Media Valuation Tracker Update – Week of Sep 8, 2025

Notes on $PSKY, $GOOG, $APP and more

This is the sixth edition in an ongoing series in which I update my Accrued Interest Multiple Tracker. I want to focus on some of the biggest changes since last update. My aim for Accrued Interest is to create actionable research materials. You can find past editions here: Aug 12, July 28, July 21, July 14 and July 7.

Valuation Tracker Update – Week of Sep 8, 2025

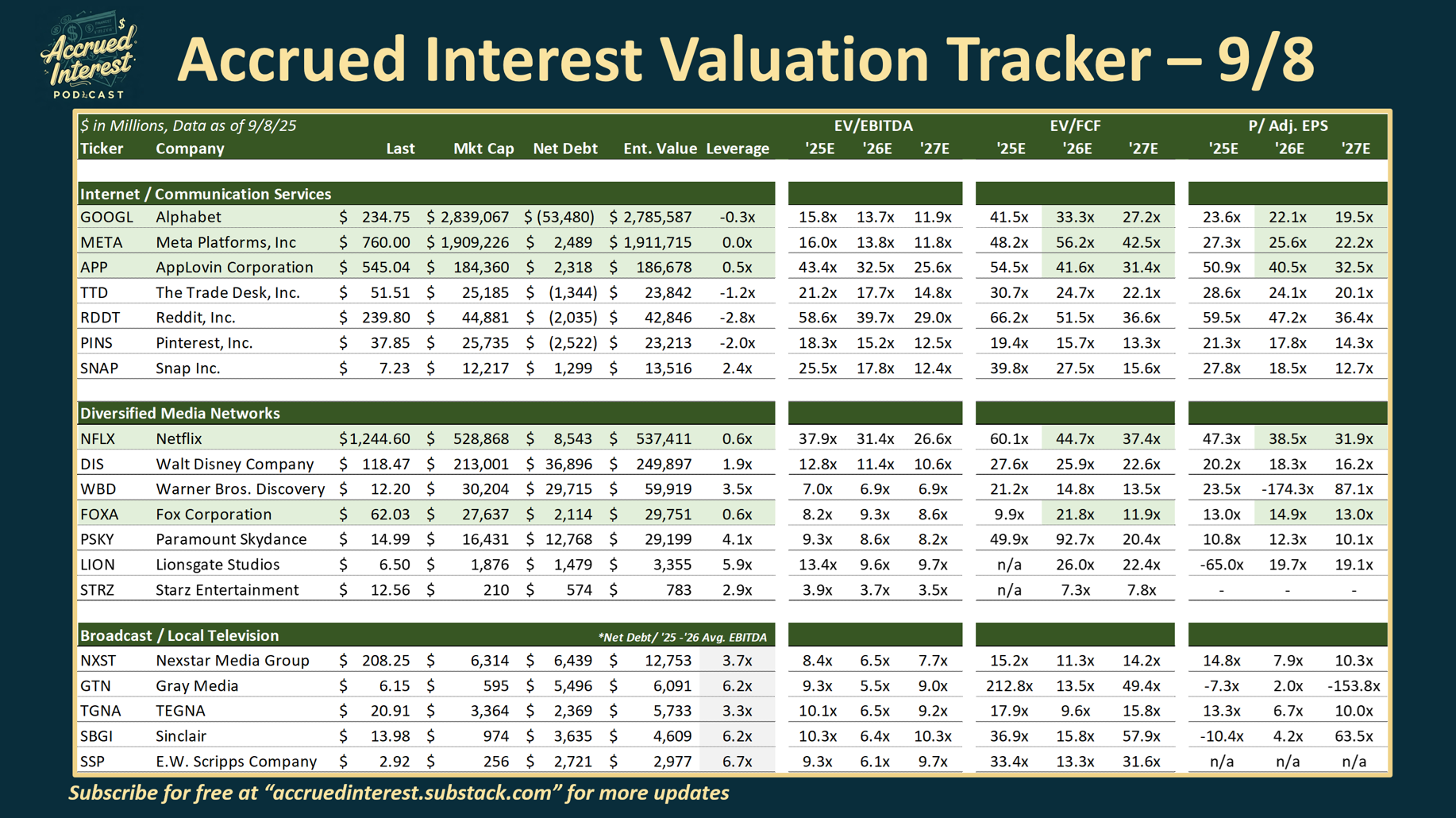

Here is the tracker update with all the company companies' respective multiples for EV/EBITDA, EV / Free Cash Flow (always fully levered), and Adjusted P/E.

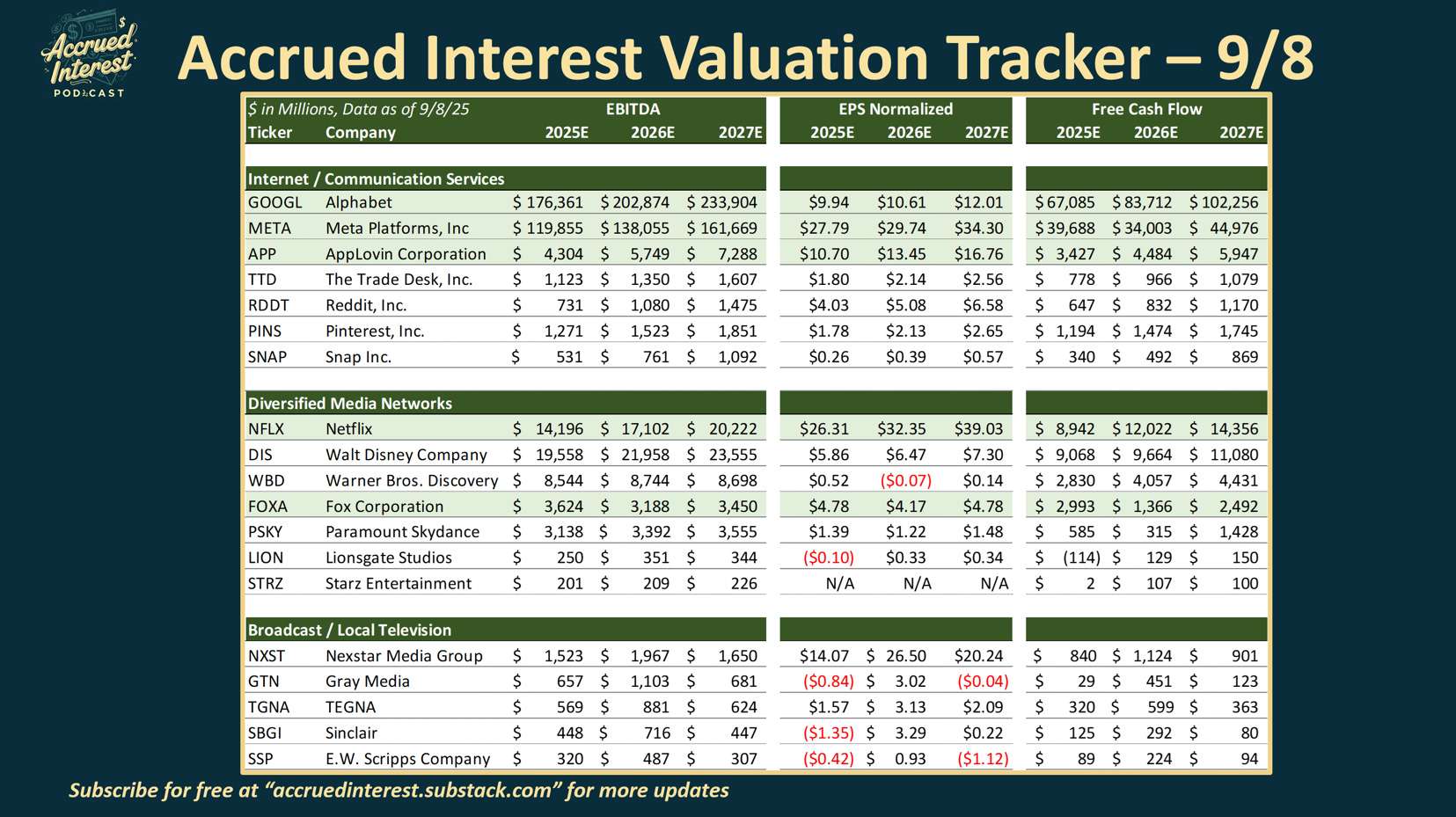

And for those who just want the raw data - here are the average consensus estimates.

Here are a few top trends I wanted to highlight today, in no particular order.

1)Paramount Skydance ($PSKY): Up +37% since 8/12

Paramount-Skydance shares surged in recent weeks. This increase followed the formal closure of their merger and the stock's emergence as a meme stock.

Based on online chatter among day traders on message boards and Reddit forums like WallStreetBets, $PSKY appears to be a meme stock.

Do not short $PSKY. This stock has over 4x leverage, which means even slight changes in valuation or earnings will cause it to either skyrocket or plummet.

Investors' optimism about the new earning potential seems excessive, as I do not yet have a detailed understanding of what is truly achievable.

I am concerned that many investors believe CEO David Ellison can use his father, Oracle founder Larry Ellison's wealth to fund PSKY, enabling it to compete with Netflix and other media companies.

At Accrued Interest, my investment approach focuses on a company's fundamental earnings power. I do not subscribe to blind faith in management, especially without a clear explanation for why "this time will be different." Regardless of the tech buzzwords or discussions of AI and synergies, remember that $PSKY remains, at its core, a legacy media company.

Under the new regime, PSKY has made a significant and costly gamble: broadcasting UFC mixed martial arts matches on Paramount+ and CBS, a move intended to rapidly boost audience numbers.

The UFC is poised for significant growth, due to its departure from the traditional pay-per-view model for major fights, which will increase visibility. However, the sport's inherent violence presents a challenge for advertisers seeking "brand-safe" content, unlike what they typically find with the NFL.

It is uncertain if the tapping into the popularity of the “manosphere” can translate into sufficient incremental advertisers and new Paramount+ sign-ups to improve EBITDA margins to justify the current stock price.

Rating: No recommendation PSKY 0.00%↑ today. But we will be talking a lot about Paramount strategy in the coming months.

2)Alphabet ($GOOGL): Up +15% since 8/12

As previously discussed, Google's stock rose to $200 following strong Q2 earnings. This performance indicated that shifts in consumer Search behavior had minimal impact on the company's profitability.

Last week, GOOG 0.00%↑ stock surged past $230 following a favorable ruling in the DOJ antitrust case. Despite the government proving Google's monopoly status, experts believe the remedies imposed were minimal.

Crucially, Google will not be required to divest Chrome, its browser. The company will also have to "share" some Search data with competitors, though the specifics of this requirement remain unclear.

As expected, the narrative around a stock often follows its price. Analysts who were hesitant to consider the stock at $150 are now comfortable with a position above $230. Google demonstrates that a contrarian approach can be successful even with highly covered large-cap stocks.

One approach to being contrarian is to identify situations where the worst-case scenario has already been factored in. For example, I recognized that many investors were avoiding Google due to fears of a potential breakup or other punitive actions.

Following the case, Google has finally seen its earnings multiple expand.

Since the August 12th, Google's stock has seen its implied Price-to-Earnings (P/E) multiple increase by approximately 3x for each of the next three years. Previously, the P/E ratios were 21x, 19x, and 17x for earnings from 2025 to 2027, respectively. They are now 24x, 22x, and 20x, indicating a consistent 3x increase across these periods.

Google's recent legal victory was ironically aided by the emergence of new AI competitors such as OpenAI and Perplexity. The presiding judge indicated that, given the nascent and disruptive nature of AI technology and its uncertain future trajectory, it would be premature to implement extensive, far-reaching changes while Google is actively contending with these new competitive pressures.

In a key line of the 230-page ruling, Mehta wrote, “The emergence of GenAI changed the course of this case.”

“Judge Mehta said in his ruling Tuesday that he lacked expertise in the business of search engines and A.I., and that “unlike the typical case where the court’s job is to resolve a dispute based on historic facts, here the court is asked to gaze into a crystal ball and look to the future.”

Despite extensive media appearances by Lina Khan on the podcast interview circuit, despite all the promises to “reign in big tech”, the worst has not occurred. I am not a legal expert, but I think some reflection by anti-trust advocates is warranted to understand what went wrong.

For example, during her July interview with acclaimed journalist Pablo Torre (YouTube: "Pablo Torre Finds Out") it was claimed she was the “most feared person in Silicon Valley.” However, I never understood how this could be true, especially given the objective lack of success of the alleged "hipster anti-trust" movement.

I expect $GOOGL to head higher as analysts are no longer afraid to recommend the stock based on antitrust fears. I am seeing price targets being raised to $300 for the first time. However, expect it to take a bit of a breather after such a strong run-up over the last few months. (Barron’s: Can Alphabet Stock Keep Rising After Ruling? What Analysts Think)

Rating: Google ($GOOGL) remains one of my favorite companies and stocks. — Outperform

Recent Accrued Interest articles on Google:

Media Stock Insights from Nielsen’s June-25 TV Snapshot - July 17

Media Stock Insights from Nielsen’s May-25 TV Snapshot - June 17

3 Reasons to Stay Bullish on Google Stock Following Q1 Earnings - May 1

3)AppLovin ($APP): Up +17% since 8/12

AppLovin APP 0.00%↑ is experiencing a recent surge, driven by the announcement of its inclusion in the S&P 500. This addition to the index, effective September 22nd, will necessitate purchases of the stock by portfolio managers tracking the S&P 500 over the next two weeks.

As long-time subscribers of Accrued Interest know, AppLovin is my top stock pick and currently holds the number one position in my personal portfolio. I am thrilled that millions of investors will wake up soon with shares of AppLovin in their portfolio. However, joining the S&P 500 does nothing to enhance the company's intrinsic value.

Although the stock's earnings multiples for 2025 and 2026 suggest it is expensive, I maintain that analyst revenue estimates for 2026-2027 are underestimated.

I anticipate the stock will trade sideways until the Q3 earnings announcement in November, which will be the next major catalyst.

Rating: Stay long $APP, one of the most interesting advertising technology companies I have seen in the last decade. — Outperform

Recent Accrued Interest articles on AppLovin:

-Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.