Decoding the Nexstar M&A Deck ($NXST)

Reading Between the Lines of the Aug 2025 Tegna Deal

Nexstar ($NXST) dropped a new investor presentation when they held an update call on Aug 19th with official announcement that they were acquiring Tegna ($TGNA). Similar to what I did last time NXST put out an investor deck, I wanted to give you my annotated notes. Keep in mind, that there are many different audiences for an M&A announcement – not just the public shareholders. Let me help you read between the lines, as someone who used to make these decks from scratch.

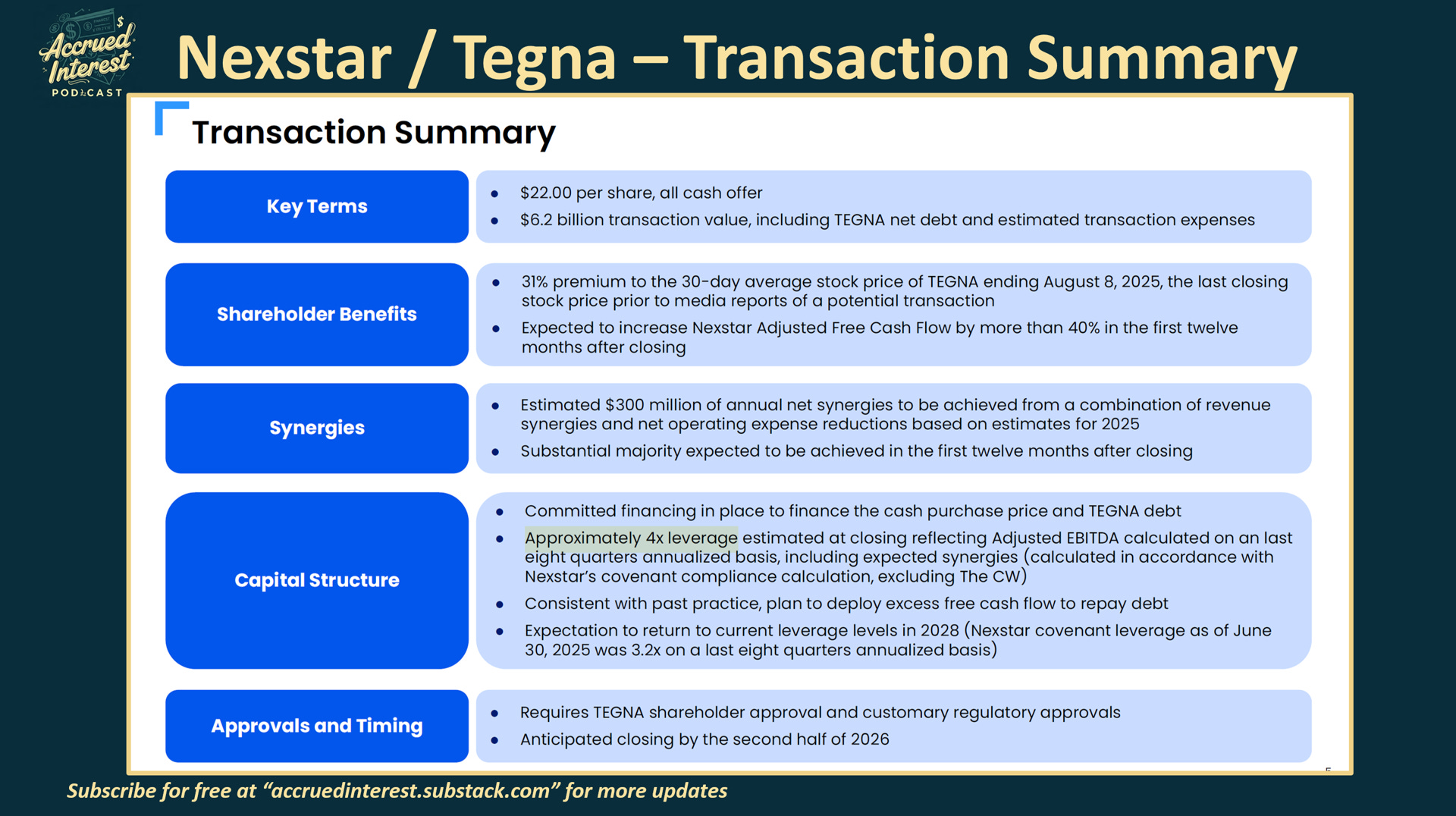

SLIDE 5 – Transaction Summary

Accrued Interest Take:

My first reaction was to ask myself - why is NXST doing an all-cash deal for Tegna? If the deal is so accretive, why can't Tegna shareholders take some equity and help have a stronger company with less debt post-close?

It is possible that based on the market interest for Tegna, their side was able to push for an all-cash deal and lock-in the economics for their shareholders.

This morning it was reported that Sinclair had also proposed a deal to buy Tegna. (WSJ: TV-Station Owner Sinclair Proposes Merger With Tegna)

The Nexstar deck undersells just how much leverage is going up at Nexstar in the short-term with an all-cash deal.

Slide says 4x leverage, gives no nominal figure. And that 4x leverage includes annualized synergies…

They do not expect to get back to 3x leverage until 2028…that’s a long time!

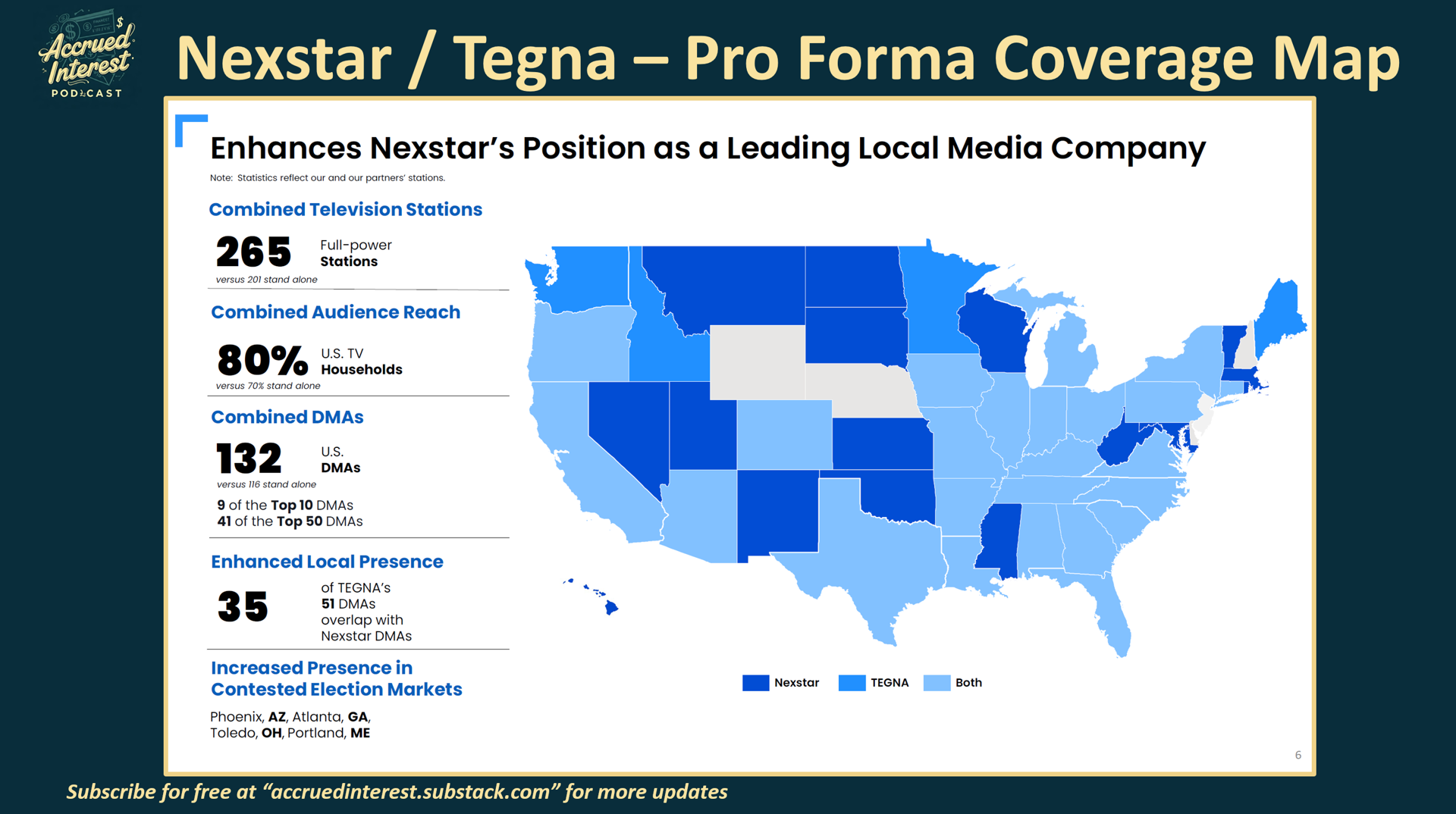

SLIDE 6 – Enhances Nexstar’s Position as a Leading Local Media Company

Accrued Interest Take:

As expected, there is an unwritten rule that requires every broadcast TV M&A deck to have a coverage map of the United States.

While it is a “nice to have” that NXST can reach more markets thanks to TGNA stations...how much do advertisers really care?

Broadcast investors need to ask themselves in 2025 what is the value of more geographic reach for broadcast TV when advertisers can already go national with Google or Meta.

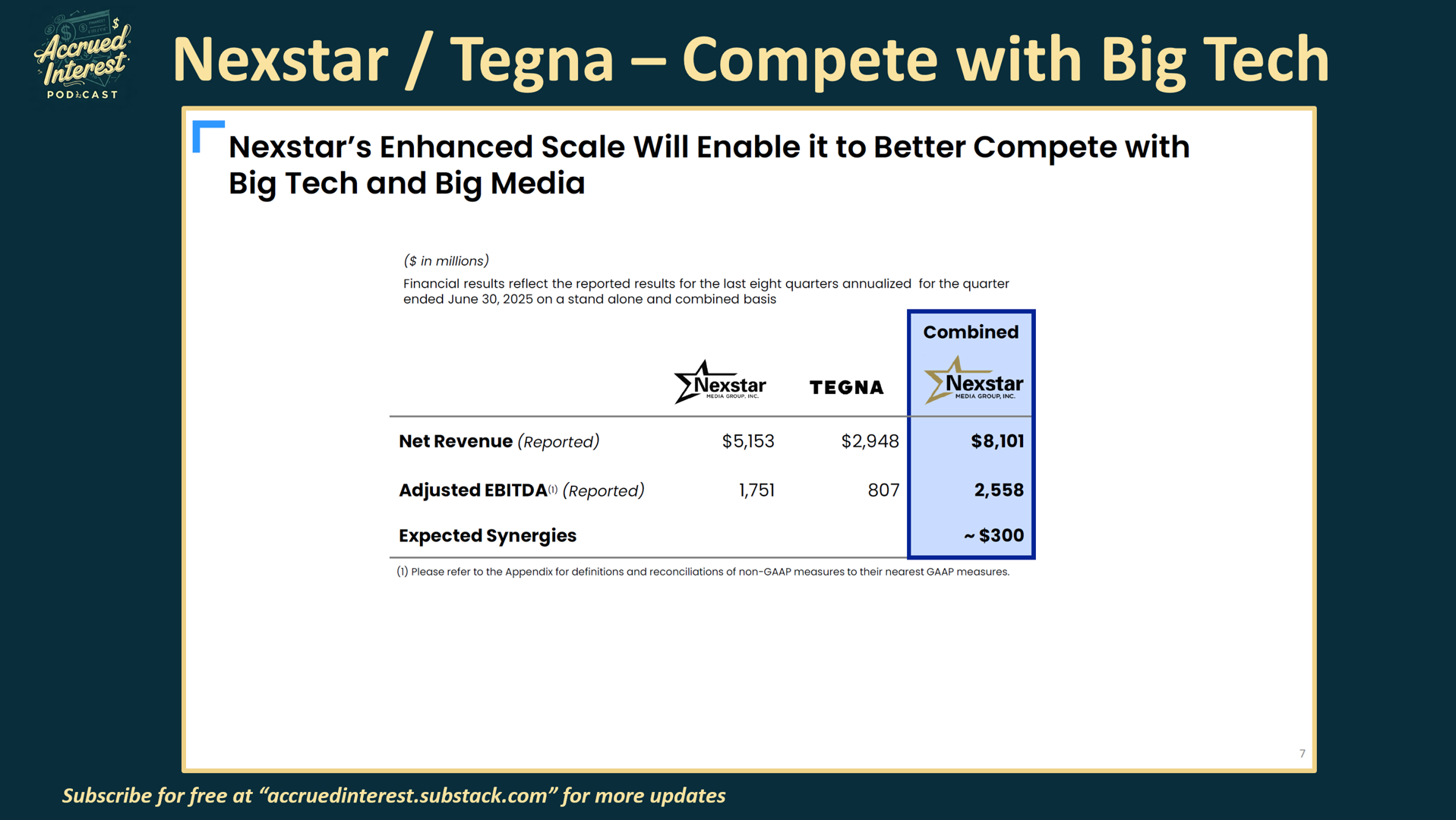

SLIDE 7 – Nexstar’s Enhanced Scale Will Enable it to Better Compete with Big Tech and Big Media

Accrued Interest Take:

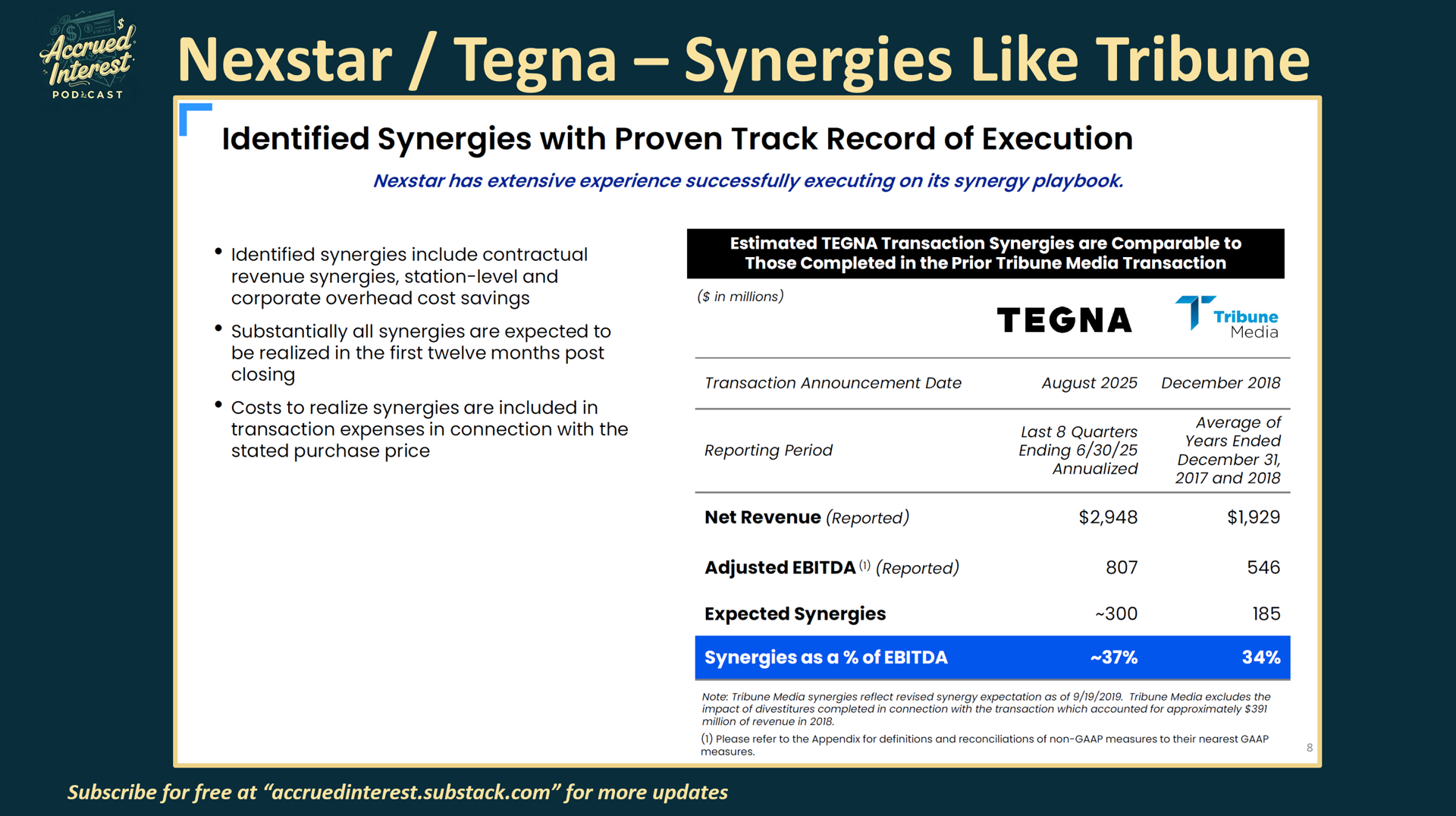

Here Nexstar finally shows us expected synergies with Tegna and the total is $300M or about 37% of Tegna's current EBITDA.

That scale is indeed sizable and accretive to current earnings. However, does anyone really believe an extra $300 million will help Nexstar compete against big tech such as Meta, Google and others?

A lot of the statements around competition seem to be aimed at winning the attention and approval of both the regulators and the White House.

SLIDE 8 – Identified Synergies with Proven Track Record of Execution

Accrued Interest Take:

Nexstar here is saying "trust us" with M&A on Tegna - by showing how it is similar on paper to their past acquisition of Tribune Media.

As I have mentioned on this Substack before - I won the Ira Sohn Investment Idea Contest with a blind submission where I pitched Tribune Broadcasting.

In my coverage of Tribune, I pointed out that the real winners were the shareholders who took the buyout. The combined Nexstar / Tribune merged entity has underperformed the S&P 500 since the deal closed in 2019.

All the projections about the cost synergies are factually correct. My issue is that these large broadcast M&A deals never create the revenue synergies to drive organic growth. Financial engineering is not a long-term sustainable strategy.

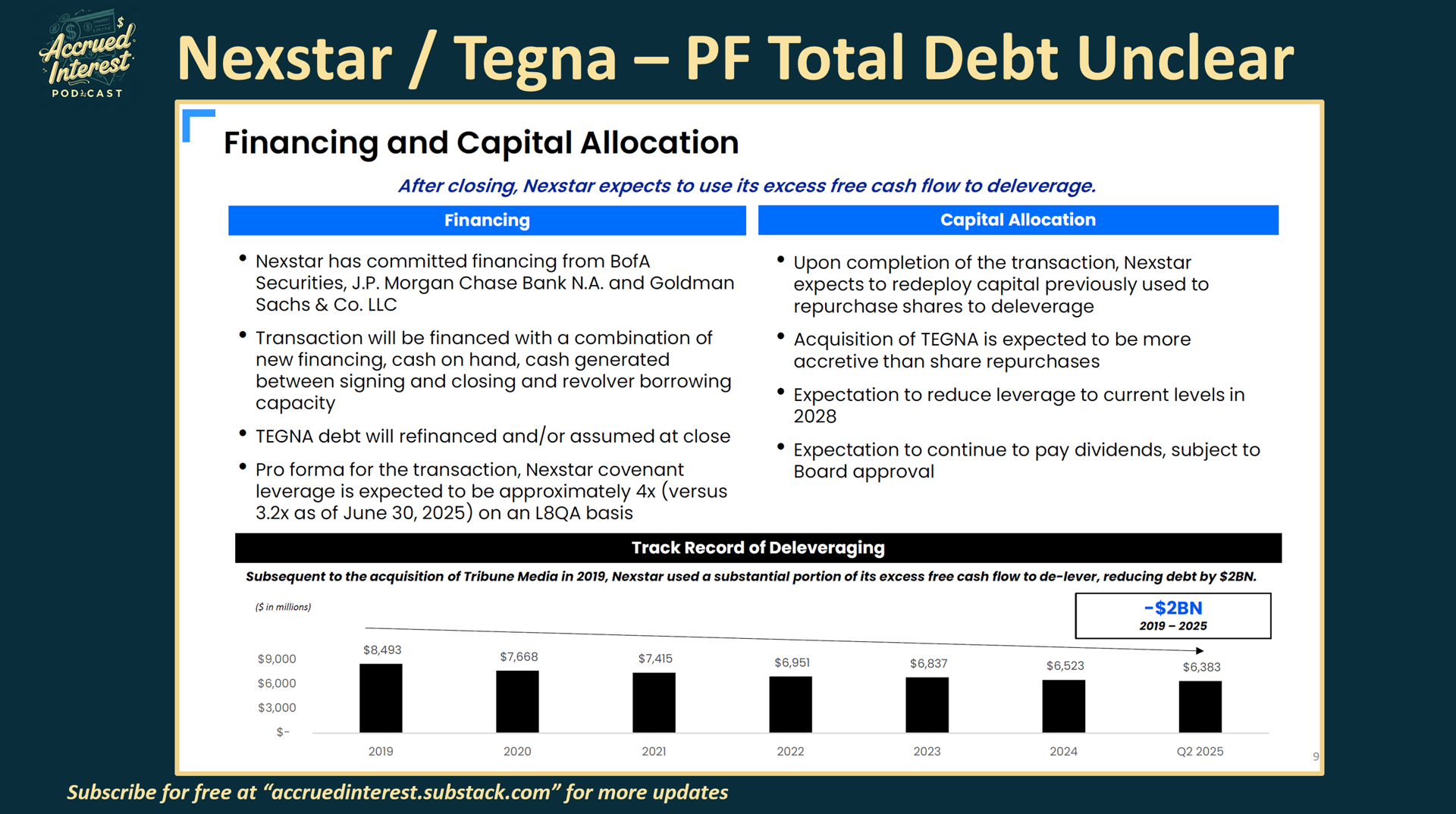

SLIDE 9 – Financing and Capital Allocation

Accrued Interest Take:

I found it both amusing and frustrating that Nexstar makes it a logic-puzzle to figure out what the total expected debt is, post-closing.

Tell me if I missed something, but the deck never states the combined debt!

The details they give are very confusing! They say combined debt will be 4x, but that figure includes synergies annualized for the 8 quarters.

Also, management is asking equity holders for a lot of patience. Waiting until 2028 to return to 3x leverage is a long time when broadcast TV viewing is in decline today with no signs of slowing down.

Management does not want to scare the market by showing everyone just how highly levered this all-cash deal will be. To stay long requires full faith that the EBITDA does not materially decline over the next 3 years.

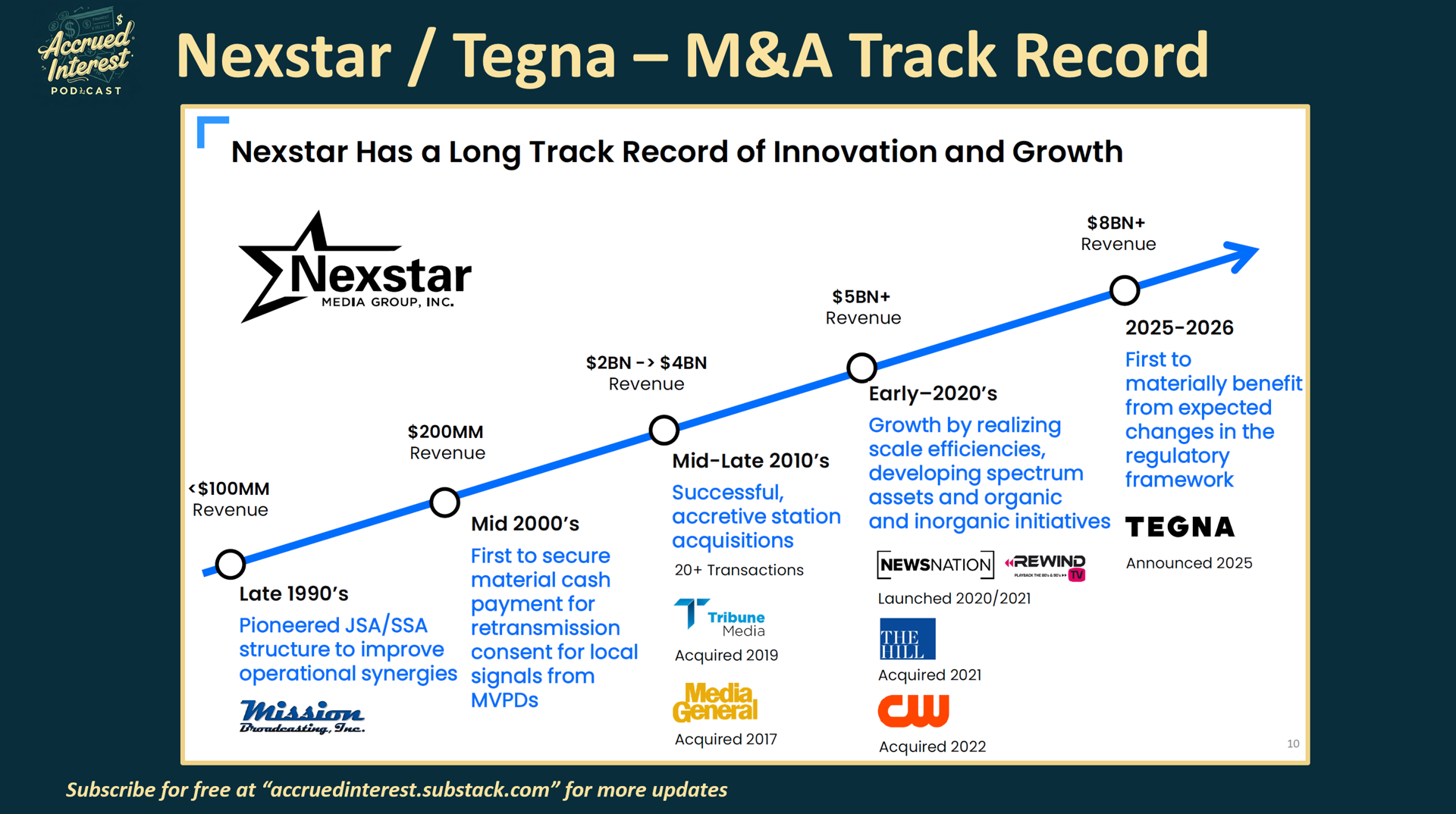

SLIDE 10 – Nexstar Has a Long Track Record of Innovation and Growth

Accrued Interest Take:

Media M&A slides love to show revenue because they do not want you asking how much value was created for equity holders by past $NXST deals.

$TGNA is the biggest deal that Nexstar can do right now...it needs to work and spark more revenue growth. However, I wonder, what is next? There are not nearly as many large broadcast TV targets once Nexstar devours Tegna. Long investors need to ask themselves how much more M&A can do for the story?

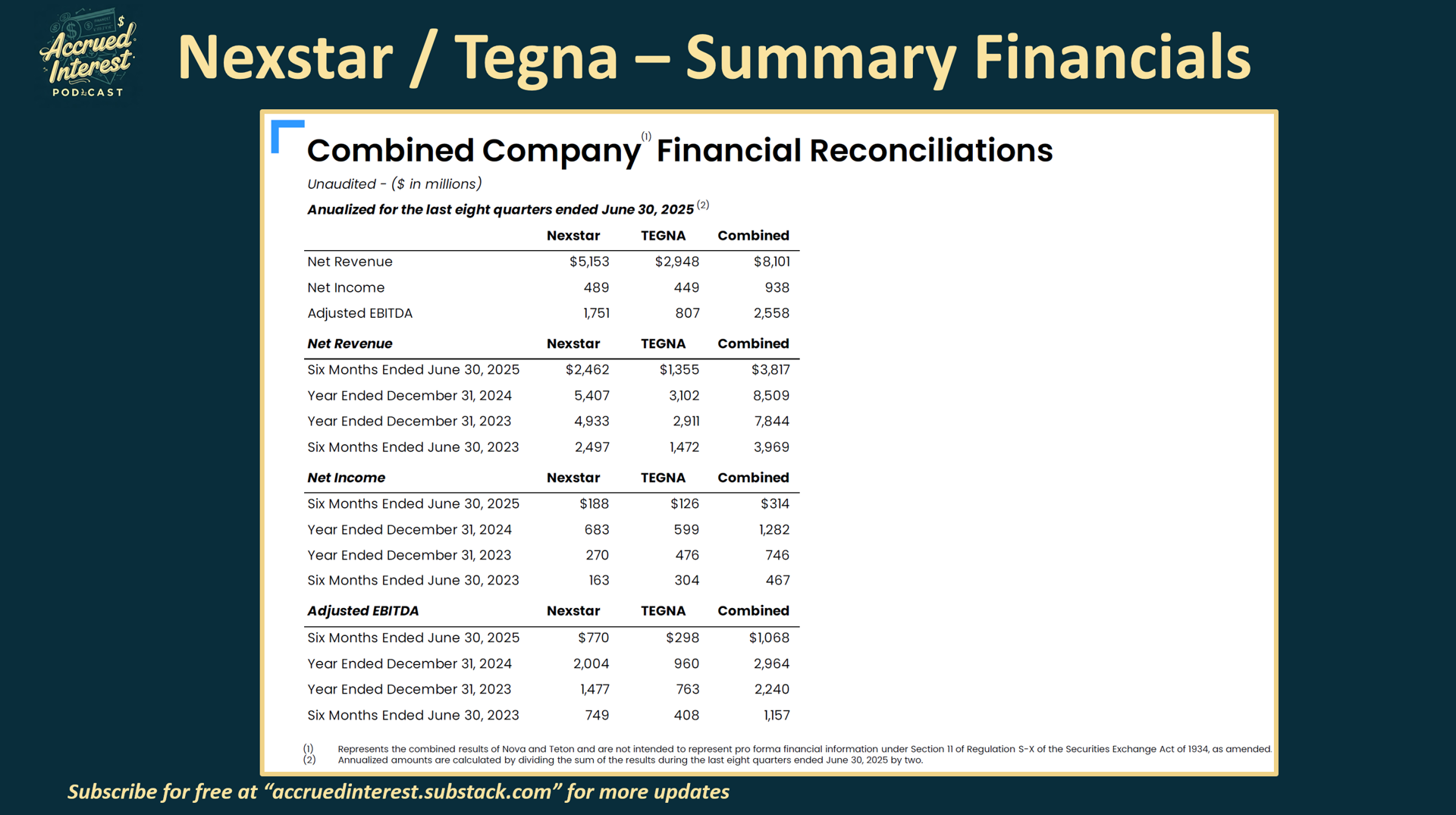

SLIDE 13 – Combined Company Financial Reconciliations

Accrued Interest Take:

Given the size of Tegna relative to NXST, I would prefer TGNA to take equity to help lower post-deal leverage.

Synergies are large, but broadcast share is still falling. High leverage just accelerates the stock performance in either direction. I think it would be healthier for Nexstar to keep leverage as low as possible. But with this deal they have no choice.

CONCLUSION

This deal will buy Nexstar a few more years of runway because they will be able to get a lot of cost synergies out of firing employees.

However, I would rather be a seller rather than the buyer of broadcast television stations, because neither M&A nor the regulatory environment can create the much-needed organic growth that has been elusive.

Even if regulators can change the profit-sharing agreements between the Big Four networks (ABC, CBS, NBC and FOX) and their local market affiliates (NXST, SBGI, etc.), it does not change the fact that audiences are leaving the pay TV ecosystem.

I do not have a strong opinion of whether Sinclair or another entity will launch a bidding war for Tegna. I know for sure that Nexstar needs to pay up for this asset because it is the largest competitor in the public markets.

If you must go long broadcast stations, I would rather sell out to Nexstar rather than buying up highly levered assets in a declining industry. Or just buy Fox Corporation, ($FOXA) .

If you are a Tegna shareholder I recommend you take the deal! TGNA shareholders do not have to decide whether to accept stock in NXST. Getting 100% cash is truly a gift too good to pass up.

-Accrued Interest

Recent Accrued Interest articles on Nexstar ($NXST):

Media Stock Insights from Nielsen’s June-25 TV Snapshot, July 17

Interview – Nexstar Media Group: Broadcasting's Biggest Bet ($NXST), June 25

Byron Allen's AMG Selling TV Stations: An Ominous Sign for Broadcast, June 6

How My Stock Pitch Won the Ira Sohn Investment Idea Contest, May 15

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.

Great breakdown! It will be interesting to see how NXST and their management try to utilize their M&A going forward. As you say, with these combination there will not be as many, if any, enticing deals to make going forward so I will be curious how the market looks at this huge fish in a shrinking pond going into the future.