Media Stock Insights from Nielsen’s Oct-25 TV Snapshot

YouTube ticks up again; Roku is here to stay

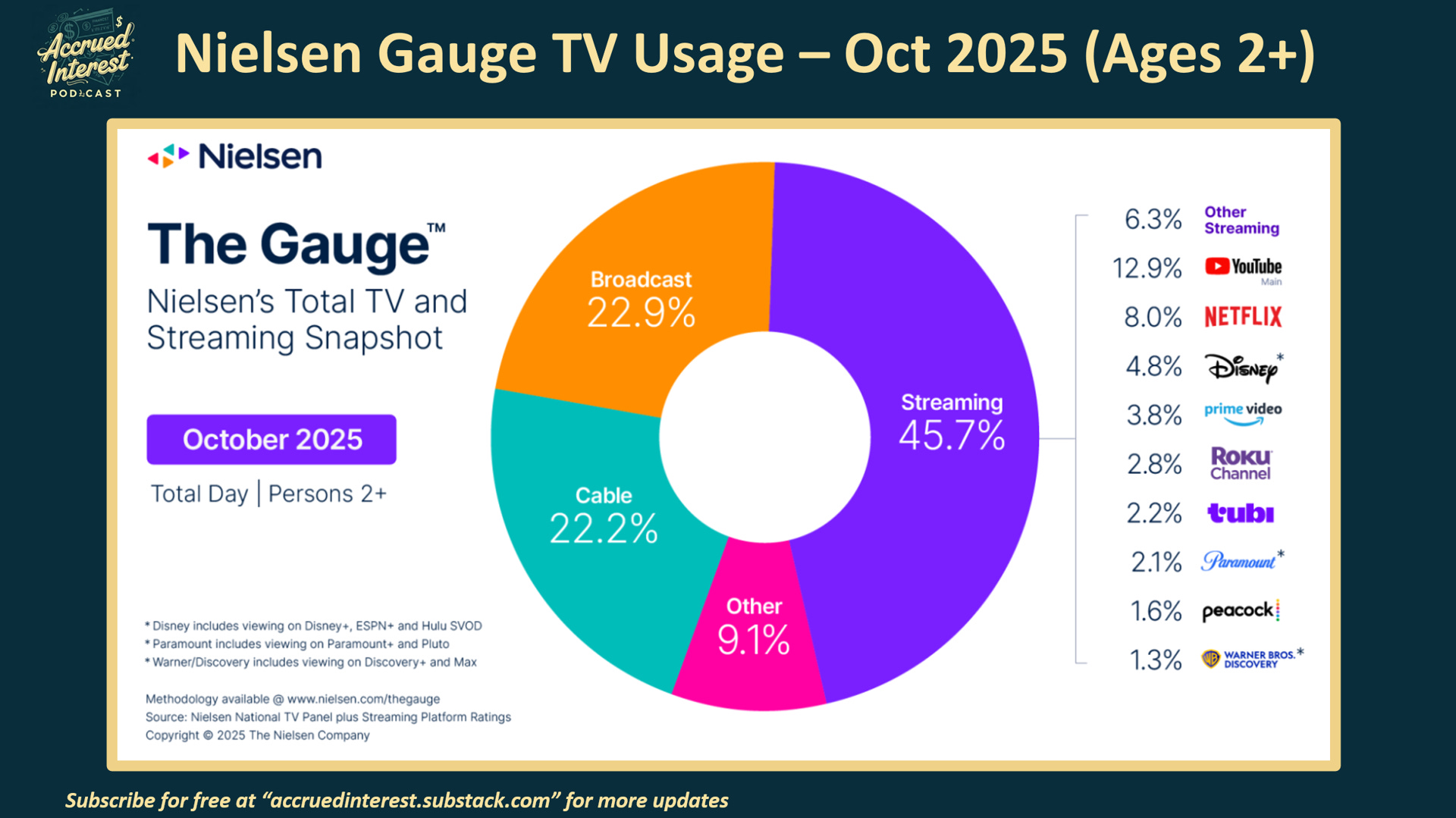

Nielsen is out with its October 2025 Gauge report, exploring what Americans are watching on their big screen televisions (excluding mobile devices). YouTube is again #1 with 12.9% of all TV viewing in America.

Here are the 3 major themes from the October report:

YouTube, GOOGL 0.00%↑ continues to have YoY share gains (+2.3 share pts) that are larger than the entire audience of many services.

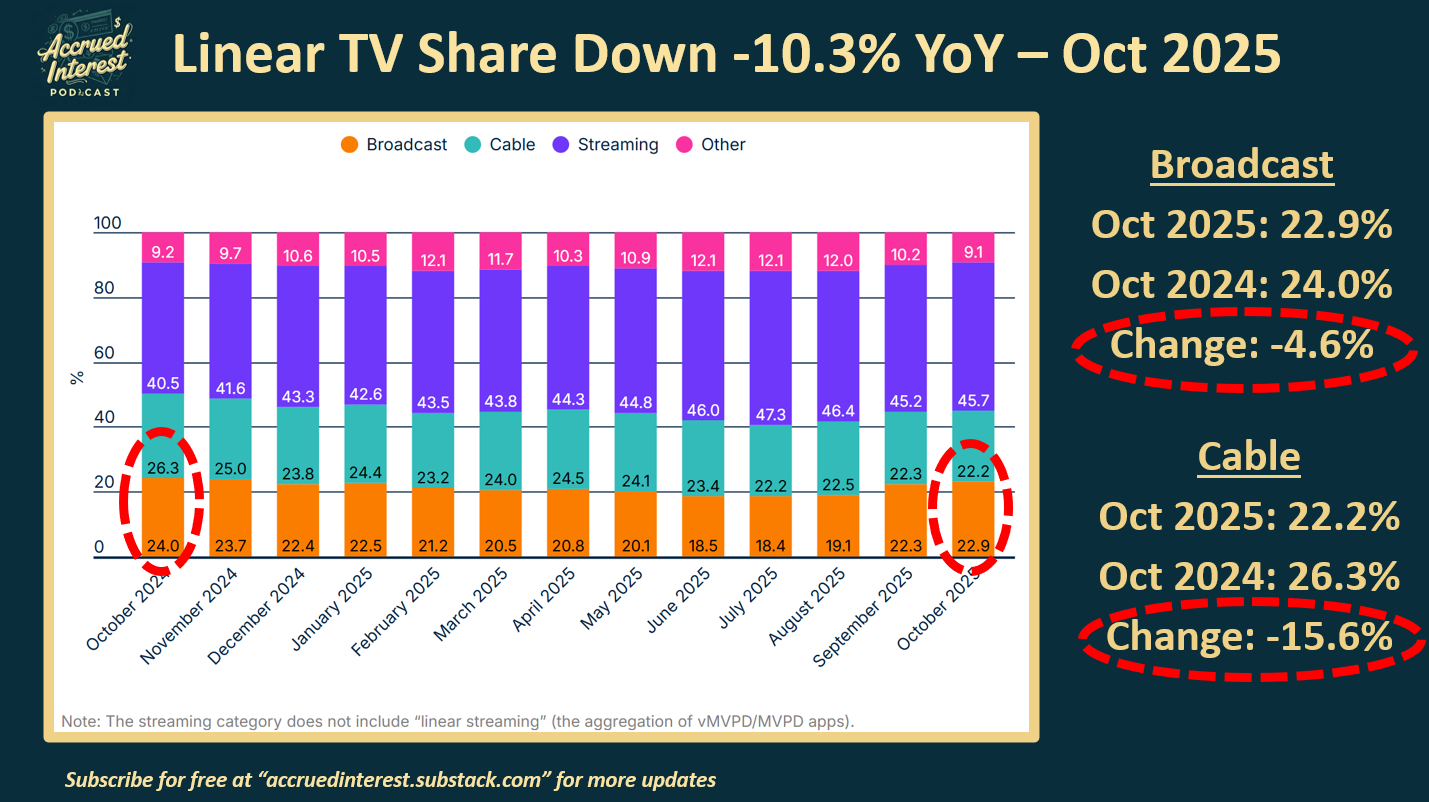

Linear share losses show no signs of abating. Cable audience decline increased slightly to -15.6% YoY, with broadcast down -4.6% YoY. Winning WBD will not fix this!

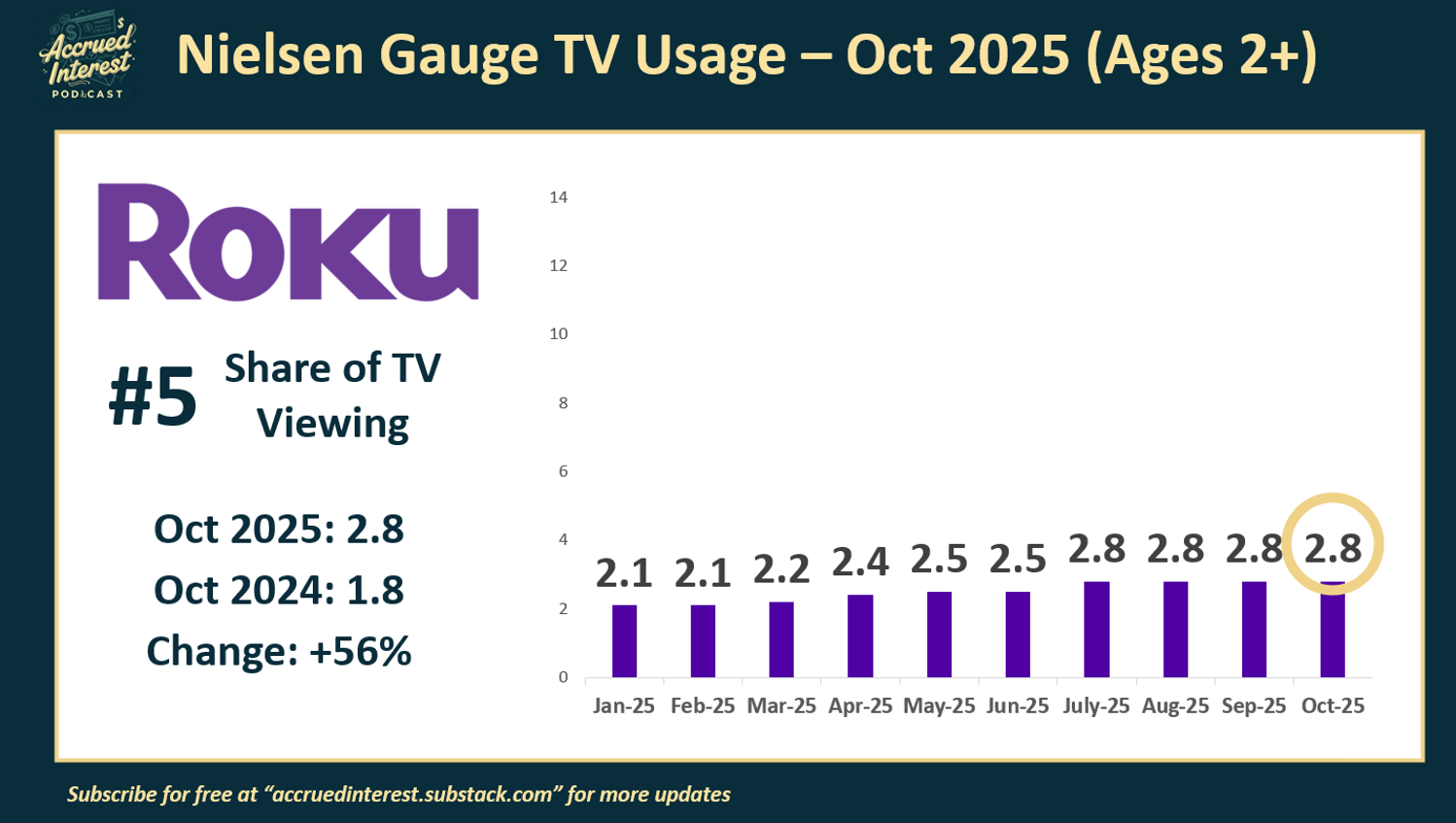

I added Roku, ROKU 0.00%↑ to my monthly rundown, as they are #5 with 2.8 share - more than any legacy player except for the Disney, DIS 0.00%↑ family.

I have been reporting on YouTube’s rise all year. Check out past monthly updates here: Sep, Aug, July, June, May, April, March, Feb and Jan.

Here are the key takeaways from the October report…

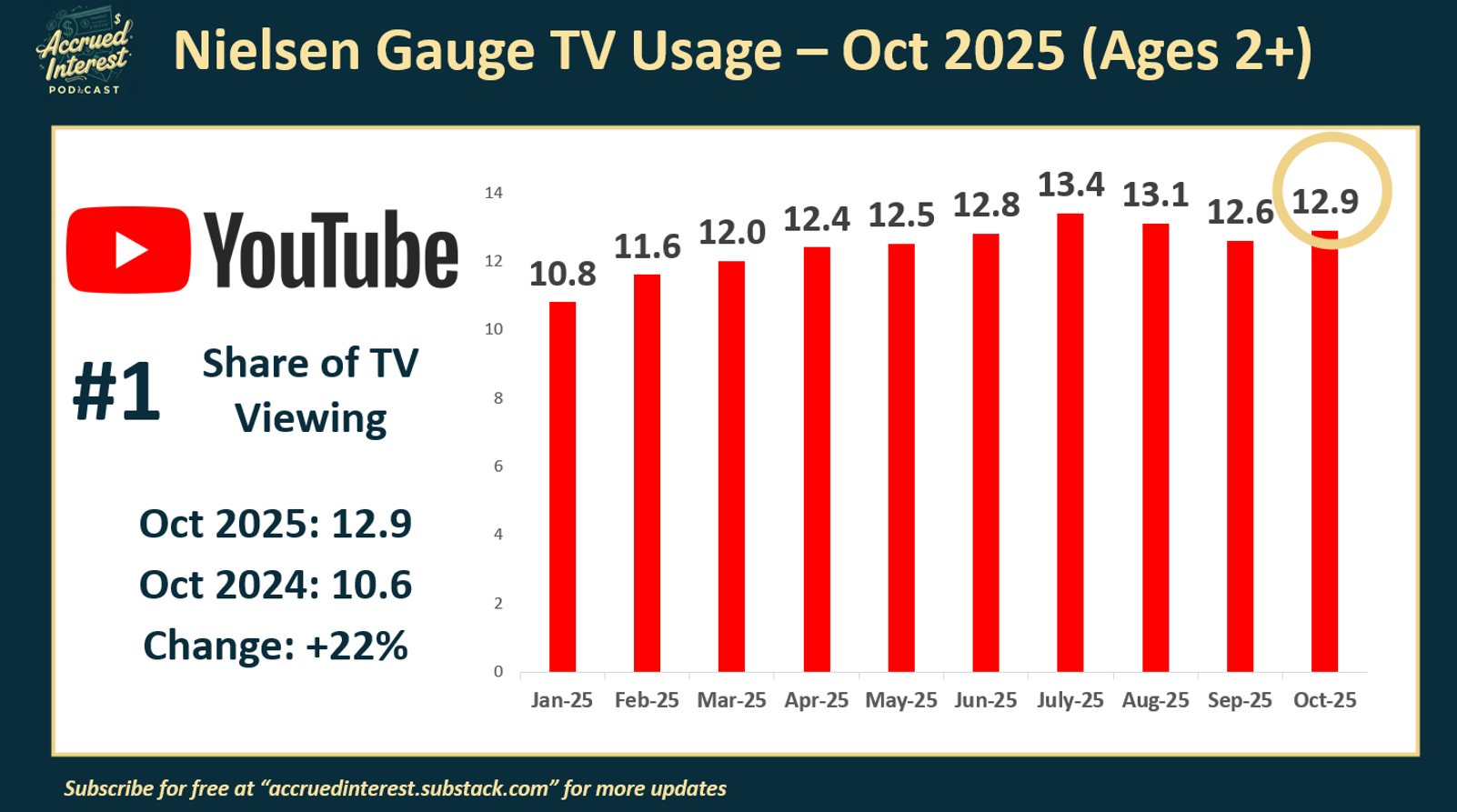

1) YouTube ($GOOGL) #1 with 12.9% share, up +22% YOY and close to 13.1% all-time high in Aug

YouTube’s viewership share showed a sequential increase to 12.9% last month, up from 12.6% in September. This is the first monthly uptick since June. July’s 13.4% is still the all-time high for YT and we saw slight declines through Aug - September.

It is noteworthy that YouTube GAINED in October because more sports were on the air and yet, Broadcast and Cable could not take share from YT.

I want you to focus on the +22% increase from October 2024.

If you read the summaries on Nielsen’s blog, you will notice that it is written to portray their legacy TV clients in a more favorable light. I urge you to look at the annual changes because this is where you can see YouTube pull away from the pack.

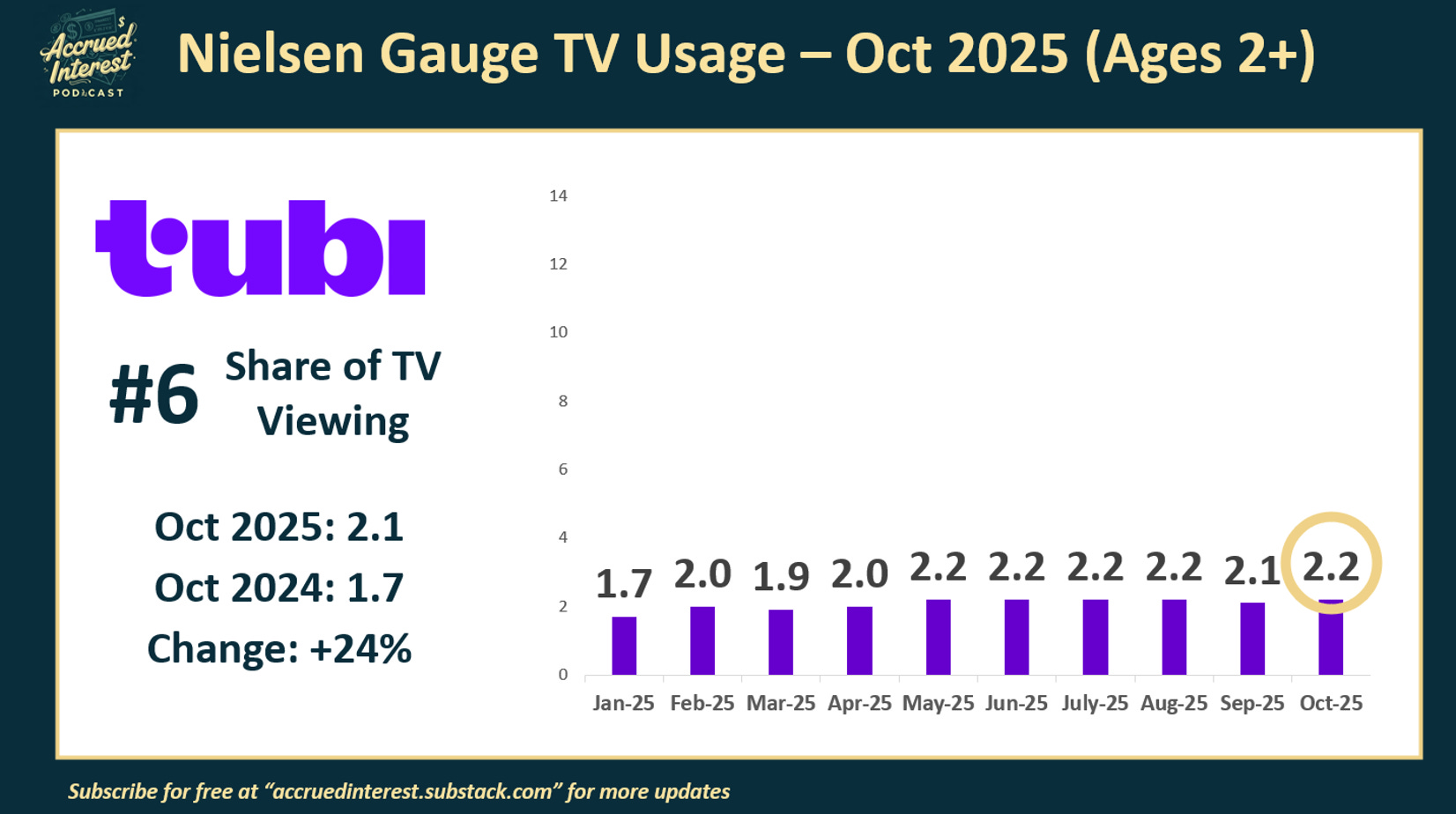

The +2.3 pts of viewing share GAINED over the last year, is equal to the entire audience of Tubi (#6 in this month’s rankings and owned by Fox Corporation)

No other service gained as much absolute viewing share as YouTube.

A fact I think should scare legacy media investors is that these YouTube figures are for “classic” YouTube, NOT YouTube TV - the over-the-top streaming service that acts as a cable replacement delivering live TV channels.

YouTube TV and Disney just concluded a very public fight over the cost of carrying Disney’s cable channels, including ESPN. People are quickly realizing that YouTube TV got the better of Disney. We will discuss the strategic implications of that carriage dispute in future posts…but it should not make more bullish for Disney.

Again - totally separate from the 12.9% viewing share YT discussed above, YTTV has 10 million paying subscribers. This makes it the FASTEST growing major TV provider during the post-COVID period. (They were at about 2 million subs in late 2019, for context).

Google’s TV service is the #3 pay TV provider in the U.S. Only Comcast and Charter are bigger. It is very possible that in a few years Google surpass them and they end up with even more power over the U.S. television industry.

I have spent a LOT of time discussing YouTube all year because I have super bullish on Google’s stock. With GOOGL 0.00%↑ reaching new all-time highs, crossing $300 per share, I feel vindicated for talking so much about YouTube.

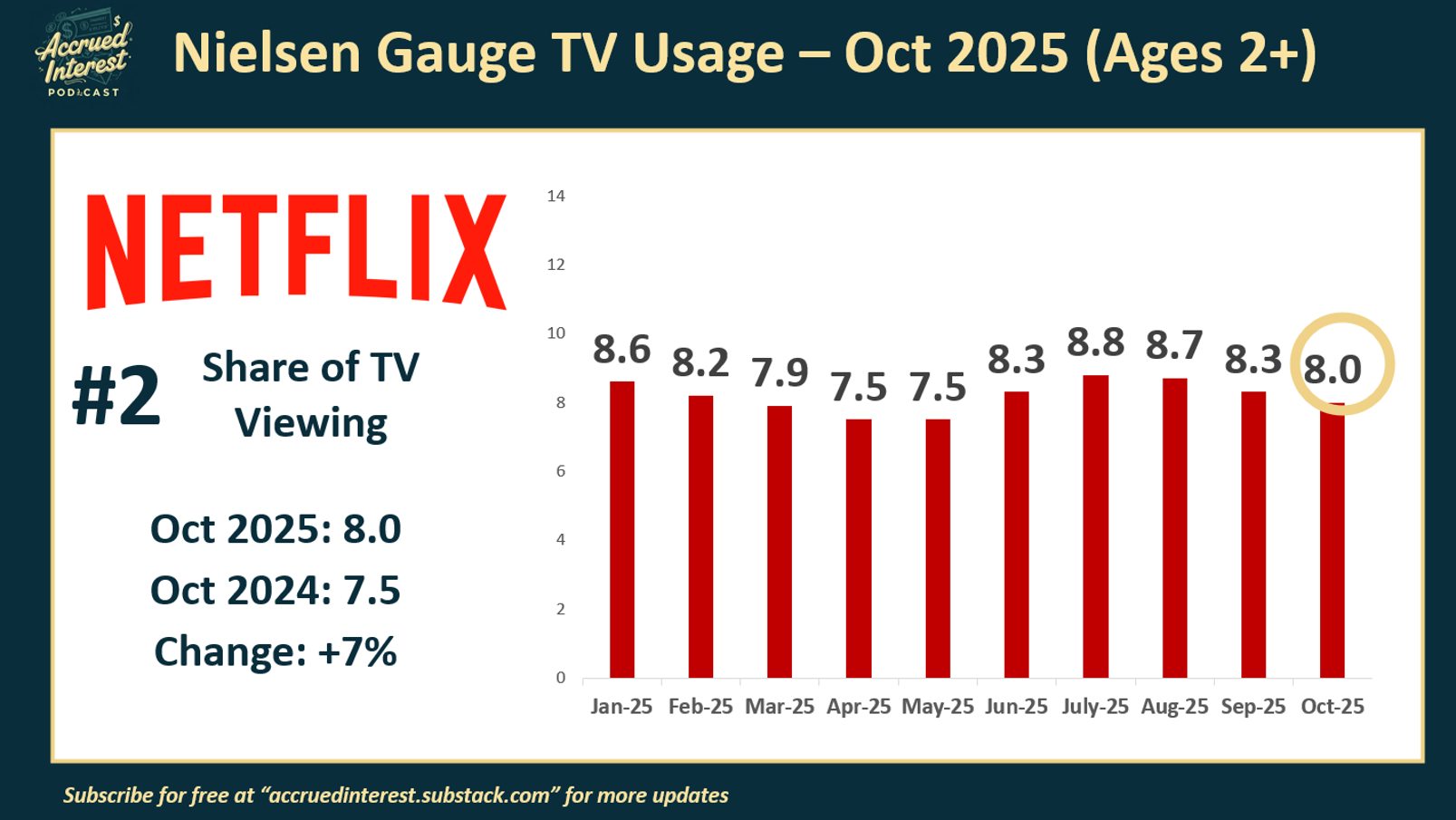

2) Netflix ($NFLX) was #2 with 8.0% share, still unable to get above 9%

Netflix’s share in the Nielsen report decreased to 8.0% in October, a quarter-over-quarter drop from 8.3% in September. The service’s all-time high remains 8.8% in July. This is the 3rd sequential down month since July.

However, on a YoY basis, NFLX was up +7% YoY, from 7.5% last October-24.

As I have highlighted in past updates, Netflix’s share of TV viewing has hit a bit of a ceiling in the U.S. The company is still in an enviable position as a strong #2 with a huge 4.9 pt GAP between 3rd place, which is Disney* (which includes Disney+, ESPN+, and Hulu SVOD).

I would not be surprised to see NFLX viewing share rise again as we head into Nov/Dec of 2025 as they have some marquee sporting events scheduled late in Q4.

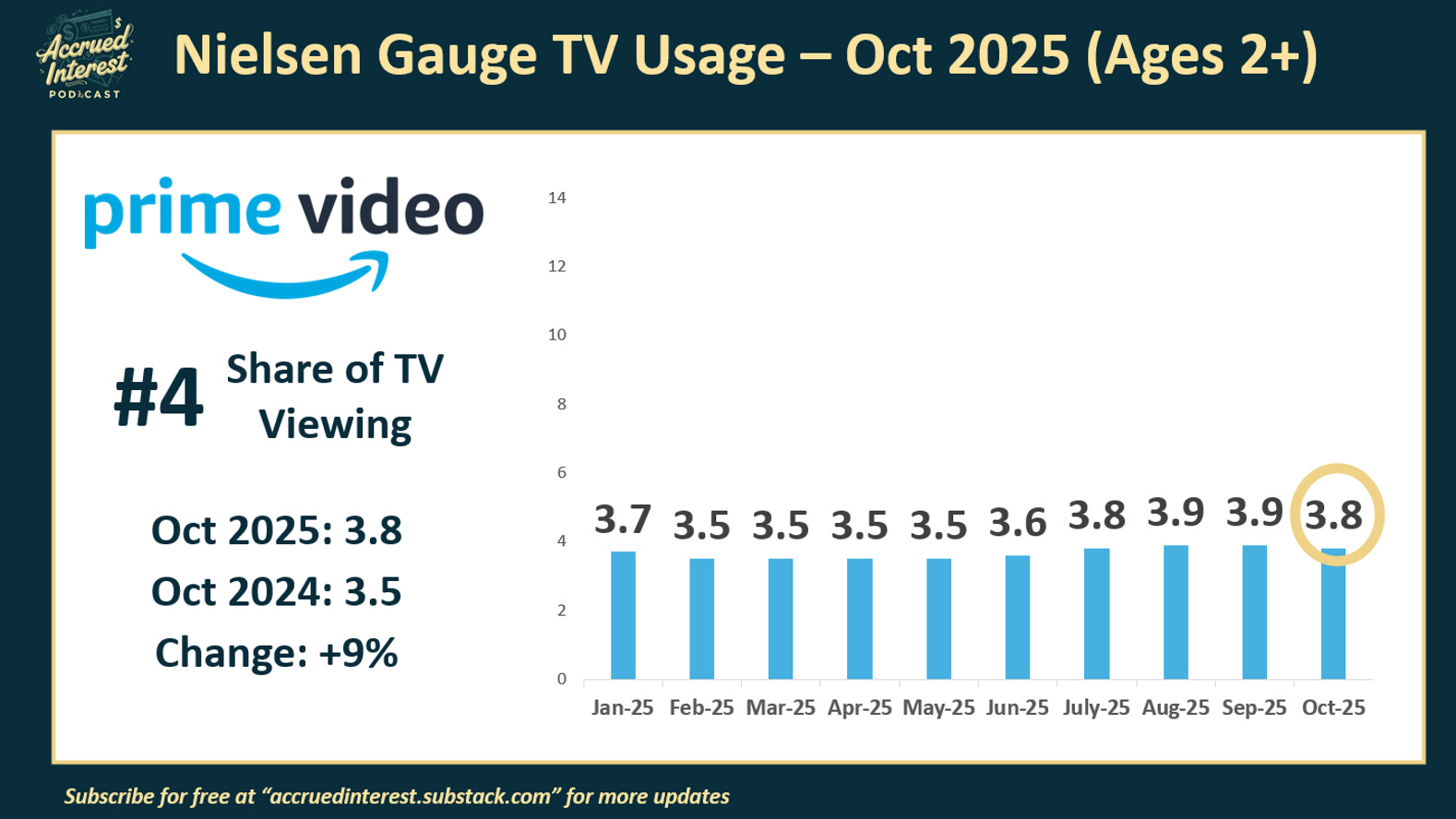

3) Prime Video ($AMZN) was #4 with 3.8% share

Amazon’s Prime Video posted a +9% YoY change, going from 3.5% to 3.8%

AMZN’s viewership again hovers just below 4%.

I still anticipate Amazon’s viewing share will start to grow eventually due to their increased sports focus. This is their first year as an NBA partner.

4) Roku ($ROKU) was #5 with 2.8% share

Readers will note this is my first time including Roku in my summary. My apologies, I should have done it sooner! Roku ROKU 0.00%↑ is unique because the company is a platform to watch other video content (NFLX, YouTube) while having their own originals.

I chose not to highlight Roku in past updates because their 2.8% share has been stagnant since July. The mistake I made was in forgetting to look at the year-over-year change. Their +1.0 share gain vs. last October was DOUBLE the +0.5 share gain of Netflix.

The +56% YOY change is high because it is growing off a small base, but it should not be ignored. Roku is yet another new-media, digital-first, competitor taking share from the legacy media providers.

5) Tubi ($FOX / $FOXA) was #6 with 2.2% share

I remain a huge believer in Tubi, FOXA 0.00%↑ and think it is still an underrated player in the streaming television race. Its 2.2 share in October has it at #6, ahead of more well known legacy media players such as Peacock (NBC - 1.6), Warner Bros Discovery (1.3).

Tubi is essentially tied with Paramount+, PSKY 0.00%↑ which has 2.1% share. But PSKY’s total includes both Paramount+ and Pluto.

With Fox Corporation stock sitting at fresh all-time highs, investors are bullish that Tubi can be incremental to profits in 2026 and 2027.

6) Linear losses accelerate, with both broadcast and cable down YoY

Another month goes by and it is still the same story for the legacy media. They continue to lose share at a pace that makes most of them uninvestable.

I seriously recommend you read the October summary from Nielsen’s blog and compare / contrast it with my article here. You will notice Nielsen spends a lot of time discussing the positive impact the NFL had on broadcast viewing. I do not mean to be cynical, but Nielsen tries to craft a story that puts the linear TV networks in a more POSITIVE light because they are clients of Nielsen’s ratings measurement services.

Notice how they compare October to September, and not to October 2024.

As an independent analyst I can present the facts without favor. There is no use in sugar coating the fact that broadcast was -4.6% lower vs 2024 (22.9% vs. 24.0%).

Cable continues to bleed faster - down -15.6% (22.2% vs. 26.3%). Combined linear was down -10.3% YoY.

It will not matter which company ultimately gains control of Warner Bros Discovery (WBD) if viewers continue to change the channel away from the old Hollywood guard and over to the new digital overlords.

-Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.