Media Valuation Tracker Update – Week of Aug 12, 2025

Notes on $RDDT, $APP, $META, $GOOG, $SNAP and $NXST

This is the fifth edition in an ongoing series in which I update my Accrued Interest Multiple Tracker. Today I wanted to focus on some of the biggest changes since last month. My aim for Accrued Interest is to create actionable research materials. You can find past editions here: July 28, July 21, July 14 and July 7.

Almost all of the companies on my TMT tracker have reported Q2 earnings by now. I will be doing a new batch of articles and updates that go deep on many companies individually.

Valuation Tracker Update – Week of Aug 12, 2025

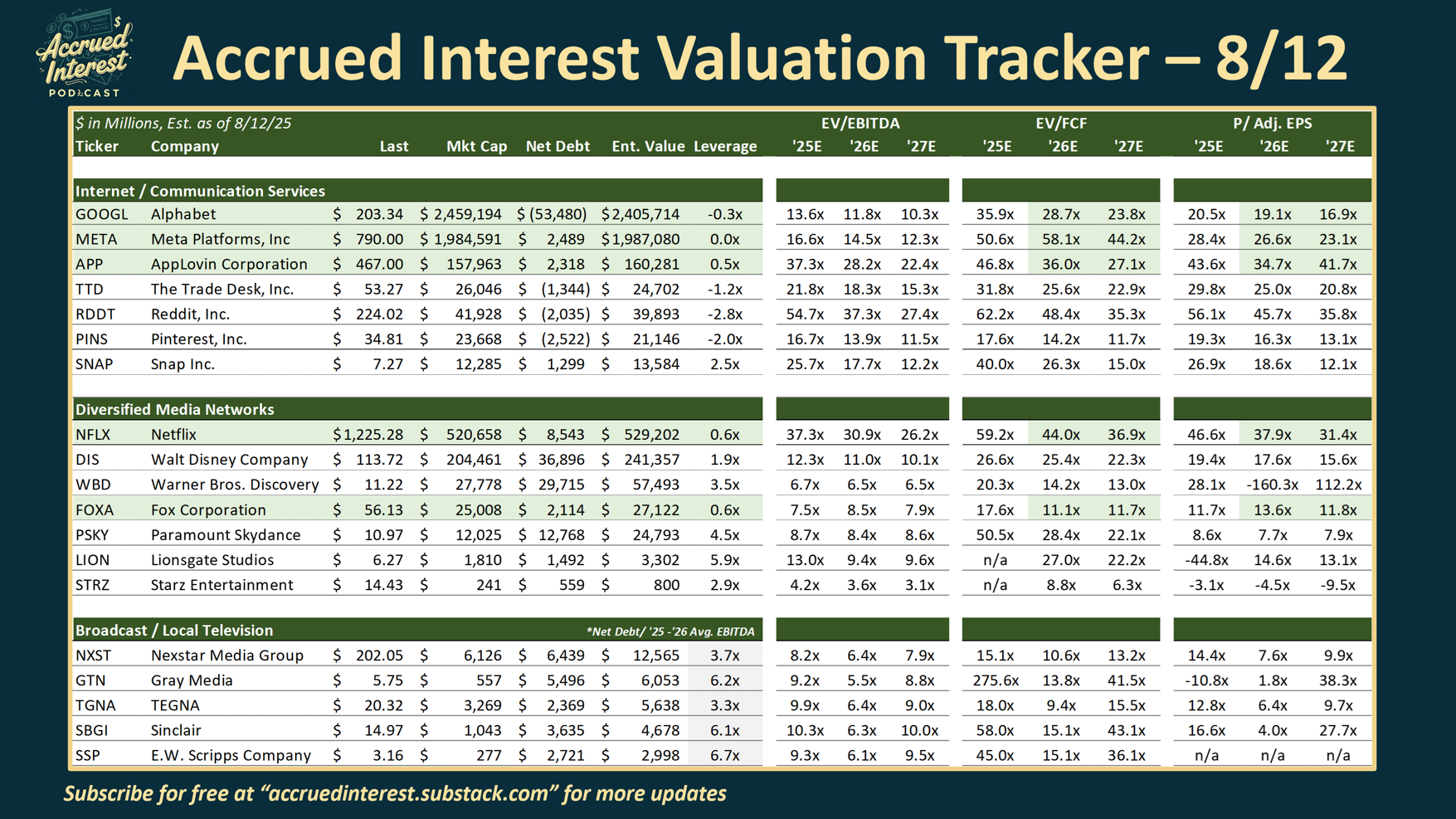

Here is the tracker update with all the company companies' respective multiples for EV/EBITDA, EV / Free Cash Flow (always fully levered), and Adjusted P/E.

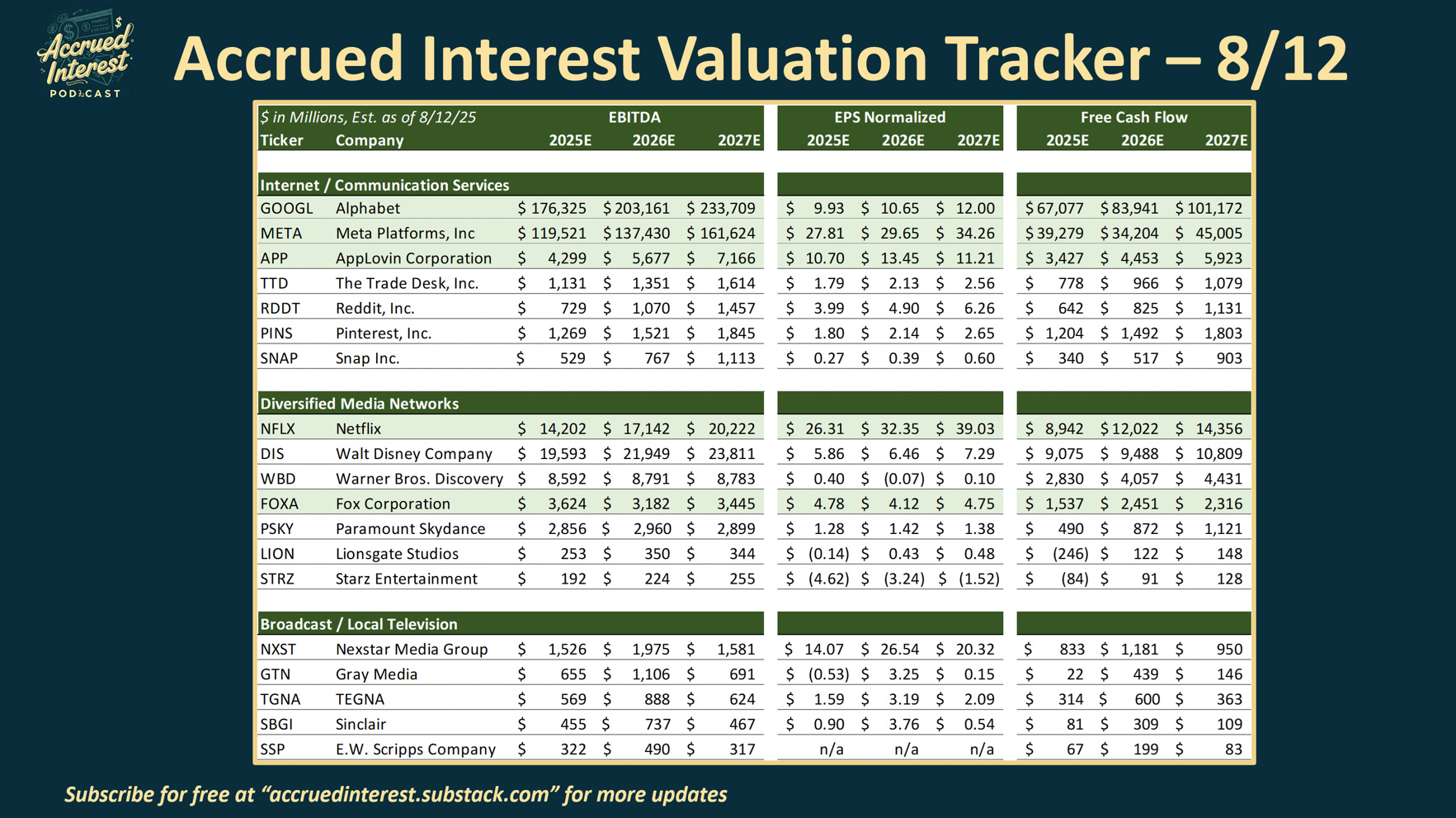

And for those who just want the raw data - here are the average consensus estimates.

Estimate Tracker Update – Week of Aug 12, 2025

Here are the top 6 trends I wanted to highlight today, in no particular order.

1)Reddit ($RDDT): Stock +56% over last month

Stock Price: $228.95 vs. $146.38, up +56%

EV/ 2027 FCF Multiple: 36.1x vs. 25.5x, up +42%

2027 Free Cash Flow Est: $1.1B vs. $984M, up +15%

Guys, on this one I blew it! Missing the rise of Reddit over the past quarter was an error of omission. I knew things were going on with Google but I thought that the multiple was too rich and then I never did the work.

There is nothing wrong with avoiding high multiple stocks, but there are exceptions to every rule. These trackers are designed to generate new ideas.

I should have investigated Reddit earlier. Despite its high multiple, it has demonstrated significant revenue and earnings growth.

I am doing research NOW to understand the company better and look forward to discussing it more in the coming weeks and months!

For now, learn from my mistake and put Reddit on your radar and do not write them off as a meme stock.

Why Reddit is pivoting from social platform to ‘go-to search engine,’ with COO Jennifer Wong

Rating: I have no recommendation on $RDDT today. But make sure to keep this company on your watchlist!

2)AppLovin ($APP): Stock +29% over last month

Stock Price: $459.79 vs. $335.90, up +29%

EV/ 2027 FCF Multiple: 26.6x vs. 21.9x, up +22%

2027 Free Cash Flow Est: $5.9B vs. $5.6B, up +5%

Subscribers of Accrued Interest should be aware by now that AppLovin is my favorite stock. (Full disclosure - it is the #1 stock in my personal portfolio)

APP stock was up +29%, mostly driven by multiple expansion as investors raised their confidence in the company's future growth prospects.

Analysts did not raise their estimates all that much following the Q2 call. Revenue forecasts for 2025 were almost unchanged, but sellside analysts raised their 2026 and 2027 revenue estimates +5% and 6%, respectively.

Last week I discussed how AppLovin quieted many of its most vocal bears. (See AppLovin Q2-25: Where Did the Short Sellers Go?)

Accusations of APP being a fraudulent company or enabling corporate espionage have ceased. The short sellers who were prevalent in recent months have disappeared.

Should you encounter any of these former bears in hiding, please inform them that their self-imposed exile can end. We forgive them for underestimating this company.

Rating: Stay long $APP, one of the most interesting advertising technology companies I have seen in the last decade. — Outperform

Recent Accrued Interest articles on AppLovin:

3)Meta ($META): Stock +9% over last month

Stock Price: $786.47 vs. $720.92, up +9%

EV/ 2027 FCF Multiple: 44.0x vs. 30.1x, up +46%

2027 Free Cash Flow Est: $45.0B vs. $59.5B, down -24%

Meta has been a top performing stock since I have been doing the valuation tracker. In my article last week recapping Meta's strong Q2 earnings, I pointed out how enthusiastic investors were to see ad impression growth of +11% YOY was driving revenue higher. Analysts have raised their revenue estimates for Meta +5% for 2026, and +6% for 2027.

The company announced that the audience on their Twitter rival, Threads, is growing, now with almost 400 million monthly active users. This is how they can get more ad impressions which can generate more future revenue.

Meta’s FCF multiple expanded because the stock went up while free cash flow estimates were lowered post earnings. Investors do not mind Meta spending as much money as needed to compete in AI.

While Meta's current multiple is rich, it is a stock worth owning if it's not already in your portfolio. Their AI advancements are proving effective in both monetizing and driving impressions.

Rating: $META is not cheap after the current run, but you need to own Meta either outright or through a low-cost S&P 500 index. – Outperform

Recent Accrued Interest articles on Meta:

3 Key Takeaways from Meta’s Q1 2025 Earnings Release - May 1

3 Things We Learned About Media Stocks from Meta vs. FTC - April 17

4)Alphabet ($GOOGL): Stock +11% over last month

Stock Price: $202.27vs. $181.56, up +11%

EV/ 2027 FCF Multiple: 23.7x vs. 19.8x, up +20%

2027 Free Cash Flow Est: $101.2B vs. $108.1B, down -6%

I love Google because it is never a high-flying stock. But slowly and surely over time it grinds up to where we are almost looking at all-time highs today.

It is remarkable that Google's over $200 per share, despite the wall of worry they have climbed. Although often seen as a search monopoly, the company has consistently faced skepticism in competition with smaller, agile firms like OpenAI.

As I explained in my Q2 recap of Google’s earnings, the company is proving the naysayers wrong, through strong execution.

Over the past month, analysts raised Google's revenue estimates slightly by +2% for 2025 and 2026 each. But over the past month the street FCF forecast for 2026 / 2027 came down, about -7% and -6%, respectively. Similar to Meta, but not to the same extent, Google is ramping up capital expenditures to compete in AI.

I expect $GOOGL to head higher, as the market gets clarity over some of antitrust concerns. A federal judge is expected to issue a ruling on the government's antitrust suit against Google's search business by the end of August.

Rating: Google ($GOOGL) remains one of my favorite companies and stocks. — Outperform

Recent Accrued Interest articles on Google:

Media Stock Insights from Nielsen’s June-25 TV Snapshot - July 17

Media Stock Insights from Nielsen’s May-25 TV Snapshot - June 17

3 Reasons to Stay Bullish on Google Stock Following Q1 Earnings - May 1

5)Snap, Inc. ($SNAP): Stock -24% over last month

Stock Price: $7.23 vs. $9.54, down -24%

EV/ 2027 FCF Multiple: 15.0x vs. 16.9x, down -11%

2027 Free Cash Flow Est: $1.0B vs. $903M, down -11%

Snap's stock was down -24% over the last month, with only The Trade Desk ($TTD) showing comparable movement down -29%. While I have not discussed Snap previously on the Substack, its recent underperformance warrants attention.

For benchmarking purposes, Snap will always be included in my tracker due to its presence in the digital advertising sector. I also monitor their products and innovations, as their successful offerings often inspire similar developments from competitors.

However, it is important to clarify that I do not consider Snap an investable company.

$SNAP has had ample time to establish itself as a formidable competitor to Meta, but that window has passed.

While I do not endorse shorting stocks, I strongly advise against long positions in Snap.

Rating: Avoid $SNAP. It is not an investable company — Underperform

6)Broadcast Television Stocks

Over the past month, broadcast television stocks have traded as a mixed bag. Companies that announced deals were up, while others were volatile.

Nexstar Media Group ($NXST) was up +8% and its intended M&A target, Tegna ($TGNA), was +17%

Others such as Scripps ($SSP) were down -15%, and Sinclair ($SBGI) down -5%, but those stocks continue to be volatile day-to-day.

Again, I am not telling anyone to go short on all broadcast television stocks. I am just pointing out that there is almost no organic revenue growth left in this industry.

Until we close some deals - all these stocks are going to be trading vehicles that rise and/or fall based on speculation.

For the Broadcast Bulls…

Let me note a few macro events that could support broadcast TV stocks in the short-to-medium term:

It would be a positive for broadcast stocks if the Fed lowers interest rates more quickly, because they all have highly levered balance sheets.

Recent announcements that more sports are coming to linear television could hold the pay TV bundle together just a little longer.

UFC fighting is coming to CBS and Paramount+, leaving behind the PPV model. And beginning in 2026, ESPN's new direct-to-consumer service will feature all live premium WWE events, and ESPN will simulcast select events on linear.

Remember, even if all regulations go away tomorrow, Nexstar cannot buy out the industry. So be careful when you see broadcast stocks spiking green, because not every company will be able to find a dance partner before the M&A music stops playing. If you want a broadcast stock I am certain will be around in 3 years, look at Fox Corporation. I published my stock pitch on $FOXA here.

Rating: Except for Fox, none of the broadcast stocks are 2-year holds. If you want to speculate on short-term gains, bet on the companies that are cashing out, like Tegna, and avoid the buyers left holding the bag, like Nexstar.

Recent Accrued Interest articles on broadcast TV stocks:

Fox Corp ($FOXA): Unlocking Hidden Value in Gambling & Streaming - July 19

Media Stock Insights from Nielsen’s June-25 TV Snapshot - July 17

Interview – Nexstar Media Group: Broadcasting's Biggest Bet ($NXST) - June 25

CONCLUSION

I will be analyzing more individual companies in the coming days and weeks. Earnings season provides a wealth of new data, and I am eager to delve into it and share my findings with you.

If you find this information valuable, please subscribe and share this publication. A limited paywall will be implemented in certain sections before the end of the year, so subscribe now to take advantage of preferential pricing for early subscribers!

-Accrued Interest

You can always reach me at simeon@accruedint.com.

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.