Byron Allen's AMG Selling TV Stations: An Ominous Sign for Broadcast Media

Implications for Media Stocks Today

When I first heard that the Allen Media Group was looking to sell their entire portfolio of television stations, I immediately thought this was an ominous sign for the industry. It is never promising when one of the biggest cheerleaders of local TV over the last 20 years decides to exit entirely.

Earlier this week, the Hollywood Reporter announced that the Allen Media Group (AMG) “had hired the investment bank Moelis & Company to market its local stations…28 ABC, NBC, CBS and Fox affiliated stations in 21 markets”.

Because AMG is a privately held, I am not going to speculate about all the inner workings of the business. But I do know that for the last 5 years, AMG was very public with their desire to bid on the biggest media assets up for sale. If someone was selling - Allen made CERTAIN that everyone knew he was ready to buy, buy, buy.

BYRON IS BUYING

Here’s a short list of some of AMG’s many public offers from just the last 5 years:

Offered to acquire Tegna, reportedly for $8.5 billion including debt, with plans to combine his existing Entertainment Studios operation with Tegna stations.

February 2022 - Denver Broncos

Allen announced his intention to bid for the Denver Broncos NFL team, stating he was encouraged by NFL commissioner Roger Goodell and New England Patriots owner Robert Kraft.

April 2023 – Paramount Global ($PARA) – 1st Offer (Not public)

In April 2023, AMG had submitted an offer to buy Paramount to the company’s board. This offer was not made public however, until AMG’s second attempt to buy Paramount in Jan 2024 (see below).

September 2023 - ABC TV network, local stations, FX, and National Geographic

Allen shared publicly that he sent a text message to Disney CEO Bob Iger with an unsolicited $10 billion offer for the above assets.

November 2023 - E.W. Scripps Co. television stations ($SSP)

AMG had tried to line up funding to make a bid for several E.W. Scripps Co. television stations.

January 2024 - Paramount Global ($PARA) – 2nd Offer

Made a $14.3 billion bid (total value including debt of $30 billion) to buy all outstanding shares of Paramount Global. It was during this 2nd attempt that AMG disclosed the previously unreported April 2023 offer.

Fast forward to June 2025 - here was AMG’s statement…

“Six years ago, Allen Media Group began the process of investing over one billion dollars to acquire big four network-affiliated television stations. We have received numerous inquiries and written offers for most of our television stations and now is the time to explore getting a return on this phenomenal investment,” said AMG founder and CEO Byron Allen. “We are going to use this opportunity to take a serious look at the offers, and the sale proceeds will be used to significantly reduce our debt.”

Here is what I think it means for broadcast and media stocks generally.

LESSONS LEARNED

Part of my research process when I evaluate companies is to look at both their public AND private market comparables (comps). Oftentimes actions taken by the PRIVATE companies foreshadow what is ultimately going to happen to their PUBLIC counterparts.

A lesson I learned when working on my Tribune pitch that won the Ira Sohn Investment Idea Contest back in 2013, was that you can make a lot of money in the stock market when you notice that the private and public entities for a particular asset class are being valued differently.

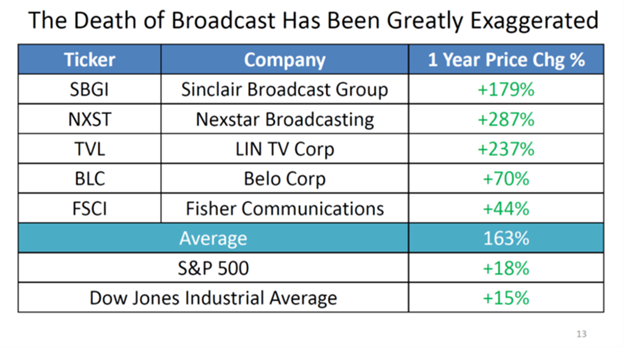

During the early 2010s, broadcast television stocks were strongly outperforming the market. This chart below from my presentation (MAY 2013) shows that many were up over 40%, 50%, even 100% over the trailing 12 months.

What I noticed back then, was that when there were more companies looking to BUY than there were willing SELLERS. That inevitably pushed the entire group higher.

Most of the time, investing is complicated, but in rare instances it is amazingly simple. See the LTM chart below from May 2013.

The entire sector was trading higher due to M&A activity, as both public and private operators were “rolling up” the space.

For those unfamiliar with the jargon of “Compounder Bros,”, a "roll-up" strategy involves acquiring and merging multiple smaller companies within the same fragmented industry to form a larger, more competitive entity.

Broadcast television had qualities conducive to successful roll-ups. While the editorial voice of a channel may vary greatly, the back-office operations are virtually identical whether you are operating an affiliate of ABC, NBC, CBS or Fox. Fueled by a powerful tailwind of low-cost debt, there was a buying spree. The only question was which entity would be the acquirer or the target.

CONCLUSION

Fast forward to June 2025…. the broadcast industry is mostly consolidated, at least among the public market names. $NXST (see my coverage here), $SBGI and $TNGA are the biggest remaining public companies, along with a handful of smaller ones.

What is different this time, is that there are fewer bidders for these companies. Private equity mathematically won’t be able to bid as aggressively due to the higher cost of debt. Weak institutional interest in TV stocks also means PE can’t count on a strong IPO market to sell back those companies 5-7 years later to return capital to their investors.

In my piece on Nexstar, I explained how I was afraid the company was going to take on the risk of buying more TV stations, without any exit plan if the TV ecosystem continued to decline. I said, “I am bearish on Nexstar specifically, because after the next wave of M&A is over, they will have no one left to sell to”.

If even Bryon Allen is not buying, who is the marginal buyer for these assets? This only adds to my conviction that broadcast stocks will continue to underperform the S&P 500.

-Accrued Interest

I’m guessing Moelis is there on a dual mandate, and asset sales aren’t the primary focus (LME and/or restructuring is). They have to deal with a maturity wall in early 2027, and the market is telling them they’re gonna have a hard time - term loan is in the 60s, bonds in the 30s.

But your broader point stands. Byron has always been willing to at least pretend to try to bid for things (even if he didn’t have the coin to do it) so this is a pretty marked shift in his outward posturing. Perhaps placating his creditors is the priority now, but perhaps it’s just much harder to continue his usual spiel with a straight face.

Hi Simeon, appreciate your insight. This isn’t an industry I have much knowledge of but my question is even though broadcast is a declining business isnt it possible that these major companies left shift from acquirers to capital managers/cash cows that just distribute whatever cash flow they have? I feel like this was the story for old businesses like newspapers etc but the NYT for example is has performed well over the past 5 years +33% and distributing cash back to shareholders in the form of dividends to the tune of $359 million over those five years.

I guess my question is can these broadcast companies accomplish this sort of capital allocation and management in the future?