Laying the Digital Tracks: Decoding Alphabet's Watershed Capital Event

$GOOG, $GOOGL

Accrued Interest TLDR: Alphabet is raising $80 billion in equity—its first issuance in ~20 years and the largest equity offering in history. While Wall Street panics over the $180B–$190B 2026 capex, the structure of this raise is the real story. Google isn’t guessing at demand; internal data (a $462B cloud backlog) proves it is funding contracts already on the books. Ruth Porat designed a defensive capital stack to lock up constrained physical supply, and Berkshire’s $10B check validates this utility-grade infrastructure play. At 26x 2027 earnings, the stock isn’t cheap, but the 1.8% dilution will be organically erased by buybacks in about a year. Alphabet is securing its future from a position of ironclad strength. It remains an Outperform.

Please subscribe for free to read the rest of this Accrued Interest Google deep dive.

0. Revisiting Alphabet Amidst a Watershed Capital Event

Last December, on Day 3 of our “12 Days of Pitch-Mas,” I gave readers a simple recommendation: stop overthinking and buy Google. The point was that creativity doesn’t win in this business. The thesis required no contrarian leap or hidden catalyst; just patience while the market caught up to obvious fundamentals.

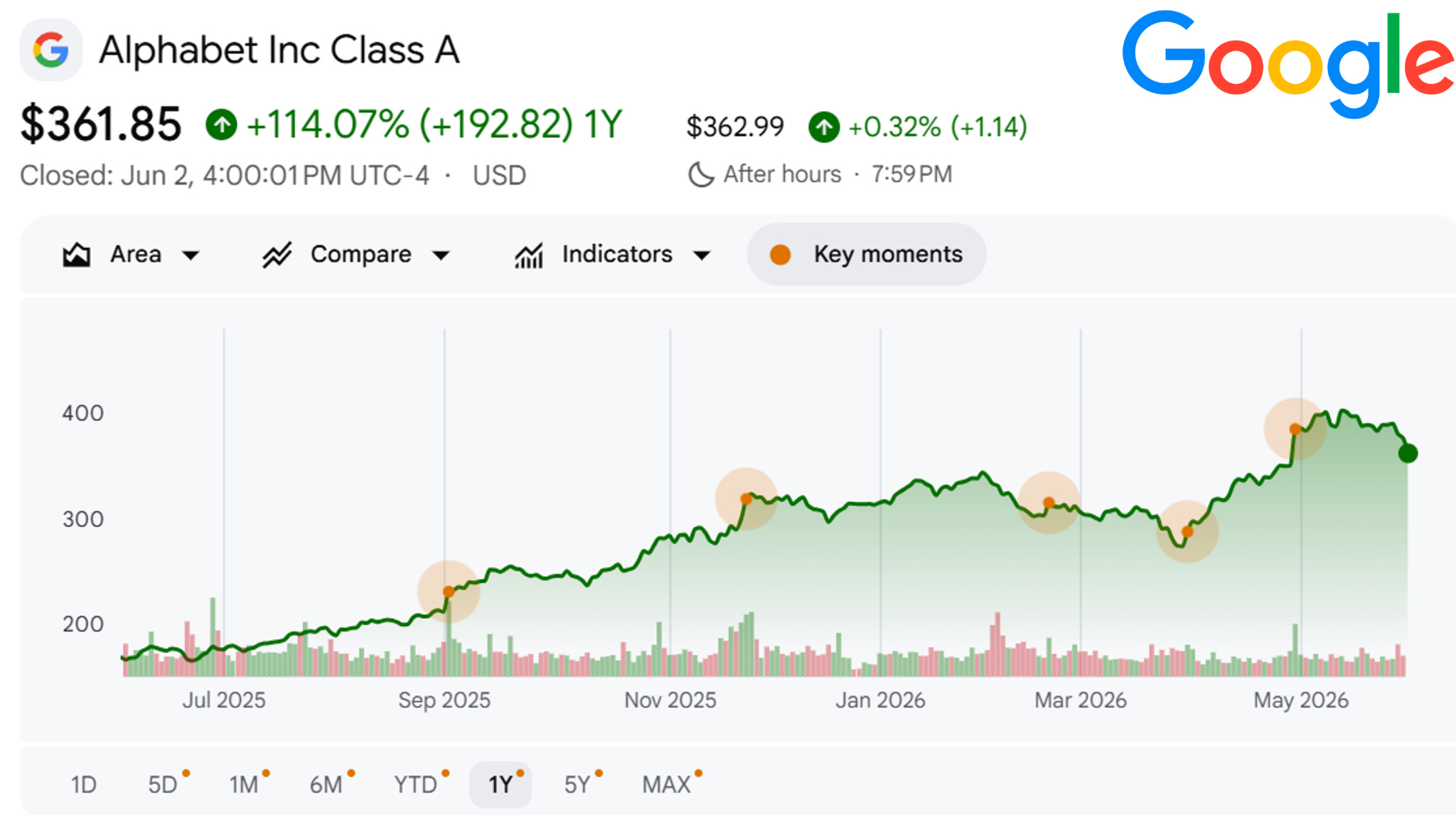

The market caught up quickly. Google closed at $312 on December 11th, and from there it ran all the way to the $400 mark by May 8th — a roughly +28% move in about five months. The stock has since pulled back modestly, but has still solidly outperformed the S&P 500 since my last deep dive.

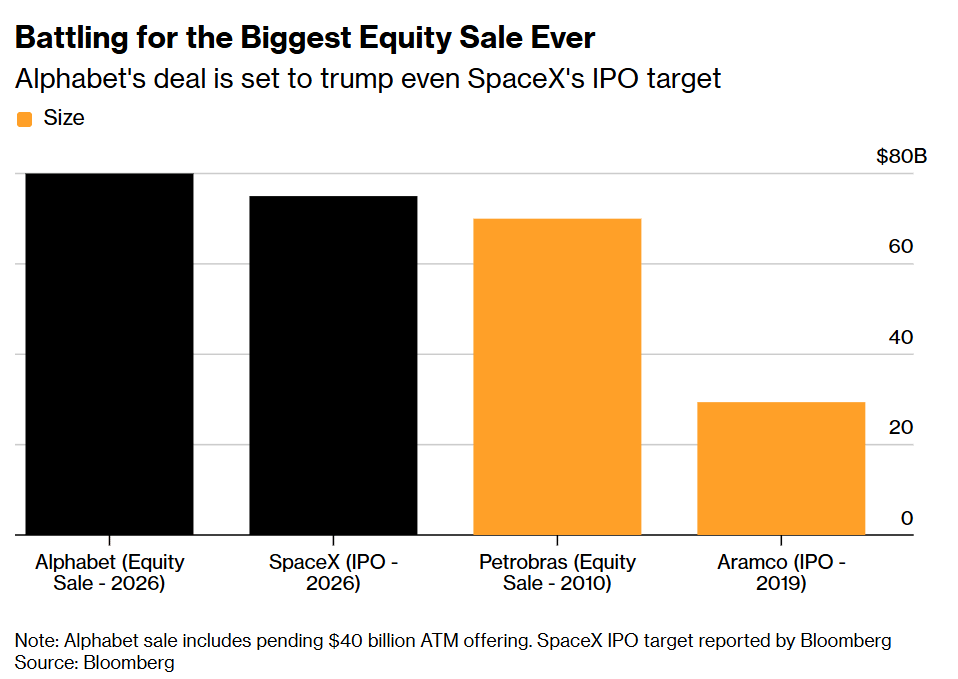

Fast forward to present day, and Alphabet is raising $80 billion in equity — its first equity issuance in roughly twenty years. And the size makes it historic: according to data compiled by Bloomberg, Alphabet’s $80 billion equity sale is set to be the largest equity capital markets transaction ever completed, surpassing the roughly $70 billion common + preferred stock sale that Brazil’s Petrobras executed in 2010. (See table below from Bloomberg)

The headline number everyone wants to talk about is the revised 2026 capex guidance of $180 billion to $190 billion. The reflexive reaction has been to ask whether Google is spending recklessly into an AI bubble. I think that framing misses the real story. The more interesting question is not “why is Google spending so much?” but “what does the structure of this raise tell us about the broader economy?”

1. The Dashboard Advantage Exposes the Information Asymmetry Gap

The standard Wall Street bear case treats hyperscaler capex as a speculative “Field of Dreams“ bet — build it and PRAY that demand shows up. That skepticism is not irrational, but structural. The sell-side is forced to evaluate this spending using lagging indicators. They wait for the quarterly earnings print, and try to reverse-engineer demand from results that are already in the rearview mirror.

Google is not operating on lagging indicators, but on leading ones. Management has something no outside analyst has: real-time KPIs. Their internal dashboards give them visibility into the enterprise cloud pipeline, the length of the compute waitlist, and — critically — the computational requirements of models that have not even been released yet. This is the information asymmetry gap, and it is the entire reason the spend looks aggressive from the outside and obvious to the operators observing these trends from inside Google HQ.

For those who may have forgotten the power of the GOOGLEPLEX, I will help remind you. Google’s Q1 2026 print was one of the strongest quarters the company has ever delivered.

Total revenue of $109.9 billion, up 22% YoY — Fastest quarterly growth rate since 2022, and its 11th consecutive quarter of double-digit growth.

Search and Other revenue grew 19% YoY to roughly $60.4 billion. While bears have spent two years insisting GOOGL would be eaten alive by AI chatbots, growth is actually accelerating. The “10 blue links” bear thesis is over.

Google Cloud revenue surged 63% to about $20 billion, with enterprise AI solutions becoming Cloud’s primary growth driver for the first time.

Operating margin expanded to 36.1%, and EPS came in at $5.11, demonstrating that operating income is growing even as capex ramps.

Now for the demand signals. Google Cloud’s contracted backlog recently nearly doubled sequentially to roughly $462 billion. Search queries are at an all-time high, running at more than 5 trillion annually, and paid subscriptions have crossed 350 million. When you line it all up, the capex stops looking like a leap of faith.

2. A Calculated Capital Stack Designed to Protect Existing Shareholders

If the “why” is information asymmetry, the “how” is financial engineering. To understand the architecture, you have to appreciate the architect. Ruth Porat, Alphabet’s President and Chief Investment Officer and former CFO of Morgan Stanley, certainly was involved in this deal. Her Wall Street pedigree is evident in every tranche of this structure, which is built to raise an enormous sum while inflicting the least possible damage on existing shareholders.

Bear with me for a minute — this section will get a bit more technical. The capital raise can be described in four components:

1)The $40 billion at-the-market (ATM) program. The single largest component, expected to begin in Q3-26, lets GOOGL drip-feed shares into the market rather than dumping a single block and crushing the price. This is the flexible, low-impact backbone of the deal.

2)The $15 billion sale of common stock. A more conventional block, sold concurrently to seed the raise and anchor institutional demand.

3)The $15 billion mandatory convertible preferreds. This is the most surgical piece. The preferreds secure cash today but, because they convert in roughly three years, delay the actual equity dilution until 2029. That is a duration match, and a deliberate one: the new common shares hit the market at almost exactly the moment the newly built data centers are throwing off free cash flow. Management is timing the dilution to coincide with the earnings it is meant to fund — you take the hit to your share count right when the assets you bought start paying for themselves. As a bonus, mandatory convertibles are typically a cheaper source of capital than debt and are frequently treated by the ratings agencies more like equity than debt.

4)The $10 billion Berkshire Hathaway private placement. (I will come back to this.)

Sitting on top of the convertible tranche, Google also purchased capped call options — essentially derivative insurance policies — to synthetically raise the effective conversion premium. In plain English, they bought protection on the upside so that common shareholders keep more of the gains if the stock appreciates before 2029. This signals how defensive the whole thing was structured.

Now - here are two more strategic considerations, unrelated to the deal structure.

A)I think Google is partially front-running several mega IPOs. Anthropic, SpaceX, and OpenAI are all aiming to go public later this year. The timing here was not subtle: Alphabet announced its raise just days before SpaceX is expected to begin marketing what could be the largest IPO of all time, effectively stealing its thunder and getting to the front of the line. The early read is that it worked, with the common and convertible tranches reportedly oversubscribed.

B)Google is preserving its debt arsenal. They could have funded this with another jumbo bond, but doing so would have used up their debt capacity in one shot. By raising equity instead Google keeps its powder dry.

3. Weaponizing the Balance Sheet to Secure Constrained Supply

Raising the cash is only half the play. The other half is what they do with it.

First, the primary bottleneck in the AI race is not capital but physical supply. From transformers to specialized labor, the supply chain is severely strained. By weaponizing its massive cash reserves to secure priority access, Alphabet is effectively jumping to the front of the line.

Next, there is a second-order effect here that benefits the suppliers too. By handing out guaranteed, multi-year, non-cancellable contracts, Google is effectively removing the boom-and-bust cyclicality that has historically plagued industrial component manufacturers. A transformer maker that knows it has years of locked-in Google orders can invest in expanding its own capacity with confidence. That stability is valuable — and it is exactly why suppliers will prioritize Google over a smaller buyer waving a one-off purchase order.

The third, most competitive effect: securing physical supply early effectively starves the competition. Every transformer and cooling unit Google locks up is a unit smaller competitors cannot buy.

4. Treating AI Datacenters as the New American Infrastructure

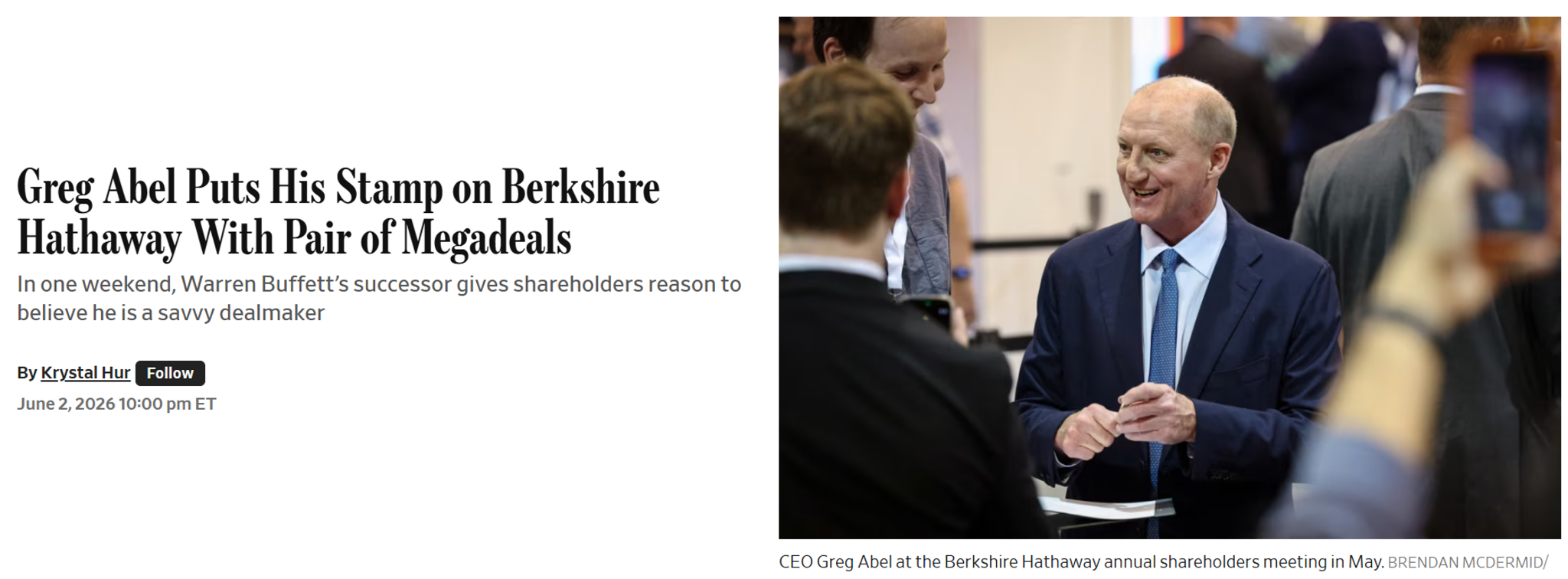

If you want validation that this is an infrastructure play rather than a software gamble, look at who showed up to write a check. Greg Abel and Berkshire Hathaway committed $10 billion via a private placement, securing roughly a 6.5% discount to Monday’s close (buying both Class A and Class C shares at that discount to their respective closing prices before the deal was announced). Berkshire does not chase momentum and does not make speculative bets on technology fads. So why is it here?

I would argue that Berkshire is not looking at this through a “value software” lens at all. Under CEO Greg Abel — who built his career running utilities, pipelines, and energy assets — Berkshire evaluates an investment by asking whether it is a durable piece of essential infrastructure. Through that lens, an AI data center is not a speculative tech asset. It is the 21st-century equivalent of a railroad or a power grid: a digital toll bridge that the entire economy will eventually have to pay to cross.

This is the same firm that under Buffett invested heavily in BNSF Railway and in regulated energy grids — the literal tracks and wires of the old economy. Berkshire views AI data centers as the next pillar in that lineage, and there is a tangible sign that Google sees it the same way. According to Amin Vahdat, Google’s Chief Technologist for AI infrastructure, Alphabet is transitioning toward modular, repeatable data center blueprints — standardized designs that can be stamped out and deployed at scale rather than custom-built one at a time.

5. Securing the Future From a Position of Valuation Strength

Let me be clear-eyed about the price, because I am not going to pretend the stock is a bargain here. Anchoring on Monday’s close of $376.26, Alphabet is trading at roughly 26x the 2027 GAAP EPS consensus estimate of $14.34, and 22x the 2028 estimate of ~$17.00. The multiple is full and the stock is not cheap.

The overlooked math is simple: an $80 billion raise against a $4.55 trillion market cap is a manageable dilution of about 1.8%. Alphabet could erase that in about a year through its $60B+ annual buybacks. However, I do expect the pace of buybacks to slow during this period of hyper-investment.

The timing of this raise is what separates good management from merely competent management. Rather than rushing to issue equity into the negative sentiment of early 2025 — when tariff fears and “Google is dead” AI panic had the stock under pressure — GOOGL management let that sentiment wash away. They are now selling equity near 52-week highs, taking full advantage of the multiple expansion the market handed them over the past year.

This is George Soros’s theory of financial reflexivity in action. By accepting a small amount of dilution today, Alphabet is securing the physical equipment — the chips, the transformers, the cooling, the land — required to drive its future earnings growth. The dilution funds the assets; the assets generate the earnings; the earnings more than offset the equity dilution.

CONCLUSION

So here is where I land. AI is still in its early innings, and it is severely capacity-constrained. A trillion-dollar buildout is not optional if AI is going to become as ubiquitous as the bulls (myself included) expect. Google stock is taking a natural breather right now as the market digests the dilution, and that is fine. Selling equity from a position of strength, into a full multiple, with the most disciplined investor in the world co-signing the thesis, sets the company up for much larger gains down the road. I firmly believe that Alphabet stock remains an Outperform.

— Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.

lots of confirmation bias here but this was great. i loved how you weaved in the personalities involved (e.g., porat) and how that might have played into timing, deal structure.