Media Stock Insights from Nielsen’s Sep-25 TV Snapshot

YouTube Extends Lead, While Netflix Stalls Below 9%

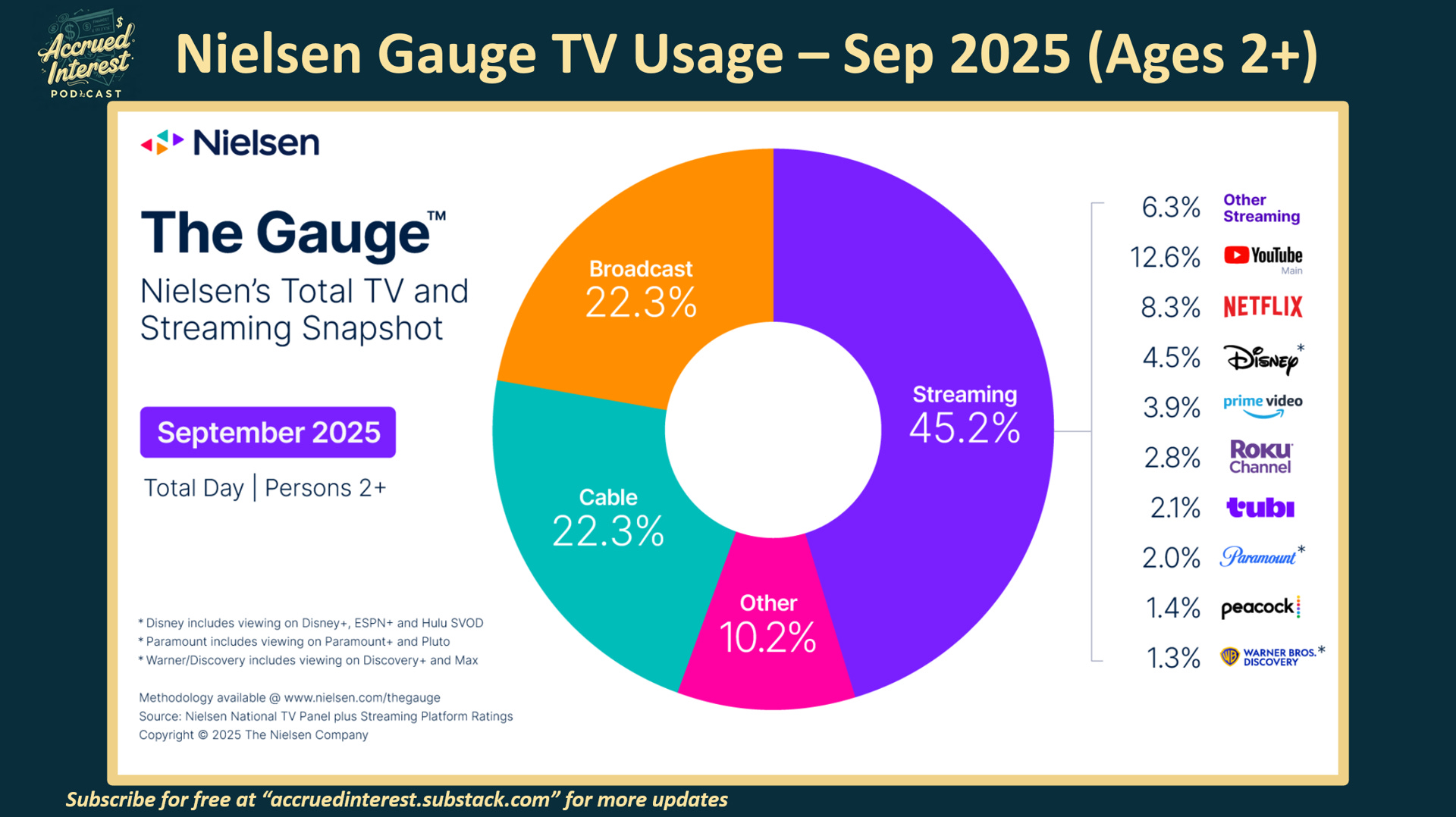

Nielsen is out with its Sep 2025 Gauge report, exploring what Americans are watching on their big screen televisions (excluding mobile devices). YouTube is again #1 with 12.6% of all TV viewing in America.

Here are the 3 major themes from the September report:

YouTube GOOGL 0.00%↑ continues to have YoY share gains (+2 share pts) that are larger than the entire audience of many services.

Netflix, NFLX 0.00%↑ still cannot grow its audience share above 9%. I think expanding into podcast content will take them to the next level.

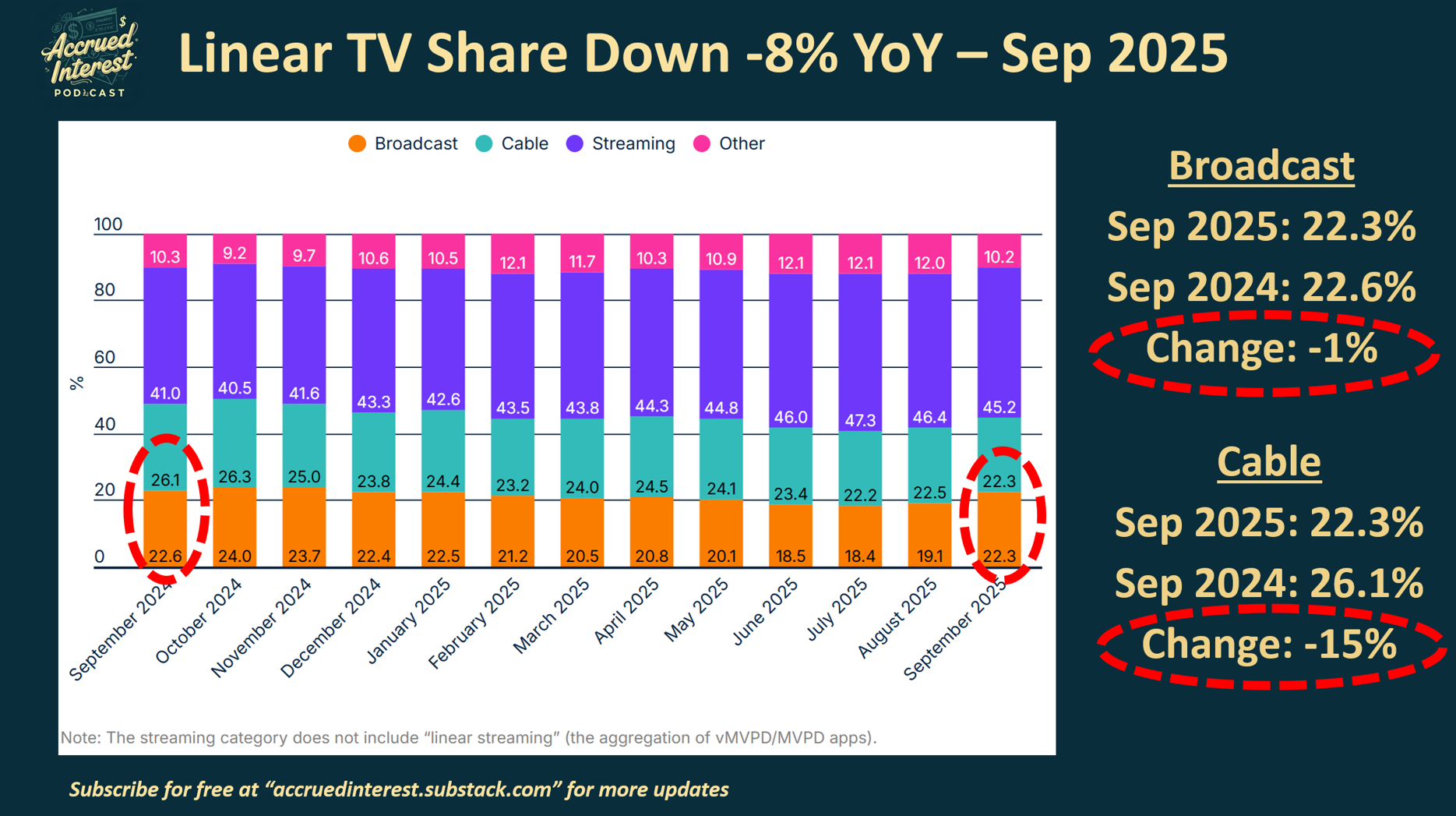

Cable audience declines accelerated to -15% YoY, with broadcast gains unable to fill the losses.

I have been reporting on YouTube’s rise all year. Check out past monthly updates here: Aug, July, June, May, April, March, Feb and Jan.

Here are the key takeaways from the September report…

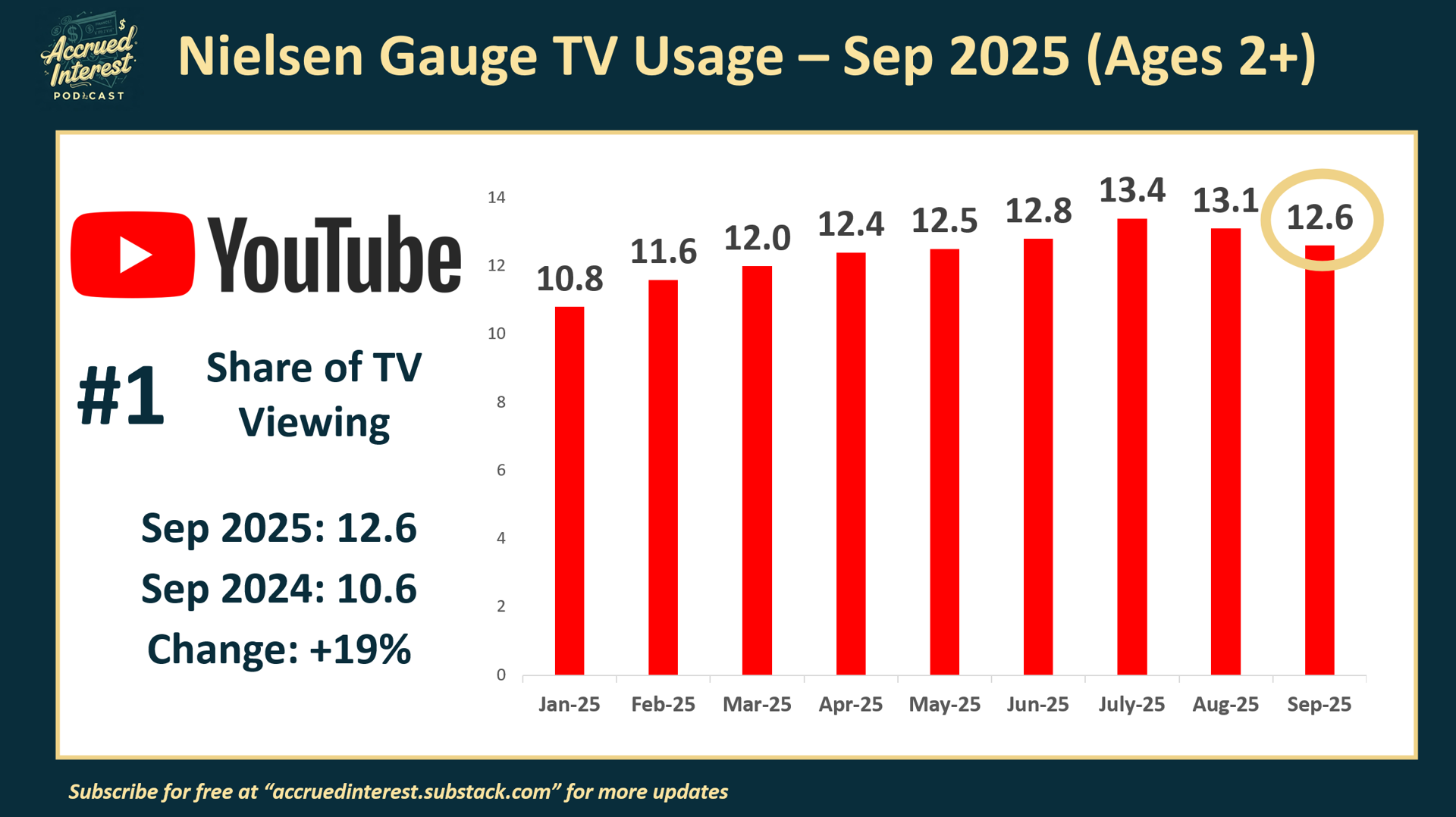

1) YouTube ($GOOGL) is still #1 with the highest YOY growth, but now under 13% share

YouTube’s viewership share decreased to 12.6% this quarter, down from 13.1% in August. This marks the second consecutive monthly decline, with July’s 13.4% remaining the highest point to surpass.

The September numbers were the first full month to include both college and NFL football games, so I believe this pullback is perfectly normal and expected.

YouTube continues its remarkable growth, increasing its year-over-year viewership by +19%, up from 10.6% a year ago. This expansion is particularly notable given YouTube’s already substantial user base that is 3x - 5x the size of other services.

YouTube also once again led in year-over-year share growth, increasing by 2.0 share points.

I believe YouTube can continue to gain market share at an impressive rate because its focus on user-generated content (UGC) ensures a constant influx of new shows and podcasts.

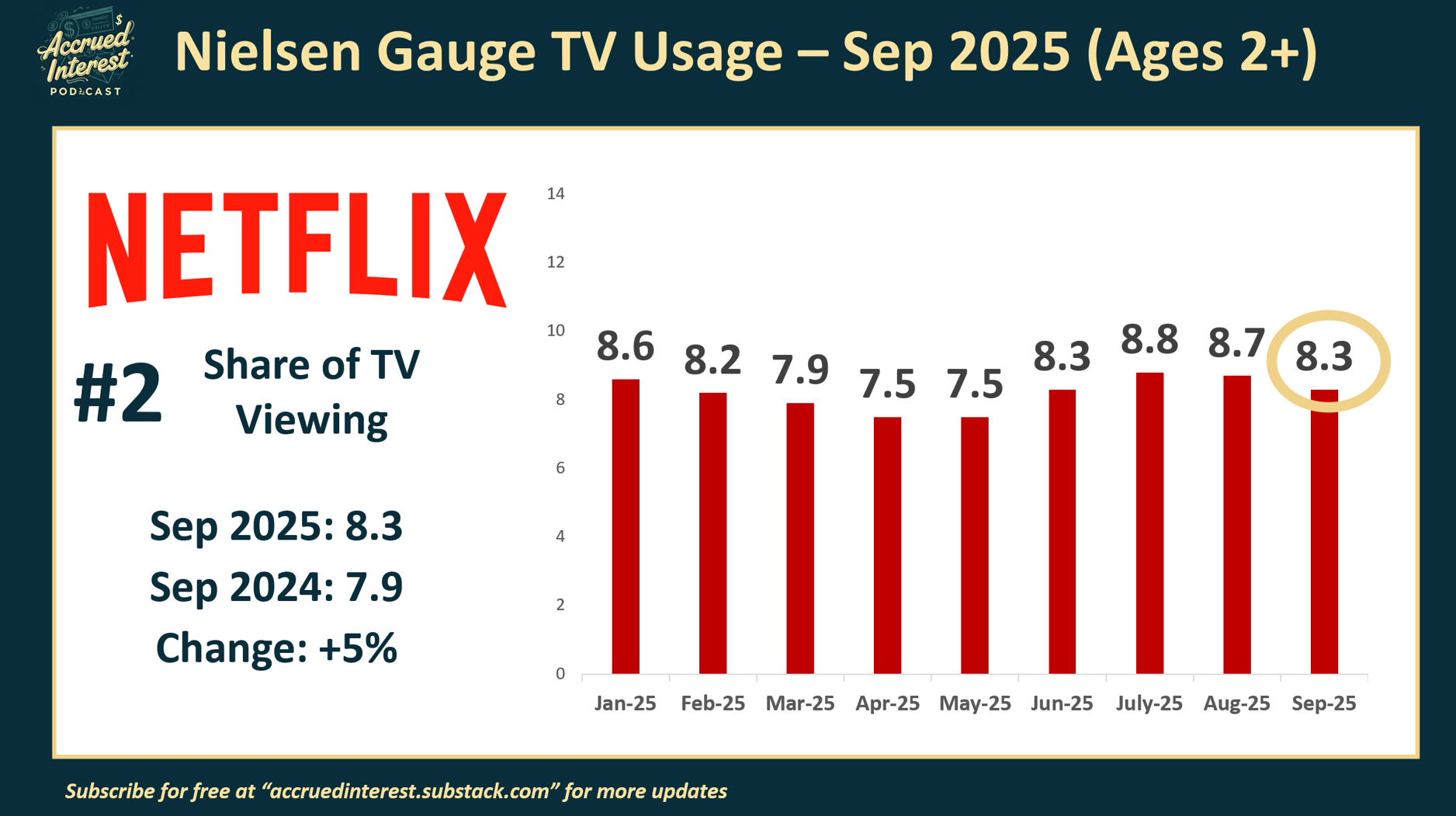

2) Netflix ($NFLX) was #2 with 8.3% share, still unable to get above 9%

Netflix’s share in the Nielsen report decreased to 8.3% in September, a quarter-over-quarter drop from 8.7% in August. The service’s all-time high remains 8.8% in July.

On a percentage basis, NFLX 0.00%↑ was up +5% YoY, from 7.9% last Sep-24.

While Netflix has yet to gain enough momentum to unseat YouTube from the #1 position, securing the #2 spot on U.S. big-screen televisions is still a commendable achievement.

Netflix’s audience size remains nearly double that of its closest legacy media competitor, Disney.

Disney’s 4.5% total in the Nielsen study represents a combined measurement of Disney+, ESPN+, and Hulu SVOD. Nielsen recently altered its methodology for assessing Disney-owned services, so year-over-year comparisons using this new combined figure will not be available for several months.

To break through the 9% ceiling, Netflix will require more major sporting events, such as the upcoming Jake Paul vs. Gervonta Davis boxing match in November and the two NFL games scheduled for Christmas Day.

Netflix’s recently announced partnership with Spotify, which will bring 16 video podcasts from Bill Simmons’s The Ringer, indicates that Netflix is poised to significantly expand its presence in the podcasting landscape in the coming years.

Podcasts offer NFLX a way to engage current subscribers, encouraging them to spend more time on the service. This format often features shows with numerous episodes and higher advertising loads compared to scripted content.

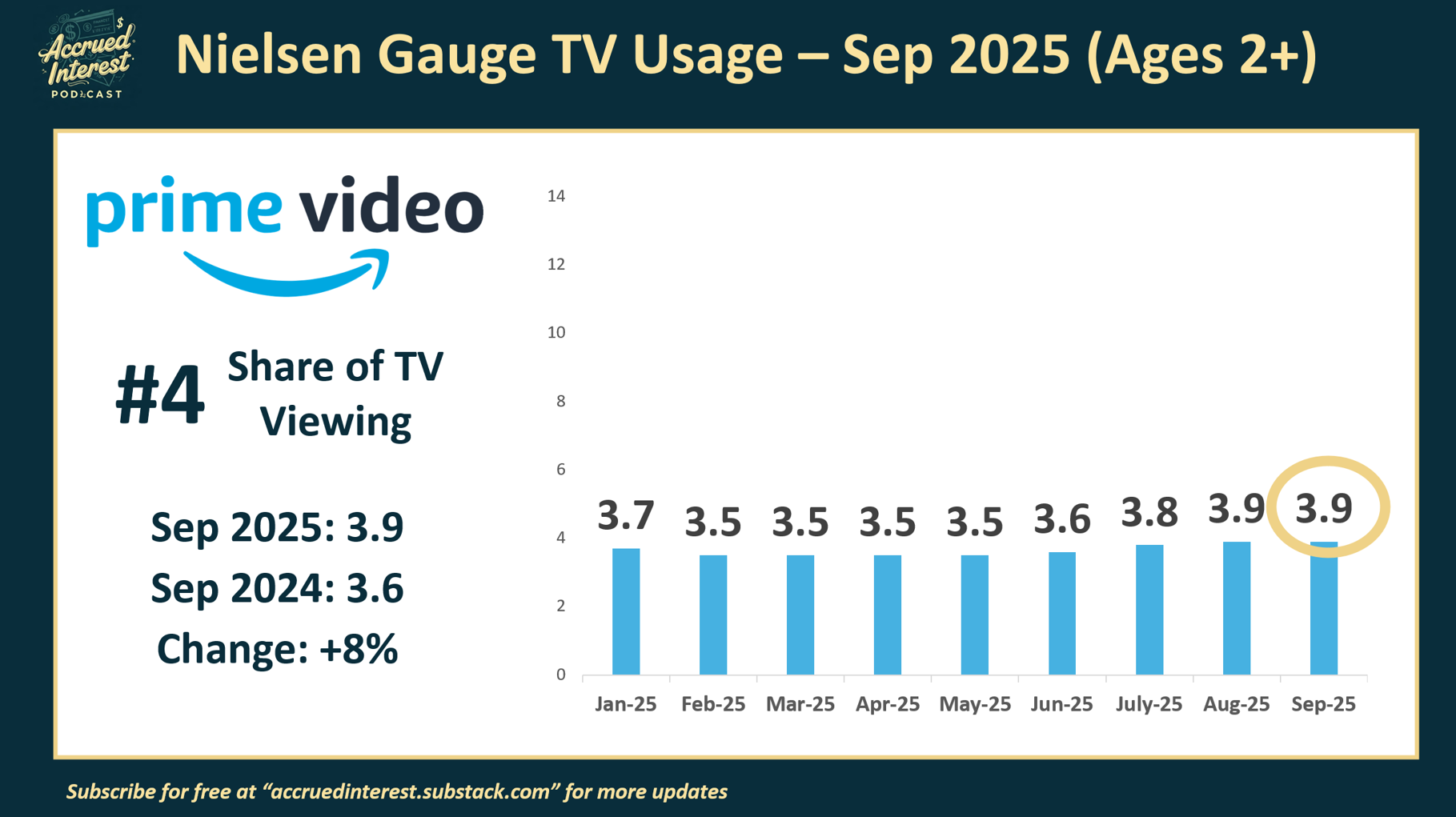

3) Prime Video ($AMZN) was #4 with 3.9% share

Amazon’s Prime Video posted a +8% YoY change, going from 3.6% to 3.9%

AMZN’s viewership has consistently hovered between 3% and 4% over the last year, showing no sustained growth, and September’s figures align with this trend.

I anticipate Amazon’s viewing share will start to grow in October and November due to the introduction of NBA games as a new league partner.

Amazon’s status as “The Everything Store” for millions of Americans provides advertisers with strong incentives to purchase Prime Video advertising, extending beyond mere audience viewership.

Amazon strongly encourages advertisers to buy Prime Video ad space by offering financial incentives, using proprietary customer data for precise targeting, leveraging its massive audience, and developing innovative, shoppable ad formats

I favor ad-supported streaming models over subscription-only options. However, I do not have a recommendation for AMZN 0.00%↑ shares.

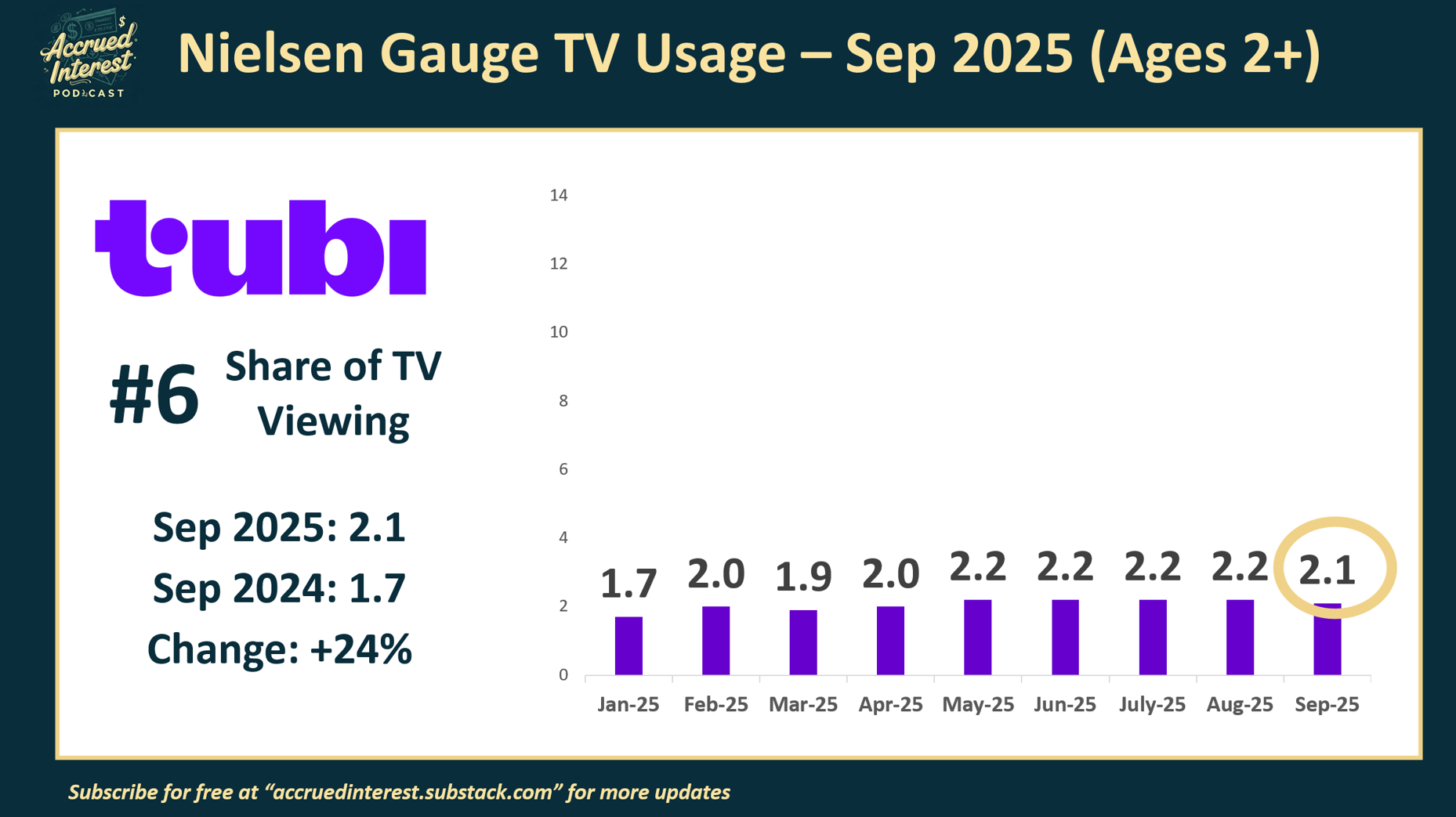

4) Tubi ($FOX / $FOXA) was #6 with 2.1% share

Tubi’s viewership saw a healthy 24% increase, rising to 2.1% from 1.7% in September 2024. However, I anticipate a decline in year-over-year gains as we approach February, which marks the one-year anniversary of Fox’s, FOXA 0.00%↑ free Super Bowl simulcast on Tubi.

Overall, Tubi viewership remains solidly in the 2% range without much monthly fluctuations.

Given that Tubi is a Fox Corporation-owned free, ad-supported streaming service (FAST), it’s notable that its viewing share surpasses that of HBO Max WBD 0.00%↑ , Paramount+ PSKY 0.00%↑ , and Peacock CMCSA 0.00%↑ .

5) Cable losses accelerate, while brodcast rebounds

Let me start with some positive news for linear TV, so I don’t sound like a perpetual pessimist about broadcast. In September, broadcast television accounted for 22.3% of TV viewing, marking a 20% increase from 19.1% in August.

The spike was mostly due to the return of college and NFL football, helping broadcast gain 3.2 share points, for the latest monthly increase in the history of Nielsen’s The Gauge report.

Now for the bad news for linear investors – cable share was down -15% YoY, falling from 26.1% last year, losing 3.8 share points. Combined (cable + broadcast) saw an -8% YoY decline.

Bad news for linear investors: cable share plummeted by 15% year-over-year, dropping from 26.1% and losing 3.8 share points. The combined share of cable and broadcast also declined by 8% year-over-year.

M&A drama is still playing out in the headlines - with Warner Bros. Discovery formally announcing this week it “has initiated a review of strategic alternatives to maximize shareholder value.”

The fact that I rarely mention Paramount, Peacock or WBD in these monthly Nielsen updates is not an accident. I cannot recommend investing in their parent companies until I observe concrete gains in their viewership.

-Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.