Comcast Says the Quiet Part Out Loud

Comcast is spinning off NBCUniversal and Sky — my first take on the biggest TMT breakup in years.

Accrued Interest TLDR: Comcast is spinning off NBCUniversal and Sky into a separate public company, and after fifteen years of insisting that content and distribution belong together, I read this as a tacit admission that the synergies never really showed up. The most valuable company this split creates is the one keeping the Comcast name: a clean broadband utility the market can finally re-rate, which is exactly what today’s tape reflected. NBCUniversal walks out as a predator, not prey — barred from being acquired for roughly two years, but free to go shopping itself. I’m skeptical of the “stronger apart” pitch for the media side, which loses Comcast’s balance sheet just as the sports-rights and carriage wars heat up. And the orphaned Versant networks look lonelier than ever.

Please subscribe (free) to read the rest of this Accrued Interest deep dive. I send these to 1,400+ investors and operators who care more about what really moves the needle than what the spreadsheet whispers.

Introduction

This one hits close to home. I began my career as a TMT analyst at Goldman Sachs from 2008 to 2010, sitting a few seats from the team grinding through the original Comcast–NBCUniversal acquisition — the deal that defined the “content meets distribution” paradigm the entire media industry has been organized around ever since. So when Comcast announced on its 8:30 AM investor call this morning that it was spinning off NBCUniversal and Sky into a separate public company, it felt like a full-circle moment. The experiment I watched get built at the start of my career is now being taken apart, in public, and — ironically — by the same people who built it.

This is a first take, written hours after the announcement with only a thin investor deck to go on. But the strategic message is loud and clear. I’ve laid out my Top 10 takeaways below so you can follow exactly how I’m thinking — and let me know where you disagree.

Let’s dive in.

The Deal, in Plain Terms

In case you haven’t heard by now, here is what was announced this AM:

A tax-free spin-off of NBCUniversal (including Sky, the European media and pay-TV business) into a separate, publicly traded company.

12-month timeline, targeting completion around June 2027. (No shareholder vote required.)

NBCUniversal keeps the crown jewels: Universal’s film and TV studios, the theme parks (including the brand-new Epic Universe), the NBC broadcast network, Telemundo, Bravo, Peacock, and Sky.

Comcast keeps the pipes: Xfinity broadband, wireless, business services, and the nation’s largest converged network passing more than 65 million homes and businesses.

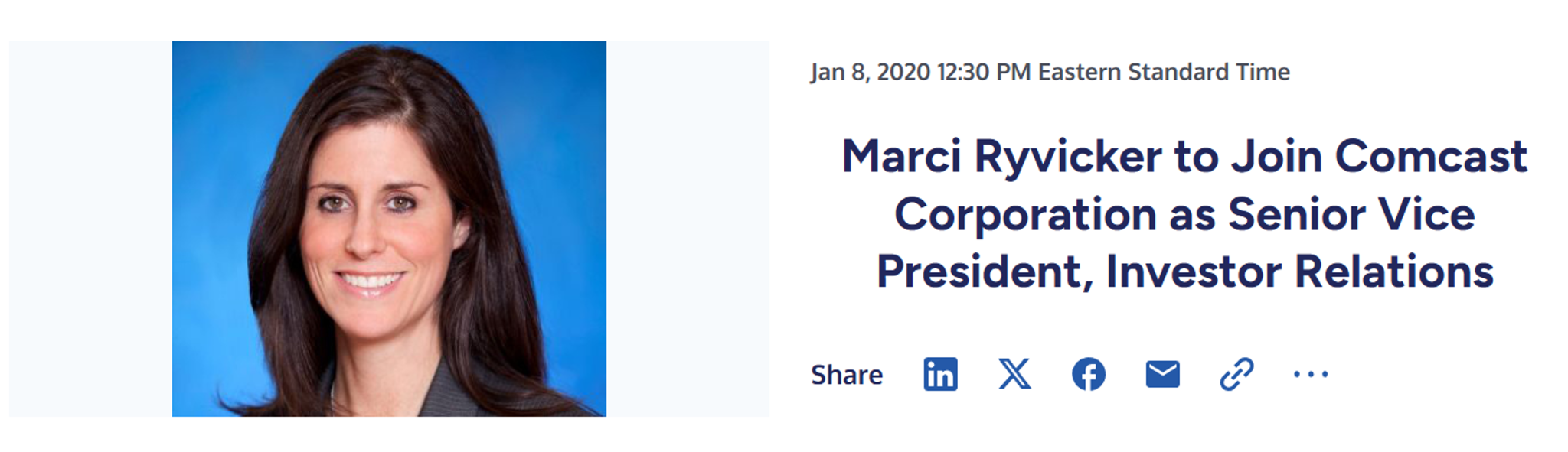

Leadership: Mike Cavanagh becomes CEO of the independent NBCUniversal. Former CFO Michael Angelakis returns to run Comcast. Brian Roberts stays Chairman and remains involved in both. And — this matters — Marci Ryvicker, Comcast’s head of Investor Relations and a former top-ranked TMT sell-side analyst, is clearly the architect of how this story is being told.

Comcast will retain up to 19.9% of NBCUniversal, to be sold off for cash over time in a tax-efficient way and used to pay down debt.

Comcast is suspending its share repurchase program, redirecting that cash to set up both companies with strong, low-debt balance sheets from day one.

1. This Is a Retreat, Not a Bold New Strategy

I spent more than a decade building investor decks like the one Comcast put out this morning, so let me translate what management is thinking but can’t say outright.

This is a capitulation — a graceful one, wrapped in the language of “enhanced strategic focus,” but a retreat all the same.

About fifteen years ago, Comcast made the bet that owning both the content (NBCUniversal’s shows, movies, and channels) and the pipes (the cable operator that carries them into your home) would make each side stronger. The idea was that the pipes would always have something to sell, and the content would always have a guaranteed way to reach homes. Now, I am leaving a lot out, but this was the entire “convergence” strategy in a nutshell.

Today, Comcast effectively admitted the synergies never showed up.

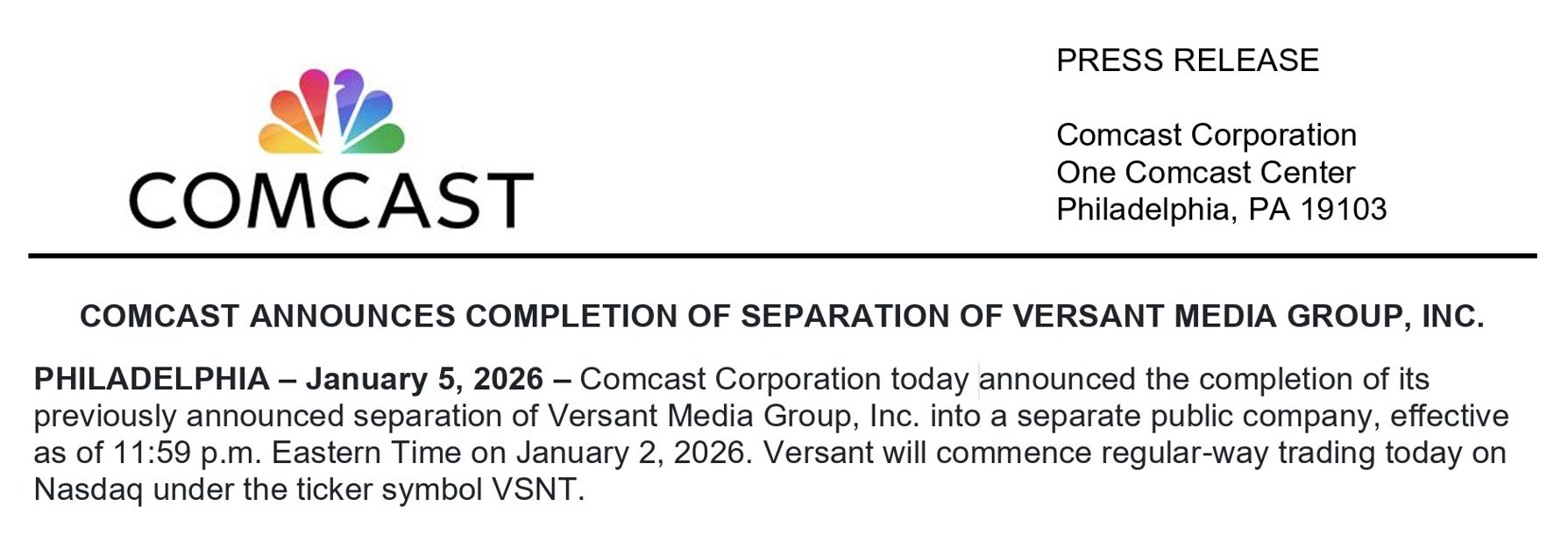

To see how sharp the reversal is, rewind just seven months. Back in December 2025, Comcast spun off Versant Media, which was a hodgepodge of assets but consisted mostly of its weakest and fastest-shrinking cable networks. (Please see the Accrued Interest archives for my extensive coverage on Versant - Underperform.)

The pitch at the time leaned on the idea that what stayed behind inside NBCUniversal — the theme parks, the studios, Peacock, the NBC network — were the crown jewels, and that they were better attached to Comcast’s broadband cash machine.

Seven months later, the good stuff is being shown the door. You cannot defend “content and distribution belong together” for fifteen years, reaffirm it in December, and then quietly reverse it in June without investors noticing the whiplash.

2. The Two Spin-offs Were Always One Plan

Here is how I read the sequence: the Versant spin and this NBCUniversal spin were never two separate decisions. They were one decision, executed in two stages. First you clear out the assets nobody wants to own — the melting-ice-cube cable networks — and package them into Versant. Then, once the portfolio is clean, you cut loose the genuinely valuable media assets so the market can price them on their own merits. I think of the Versant spin-off back in December almost like a garage sale, whereas the NBCUniversal spin-off news in June is more like an estate sale.

So why would Comcast bother splitting at all? Because of something called the conglomerate discount. In plain terms: when one company owns a grab-bag of very different businesses, the stock market often values the whole thing at less than the pieces would fetch separately. An investor who wants a clean, growing broadband stock doesn’t also want a shrinking-TV business stapled to it, and an investor who wants media exposure doesn’t want it watered down by a capital-heavy utility. So the good business gets dragged down by association with the weaker ones, and the share price reflects the muddle. Splitting them up is how you make that discount disappear.

Marci Ryvicker leading IR over at Comcast is something I want to call out. When you hand investor strategy to one of the most respected former sell-side TMT analysts on the Street, that’s worth noting. This is a decision made by people who know exactly how investors value a high-margin theme-park business versus a declining cable channel versus a broadband utility, and who concluded the parts are worth more than the whole.

3. The Real Prize Is the Pipes, Not the Pictures

Here is the part I think a lot of the media-focused coverage will underweight today: for many investors, the most important company created by this deal is the one keeping the Comcast name.

The tape tells the story. Here is roughly where the relevant names sat in mid-afternoon trading on June 29, 2026 (sorted from biggest winner to biggest loser):

Comcast (CMCSA): $24.63, +6.3%

Charter (CHTR): $146.03, +9.3%

S&P 500: 7,435.97, +1.1%

Versant (VSNT): $36.12, −0.1% (essentially flat)

Verizon (VZ): $43.71, −6.1%

AT&T (T): $21.70, −4.5%

T-Mobile (TMUS): $175.25, −4.1%

A few things stand out. Comcast jumped on the news, though it gave back a good chunk of its gains after gapping up toward $27 at the open. Charter rose sharply on M&A speculation, with traders betting a streamlined Comcast might finally try to roll up the rest of the cable industry. The other carriers — Verizon, AT&T, and T-Mobile — fell on the opposite fear: that a leaner, more focused Comcast means tougher competition ahead in broadband and wireless. And Versant actually slipped, slightly underperforming an S&P 500 that was up about 1% on the day. It’s a small move, but a telling one — it says the market doesn’t see this separation helping Versant’s investment case, exactly as I’ve argued.

4. A Leaner Comcast Is a Bigger Threat to the Phone Companies

The reason the wireless carriers sold off is just as revealing as Comcast’s pop.

Some background: for the last couple of years, Verizon and T-Mobile have been quietly peeling home-internet customers away from cable using something called fixed wireless access — internet delivered over the same cellular network that powers your phone, instead of through a cable wire. It’s cheap to roll out and it’s been a genuine headache for cable.

Now picture a slimmer Comcast that is no longer funneling billions into an expensive Hollywood arm. All that freed-up cash can go toward fighting back. That is precisely the threat the market is pricing this afternoon — a more focused, better-funded Comcast.

A caveat: on Accrued Interest I don’t really cover the telecom names (Verizon, AT&T, T-Mobile, etc.), nor am I staking out a view for or against any of them. What I’m describing is how Mr. Market is reading the news this afternoon: that a leaner, better-funded Comcast could compete harder against the telcos.

5. NBCUniversal Comes Out a Predator, Not Prey

This is where the deal structure gets genuinely interesting, and where I think the smart money will spend the next two years.

If you spin a business off tax-free and then it gets acquired within two years, the IRS assumes you secretly planned to sell it all along — and hits the parent company with an enormous tax bill. So in practice, nobody can simply buy NBCUniversal outright until roughly 2029.

But that rule does not stop NBCUniversal from being the buyer, so long as NBCU ends up owning more than 50% of whatever it merges with. So post-spin, NBCU should have a (relatively) clean balance sheet, freshly minted stock to use as currency, and the freedom to go shopping from a position of strength — unburdened by the declining cable networks already carved out into Versant.

And it isn’t only about outright acquisitions — the spin-off also frees NBCU to strike creative partnerships and joint ventures. There are more media “free agents” floating around than ever — companies that have been spun off, broken up, or quietly put on the block. The flexibility to work more closely with companies such as the newly combined Paramount/WBD is exactly what this structure is built to enable.

On the perennial Netflix chatter: I continue to take Netflix at its word that it isn’t interested in big legacy-media deals. Warner Bros. Discovery was the real wild card, which PSKY bid aggressively to win. While PSKY may eventually need to sell assets to pay down its heavy debt load, I wouldn’t expect NBCU to rush into buying more linear networks the moment it becomes independent from Comcast.

6. Don’t Bet on a Comcast–Charter Merger

Charter ripping more than 9% today tells you that some traders were already dreaming about a streamlined Comcast rolling up the rest of the cable industry. Let me pump the brakes.

Now, while I am no antitrust expert, a Comcast–Charter combo would bring together two of the largest internet providers in the country. And that would mean a brutal antitrust fight in Washington that I think would be difficult to overcome. On top of that, the bigger these companies get, the less extra savings they actually squeeze out of merging, so the M&A synergies shrink even as the regulatory risk grows. And Charter already has its hands full digesting its combination with Cox. The new structure gives Comcast the flexibility to do a big deal if sentiment shifts, but near-term I would not expect an imminent acquisition. And to be clear, this isn’t me starting coverage on Charter — I’m simply explaining why I wouldn’t chase today’s pop on merger speculation alone.

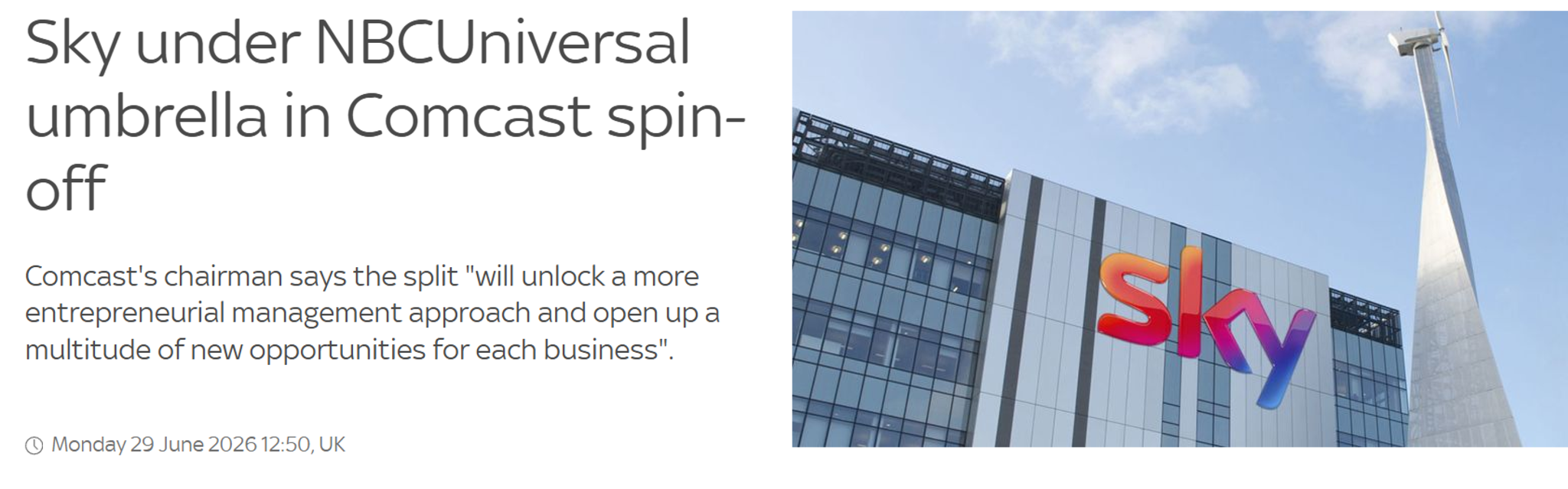

7. Sky Gives NBCUniversal the European Footprint It Lacks

Sending Sky — the European pay-TV and media business — off with NBCUniversal rather than keeping it inside Comcast may have confused some people, but let me explain why it makes sense for two reasons.

The first is housekeeping: a European pay-TV operator has no place inside a clean, domestic U.S. broadband utility; it would muddy the exact story this whole deal is engineered to tell. The second, and more important, is that Sky helps give NBCU a presence in Europe. As a media company, NBCUniversal has very little footprint across the Atlantic on its own. Sky brings roughly 17–18 million existing customer relationships across the UK, Germany, and Italy, plus the billing systems and distribution pipes to reach them. That hands a standalone NBCUniversal an established on-ramp to put Universal’s movies and its streaming content in front of European audiences, without having to build a customer base from scratch. The launch of SNL UK on Sky was an early taste of this. For a media company that needs international scale to stay relevant, Sky is the European foothold NBCUniversal couldn’t build on its own.

8. “Stronger Apart” Doesn’t Add Up for the Media Side

The Comcast spin-off deck today claims both companies will be stronger apart than together. For the broadband business, I buy it. But for NBCUniversal, I find it genuinely hard to believe.

A TV and media business carries enormous fixed costs; you pay for the shows and the sports rights whether 8 million or 10 million tune in. So when revenue dips a little, profit drops a lot (and the same works in reverse on the way up). Tucked inside Comcast, NBCUniversal had a giant broadband cash flow acting as a shock absorber. On its own, NBCU’s profits will be more volatile.

The clearest example of the potential dis-synergies is in sports. Bidding for the Olympics or the NFL packages is an arms race, and Big Tech has shown up with effectively bottomless pockets. Competing for those rights without Comcast’s balance sheet behind you is a much harder game. I’d expect NBCU to need creative partnerships just to stay at the table.

9. The Carriage Wars Are Coming — and Versant Is the Loser

There’s a quieter consequence here, and it loops back to Versant. Pay-TV distributors and the networks they carry renegotiate carriage fees every few years, often in tense standoffs. Right now, Comcast’s distribution arm and NBCUniversal’s networks are on the same side of that table; once they’re separate companies, those negotiations may turn cold and adversarial. I wouldn’t be surprised to see Comcast one day play hardball with both NBCUniversal and Versant.

To be clear, I don’t mean tomorrow. This won’t really come to a head until Comcast is fully separated from both companies, which realistically isn’t until after 2029. But once that happens, Comcast has no structural incentive to go easy on either one — especially as YouTube TV increasingly becomes the fastest-growing pay-TV distributor. That’s what makes me more bearish on the standalone Versant networks over the long run, not less. The VSNT networks were carved out precisely because nobody wanted them inside the new NBCUniversal, and eventually they’ll be negotiating carriage in a colder world. Tellingly, Versant’s own stock stayed basically flat while Comcast popped — a sign the market doesn’t see this separation as any kind of benefit for the VSNT channels Comcast already showed the door.

10. Disney Is Making the Opposite Bet — and I Think It’s Wrong

I can’t close the arguments without the strategic fork between Comcast and Disney.

The timing is almost poetic. Just as Comcast is breaking itself in two, the Wall Street Journal published a feature this past weekend on the new Disney CEO’s first 100 days in the job (Josh D’Amaro Is 100 Days Into His Mission to Make Disney Faster and Fiercer), and the throughline was the opposite instinct. D’Amaro is doubling down on keeping ESPN and Disney’s linear networks bundled inside the mothership, pushing back on the very calls to spin off ESPN that Comcast effectively just answered for its own assets. Two companies, staring at the same decline of traditional television, reaching opposite conclusions about what to do about it.

Comcast’s willingness to act this decisively makes me think Disney is on the wrong side of the trade. I’ve held an Underperform rating on Disney since Dec 2025, and if anything, today’s news adds to my conviction.

Conclusion

This is the most consequential TMT breakup in years, and a genuine inflection point for the industry. From here, I’ll be watching for the standalone NBCUniversal financials and more information about the spin-off. Zoom out, and the bigger story is that this deal drops another free agent into a rapidly changing media industry. A newly independent, well-capitalized NBCUniversal — free to buy, partner, and deal — sets up a great deal more strategic activity across media and telecom over the next few years. This is going to be one of the most fascinating things to watch.

For now, that’s my initial take. I’d love to hear yours. Let me know in the comments and thank you for subscribing and supporting my work!

Relevant tickers: CMCSA 0.00%↑, VSNT 0.00%↑, DIS 0.00%↑, PSKY 0.00%↑, WBD 0.00%↑, NFLX 0.00%↑, CHTR 0.00%↑

— Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.