Accrued Interest Weekly Cypher: Apr-10-26

Vol. 2 - 2026

Welcome to Volume 2 of the Accrued Interest Weekly Cypher! Think of this as your “in-case-you-missed-it” digest for weekend catch-up, covering all the analysis and commentary I published this past week.

This week, I explored how CBS is trading cultural curation for passive rent collection, why OpenAI’s $100 billion ad revenue target looks like a financial modeling mirage, and how Meta’s new proprietary AI model validates my bullish thesis. Let’s cue the record drop and get into this week’s cypher for the week ending April 10, 2026.

Before I dive in, a quick reminder: much of Accrued Interest’s investment content will soon be moving behind a paywall. Please subscribe today to ensure you don’t miss out on my ongoing TMT stock analysis, media industry commentary, and deep-dive financial breakdowns.

CBS Abandons Late-Night Ambition for Rent Collection

CBS deciding to lease Stephen Colbert’s old 11:35 p.m. slot to Byron Allen’s Allen Media Group shows some incredibly small thinking. Instead of investing in original programming to grow their audience, CBS has opted to play the role of a passive landlord. They are handing over premium late-night real estate to an operator who is simultaneously selling off his own local broadcast stations just to manage distressed debt. To me, this signals a total lack of creative ambition.

Starting May 22nd, Byron Allen will fill the 11:35 p.m. slot on CBS with syndicated episodes of Comics Unleashed.

CBS is exchanging the role of cultural curator for passive rent collection through a time buy.

Leasing to a smaller, independent entity like Allen Media Group indicates the perceived low value of this premium asset by larger tech or media companies.

Allen Media Group is actively selling off its own local TV stations to pay down distressed debt, highlighting the broader struggles of the broadcast model.

The Netflix Algorithm: Media’s Ultimate Kingmaker

Netflix is pulling off a brilliant move by bringing the YouTube sensation Danny Go! onto its platform non-exclusively. The streaming giant is leveraging its massive distribution power—specifically, that highly coveted home page—to expose proven, de-risked content to a huge, passive audience of parents. Furthermore, launching the curated, ad-free Playground app for kids shows exactly how Netflix is actively building an interactive moat. They are securing an ecosystem that parents simply won’t be able to afford to cancel.

Netflix added the popular live-action children’s series Danny Go! to its lineup, though it remains available for free on YouTube.

This non-exclusive licensing play leverages Netflix’s algorithmic distribution engine to expose the property to parents who might not actively search for it on other platforms.

Netflix is also launching a curated, ad-free app called Netflix Playground featuring interactive games for children aged 8 and under.

Unlike CBS, Netflix is using its robust revenue to build permanent, multi-modal ecosystems and interactive moats.

Navigating the Fog of War: Fundamental Focus Over Geopolitical Panic

The market finally let out a collective sigh of relief following the two-week US-Iran ceasefire, which lifted a massive geopolitical overhang. While the extreme tail risk of nuclear war seems to be off the table, I want to remind investors that pointless conflicts still exact a heavy toll on global energy prices. I’m using this recent drop in volatility as an opportunity to remind you to stay honest about what you don’t know. Let’s focus on what consumers actually do with their money, rather than getting distracted by fleeting relief rallies.

The S&P 500 experienced a total year-to-date intraday drawdown of -7.72% amidst peak uncertainty on March 30, 2026.

De-escalation hopes and the provisional truce helped the market recover, effectively cutting its YTD loss to roughly -3.3% by April 7. As of April 10th, the S&P has rebounded further and is basically FLAT YTD.

Despite higher prices stinging, the American consumer remains wealthy and continues to spend.

This macro pause is the ideal window to identify fundamentally mispriced assets instead of trading the news cycle.

I will be more bullish going forward.

Deep Dive with Rigatoni Capital: Structural Shifts in Media & Ad-Tech

I had a fantastic time joining the Rigatoni Capital podcast recently to get into the weeds on the structural shifts reshaping the media and ad-tech landscapes. During the interview, I decoded the market’s current misunderstandings surrounding Meta’s CapEx panic, Netflix’s hidden catalysts, and the compounding earnings engine underlying AppLovin. It was a great opportunity to lay out my variant perceptions on these major players. You can see the interview above on YouTube.

The MCU Fallacy: Why Movie Hits Don’t Guarantee Nintendo’s Valuation

The Super Mario Galaxy Movie currently in theaters is an absolute smash hit, but I fear investors are getting a bit lazy by assuming a cool movie automatically equals a higher stock price for Nintendo. Some are also incorrectly assuming an unrealistic marketing bump from the films will magically correlate to massive game software sales. I think Nintendo is a fantastic company, but I need to be realistic about the business model. The stock currently trades at an earnings multiple that I candidly consider “fair”—neither particularly cheap nor overly expensive. In my recent article, I did some back-of-the-envelope math to show that even a top-tier cinematic success is pretty much immaterial to the company’s broader enterprise valuation.

Based on a standard studio ultimate profit model, a highly favorable 50/50 split of a $1.36 billion global gross yields Nintendo roughly $250 million in take-home profit.

This is a respectable, but not materially large boost to operating income, which is irregular and subject to a theatrical market that is clearly in secular decline.

Nintendo currently trades at roughly 21x 2027 GAAP EPS and 18x 2028, which I think are fair multiples for a gaming business. This is classic GARP (growth at a reasonable price).

Factors like the AI boom’s impact on component costs, tariff expenses, the post-COVID normalization of gaming trends, and the bootlegging of classic Nintendo games complicate earnings forecasting, in my opinion.

More to come on Nintendo…

Meta Protects its Margin-Driver with Muse Spark and CoreWeave

Meta’s stock saw a nice surge after the company unveiled its first natively multimodal AI model, “Muse Spark,” alongside a massive $21 billion cloud capacity deal with CoreWeave extending through 2032. By keeping Muse Spark strictly proprietary—a sharp departure from their open-source Llama heritage—Meta is sending a clear signal: AI is now a core margin-driver that must be fiercely protected. They have the sheer scale required to spread these massive infrastructure costs across billions of users, ultimately optimizing their core advertising machine.

Meta announced a $21 billion agreement with CoreWeave to secure AI cloud capacity through December 2032.

The highly compensated Meta Superintelligence Labs (MSL) team released the “Muse Spark” model.

Unlike previous models, Muse Spark is kept strictly proprietary to protect it as a core margin-driver.

Meta’s significant AI investments are actively boosting the profitability and efficiency of its core advertising business.

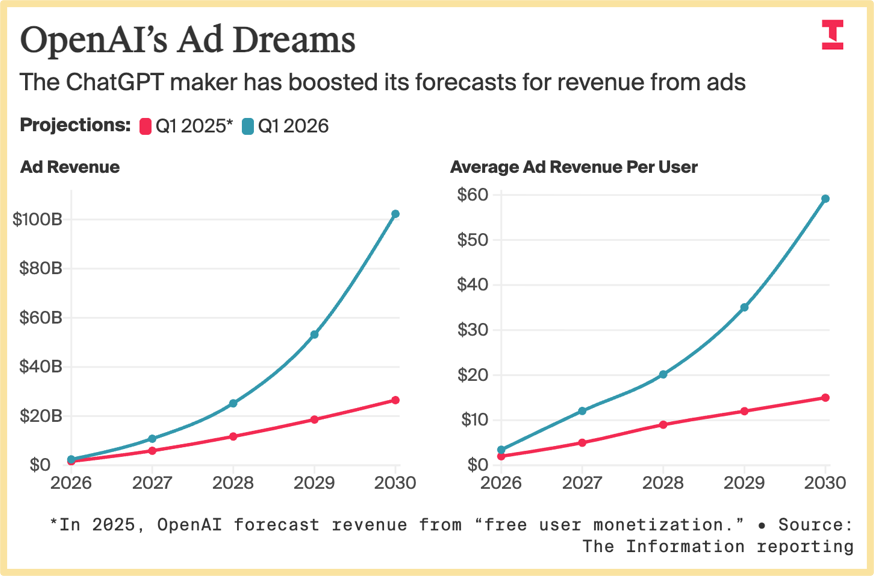

The Financial Mirage of OpenAI’s $100 Billion Ad Dreams

OpenAI is aggressively revising its internal forecasts higher, projecting that advertising revenue will hit over $102 billion by 2030 based on a global ARPU target of $60. Anyone with a corporate FP&A background recognizes this classic hockey-stick modeling maneuver immediately—it’s designed to justify an astronomical private valuation. To actually achieve this, OpenAI would have to match Meta’s highly-optimized, two-decade-old global monetization efficiency across lower-monetizing international regions, which is a massive stretch in my book.

OpenAI leadership projects ad revenue will leap from roughly $11 billion in the near term to over $102 billion by 2030.

This projection relies on generating a global average revenue per user (ARPU) of approximately $60 by 2030.

To reach this volume, OpenAI must scale heavily into the Asia-Pacific and “Rest of World” regions, where digital ad rates are much lower.

For comparison, Meta’s blended global ARPU in 2025 was just $57.03 across its massive, two-decade-old ecosystem.

Uber’s Asset-Light Approach to the Autonomous Future

While other tech giants are busy sinking billions into CapEx, Uber is quietly securing its future intrinsic value through strategic, asset-light partnerships. Their recent deal with MOIA (a Volkswagen Group company) to deploy autonomous “ID.Buzz” vehicles in LA by late 2026 illustrates this perfectly. Uber is positioning itself as the go-to “brain” handling the routing for the autonomous future, allowing them to pocket high-margin fees without taking on the depreciation nightmare of actually owning the physical fleet.

Uber partnered with Volkswagen Group’s MOIA to deploy autonomous “ID.Buzz” vehicles in Los Angeles by late 2026.

This capital-light strategy allows Uber to plug third-party robotaxis into its existing network without manufacturing or maintaining the fleet.

Uber is also expanding its AWS deal to run its complex ride-matching algorithms on Amazon’s custom Graviton4 and Trainium3 chips to lower backend infrastructure costs.

At $70 per share, Uber trades at an inexpensive 16x consensus 2027 GAAP EPS.

CONCLUSION

I want to send a huge THANK YOU to all the new readers and subscribers out there.

If you found any of my research helpful, please like and share so we can help grow the Accrued Interest community! I will continue to provide more tactical Daily Updates next week, alongside new stock deep dives to strip away the noise and provide the real-time signal that sophisticated readers demand.

-Accrued Interest

Disclaimer: The information presented in this Substack is for educational purposes and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

You can always reach me at simeon@accruedint.com.