Fubo TV Q3-2025 Earnings Recap

5 Reasons the Hulu + Live Merger Can't Save $FUBO

For Q3 earnings season I wanted to do a formal update on FuboTV, FUBO 0.00%↑ since it has been several quarters since I published on the stock. I will not bury the lede, Fubo is still uninvestable as a stand-alone company. Their Q3 financials made it clear they need the merger with Hulu + Live to survive. The stock initially fell almost -10% on Monday following the earnings release, but the stock has since regained some of these losses, bouncing back +6% on Tuesday. Fubo’s fervent fanbase of too-online posters have yet again ignored the weak financials and put all their hope in Disney saying the day. So, I take no pleasure in pointing out that Fubo’s business is still not growing. Let me explain why Q3 was weak and I am doubtful that the merger with Hulu + Live will make much difference in 2026.

Links to past FuboTV videos / posts:

The Future of FuboTV Part 1: Assessing the Disney-Hulu Merger Impact

Fubo TV’s Struggles: Q1 2025 Earnings Breakdown - Accrued Interest Podcast

1)Fubo still cannot consistently grow revenue to cover its fixed costs

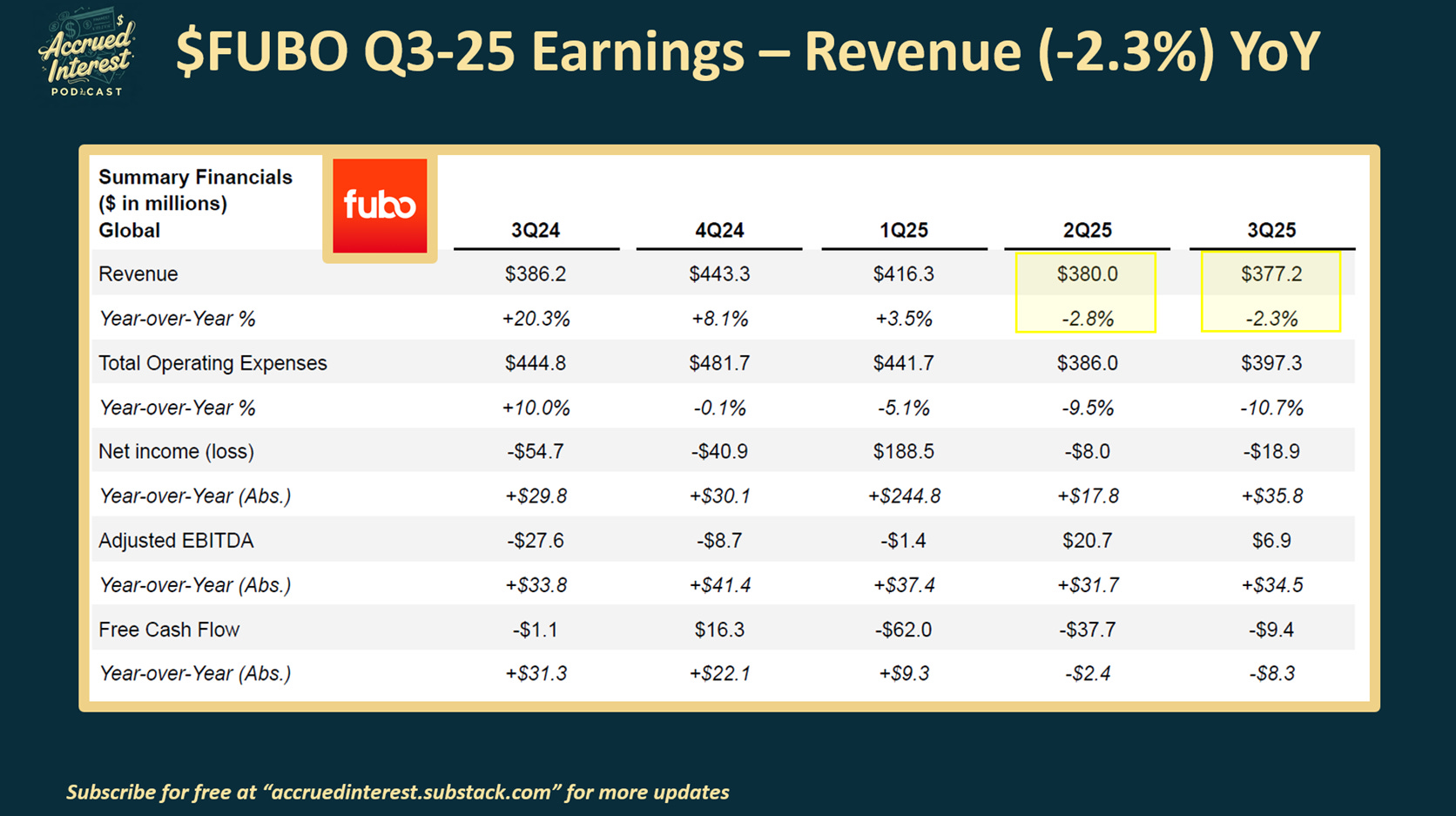

The FIRST THING that jumped out at me from the FUBO 0.00%↑ Q3-25 was that this is now the 2nd consecutive quarter of negative YOY revenue growth.

Revenue for Q3-25 is down -2.3% and Q2 down -2.8% YoY.

Being a digital MVPD is a high fixed-cost business so you NEED revenue growth to survive long-term. And it gets worse....

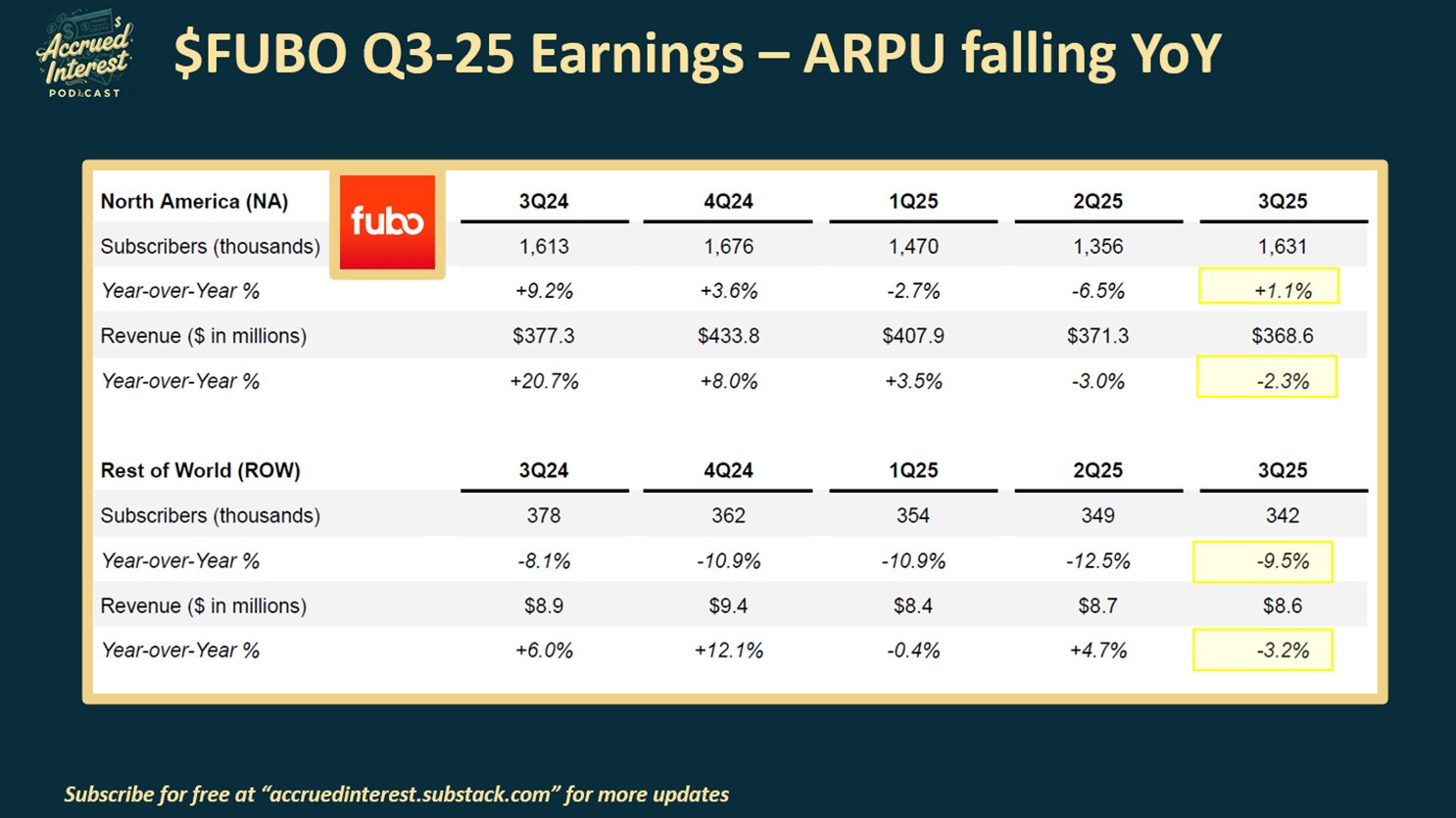

2) ARPU is falling without enough subscriber growth to make up the difference

More worrying - ARPU, average revenue per user, is also falling for Fubo.

North American subs were +1% but total revenue fell -2%, which implies they earned LESS revenue per subscriber.

This is really bad for FUBO 0.00%↑ because with the payTV ecosystem shrinking, bulls would need at least customer pricing to hold up better since subscriber growth is almost nonexistent.

Counterpoint - bulls would in theory argue that falling ARPU could be good for FuboTV because cheaper bundles would help with subscriber growth (in THEORY).

The problem is that subscriber growth needs to be greater than ARPU decreases in order to be accretive and this is not the case. I am not sure how Hulu + Live will reverse this trend since that service has also failed to grow its subscriber base!

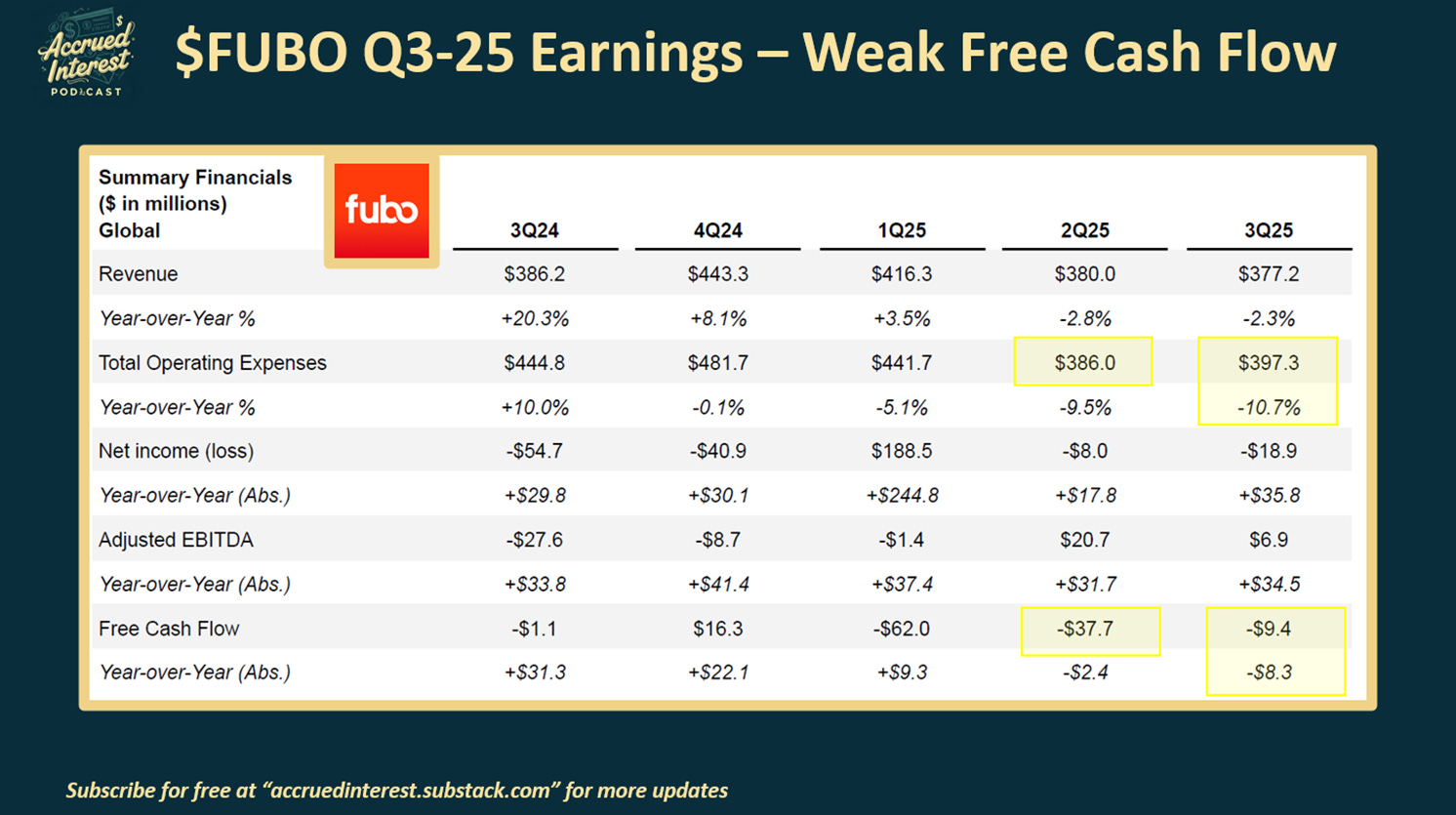

3) Free cash flow is still negative, showing no operating leverage

I’m worried that Fubo expenses were up quarter-over-quarter, while revenue fell from Q2. The free cash flow and profits here are still weaker than one would hope.

And we know from DIS 0.00%↑ earnings that Hulu + Live trends are not positive enough to reverse this, since many of the savings are going to be in just Sales & Marketing which is not a big cost center.

On the conference call - Fubo management bragged about cutting marketing expenses and still managing to grow subs. Based on my past decade of experience in FP&A roles within major media companies - I have NEVER seen marketing cuts done in a healthy business.

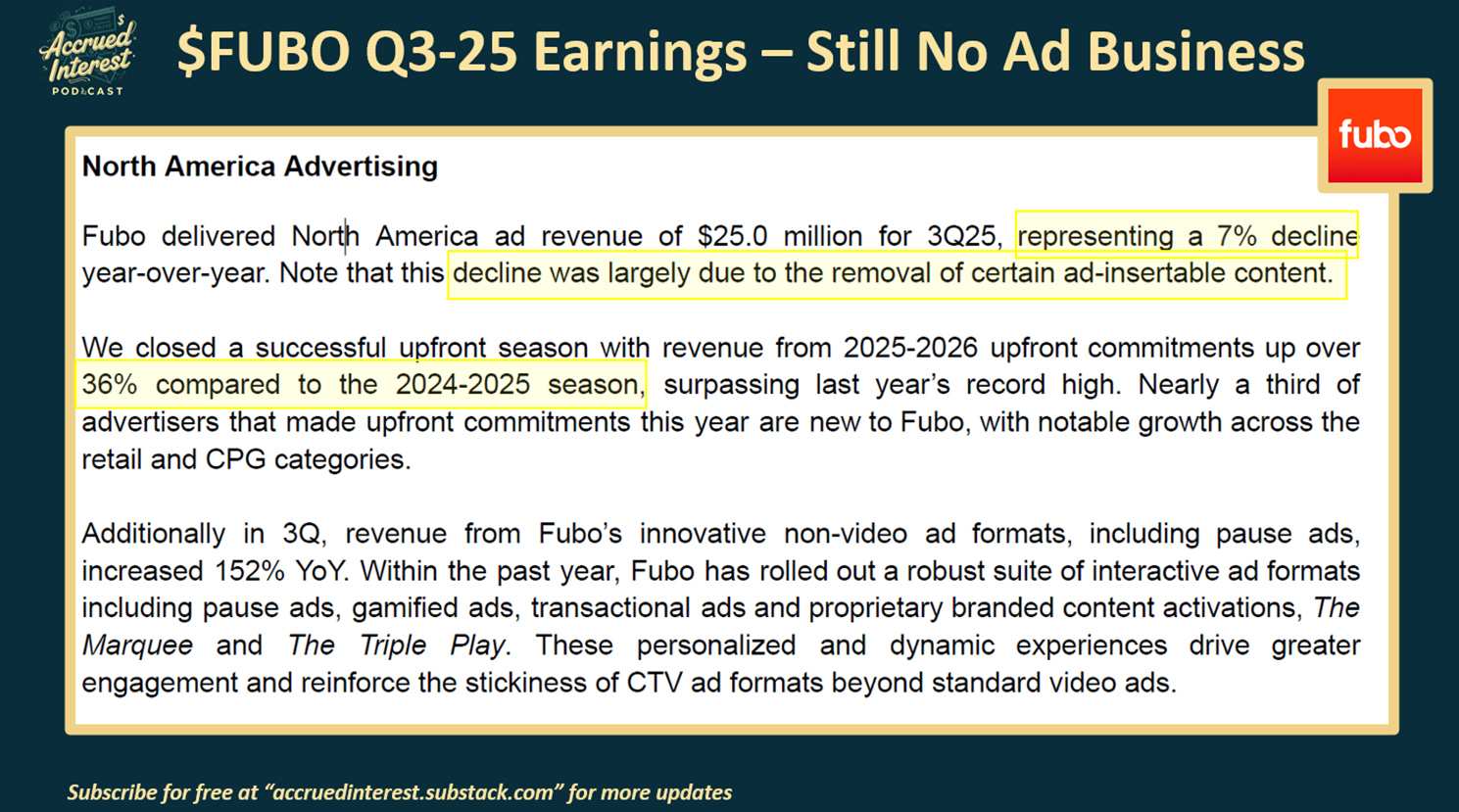

4) With no advertising business at Fubo, more pressure on Hulu + Live

Management said that North American advertising revenue was -7% YoY, due to “the removal of certain ad-insertable content”.

I would argue the reason does not matter - declines here are unacceptable.

Q3 PR brags about 2025-2026 Upfront dollars up +36% from 2024-2025. I am not impressed, +36% means little growing off a tiny base.

There is no advertiser interest in a DIGITAL service with a paltry base of less than 2 million subs (pre-Hulu merger).

In theory, you would want to see ad revenue growth at higher rates, at least double-digits, coming off such a small base.

Now to be fair, Disney is going to be taking over much of the Ad Sales function now that the merger with Hulu + Live has closed. I am just skeptical it will be enough to turn things around here.

5) Fubo’s financials no longer matter - Hulu+ Live is now in charge

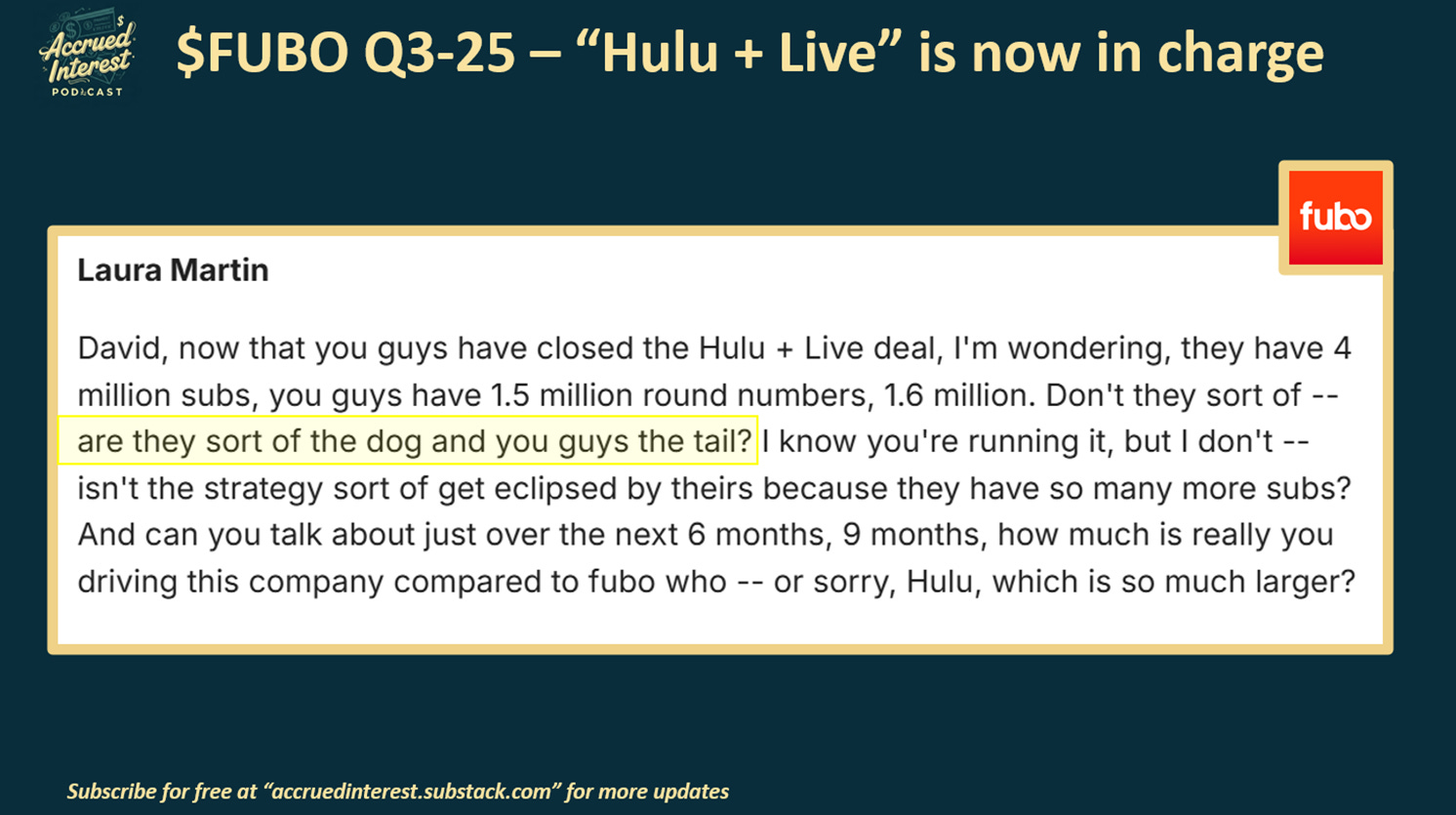

I thought this exchange from the Q&A portion of the conference call was worth highlighting because it illustrates my point that Hulu + Live is all that matters from here on out with Fubo.

Laura Martin, the senior entertainment and internet analyst at Needham & Company, asked what I found to be a hilariously direct question of Fubo management.

“David, now that you guys have closed the Hulu + Live deal, I’m wondering, they have 4 million subs, you guys have 1.5 million round numbers, 1.6 million. Don’t they sort of -- are they sort of the dog and you guys the tail?”

With Hulu + Live subscriber base of almost 4M vs. Fubo’s 1.6M, the former is going to drive the future of the combined NewCo far more than the latter. To be fair, the deal formally closed recently, so we will have to wait until management provides updated pro forma financials.

In my experience, successful investing requires you to operate without complete information. I will continue covering Fubo stock, however I am not optimistic that the combination with Hulu + Live will be enough to make me confident the stock can outperform the market in 2026. In hindsight, it makes perfect sense that management was selling stock between $5 and $6 dollars following the merger announcement.

-Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.