Decoding the Nexstar Investor Deck (NXST)

Reading Between the Lines of the June 2025 Investor Presentation

Nexstar just dropped a new investor presentation on their website for June 2025. They said in the press release that the intention was to provide additional detail “for investors that are new to the Nexstar story”. I think that is code for – “we are going to need to issue a lot of new shares for all the M&A we are about to do, so let’s start marketing again”.

Earlier this week, I did a deep dive decoding the investor deck for Starz, and it quickly became one of my most read articles. I’m going to do the same with Nexstar and give you my annotated notes so you can read between the lines. Now, let’s dive in!

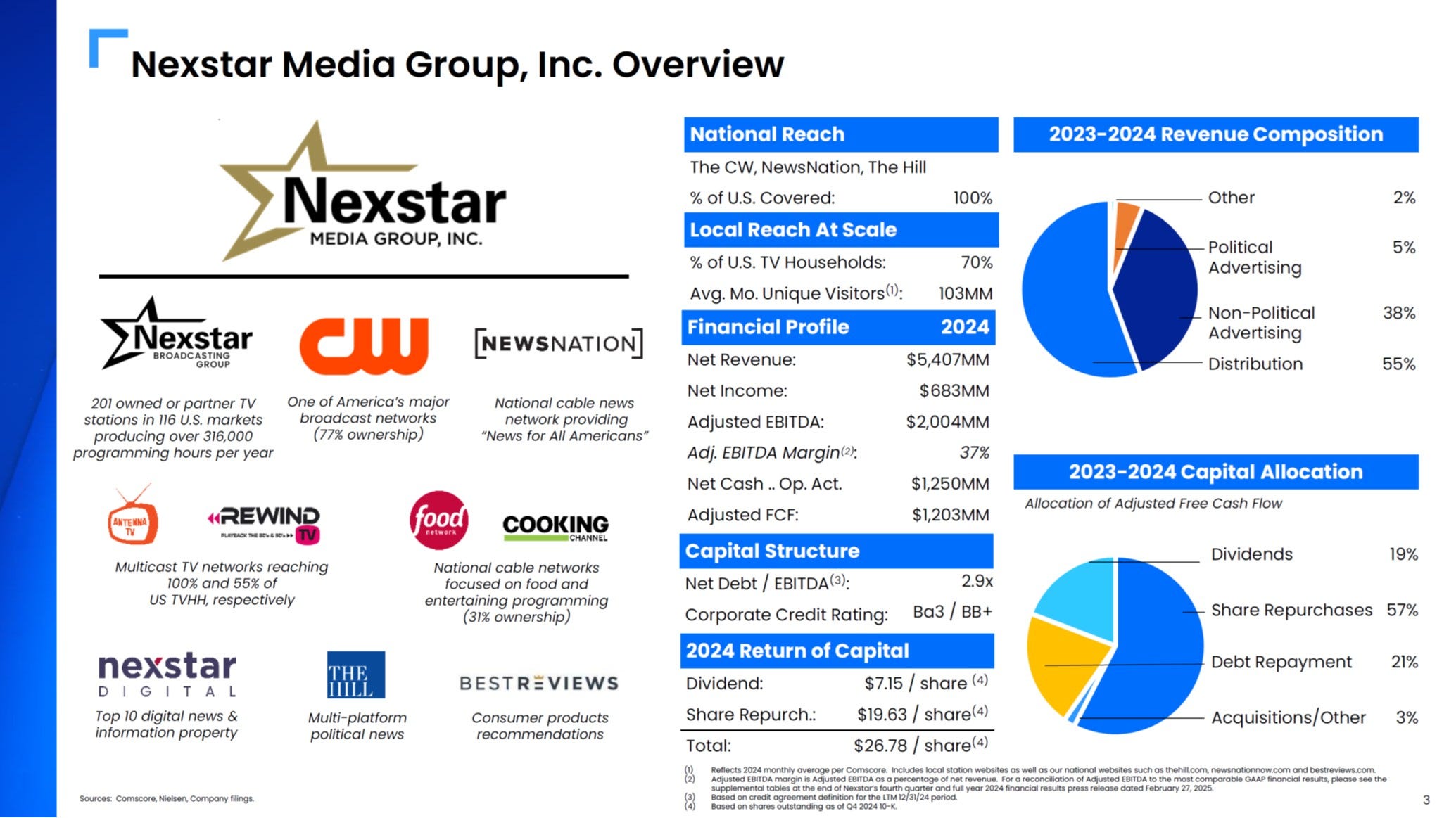

SLIDE 3 – Nexstar Media Group Overview

As I said in my latest on Warner Bros. Discovery ($WBD), “any good media investor relations deck must have at least one page with high-resolution brand LOGOS”.

This recap slide gives an excellent birds-eye view of NXST’s current portfolio. I’d suggest printing out the deck and keeping Pg. 3 next to you like a cheat sheet as you read the rest of the deck.

Remember, investing is not just about finding quality assets. It’s about forecasting the trajectory of the business starting from TODAY. The past isn’t always prologue.

The only comment I have here, is that despite the many logos on the page, the only assets that moves the needle in terms of earnings are the local TV stations. All the “digital” properties are nice to talk about, but ultimately tangential to the story.

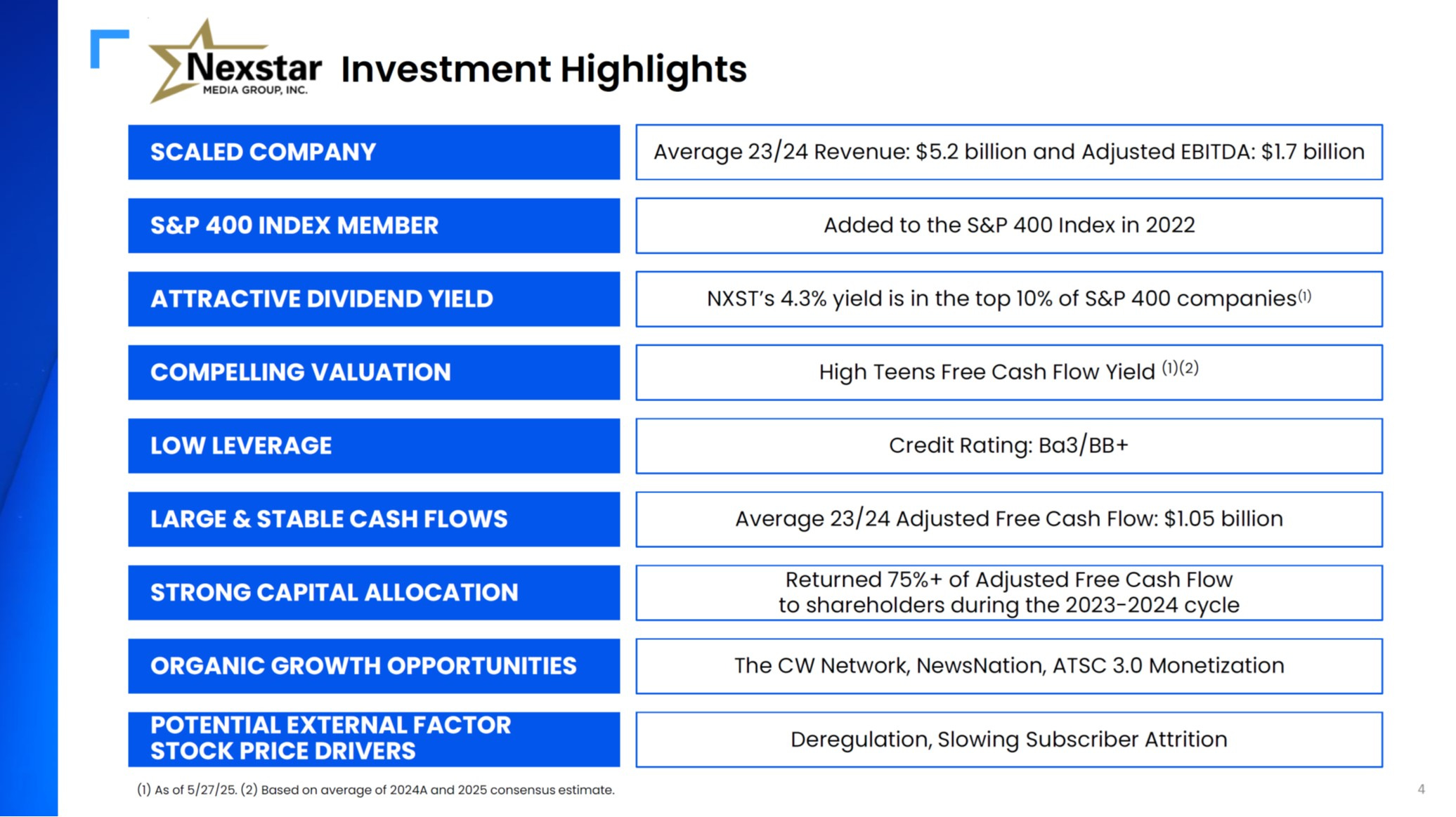

SLIDE 4 – Investment Highlights

It doesn’t matter that NXST was added to the S&P400 in 2022. A company’s earnings power is not determined by who holds the stock. If anything, one might want to ask why the largest publicly traded local TV company is NOT in the S&P500 if the industry is so attractive. Perhaps this industry has a ceiling.

As I said in my Starz piece, I have become skeptical as an investor when a management team is complaining about their “compelling valuation”. NXST management needs to convince investors there is still organic growth, and then Mr. Market will tell us if the valuation is attractive, or not.

I’m disappointed that the “organic growth opportunity” doesn’t mention subscriber GROWTH. Instead, NXST is pushing their side projects like the CW and NewsNation as growth drivers, but we all know they are too small.

Lastly, it is funny they list “slowing subscriber attrition” as an “external factor stock price driver”. I think slowing subscriber attrition should be NXST’s biggest INTERNAL focus. The continued exodus of subscribers out of the pay-TV ecosystem is not just “stock price noise”, but an existential threat they cannot ignore.

“Deregulation” is not a savior, but we will get to that later….

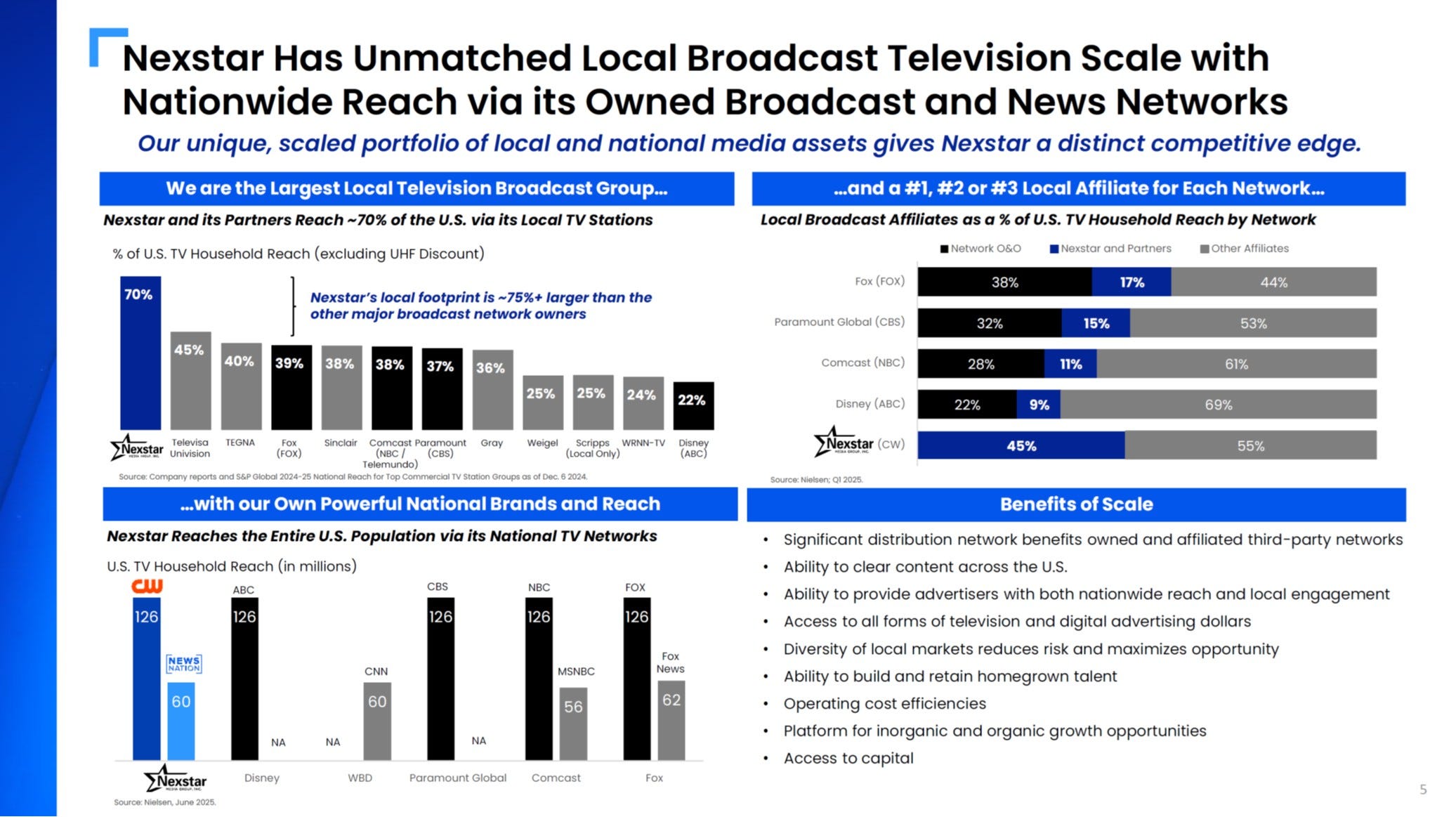

SLIDE 5 – Unmatched Scale with Nationwide Reach

The purpose of this slide is to demonstrate just how BIG Nexstar is already and make the case that “scale” is a competitive advantage. All the broadcasters are trying to tell investors that deregulation will let them acquire more stations and change the narrative.

I am not convinced. NXST's boasting about their size makes me question how much additional M&A will matter.

If by Nexstar’s own admission they already reach70% of U.S. TV households, then regulation has not been what’s holding back the business.

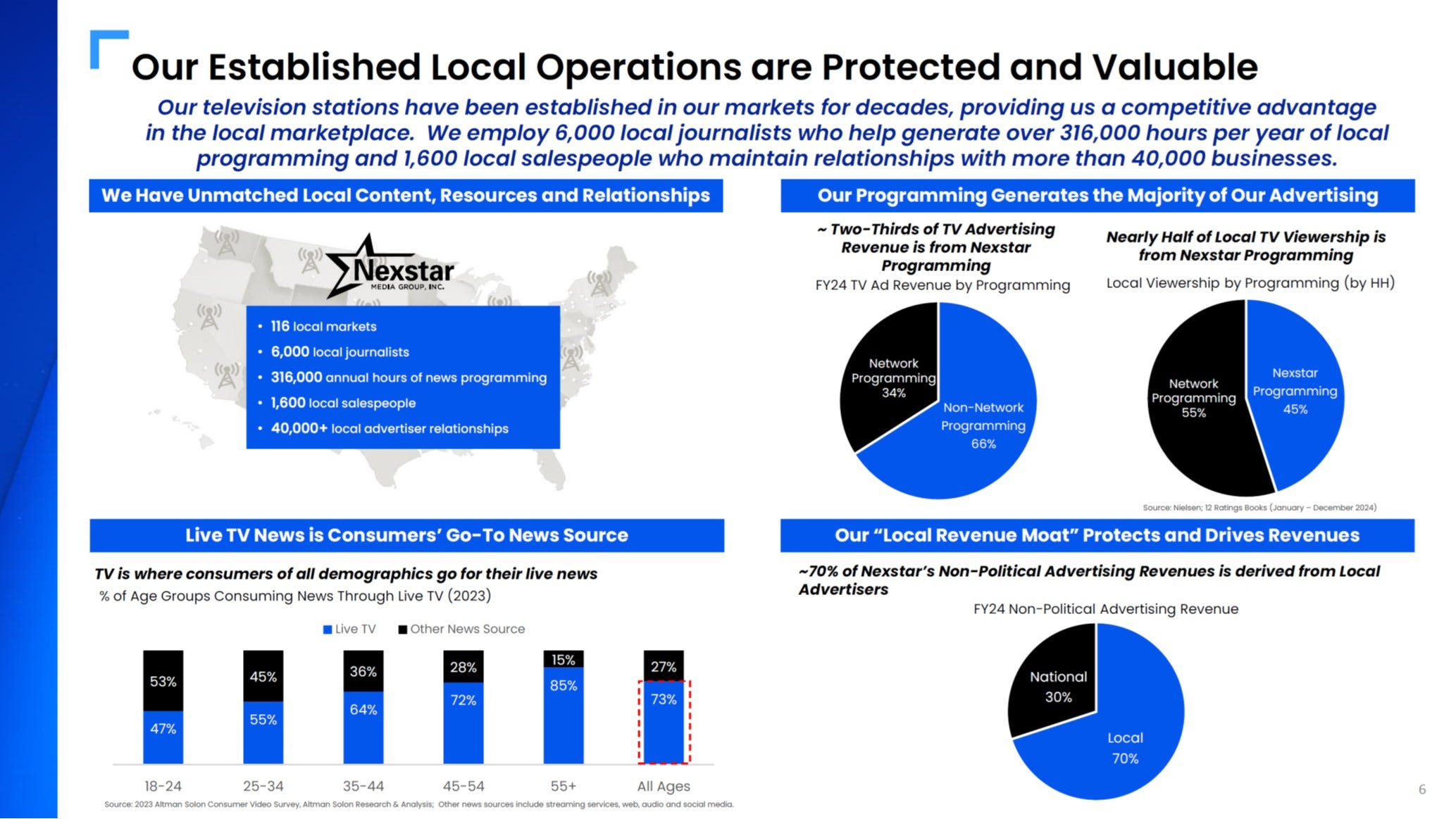

SLIDE 6 – Established Local Operations are Protected and Valuable

I agree with NXST that live local TV news is their best proprietary TV asset, and that will always help them keep subscribers. But their true #1 asset is the ability to broadcast NFL games, but that comes from their Big 4 partners – CBS, ABC, FOX and NBC.

I also agree that political ad dollars are still a big unique advantage for local TV.

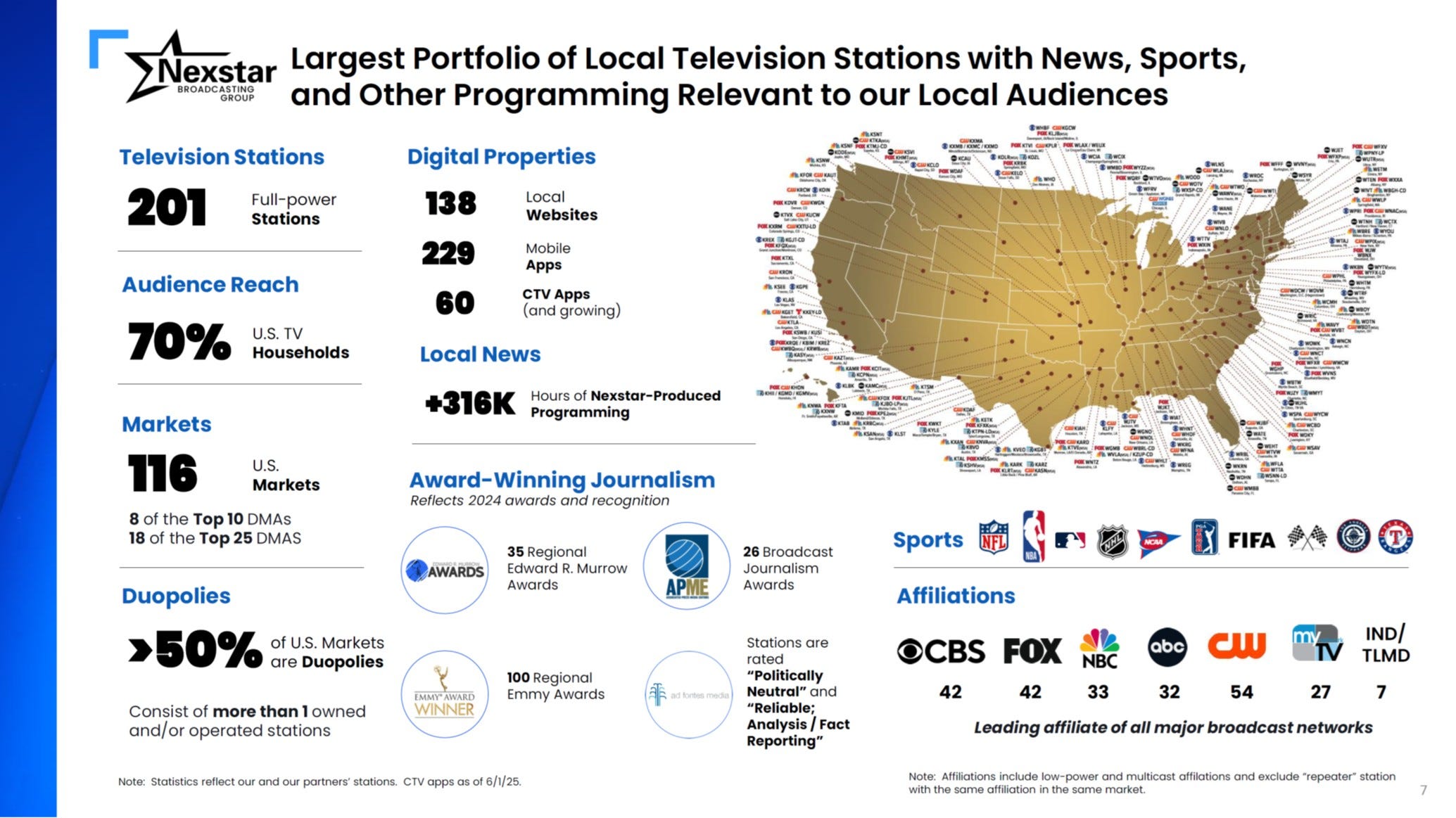

SLIDE 7 – Largest Portfolio of Local Television Stations

This is a more detailed version of the “we own lots of things” slide. Kudos to the junior analyst tasked with putting all the pins on the station coverage map.

As a bull, consider how impactful deregulation and acquiring more stations will be if NXST is already much larger than its nearest local TV competitor.

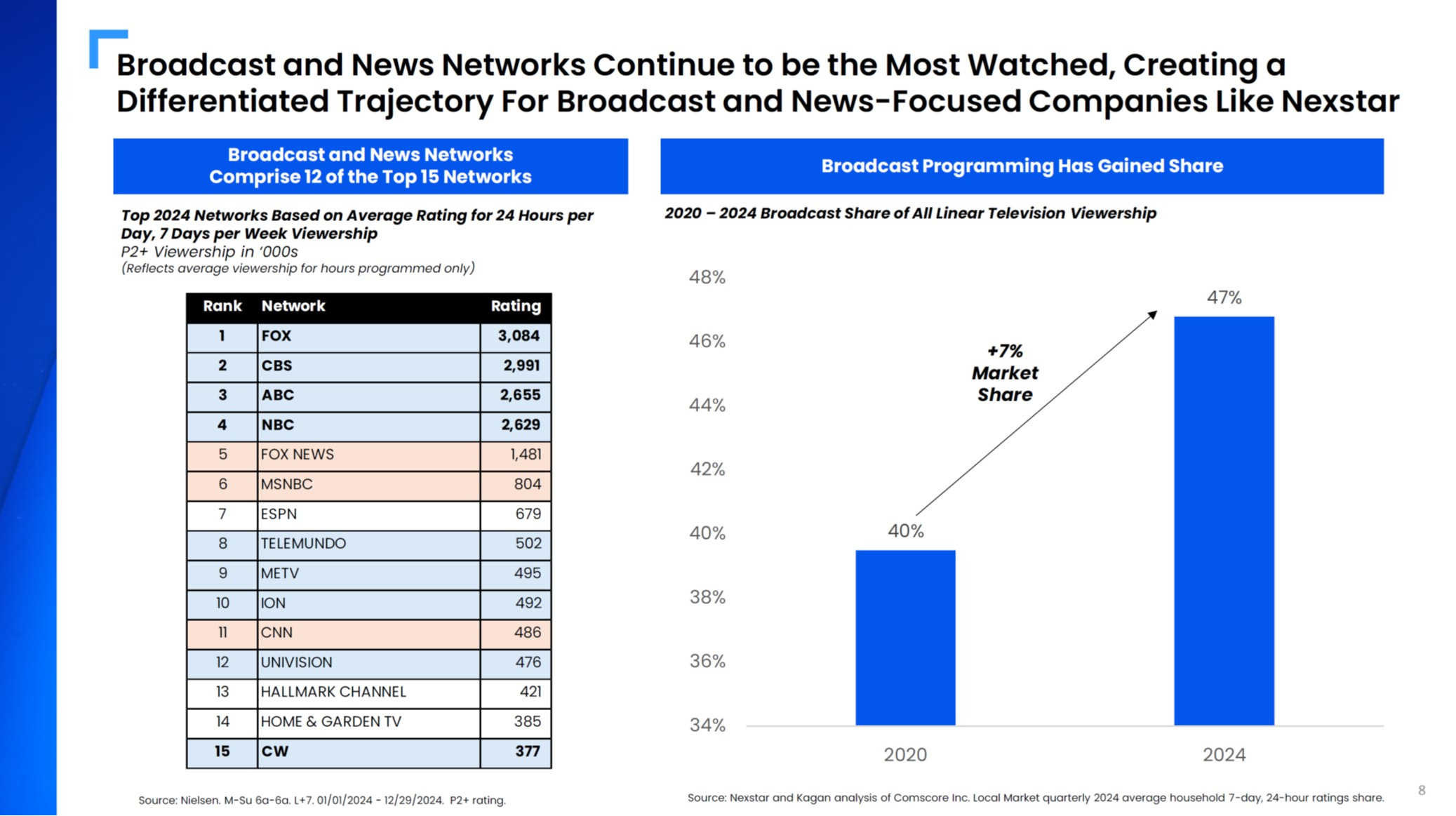

SLIDE 8 – Broadcast and News Networks Most Watched

This slide suggests that broadcast programming has "gained share," but one should consider "at whose expense?"

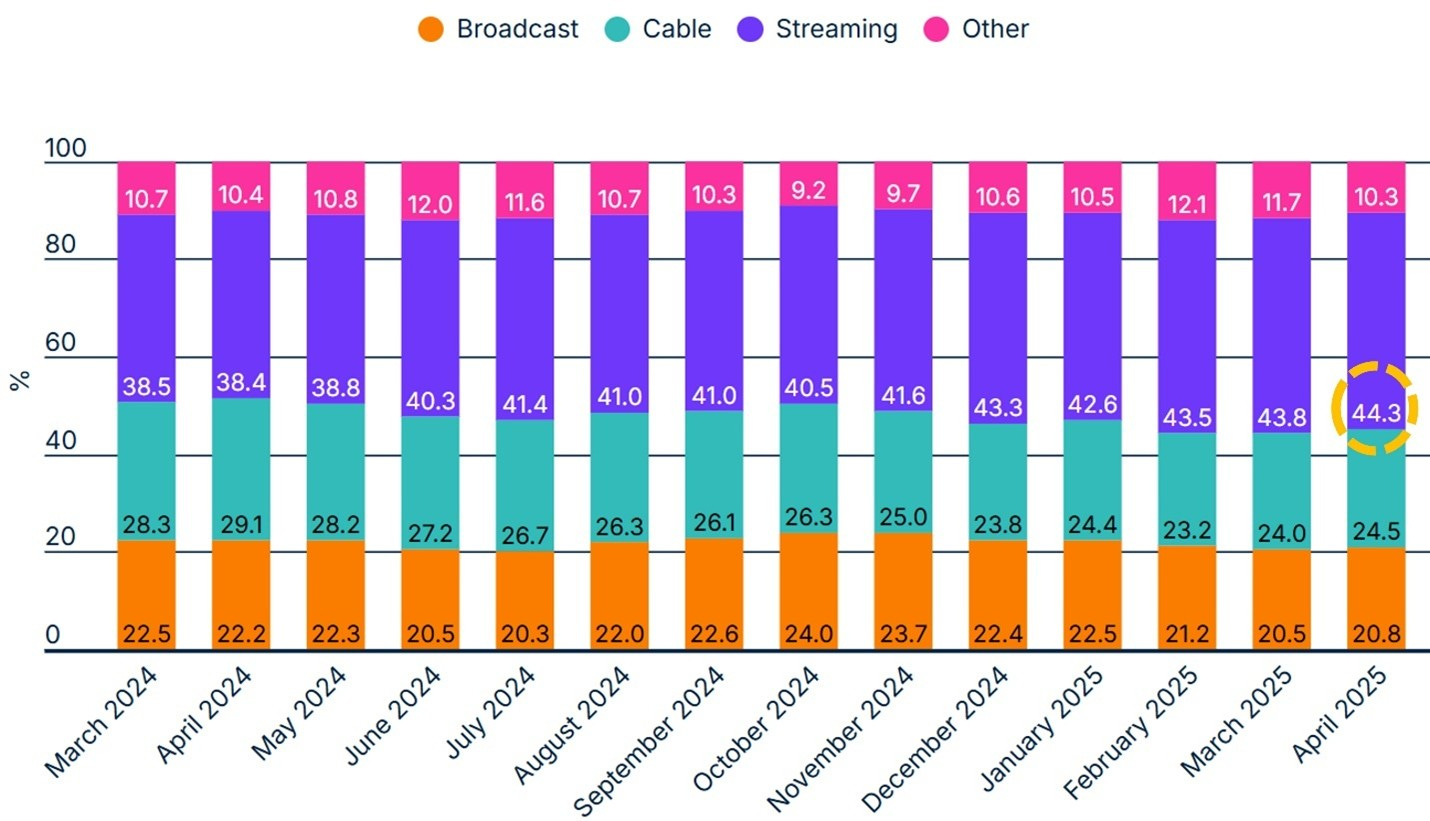

Saying broadcast has gained share “of all LINEAR television” viewership simply means that it has declined more SLOWLY than cable. On my Substack I have extensively covered the rise of YouTube taking share of big screen TV viewing.

In the chart below from the April Nielsen TV trends report, you can see that broadcast fell 7% (1.4 share points) YOY and cable fell 16% (4.6 share points). Although broadcast has mathematically gained a share of linear, this is not necessarily a positive outcome.

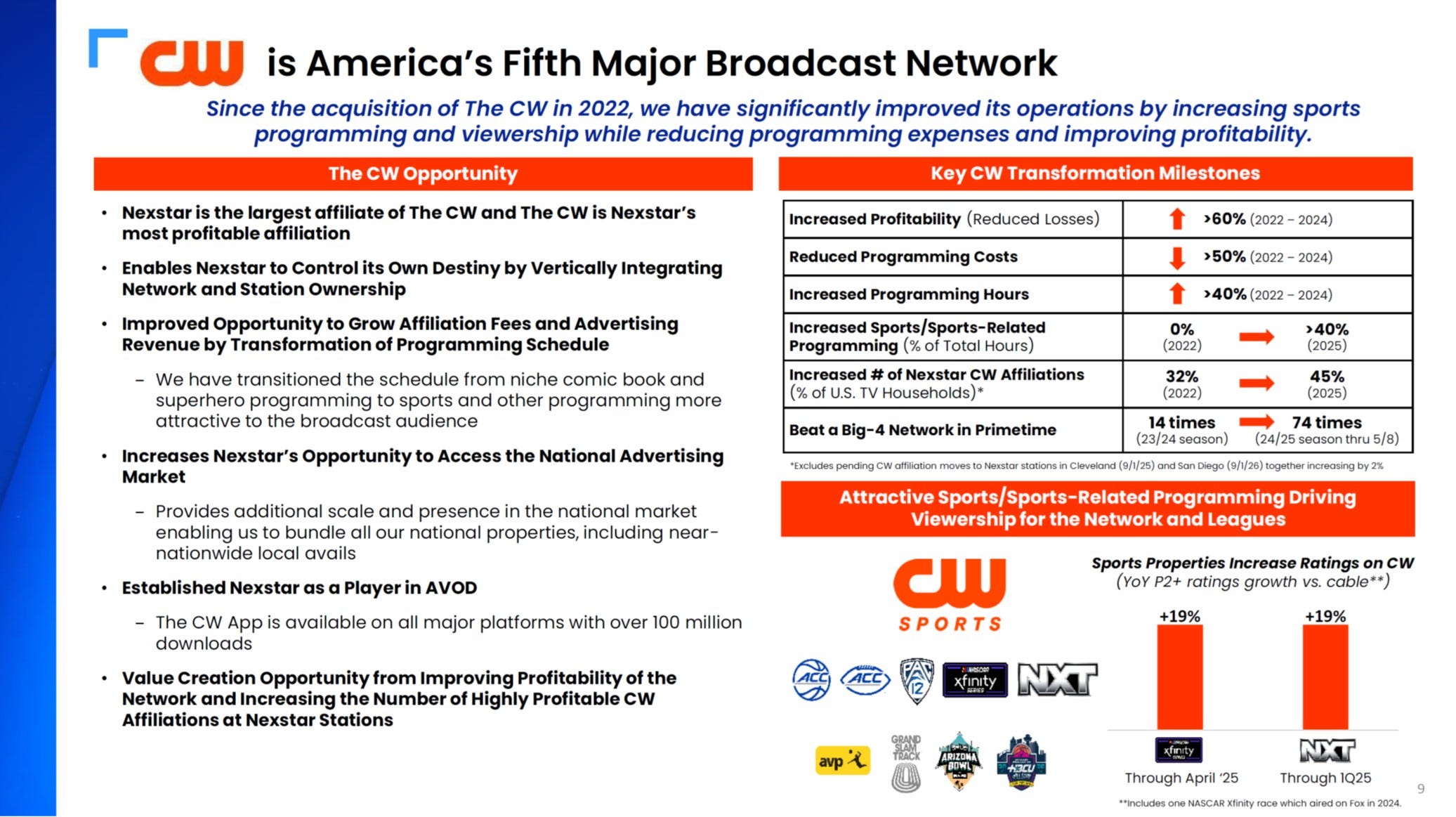

SLIDE 9 – CW is America’s Fifth Major Broadcast Network

I am not going to spend a lot of time focusing on the CW because its earnings potential is so small it is not material to the NXST story.

As I said in my Nexstar initiating coverage piece, “Cutting programing expenses to achieve profitability at the CW is welcome, but this subscale broadcast network has a tiny audience ceiling and won’t ever be large enough to move the needle on the stock”.

Oh, and one small quibble – I think TECHNICALLY the CW is America’s 5th major ENGLISH language broadcast network. I don’t have the most recent ratings, but I know Spanish language networks Univision and Telemundo often rate higher than the CW.

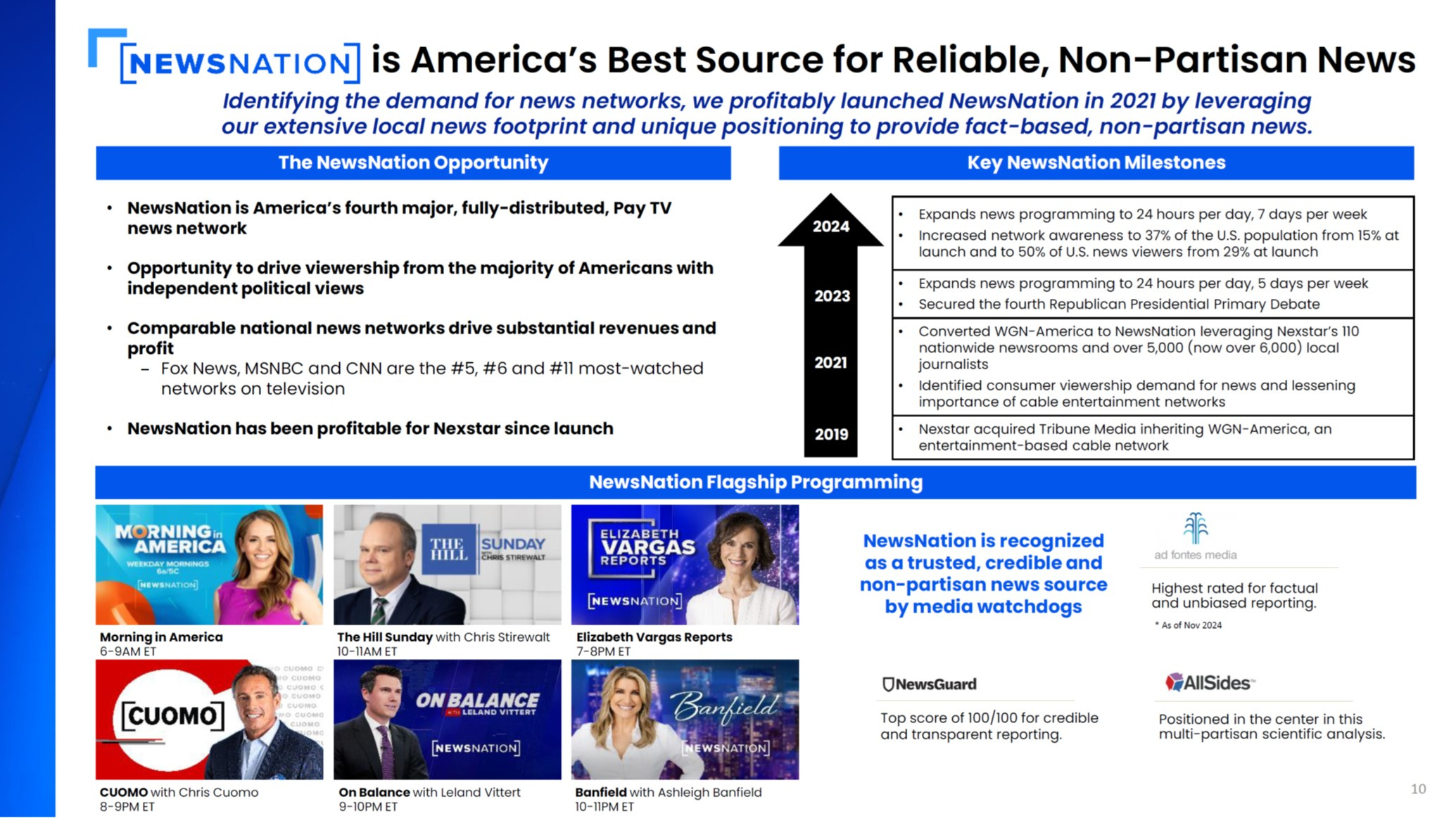

SLIDE 10 – The NewsNation Opportunity

Just as with the CW, I am not going to spend a lot of time focusing on NewsNation because its earnings potential is so small it is not material to the NXST story.

I think Fox News ($FOX) is the only publicly traded cable news business that’s worth talking about. NewsNation, as well as NewsMax, are ultimately subscale linear networks that were founded 10 years too late. See my YouTube analysis here - Understanding Newsmax: A Closer Look at FY 2024 Earnings.

SLIDE 11 – ASTC 3.0 Opportunity

It is probably worth doing a separate “expectations” vs. “reality” post where I explain why I’m skeptical that ASTC 3.0 presents any real revenue opportunity for broadcasters. In short, after over a decade of promise, this enhanced broadcasting standard has failed to gain enough traction with any constituency large enough to spur mass market adoption.

Don't include ASTC 3.0 revenue in your future forecasts if it remains a niche interest of broadcast bulls and is never rolled out nationally at scale.

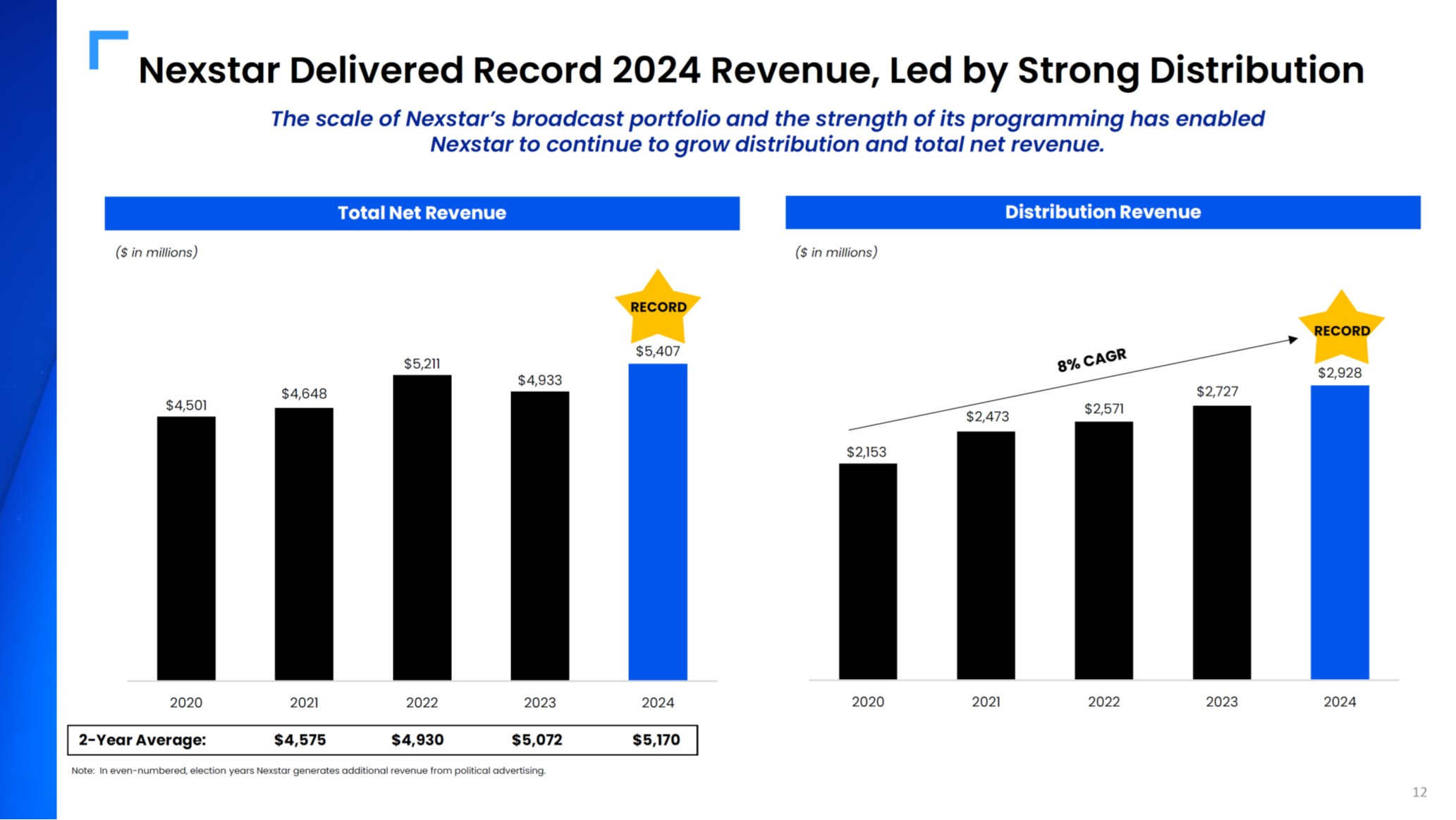

SLIDE 12 – Nexstar Delivered Record 2024 Revenue

This slide is too backwards looking. NXST correctly states distribution (affiliate fees, or retransmission fees from cable companies) was the main revenue driver, however this segment has two major headwinds.

Distribution revenue growth is going to be weaker going forward due to 1) continued erosion of the pay TV ecosystem through cord-cutting, and 2) Big 4 networks clawing back those fees by charging NXST higher reverse-retransmission fees.

I think it is inevitable that Big 4 networks ultimately take back more than 50% of the distribution revenue from local TV players as payment for the high-value sports programming they provide the affiliates.

SLIDE 13 – Broadcast Continues to be Underpaid Relative to its Strong Ratings

A lesson I learned working across several media companies is that EVERYBODY in the media value chain thinks they are “underpaid” relative to their audience. You must interrogate this claim thoroughly whenever you hear it as a media investor.

Nexstar is asserting that cable companies should allocate a larger proportion of subscription fees to them, compared to the cable networks, based on their ratings. This is the taste of the pitch NXST and other broadcasters make whenever their carriage deals with companies like Charter and Comcast are up for renewal.

But as the saying goes in business, “you don't get what you deserve, you get what you negotiate”. Last month I did a post on how a stock pitch I wrote on Tribune Broadcasting won the Ira Sohn Investment idea contest 12 years ago. In it, I showed that for over a decade broadcast TV stocks benefited from a powerful tailwind of cable providers paying them increasingly higher subscriber fees.

Cable providers have announced that they will not increase payments to TV network owners and do not prioritize video customers.

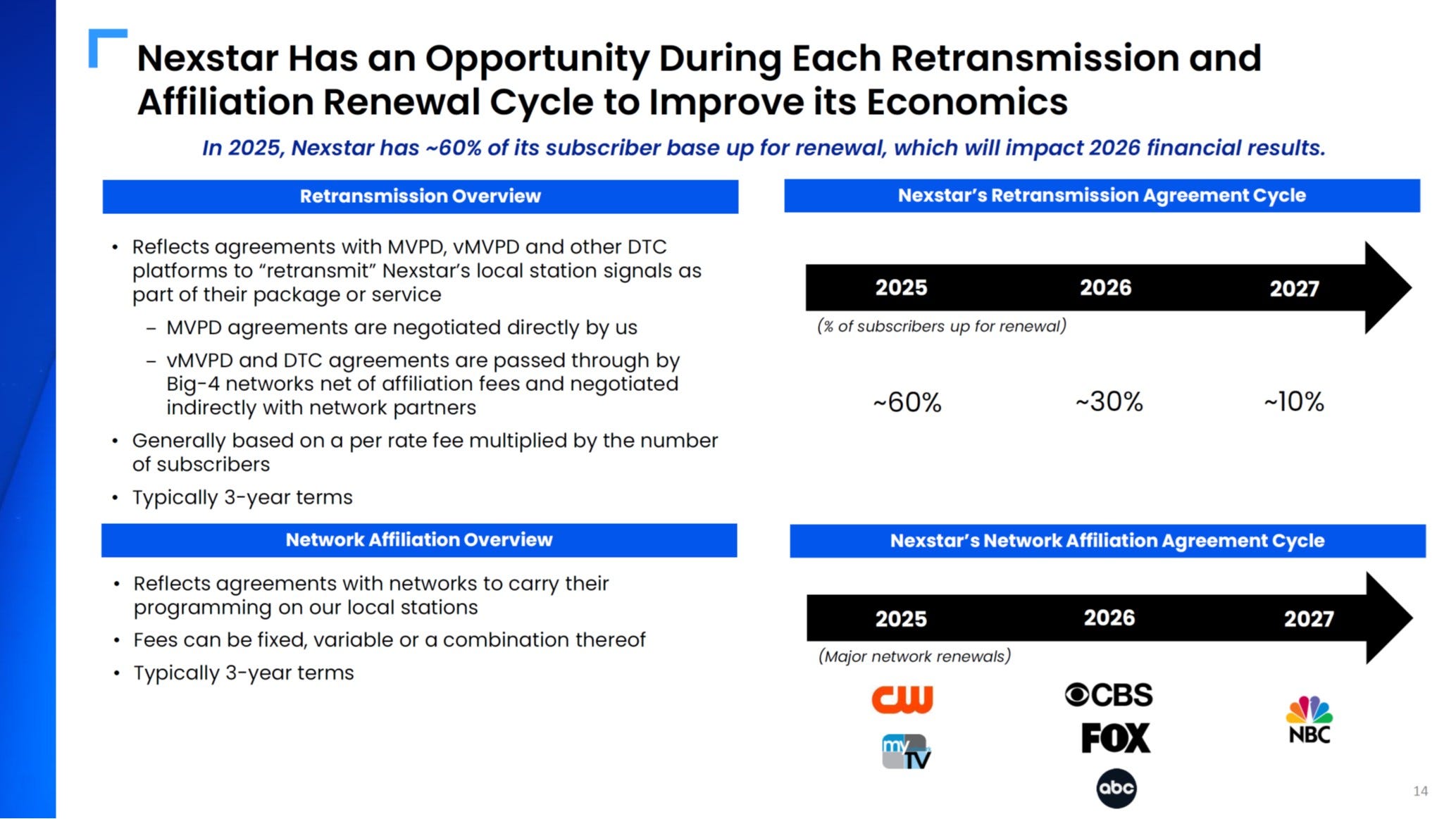

SLIDE 14 – Opportunity to Improve Retransmission/Affiliate Economics

This slide may be where I most fundamentally disagree with Nexstar management, and local TV stock bulls more generally.

Going forward - I think NXST, and all affiliate broadcasters, will be at a strategic DISADVANTAGE on both fronts. Cable/satellite providers have leverage over Nexstar, so retransmission revenue will grow more slowly. And I think investors are underestimating the extent the Big 4 networks will try to claw back the economics from the local affiliates. NBC, ABC, FOX and CBS can both charge NXST more for network programming and demand they give back a greater share of the retrans dollars.

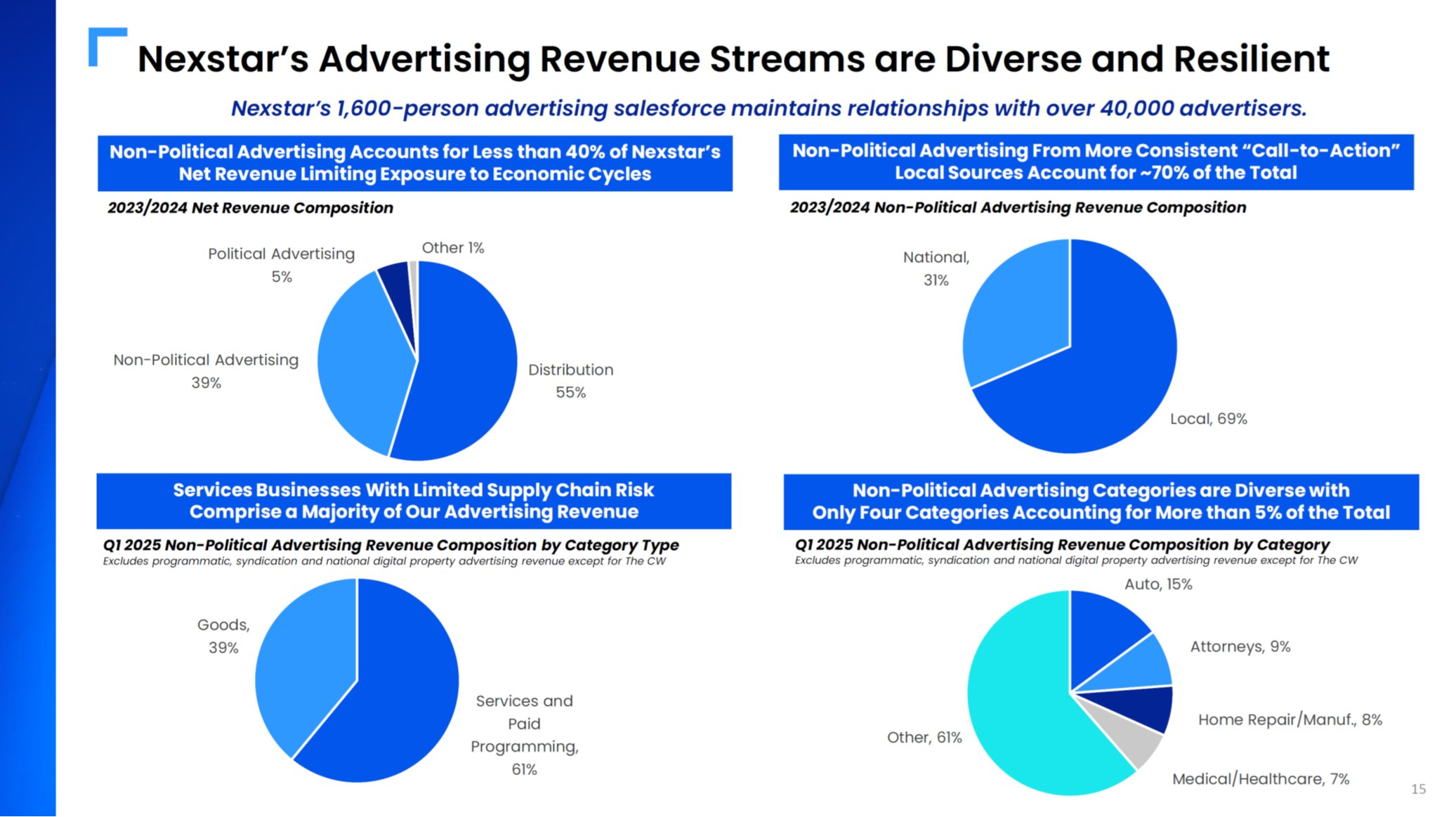

SLIDE 15 – Advertising Revenue Streams are Diverse and Resilient

I think local TV does have a competitive advantage with their local salesforce, as many local small/medium business owners want high-touch service when buying ads for their car dealerships and law firms.

However, I think the local salesforce advantage gets diluted each year, as more business owners are comfortable shifting their ad budgets to Facebook (Meta) and Google. Your cell phone is the ultimate “local” advertising distribution medium.

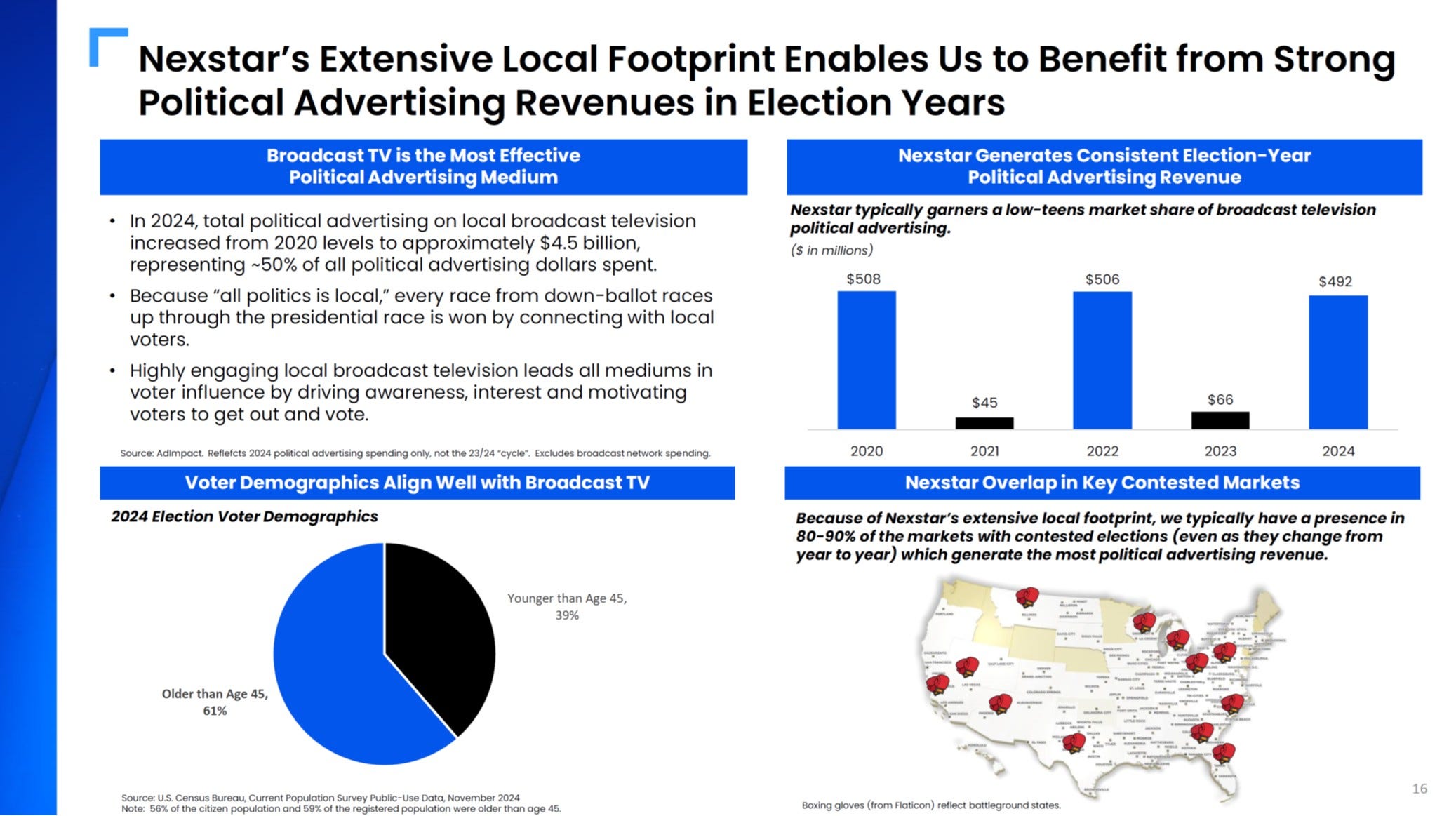

SLIDE 16 – Local Footprint Benefits from Strong Political Advertising

Political ad buys on local television I think will still be a staple of political campaigns, even after streaming is over 50% of TV viewing.

I just want to warn everyone that Political ad dollars are incredibly volatile, difficult to predict and tend to come in about 90 days prior to an election. This revenue is “nice to have” but businesses that rely on this deserve a lower valuation multiple.

Also, given the rise of podcasts, I wouldn’t be surprised if more political ad dollars shifted to digital in the 2026/2028 cycle.

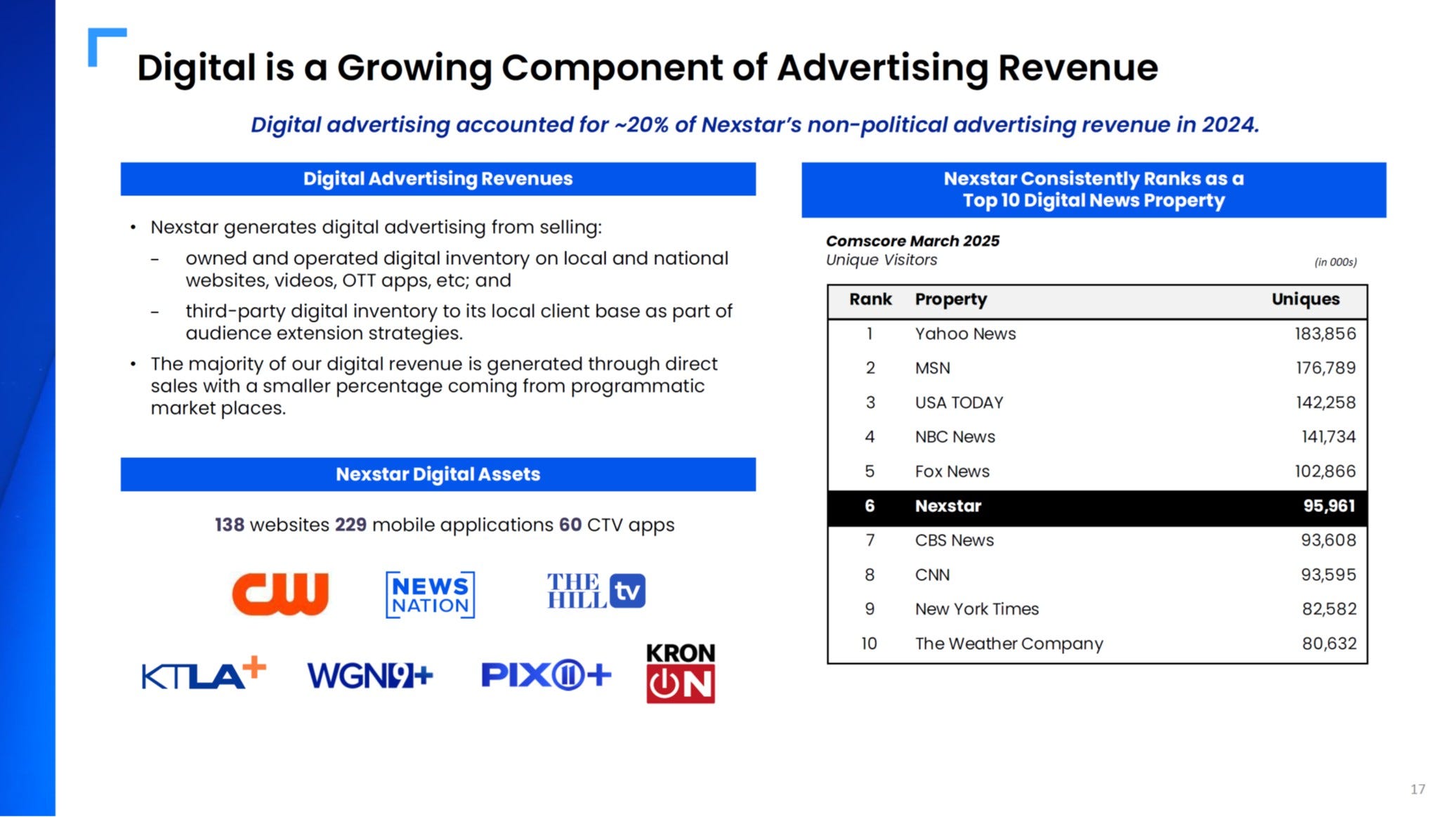

SLIDE 17 – Digital is a Growing Component of Advertising Revenue

I used to build KPI dashboards and do revenue analytics for local and TV radio sales teams. Along the way, I realized that the entire way local TV companies frame their “digital” business is a bit of a misnomer.

Linear companies love to tout their digital segments with the explicit goal of trying to convince the market that their stocks deserve a higher multiple. Nexstar is not unique – see my write-up on Starz ($STRZ) where they brag that 70% of their revenue is digital.

I would argue that many “digital” businesses are just extensions of a linear-based product. A truly “digital” product or service is one that would exist on its own, even if the underlying terrestrial TV (or radio) signal went away. Digital businesses that rely on linear to survive do not deserve higher earnings multiple.

Nexstar’s digital assets are mostly the website and the mobile apps associated with their 100+ local market stations. Their customers who purchase digital are mostly doing it as part of a larger ad-buy on the linear network. The local salespeople at these stations are incentivized to make sure their clients allocate a certain portion, 10% - 15% for example, of their ad budgets so they have variety.

I will cover this topic in more detail in future posts, but digital never ends up growing its share of the revenue mix more than ~15% because it is not a core demand of clients. After all, in 2025 if you want to buy digital ads you have better options than your local NBC affiliate.

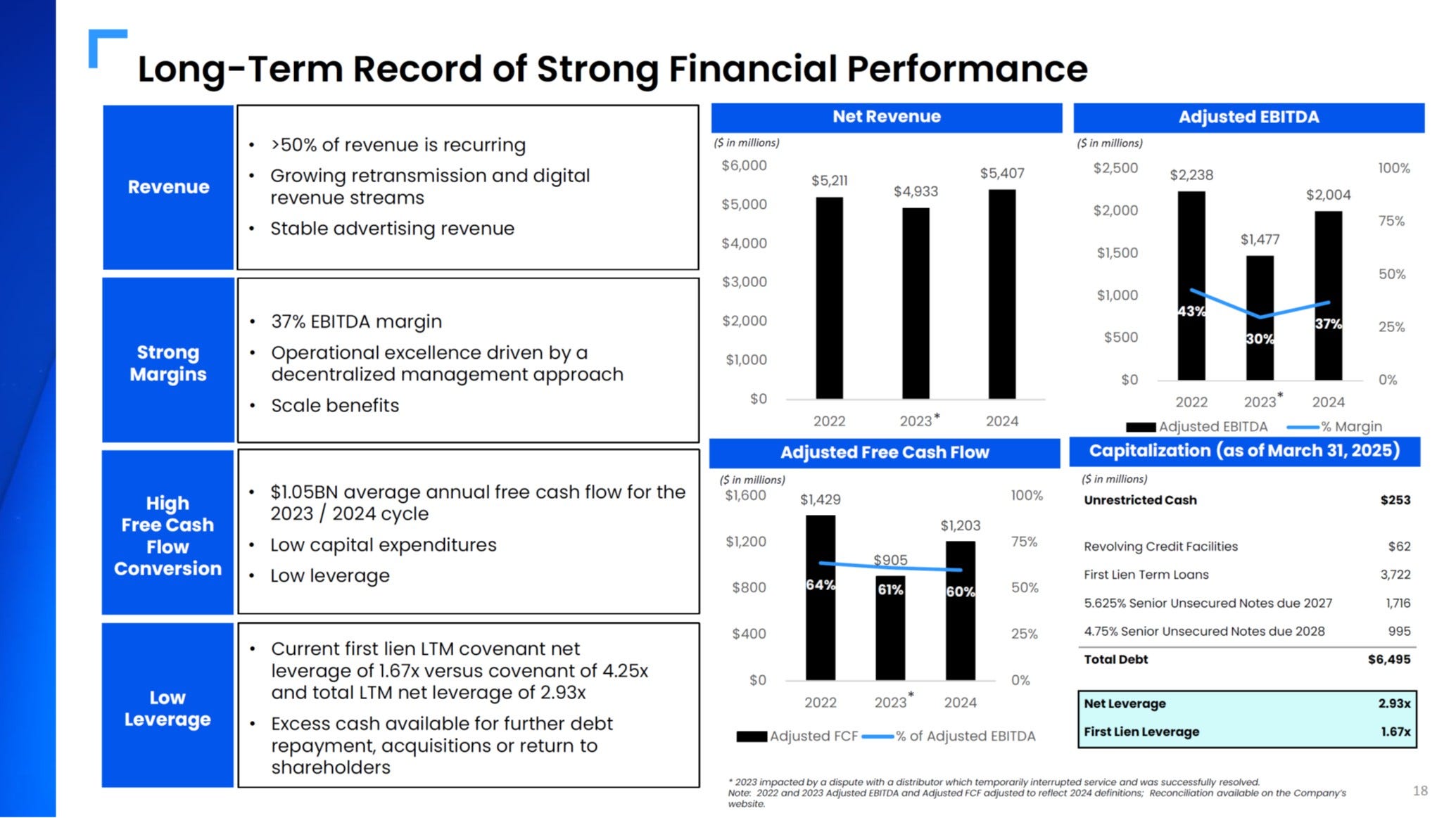

SLIDE 18 – Long-term Record of Strong Financial Performance

This entire slide is backward looking. I think it is telling that NXST won’t stick their neck out and provide 1-2 year forward guidance.

Earnings multiples are based on future growth expectations so that’s why TV broadcasters, and other media companies, often love focusing on LTM figures. You tend to romanticize the past when you know the future won’t be as bright.

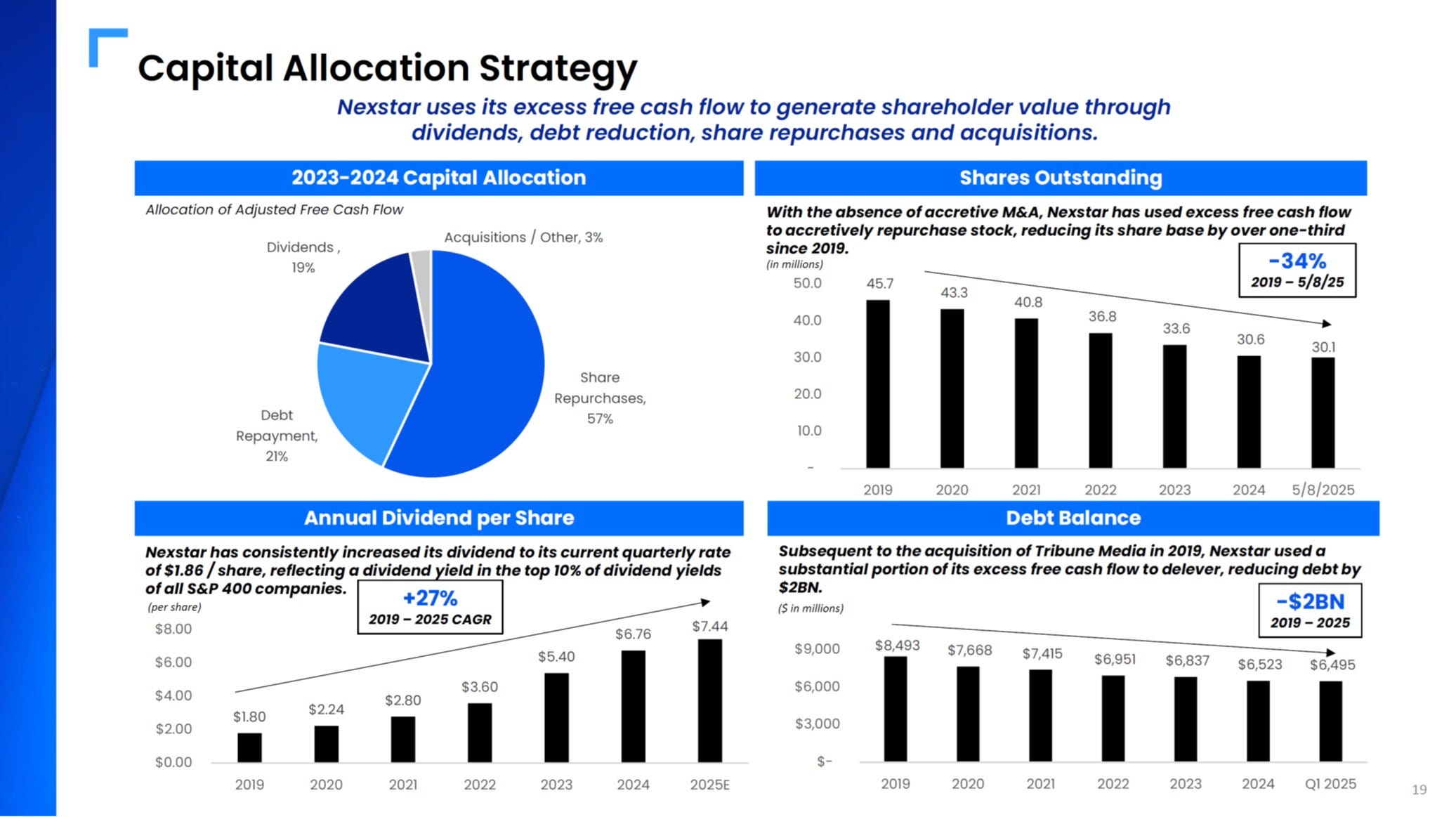

SLIDE 19 – Capital Allocation Strategy

The point of this slide is to say “NXST stock price will have downside protection because of the dividends, debt paydown and buybacks”. I disagree.

In my last post on Nexstar, I gave my take on their capital allocation strategy. My feelings have not changed in the last month:

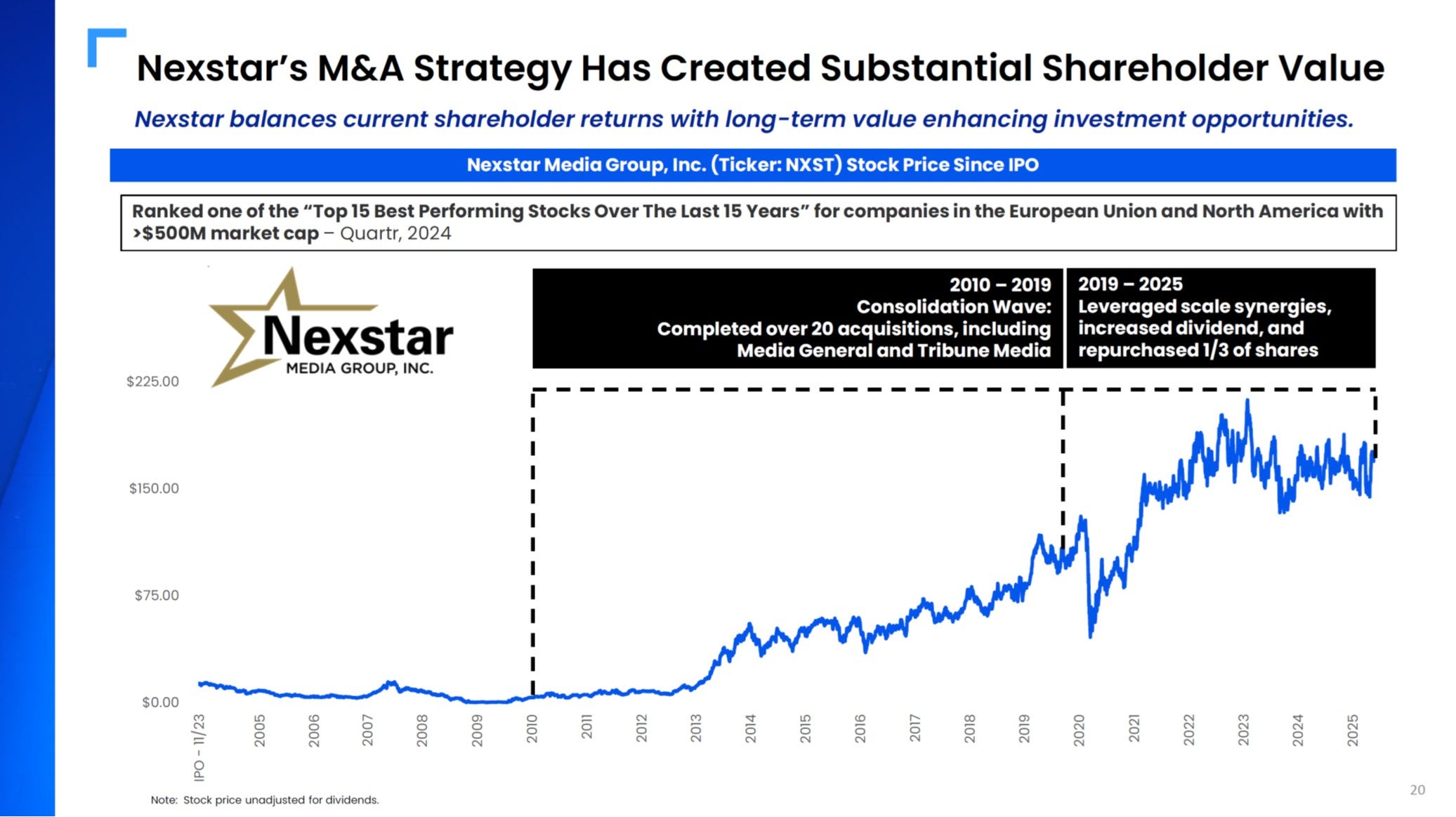

SLIDE 20 – Nexstar’s M&A Strategy Has Created Substantial Shareholder Value

I want to remind the reader of the adage - "past performance is no guarantee of future results". A historical chart of NXST’s stock price provides no predictive information to help us evaluate it going forward.

This chart almost feels like they are trying to entice retail investors who may be less discerning of the risks.

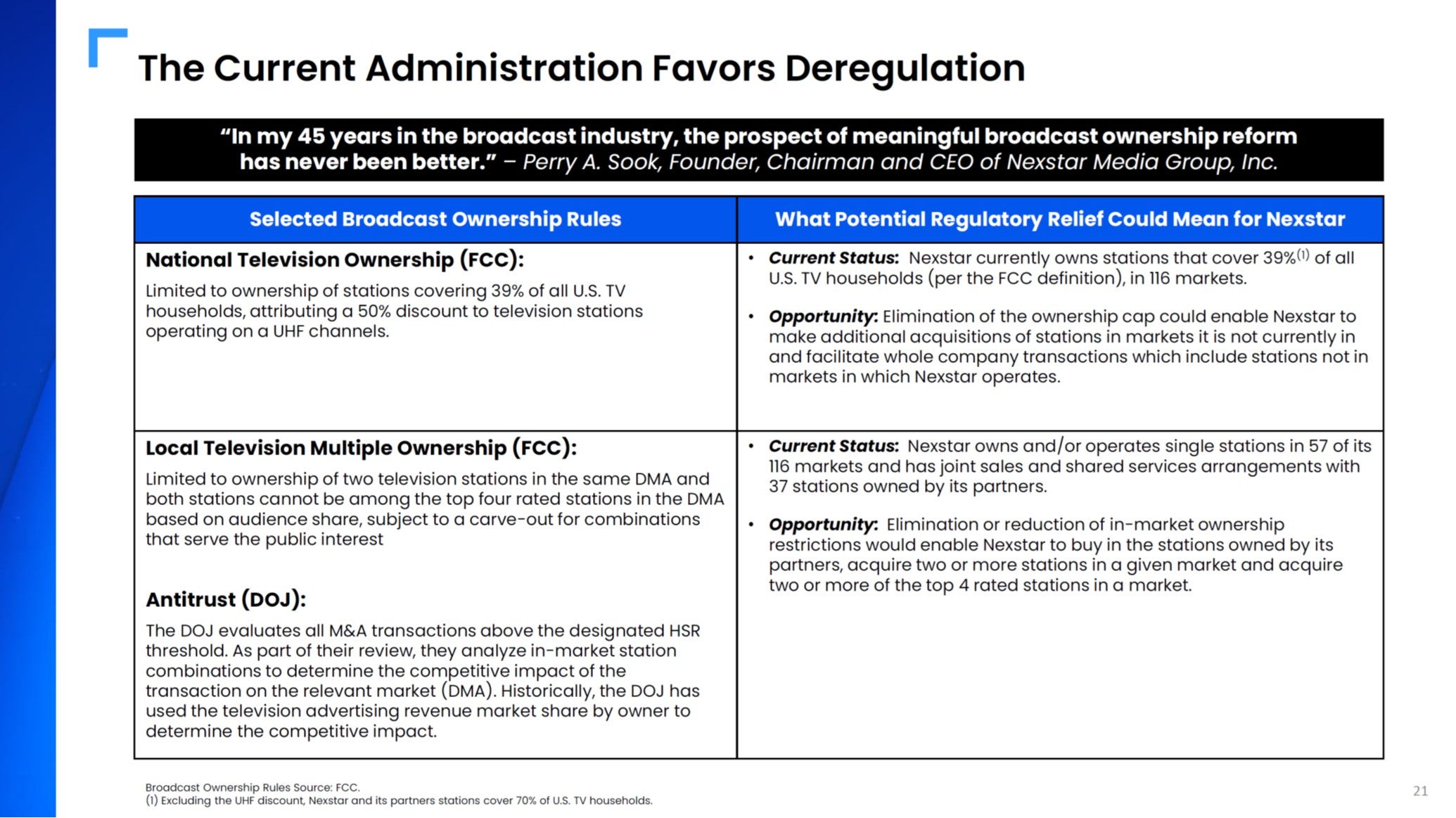

SLIDE 21 – The Current Administration Favors Deregulation

Let state plainly, I think equity investors banking on “deregulation” to drive massive returns in NXST, SBGI, TGNA and other stocks are setting themselves up for major disappointment over the next few years.

Deregulation cannot repair problems that regulation did not cause. I maintain that the biggest issue for local broadcasting stocks is that at a macro level their audience is leaving the medium. Loosening of the M&A rules does nothing to reverse this existential problem. Taking on debt, to purchase more melting ice cubes is not the fault of the U.S. government.

Again, I refer you to earlier in the deck where NXST said they reach “70% of U.S. TV households”. Nexstar and others have already exploited the numerous loopholes in current regulations. While I expect some M&A activity to occur – I think the winners will be those who decide to sell their stations.

P.S. – If you haven’t already – please Google the returns of broadcast stocks during the first Trump administration when broadcasters had a “business friendly” FCC Chair. Sinclair Broadcasting ($SBGI) can tell you; it was not all sunshine and roses!

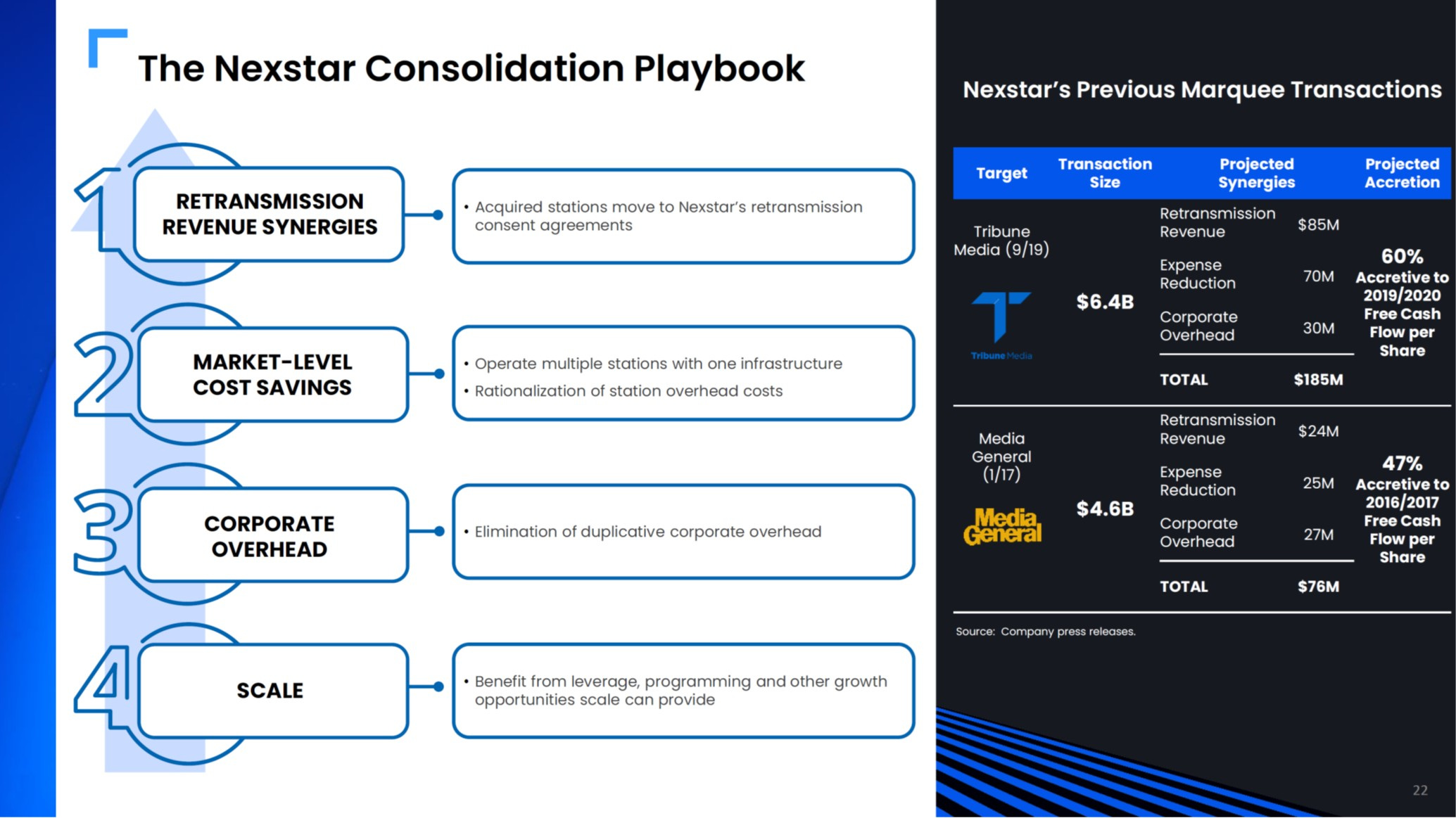

SLIDE 22 – Nexstar Consolidation Playbook

This playbook is giving the standard fare when it comes to rolling up and combing local TV stations. Nothing new here.

Let me point out on the right side under “Previous Marquee Transactions”. I think the “Projected Synergies” taken as a percentage of the total transaction size, shows the limits to the M&A strategy. Tribune’s synergies were only 2.9% of the purchase price ($185M / $6.4 Billion) and Media General’s synergies were only 1.7% ($76M / $4.6 Billion). Presented this way, as a long investor I would be concerned that a multi-billion acquisition can only generate an incremental 2% - 3% of value. That seems like a low payout for all that work!

SLIDE 24 & 25 – Market Shifts are Benefiting Broadcast

While I don’t disagree that broadcast station channels are “core” to new, smaller pay TV bundles – I question how much of those economics will NXST get to enjoy? If you take NXST’s claim at face value, this will further incentivize Big 4 networks (ABC, FOX, CBS and NBC) to demand affiliates such as NXST to pay back more to the parent, leaving less margin for themselves.

I disagree that pay TV subscriber trends will improve. YouTube is steadily taking share of big screen TV viewing each month, even outpacing Netflix, and is showing no signs of slowing down.

It is true that “sports is expanding /maintaining broadcast presence” – which means NXST will ultimately have to give back more in reverse-retransmission fees for the privileged right to show NFL regular season games. With more and more sports leagues putting games on streaming platforms, this risk will only increase.

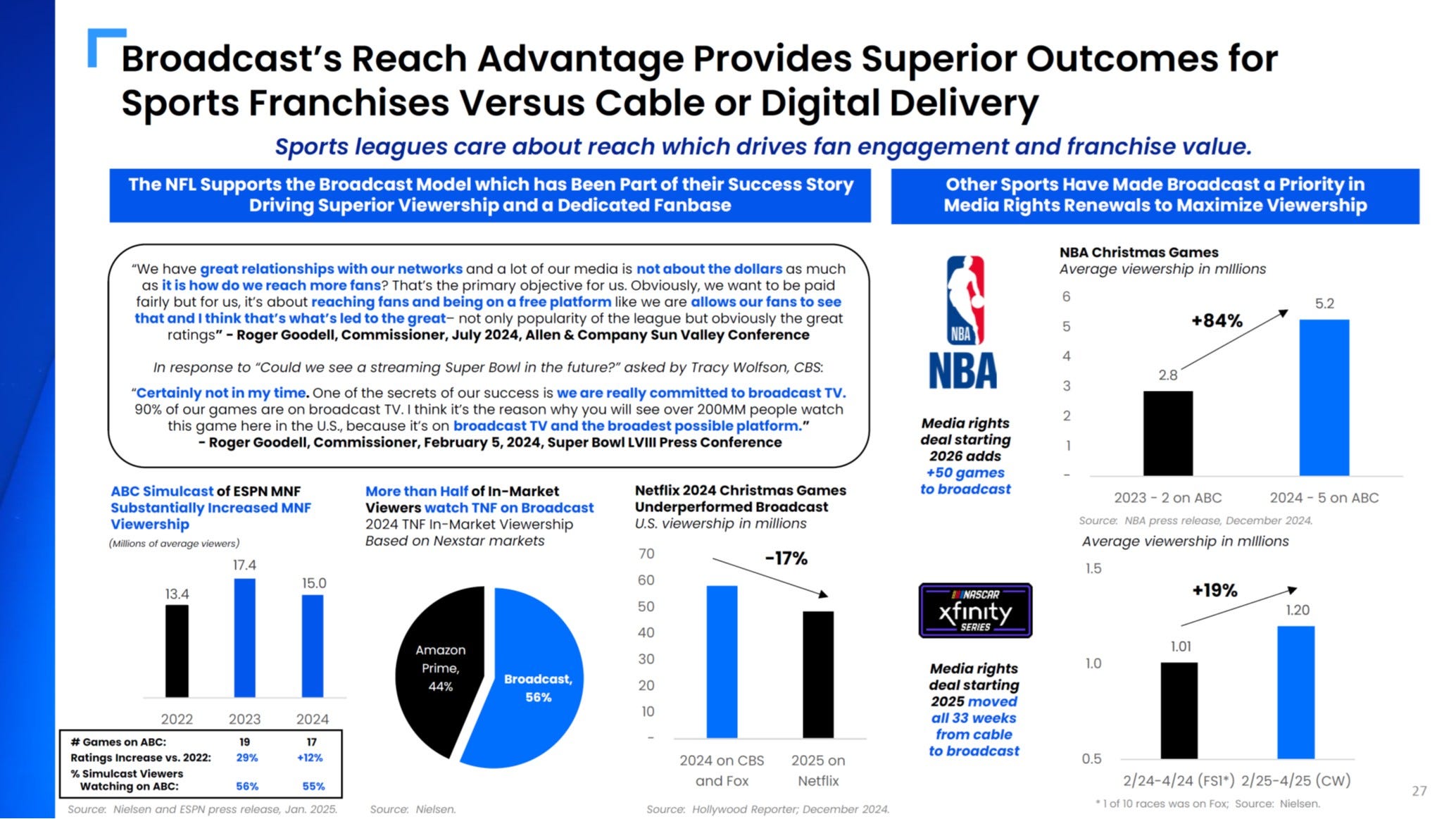

SLIDE 26 & 27 – Sports Franchises are Committed to Broadcast

While the claim is true, the sports league’s allegiance is to the broadcast NETWORKS (ABC, CBS, NBC and FOX) and is not to the local affiliates.

All the Big 4 networks have streaming services and are increasingly able to maintain, and expand, their audience reach without local TV.

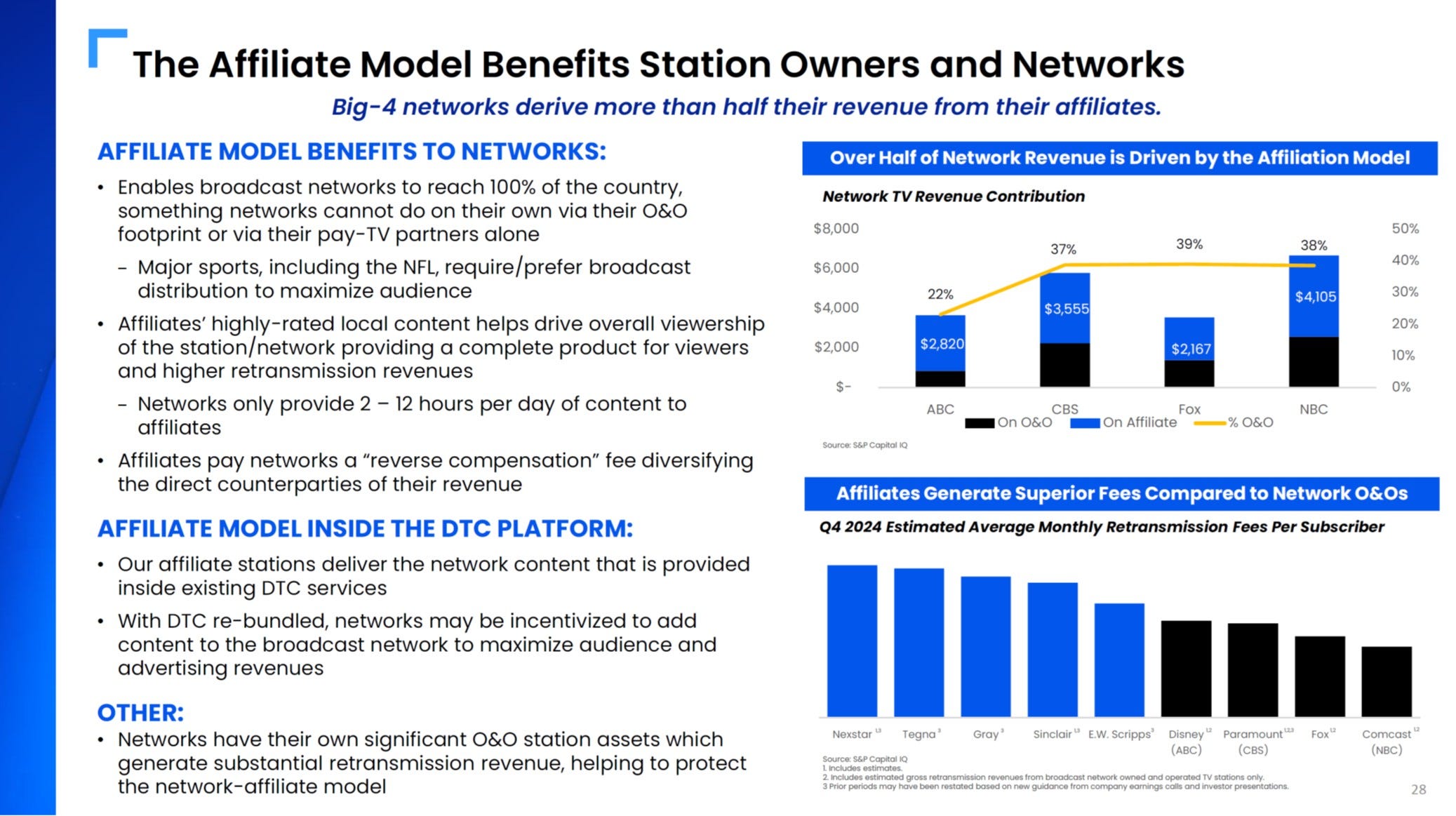

SLIDE 28 – The Affiliate Model Benefits Station Owners and Networks

This slide is supposed to be an endorsement of affiliate stations, but counterintuitively the entire thing reads like a big red warning.

“Big-4 networks derive more than half of their revenue from their affiliates”…Yes - and they will keep taking MORE revenue going forward. The affiliates do not have the bargaining leverage here!

SLIDE 29 – Broadcast Stations Provide the Content Regardless of Technology

I am not a fan when media companies pitch us on their “technology”. Tech is not why people buy television stocks!

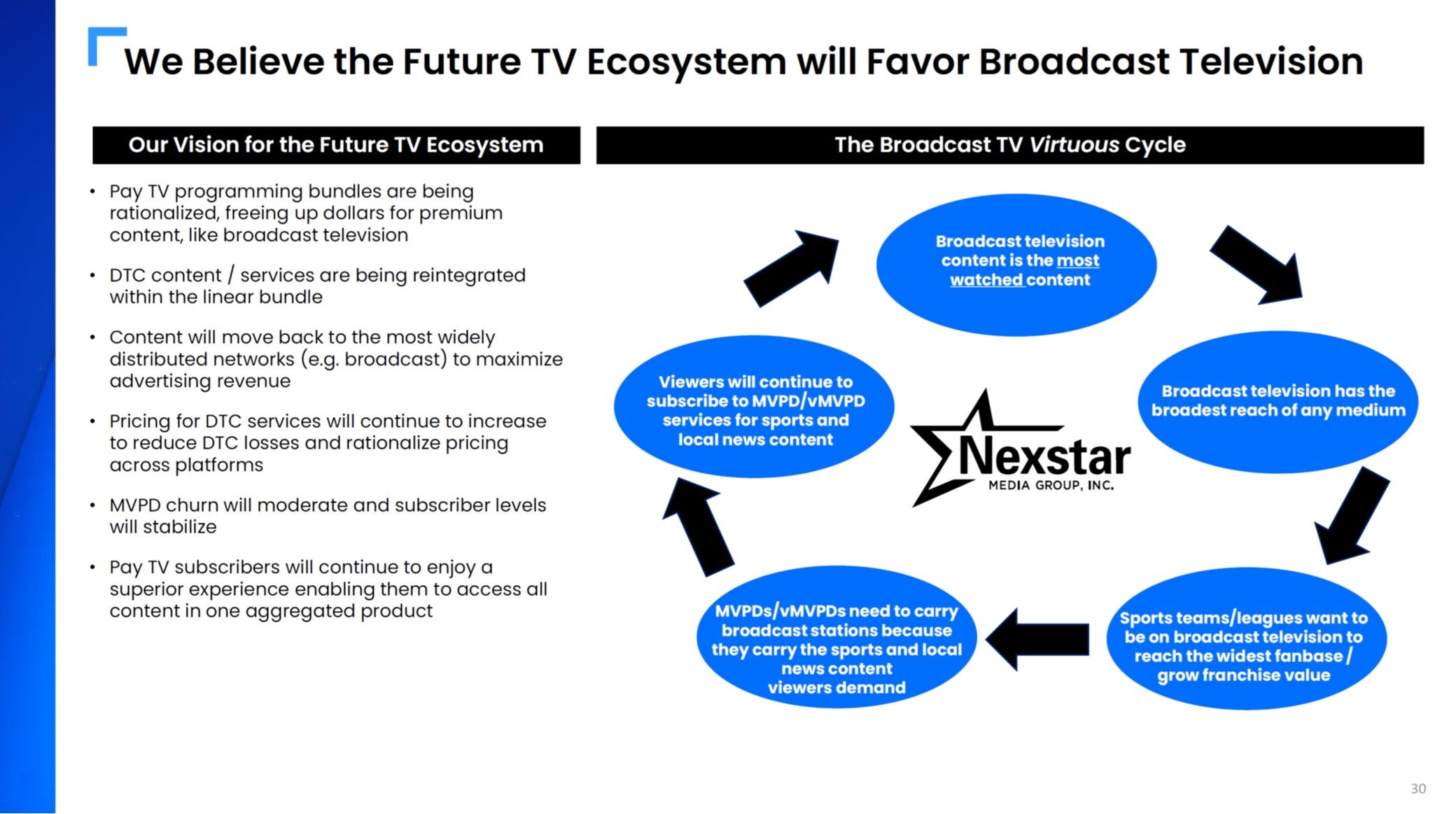

SLIDE 30 – We Believe the Future TV Ecosystem will Favor Broadcast Television

This final slide is aspirational, but market share is won through solid execution and not just hopes and dreams.

I will give NXST credit for putting together a very thorough investor presentation of their industry thesis. If the pay TV ecosystem can stop the audience attrition, then NXST, SBGI, TGNA and others could be great levered bets. And once the next M&A wave gets started, NXST can surely find some private station groups where they can squeeze out some synergies. But until the audience exodus to YouTube stops, I would much rather be a SELLER of local TV stations than a buyer.

-Accrued Interest