AppLovin ($APP) Down -44% YTD: Fear vs. Fundamentals

Why the "AI Disruption" narrative is overstated and how the buyback machine sets a floor.

Accrued Interest TL/DR: APP 0.00%↑ has crashed -44% YTD on fears of AI disruption and “whispers” of a mixed e-commerce launch. I believe the panic is overstated. In this note, we debunk the bearish narratives, explain why the “slow” e-commerce rollout is a feature (not a bug), and highlight why the massive buyback authorization begins to put a floor under the stock at less than ~25x ‘26 earnings. I am fine looking foolish in the short-term, if it means more gains long-term. Come back for the full Q4-25 report next week.

Introduction

AppLovin reports Q4-25 earnings next Wednesday, Feb 11 (5:00 PM ET). While I normally wait for the print to publish, the noise has gotten loud enough that I want to share some thoughts with subscribers now.

I am putting this under “Stock Market Commentary” because I want to do more quick reactions for subscribers dealing with big market moves. I think the fall in AppLovin justifies a clarification post. The stock is no stranger to rumors—see my archives for my coverage of past short-seller attacks on AppLovin in 2025.

There are plenty of rumors, but the sell-off comes down to a handful of main narratives:

AI Disruption Fears: Renewed anxiety about ad-tech and gaming displacement.

E-Commerce “Whispers”: Private reports circulating that the Q1 e-commerce launch has been mixed.

(Note: These concerns are more legitimate than the salacious short reports from last year, but selling a stock before the company reports in 6 days seems crazy to me).

At Accrued Interest, my edge is time horizon. Let us block out the noise and look at the facts.

1. The Bear Case: AI Disruption (CloudX & Genie)

The market hates uncertainty, and right now, “AI” is being used as a boogeyman to scare investors out of ad-tech positions.

In a note published yesterday, Morgan Stanley highlighted three key investor concerns driving the de-rating: the launch of CloudX, a renewed push by Meta into the space, and the emergence of “World Models” like Google’s Genie.

The fear regarding CloudX is that its new AI-agent-based mediation platform could commoditize the stack. CloudX recently hit General Availability with plans to “rewire the mobile ad stack,” effectively promising to cut out intermediaries.

Simultaneously, the release of Google’s Genie (a generative AI model for creating playable worlds) has investors worried that the barrier to entry for creating games will drop to zero, potentially flooding the market or disrupting the current user acquisition (UA) dynamics that AppLovin dominates.

My Take:

The market is pricing in “disruption” without analyzing the second-order effects. Just because a new tool exists (CloudX) does not mean it instantly displaces a massive, entrenched liquidity pool like AXON.

Morgan Stanley itself acknowledges that while these are “real concerns,” the launch of CloudX’s mediation is “misunderstood and only a minor competitive threat.” Furthermore, while they see Meta’s potential push as a genuine concern, they admit there is “limited evidence that a push is coming in the near term.”

In fact, Morgan Stanley argues that “none of these concerns are idiosyncratic to APP” and that the “magnitude of the derating may be creating an opportunity similar to APP’s selloff to $219 in April 25.”

2. The Bear Case: E-Commerce “Whispers”

The second weight on the stock is the rumor mill regarding the e-commerce pilot. Morgan Stanley noted that while the opportunity to re-enter the ~$80bn in-app ad market is a “clear call option,” there is anxiety that the initial rollout has been slower than the hyper-bulls wanted.

Most worrying, there are reports being shared around by investors claiming some advertisers reported “mixed” results on their e-commerce experience. And yet again for AppLovin, there are rumors that some ad buyers have identified fraudulent ads.

First, let me remind everyone that a lot of the rumors that stem from AppLovin come from folks who are not familiar with how the digital ad space operates.

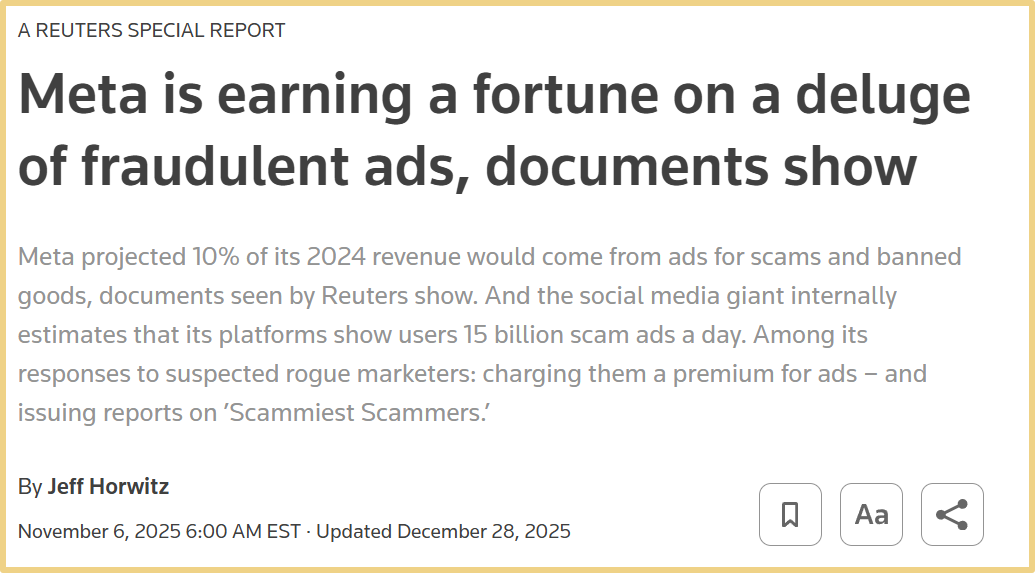

As a reminder, Meta has faced similar issues on a much larger scale. In November 2025, Reuters published a report titled “Meta is earning a fortune on a deluge of fraudulent ads, documents show,” revealing that internal documents estimated 10% of Meta’s revenue came from ads for scams and illicit goods.

That has not impacted their revenue growth at all—as we can see that Meta is still finding ways to grow +20% YoY despite their gargantuan size.

Now, it is important to stop fraud on the platform! And the good news is that this is exactly the strategy that CEO Adam Foroughi laid out clearly back in August.

During the Q2 2025 earnings call, when asked why they were limiting the onboarding of new customers, Foroughi was explicit:

“We want to make sure that we curate the marketplace. We want to make sure we weed out fraud. We want to make sure that the advertisers that come on are high quality... So we’re going to go slow to go fast.” — Adam Foroughi, Aug 6, 2025

If the “whisper” is that they are going slow, that is not a bug—it is a feature. They are deliberately weeding out the low-quality merchants to protect the ecosystem before opening the floodgates.

3. The Rebuttal: Why “Genie” is Bullish for AppLovin

I am not the only one scratching my head at the panic. Dom Davies, a sharp voice on ad-tech Twitter, posted a rebuttal yesterday regarding the Google Genie fears that I think hits the nail on the head.

It is worth noting that Dom Davies is a former Senior Manager of Business Development at AppLovin, having spent over 5 years at the company.

I have noticed a consistent pattern: AppLovin alumni are often some of the company’s strongest cheerleaders. These are not people with paid Substacks or large “Fintwit” accounts trying to pump the stock. But if you look carefully whenever there is an AppLovin sell-off, you will see former employees on social media stepping in to dispel rumors based on their deep understanding of the tech.

Davies pointed out that viewing generative AI game creation as a threat to AppLovin reveals a fundamental misunderstanding of the business model.

“Assuming Genie streamlines production for mobile games/ mobile apps, that only helps AppLovin. AppLovin’s business model is literally monetizing content - not making it. AppLovin really should’ve popped on the news of the Genie release - the product (in relation to AppLovin) is basically fuel for their network/platform to monetize.”

Exactly. If AI lowers the cost of content creation, we get more content, more apps, and more competition for attention. Who wins in a fragmented world? The company that owns the best monetization engine.

Valuation: The Floor is In

When there is a fierce debate around a stock, the best way to cut through the noise is to look at the valuation to see what is priced into the multiple. The key takeaway here is that AppLovin has sold off primarily due to multiple compression, not because analyst estimates have been slashed.

At Accrued Interest, my edge is having a longer time horizon than most investors. Let us block out the noise and look at the numbers.

The Setup at $374:

AppLovin has effectively round-tripped back to where it was six months ago. We know this stock is a “hedge fund hotel” prone to wild swings ($200 low / $745 high in the last 52 weeks).

But at $374, $APP is trading at ~25x 2026 GAAP P/E.

I would argue that at a market multiple, the bear case is already priced in. Even Morgan Stanley notes that with shares derated to ~15x ‘27 EBITDA, the stock is “priced for significant risks.”

The Valuation Floor (Buybacks):

If the stock stays here, expect the buyback machine to turn on.

Total 2025 Buybacks (Jan–Sep): ~$2.1B

Avg Price Paid: ~$376 (Basically today’s price)

FCF Conversion: They deployed nearly 100% of their ~$2.6B FCF into buybacks.

The Receipts:

Q1: $1.19B spent at $354 per share.

Q2: $341M spent at ~$368 per share.

Q3: $571M spent at ~$439 per share.

Management was aggressively buying shares at $439—15% higher than where we sit today. That signals to me that we are approaching a hard valuation floor.

And following the Q3-25 earnings in November, AppLovin’s board added an incremental $3.2 billion to their share repurchase authorization after they completed the previous $3 billion buyback that wrapped up in October.

The company has told Mr. Market many, many times they will use their free cash flow to reduce their share count before they go out and do value-destructive M&A.

CONCLUSION

Hold tight! I will do a full report on AppLovin after the Q4 earnings print next week, but this is a special company that is currently on sale due to overstated fears from many who still do not understand their business model.

Do not catch a falling knife if you are trading short-term options, but if you are an investor looking out 12–24 months, the risk/reward here is compelling.

-Accrued Interest

Relevant Tickers: APP 0.00%↑, GOOG 0.00%↑ GOOGL 0.00%↑, META 0.00%↑ , U 0.00%↑

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.

Pretty obvious that 'Project Genie' could be bullish for APP. It's almost as if algo's do the selling, not humans.

Awesome - thank you for the detailed and thoughtful response!