12.8% is that the service is still managing to take share at an impressive pace. YouTube grew +29% vs. last June while Netflix ($NFLX) stayed flat at #2.

I’ll have more to say about Google in the coming days after they report.

Rating: Google ($GOOGL) remains one of my favorite stocks — Outperform

The Trade Desk ($TTD) up +6.1% vs. last week:

While The Trade Desk (TTD) has experienced some significant declines in 2025, down almost -30% YTD, it got a reprieve last week when it was announced it was being added to the S&P 500.

Stocks typically rise when added to an index due to the significant volume of shares purchased for every customer holding the S&P 500.

While the recent market activity provides a temporary surge, it doesn't alter TTD's intrinsic value. Investment decisions should never be based solely on the actions of others, or in this instance, an entire index.

Rating: No opinion on TTD

Pinterest ($PINS) up +5.6% vs. last week:

Pinterest has been heading slowly higher recently as we get closer to Q2 earnings. From what I saw, there was not any major news last week — it looks like a little multiple expansion. I am hoping the stock takes a pause so I can finish my 2nd write-up on the company.

In case you missed it, last month I did my first "WIP" article, (Work-In-Progress), where I talk through a stock I am actively researching.

My takeaway from Pinterest ($PINS) - Is the Market Wrong?, was that Pinterest is definitely a cheap stock with low future expectations. I am reading more about how the company can use AI to improve its monetization and expand margins.

Rating: Leaning Outperform

Diversified Media + Streaming

Warner Bros. Discovery ($WBD) up +6.6% vs. last week:

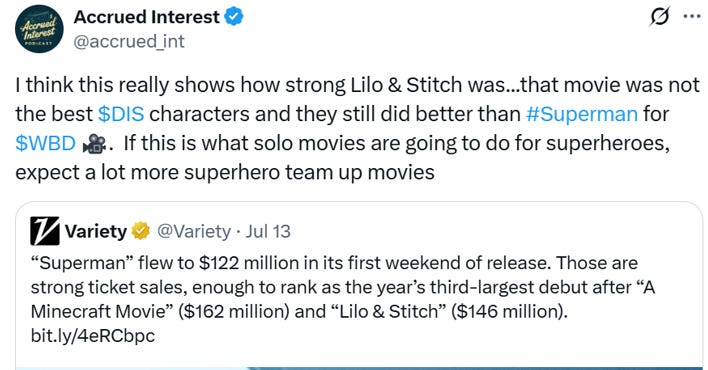

It is clear that WBD stock has been up recently due to the positive reception to the new Superman reboot. The reviews have been glowing and the box office receipts have been solid.

But let's step back and provide context. Superman has been #1 recently, but it is notable that two non-superhero franchises had BIGGER box office debuts this year.

Over on Twitter I pointed this out — “I think this really shows how strong Lilo & Stitch was...that movie was not the best DIS characters and they still did better than #Superman for $WBD 🎥. If this is what solo movies are going to do for superheroes, expect a lot more superhero team up movies”

There was also news of progress on the new Harry Potter series for HBO. "HBO’s ‘Harry Potter’ Studio Builds a School for Child Actors to Attend During Filming Over the Next 8 to 10 Years”.

My opinion on WBD has not changed. As I said in my writeup on the WBD spinoff announcement recently:

There's currently no strong reason to buy WBD stock today. Opportunities for long positions may arise closer to the spin-off, once we see the relative valuation between the businesses.

I’m more bullish on the Streaming & Studios half of the business, than I am the Global Networks part. As I said in my interview with Rich Howe on the Stock Spin-Off Investing Podcast, Harry Potter is CRUCIAL for WBD because they need more long-running series to keep viewers from canceling during the offseason of their respective favorite show. With HP expected to run for at LEAST 7 seasons (1 per J.K. Rowling book), that could be 8 to 10 years worth of content to keep subscribers hooked.

Long-term, the wizard known as “The Boy Who Lived” matters more to HBO’s future than “The Man of Steel”.

Rating: Wait until we get closer to the WBD spinoff

Broadcast / Local Television

Gray Media ($GTN) down -12.1% vs. last week

E.W. Scripps Company ($SSP) down -13.1% vs. last week

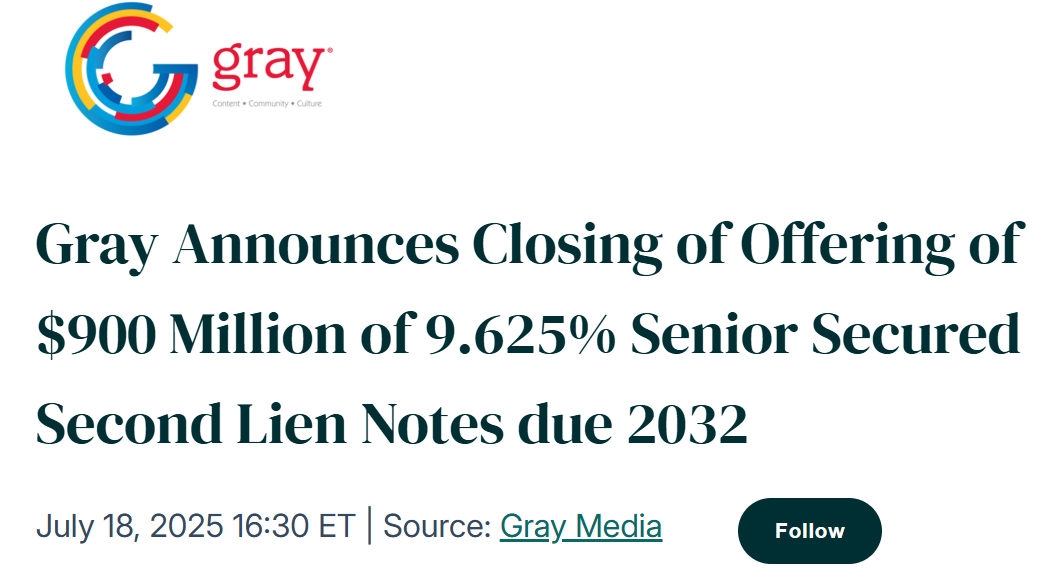

At first, there was some initial euphoria in broadcast stocks such as Gray and Scripps, on news the next M&A wave had begun. (Gray Media and Scripps Agree to Swap Television Stations). I think the stocks gave back some of their gains as news came out about the Gray Media debt refinancing.

Gray Media refinanced $700M debt with $900M of 9.625% high-yield notes, extending maturities to 2032

Short-term, GTN buys itself a few more years of runway by pushing out some of its larger debt payments. But with cord-cutting continuing and viewers moving to ad-supported streaming services, time is not on your side for TV station owners.

Remember — financial engineering is NOT a substitute for a strategy.

Rating: Nexstar (NXST) and anyone buying stations is an Underperform. The winners will be anyone who is able to sell their company!

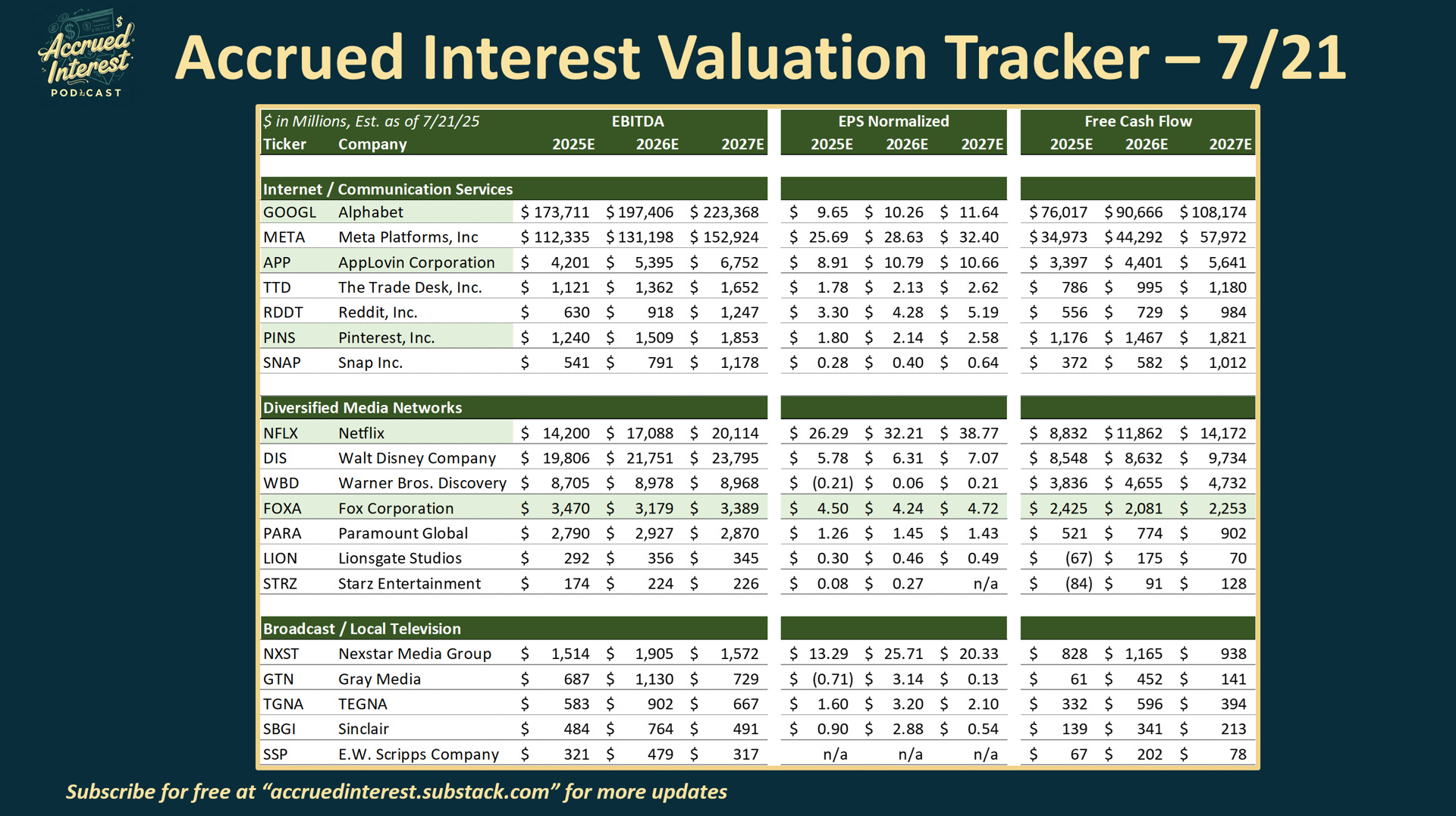

Earnings Estimates Update – Week of July 21

The following table has all the earnings estimates I gathered from Tikr. Again, the point here is not yet to agree or disagree with these figures. I find it helpful to track consensus EBITDA, adjusted earnings per share (EPS) and my favorite metric, free cash flow (FCF). Future editions will analyze how changes in earnings estimates impact company multiples. Subscribers will also receive the Excel models used in these analyses over time.

CONCLUSION

Given that we are at the beginning of Q2 earnings season, research analysts are updating their models daily. I will wait a few more weeks to measure the degree with estimates moved, in either direction. For now I have seen no material estimate changes to the TMT stocks in my coverage universe; just minor model tweaks.

I'm eager to hear your feedback! Which media and tech companies should I add to the tracker to support your research? Please share your suggestions in the comments or reach out to me directly at simeon@accruedint.com.

-Accrued Interest

Re:WBD/WB - IMO the prior DCEU run of films caused significant brand damage that caused (a) collateral damage to the DC brand, and (b) misaligned expectations regarding the appropriateness of DC films for children. So I think its feeling the impact of audience mistrust in this initial launch, but moving forward it bodes well for the DC franchise as audience acclimatize to higher quality material.

My thesis remains that the value of WB IP is undervalued, especially in an AI driven world where production budgets can fall precipitously.